Handyman insurance cost varies dramatically depending on what services you offer and where you operate. At Variant Insurance Group, we’ve helped countless Minnesota handymen understand their coverage options and find affordable rates.

This breakdown walks you through the real numbers-what you’ll actually pay for general liability, tools coverage, and workers compensation insurance in Minnesota.

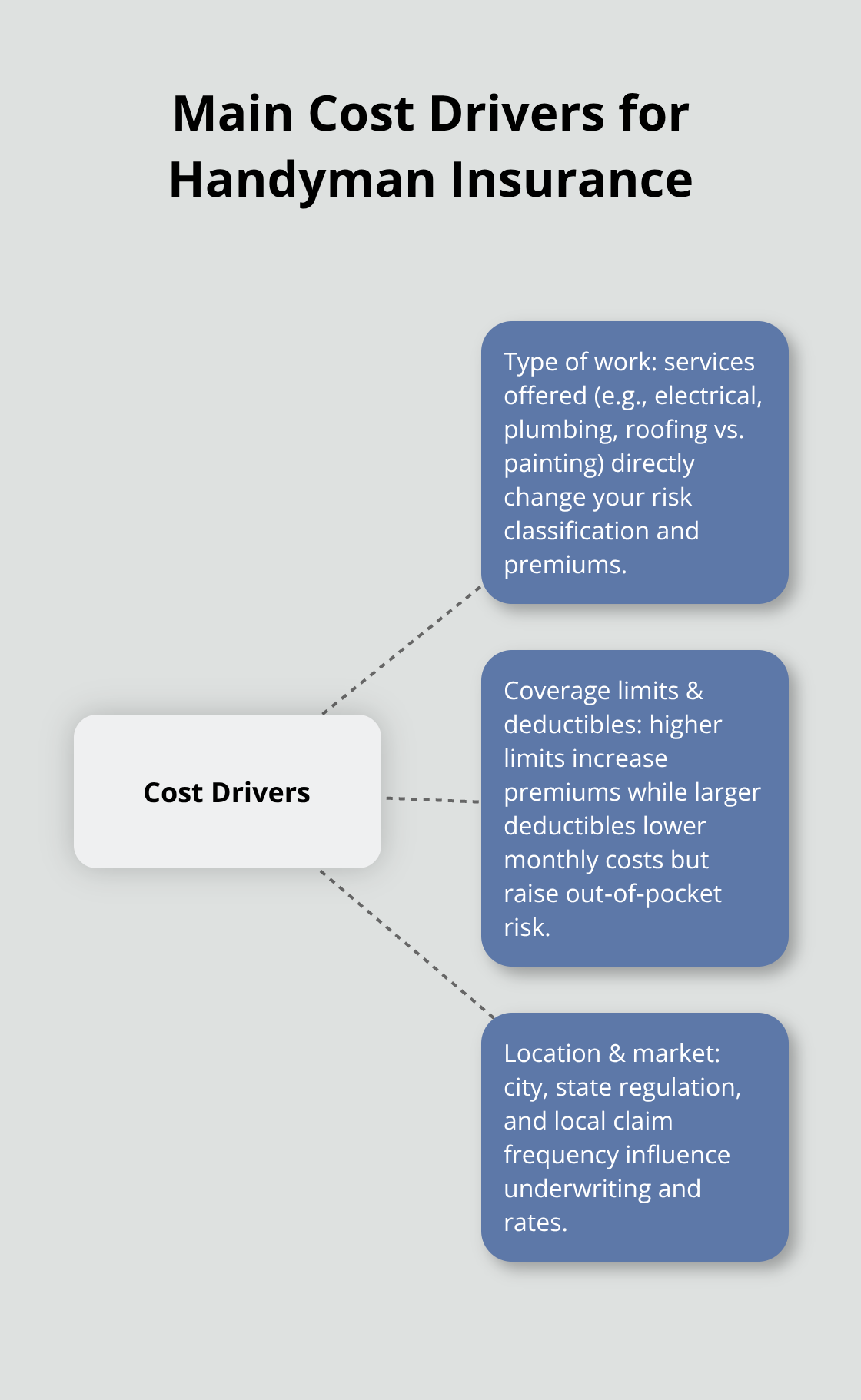

What Drives Your Handyman Insurance Costs

Your handyman insurance premium reflects specific factors that insurers evaluate with every quote. Understanding these drivers helps you control costs and avoid overpaying for coverage you don’t need.

Type of Work Determines Your Risk Category

The services you offer directly shape your premium. Basic repairs like fixing drywall or replacing fixtures cost less to insure than electrical work, plumbing, or roofing. Insurers classify electrical and plumbing as higher-risk services because mistakes can cause serious injuries or property damage. A handyman who advertises roofing services pays significantly more than one who focuses on interior painting and minor carpentry. The services you list on your contract influence your rate, so specificity prevents overpaying for unnecessary coverage or underpaying and facing claim denials later.

Coverage Limits and Deductibles Impact Monthly Costs

Your choice of coverage limits and deductibles dramatically affects what you pay each month. General liability coverage typically ranges from $300,000 to $1,000,000 per occurrence, with aggregate limits from $300,000 to $2,000,000. A $300,000 limit costs significantly less than a $1,000,000 limit, but many Minnesota clients now require $1,000,000 minimum coverage before hiring. Tools and equipment coverage limits commonly range from $3,000 to $10,000 per occurrence, and each additional dollar of coverage adds to your premium. Deductibles work in your favor when you absorb smaller losses yourself. The key involves balancing lower premiums against what you can actually afford to pay out of pocket after a claim. Minnesota handymen who understand this trade-off typically increase equipment deductibles while keeping general liability deductibles lower, since property damage claims happen more frequently than liability lawsuits.

Location and Market Variations Affect Rates

Where you operate in Minnesota affects your rates more than many handymen expect. General liability costs vary significantly by state, with Maine averaging $213 per month while New York reaches $286 per month. Within Minnesota, your specific city and surrounding area influence underwriting decisions because some regions have higher claim frequencies or more expensive repair costs. Workers compensation rates also shift based on state regulations and historical claim data. Maine averages $81 per month while Pennsylvania reaches $108 per month, reflecting how different states regulate this coverage. Professional liability insurance averages $54 per month nationwide but varies slightly by state. Business operations insurance for tools and equipment (inland marine) ranges from $311 per month in North Dakota to $423 per month in Louisiana. Your credit score, where state law allows its use, also affects pricing. An independent insurance agency that knows Minnesota’s specific market can identify which insurers offer the best rates for your particular location and service type, potentially saving you hundreds annually compared to online quotes that don’t account for local market variations.

Now that you understand what drives your costs, the actual numbers matter. Minnesota handymen need to know what they’ll realistically pay for general liability, tools coverage, and workers compensation in your state.

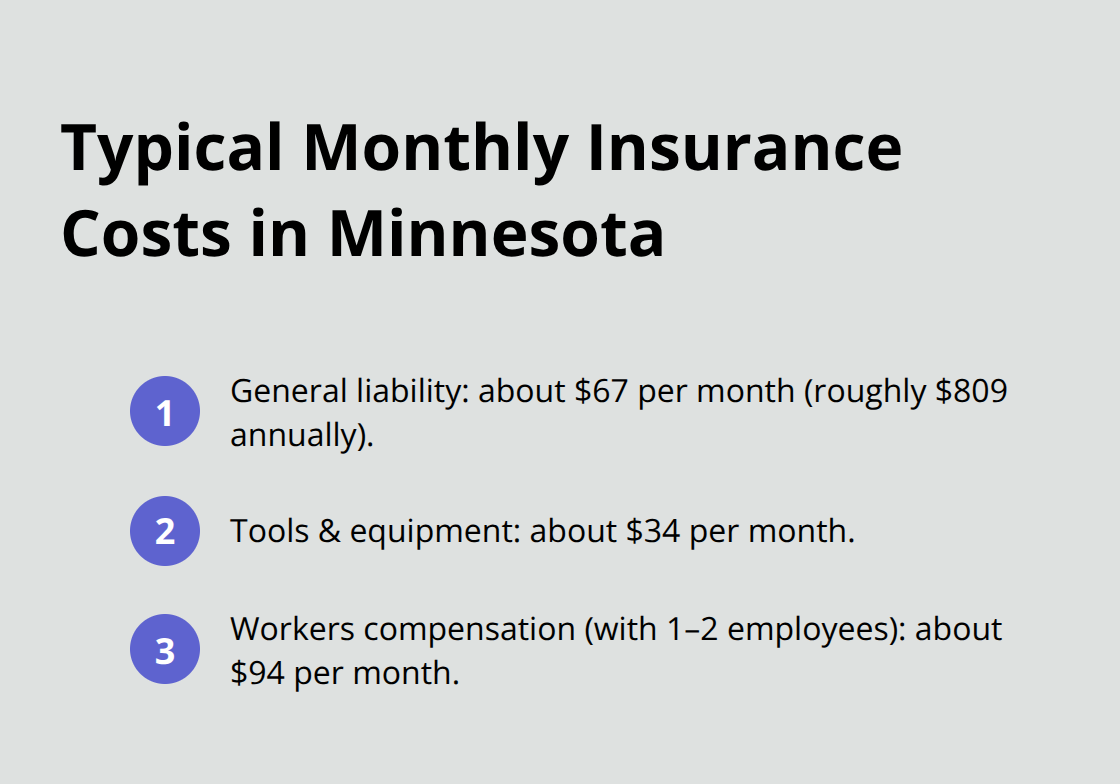

What Minnesota Handymen Actually Pay for Insurance

General Liability Costs Dominate Your Premium

General liability insurance represents your largest ongoing expense, and Minnesota rates reflect regional market conditions that differ significantly from national averages. A typical Minnesota handyman pays around $67 per month for general liability coverage, roughly $809 annually, according to industry data tracking active customer policies. This covers bodily injury and property damage claims up to your selected limit, usually $1,000,000 per occurrence with a $2,000,000 aggregate. However, your actual cost depends heavily on the specific services you advertise. A handyman focusing on interior painting and minor carpentry might pay $245 per month for general liability, while someone offering electrical work or roofing could easily exceed $300 monthly.

The deductible you choose matters tremendously here. Most Minnesota handymen select a $500 deductible for general liability since property damage claims occur relatively frequently, and paying a small deductible yourself keeps premiums reasonable. Increasing your deductible to $1,000 can reduce premiums by 10 to 15 percent, but this only makes sense if you can comfortably absorb that cost after a claim.

Tools and Equipment Protection Costs Less

Tools and equipment coverage costs significantly less than general liability but protects your most essential business assets. Minnesota handymen typically pay around $34 per month for tools and equipment insurance, with coverage limits ranging from $3,000 to $10,000 per occurrence depending on the package you select. This inland marine coverage protects your tools whether they sit in your truck, at a job site, or in your workshop, and it covers theft, damage, and loss.

The standard deductible for tools coverage runs $500, but here’s where you can save money strategically. Increasing your tools deductible to $1,500 can cut premiums by 15 to 22 percent without exposing you to unreasonable risk if you work primarily in lower-theft residential neighborhoods.

Workers Compensation Becomes Mandatory with Employees

Workers compensation insurance rounds out your core coverage and becomes mandatory the moment you hire your first employee under Minnesota law. A handyman with one or two employees typically pays $94 per month for workers compensation, translating to roughly $1,125 annually according to benchmark data. This coverage protects your employees’ medical expenses and lost wages if they sustain injuries on the job, and it shields you from lawsuits.

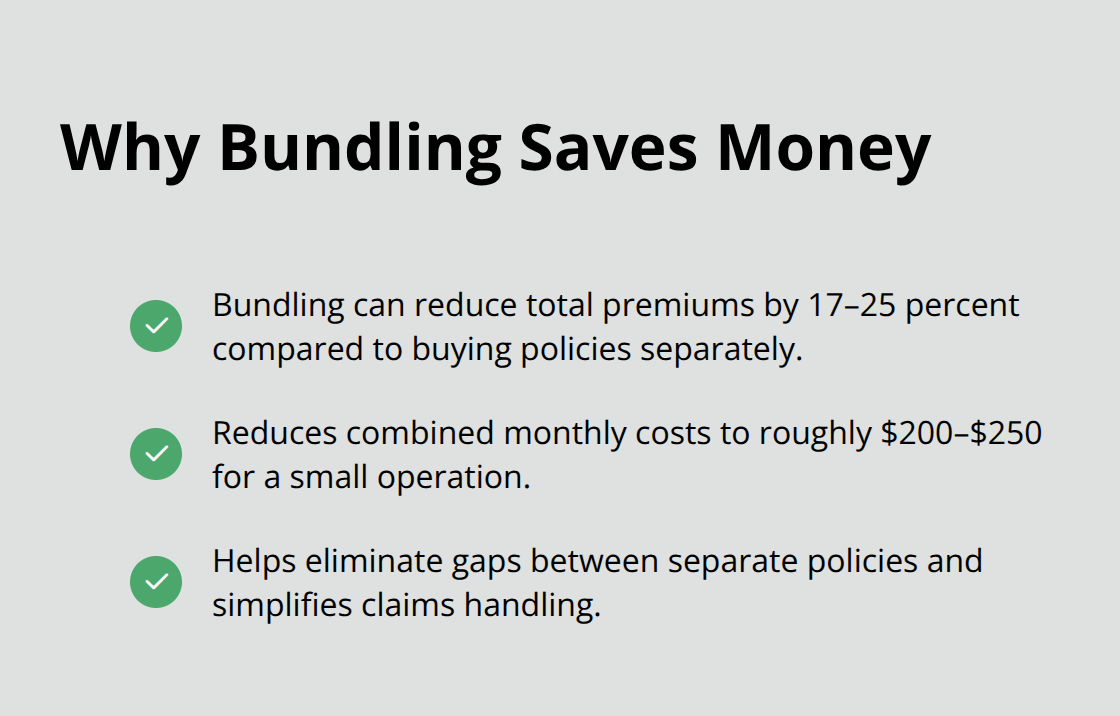

The cost per employee varies based on the specific work classification, with roofing and electrical work classified as higher-risk than general handyman services. Bundling general liability, tools coverage, and workers compensation together typically saves you 17 to 25 percent compared to purchasing each policy separately, bringing your total monthly cost down to approximately $200 to $250 for a basic package protecting a small operation.

Strategic Savings Through Smart Bundling

The real opportunity to control costs emerges when you bundle multiple policies. Most Minnesota handymen who compare quotes discover that purchasing general liability, tools coverage, and workers compensation as a package costs substantially less than buying each line separately. This bundling approach (sometimes called a business owners policy or BOP when it includes property coverage) aligns your protection with your budget while eliminating gaps that could leave you exposed.

Your next step involves understanding which specific cost-reduction strategies work best for your operation and service type. The methods that lower premiums for a roofing contractor differ from those that benefit a painting specialist, so tailoring your approach to your actual business model produces the biggest savings.

How to Cut Your Handyman Insurance Costs

Bundle Policies for Immediate Savings

Bundling policies delivers the most immediate savings for Minnesota handymen willing to consolidate coverage. When you purchase general liability, tools and equipment, and workers compensation together rather than separately, you typically save on total premiums. A handyman paying $245 monthly for general liability, $34 for tools coverage, and $94 for workers compensation separately ($373 total) could reduce that through bundling, freeing up money each month for other business expenses. Some insurers offer even steeper discounts when you add commercial property coverage or professional liability to the package.

The key involves comparing bundled quotes from multiple carriers rather than accepting the first offer, since bundling discounts vary significantly between insurers. Local independent agencies can shop Minnesota’s top-rated insurance companies to find which carrier offers the best bundled rate for your specific service type and location, sometimes uncovering savings that online quote systems miss entirely because they don’t account for local market variations and insurer-specific programs.

Increase Deductibles Strategically

Your deductible strategy determines whether you genuinely lower costs or simply appear to on paper. Increasing your tools and equipment deductible from $500 to $1,500 can cut that portion of your premium by 15 to 22 percent, translating to roughly $5 to $7 monthly savings on a $34 tools policy. However, this only works if you operate in a neighborhood where tool theft remains relatively rare and you maintain secure storage practices.

General liability deductibles should stay at $500 or lower since property damage claims occur frequently in handyman work, and absorbing a $1,000 deductible after damaging a customer’s kitchen cabinet quickly erases your premium savings. Many Minnesota handymen overlook the annual payment option, which saves 6 to 8 percent compared to monthly payments by eliminating processing fees. On a $2,800 annual premium, paying annually instead of monthly saves approximately $168 to $224 yearly.

Maximize Cumulative Savings

Combining bundling, strategic deductible increases, and annual payment processing produces cumulative savings that exceed 30 percent for well-positioned operations, though the exact reduction depends on your specific service type, claims history, and location within Minnesota.

Final Thoughts

Minnesota handymen who understand handyman insurance costs make smarter decisions about coverage and budgeting. Your premium depends on the services you offer, the coverage limits you select, your location within Minnesota, and the deductibles you absorb. General liability typically costs around $67 monthly, tools and equipment coverage runs approximately $34 monthly, and workers compensation averages $94 monthly for small operations with employees-bundling these policies together saves 17 to 25 percent compared to purchasing them separately.

Working with a local insurance agent transforms this process from overwhelming to straightforward. An independent agency shops Minnesota’s top-rated insurance companies rather than locking you into a single carrier’s rates and options. Local agents understand Minnesota’s specific market conditions, regional claim patterns, and which insurers offer the best rates for your particular service type and location, while strategic deductible increases and annual payment options add another 6 to 22 percent in savings depending on your situation.

Contact Variant Insurance Group to discuss your handyman business and coverage needs. Our team compares protection and prices across multiple carriers to find the right policy for your exact situation, and we work for you rather than a single company. Request quotes from at least three different insurers to compare rates and coverage options, then review each quote carefully before making your decision.