VRBO insurance for owners protects your rental property investment from risks that standard homeowners policies won’t cover. Minnesota property owners face unique liability exposures when hosting short-term guests.

We at Variant Insurance Group see too many owners operating without proper coverage, leaving themselves vulnerable to costly claims. The right insurance strategy can mean the difference between profit and financial disaster.

What Insurance Requirements Do VRBO Owners Actually Need?

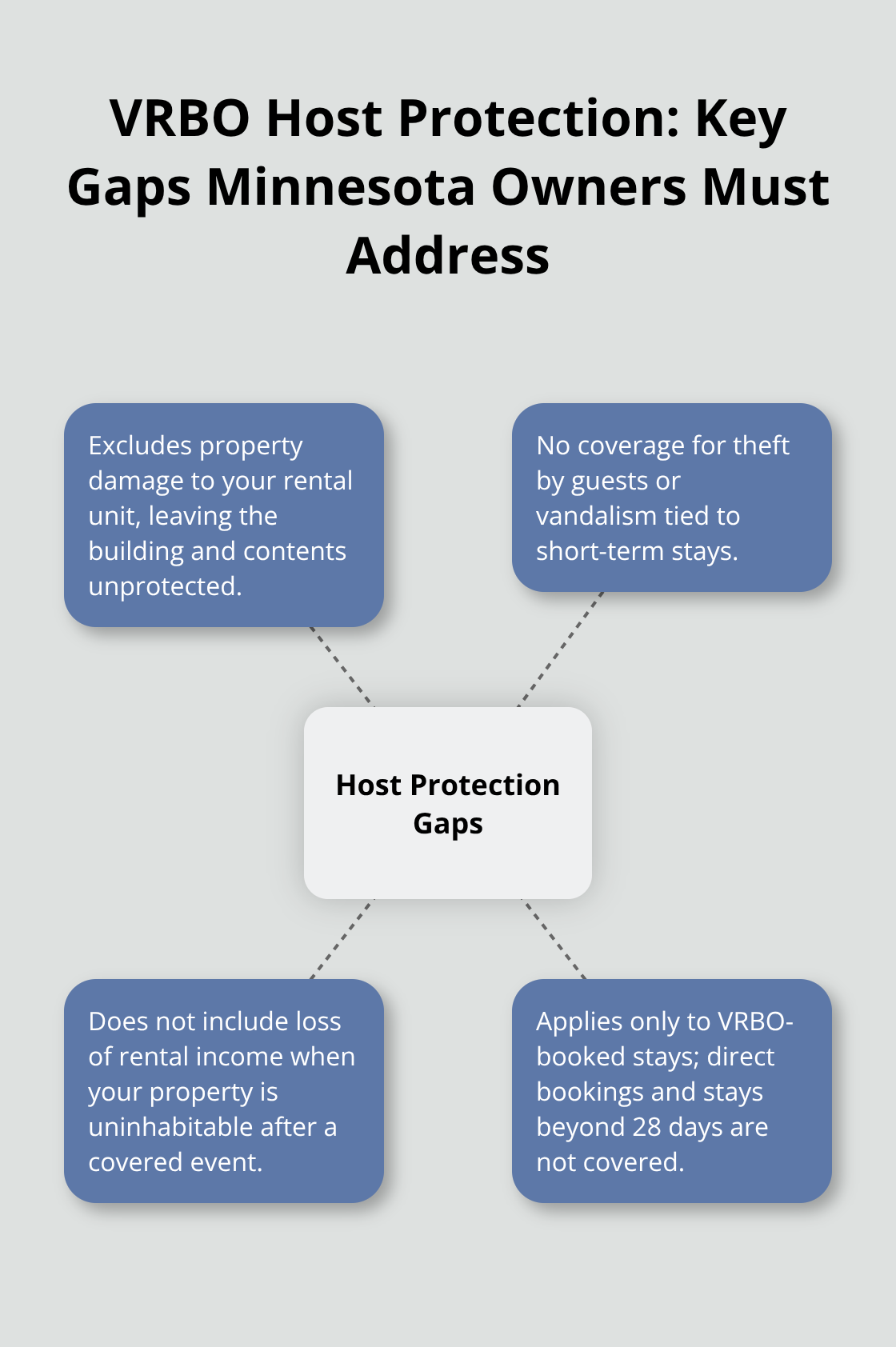

VRBO’s Host Protection Insurance provides only basic liability coverage up to $1 million per occurrence, but this platform-provided protection fails to meet what Minnesota property owners actually need. The coverage excludes property damage to your rental unit itself, theft by guests, and loss of rental income when your property becomes uninhabitable. Most critically, VRBO’s insurance only applies to bookings made through their platform, which leaves you completely exposed for direct bookings or extended stays beyond 28 days.

Standard Homeowners Policies Create Dangerous Coverage Gaps

Your existing homeowners insurance becomes void the moment you start charging guests for stays. Insurance companies classify short-term rentals as commercial activities, which standard residential policies explicitly exclude. This means fire damage, guest injuries, or theft incidents won’t receive coverage under your current policy. Minnesota’s aging rental housing stock compounds this risk, with older properties facing higher claim frequencies according to housing policy data. Property owners who continue operations under homeowners coverage face claim denials and potential policy cancellation.

Short-Term Rental Liability Exposures Demand Specialized Protection

Guest turnover in Minnesota short-term rentals has intensified liability risks, with average stays rising from 3.7 nights pre-pandemic to 4.4 nights currently. Higher occupancy rates create more potential for accidents involving amenities like hot tubs, pools, and outdoor equipment. Liquor liability represents another significant exposure that standard policies won’t touch. When guests consume alcohol and cause property damage or injure themselves, you bear financial responsibility without proper commercial coverage.

Weather-Related Risks Require Comprehensive Building Coverage

The frequency of severe weather events in Minnesota has led to rising storm damage claims, which makes comprehensive building coverage essential for rental property protection. You need a specialized form of insurance policy called Landlord Protection Insurance, also known as Vacation Rental Insurance. These specialized coverage types address the unique exposures that traditional policies ignore, setting the foundation for proper financial protection in your short-term rental business.

What Coverage Types Protect Your VRBO Investment

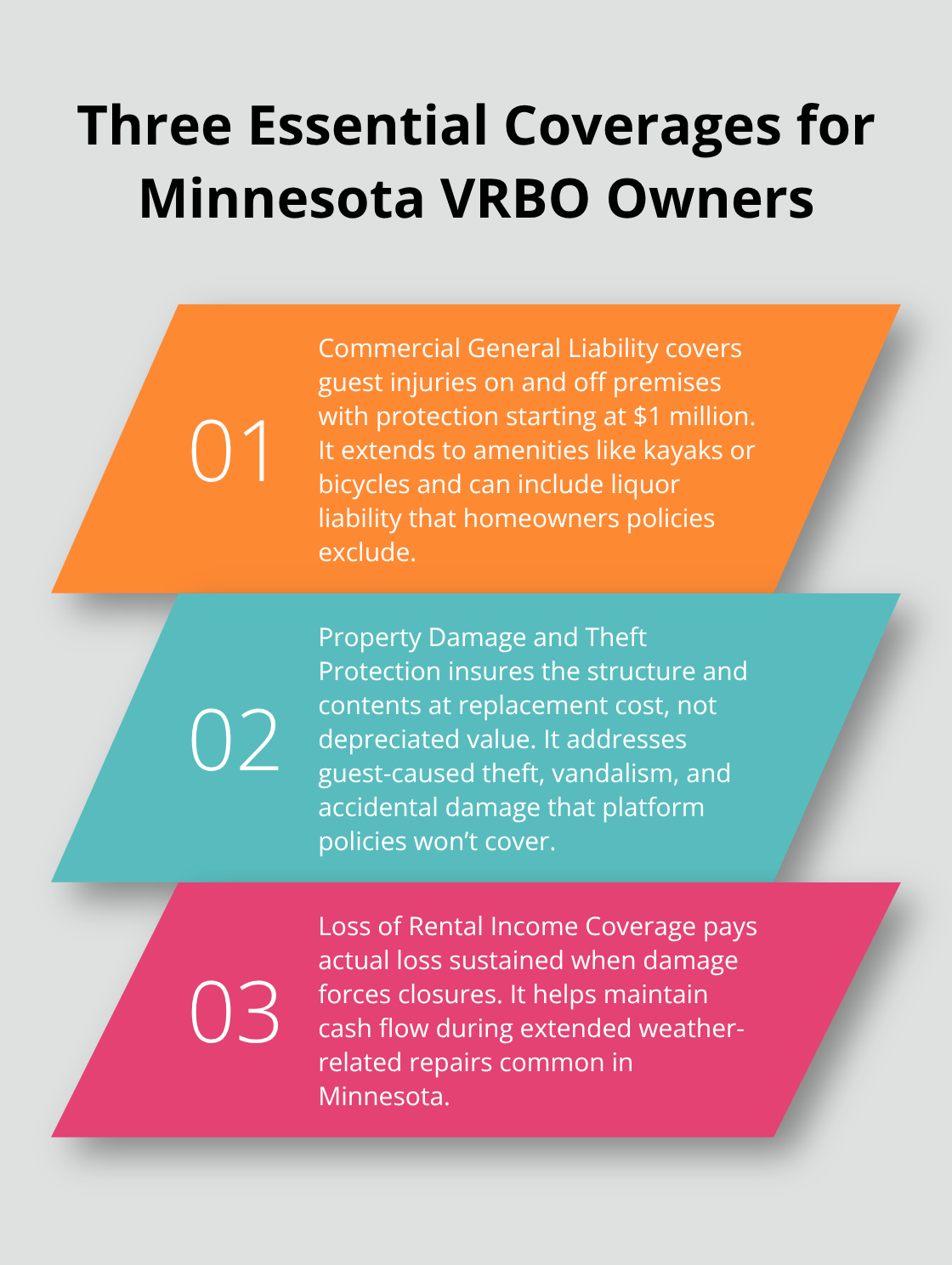

Commercial General Liability Insurance

Commercial General Liability Insurance forms the foundation of proper VRBO protection and provides $1 million in coverage for guest injuries that occur on your property. This coverage extends beyond your property boundaries and protects you when guests use amenities like kayaks or bicycles you provide. Minnesota’s specialized short-term rental policies include liquor liability protection, which standard homeowners insurance excludes entirely.

Property owners who operate hot tubs, pools, or fire pits face elevated liability exposures that require this commercial-grade protection. The frequency of guest turnover in Minnesota rentals increases accident probability and makes comprehensive liability coverage essential for financial protection.

Property Damage and Theft Protection

Property damage and theft protection covers your structure, contents, and guest-caused damages that platform insurance won’t touch. Specialized vacation rental policies provide replacement cost coverage for both the structure and personal property, which means you receive current market value for repairs rather than depreciated amounts.

Minnesota property owners should prioritize policies that cover guest-caused theft, vandalism, and accidental damage. These incidents occur frequently in short-term rental operations but receive no protection under standard homeowners coverage.

Loss of Rental Income Coverage

Loss of rental income coverage compensates you when covered damage makes your property uninhabitable and protects your cash flow during repair periods. This coverage typically provides actual loss sustained rather than arbitrary limits, which protects your revenue during extended repairs.

The coverage becomes particularly valuable when severe weather events (increasingly common in Minnesota) force extended property closures. Property owners who skip this protection face double financial hits: repair costs plus lost rental income that can stretch for months.

With these three coverage types in place, Minnesota VRBO owners need to select the right insurance provider who understands short-term rental risks and offers competitive rates.

Which Insurance Provider Should Minnesota VRBO Owners Choose

Specialized Short-Term Rental Insurers Outperform Traditional Carriers

Proper Insurance stands out as the preferred provider for comprehensive vacation rental coverage, endorsed by VRBO as their recommended insurance partner. Their policies replace traditional homeowner or landlord insurance entirely and eliminate double coverage issues while they provide seamless protection for all three property uses: rental guests, owner vacations, and vacant periods. Proper Insurance offers Commercial General Liability coverage that starts at $1 million and includes unique protections like Squatter Protection legal support and comprehensive bed bug coverage.

Their specialized underwriters provide unmatched property, business liability and lost revenue coverage for short-term rental hosts, including owners and arbitrageurs, with policies available in all 50 states that target frequent rental operations specifically.

Independent Agents Provide Superior Market Access and Custom Solutions

Independent agents give Minnesota property owners access to multiple specialized carriers rather than single-company limitations. Independent agents shop Minnesota’s top-rated insurance companies to find the perfect policy match for your specific property and rental operation. Independent agents can bundle short-term rental policies with umbrella liability coverage for cost savings and broader protection. They understand local regulations that affect Minnesota vacation rentals and can align coverage with state-specific requirements. Independent agents also provide policy reviews as your rental business evolves and adjust coverage limits and endorsements based on occupancy rates and property improvements.

Premium Costs Depend on Property Age, Location, and Coverage Limits

Minnesota’s rental housing stock significantly impacts premium calculations, with older properties facing higher risk assessments and increased costs. Property location affects rates based on severe weather frequency, crime statistics, and local claim histories. Coverage limits for liability, property damage, and loss of income directly influence premium amounts (with higher limits that provide better protection at proportionally lower per-dollar costs). Insurers also consider your property management practices, safety features, and guest procedures when they calculate rates. Property owners who invest in modernization projects and maintain detailed improvement records often qualify for reduced premiums through lower risk classifications.

Final Thoughts

VRBO insurance for owners requires three essential components: Commercial General Liability coverage that starts at $1 million, comprehensive property damage protection with replacement cost coverage, and loss of rental income protection for extended repair periods. Minnesota property owners cannot rely on standard homeowners policies or platform-provided coverage alone. Your next step involves consultation with an independent insurance agent who specializes in short-term rental coverage.

These professionals access multiple carriers and create custom solutions that traditional agents cannot match. They understand Minnesota’s specific regulations and weather-related risks that affect your property. Professional guidance delivers long-term savings through proper coverage selection and competitive rate comparison (while preventing costly coverage gaps through bundling and risk management improvements).

We at Variant Insurance Group shop Minnesota’s top-rated insurance companies to find the perfect policy match for your specific rental operation. Our experienced team reviews your options and compares protection levels to deliver the best possible value for your VRBO investment protection needs. Contact us today to secure comprehensive coverage that protects your rental property investment from the unique risks that Minnesota short-term rental owners face.