Commercial auto insurance quotes vary wildly depending on your vehicle, driving record, and how you use your fleet. At Variant Insurance Group, we’ve helped Minnesota business owners cut through the confusion and find rates that actually fit their budget.

The difference between a quote that breaks the bank and one that makes sense often comes down to knowing what insurers look for and how to shop strategically.

What Drives Your Commercial Auto Insurance Price

Vehicle Type and Usage Patterns

The cost of commercial auto insurance in Minnesota hinges on specifics about your vehicles and how your drivers use them. Insurers evaluate vehicle type first because a delivery van operating 40,000 miles annually carries far more risk than a service truck parked most days. Vehicles over 10,000 pounds trigger additional state and federal liability requirements beyond standard policies, which raises your baseline cost. The year, make, and model matter too-newer vehicles with advanced safety features and telematics systems typically qualify for lower premiums because they reduce accident frequency and theft risk. If your fleet includes hazardous materials transport, expect significantly higher rates due to regulatory exposure. Annual mileage is one of the most transparent cost drivers; a business logging 50,000 miles per year pays substantially more than one operating at 15,000 miles.

Driver Records and Age

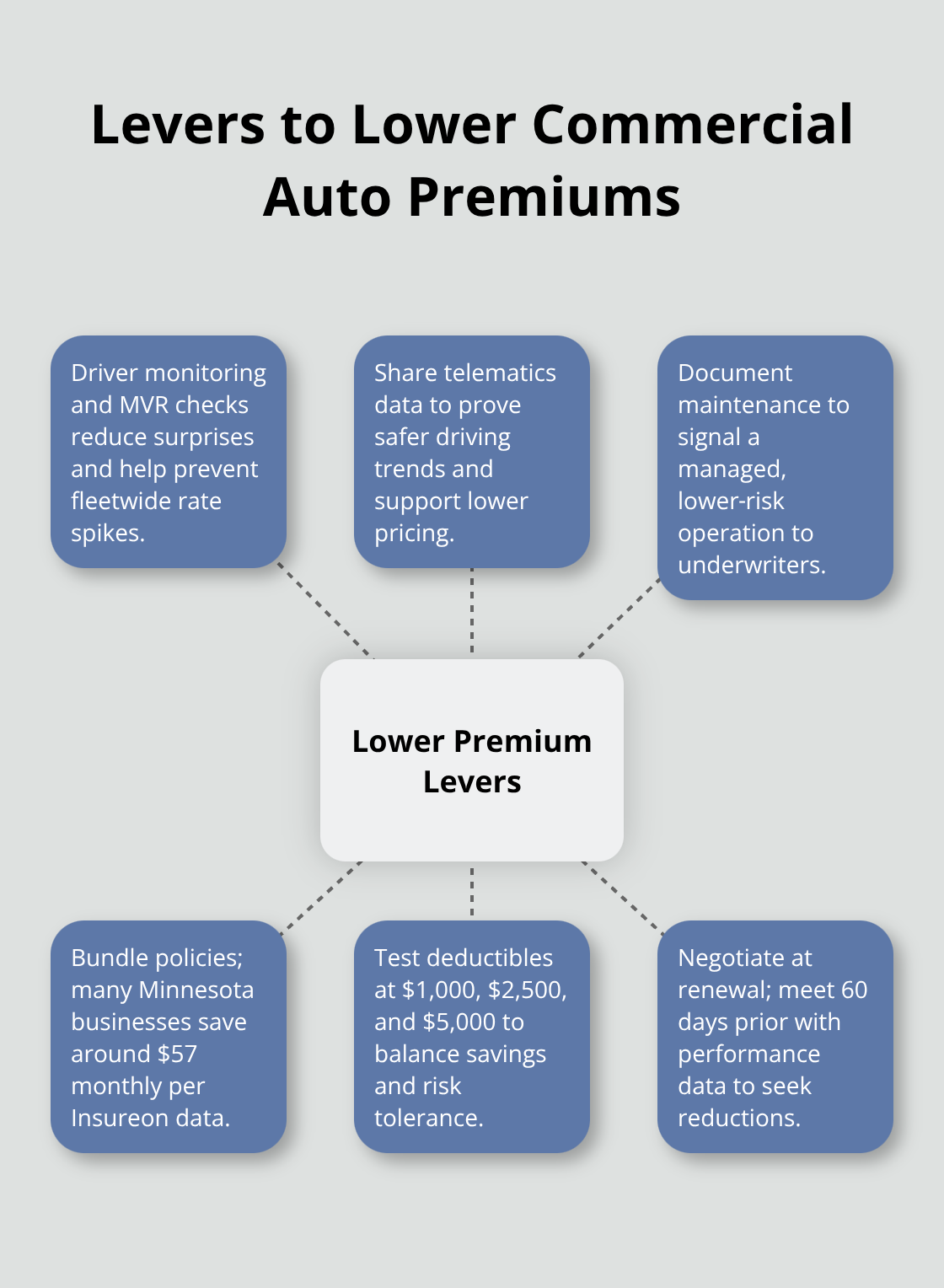

Your drivers’ records are equally critical. A single at-fault accident or moving violation on an employee’s license can increase your entire policy’s cost, which is why many Minnesota businesses now monitor driver behavior continuously using dashcams or in-cab cameras to document fault and identify distraction patterns before claims occur. Driver age creates predictable rate jumps. Operators between 18 and 25 face higher crash risk, so if your fleet relies on younger workers, targeted training programs become essential to offset premium increases. Clean driving records directly correlate with lower costs-maintain strict hiring standards and monitor license status regularly, updating your insurer immediately when violations occur.

Maintenance and Telematics Data

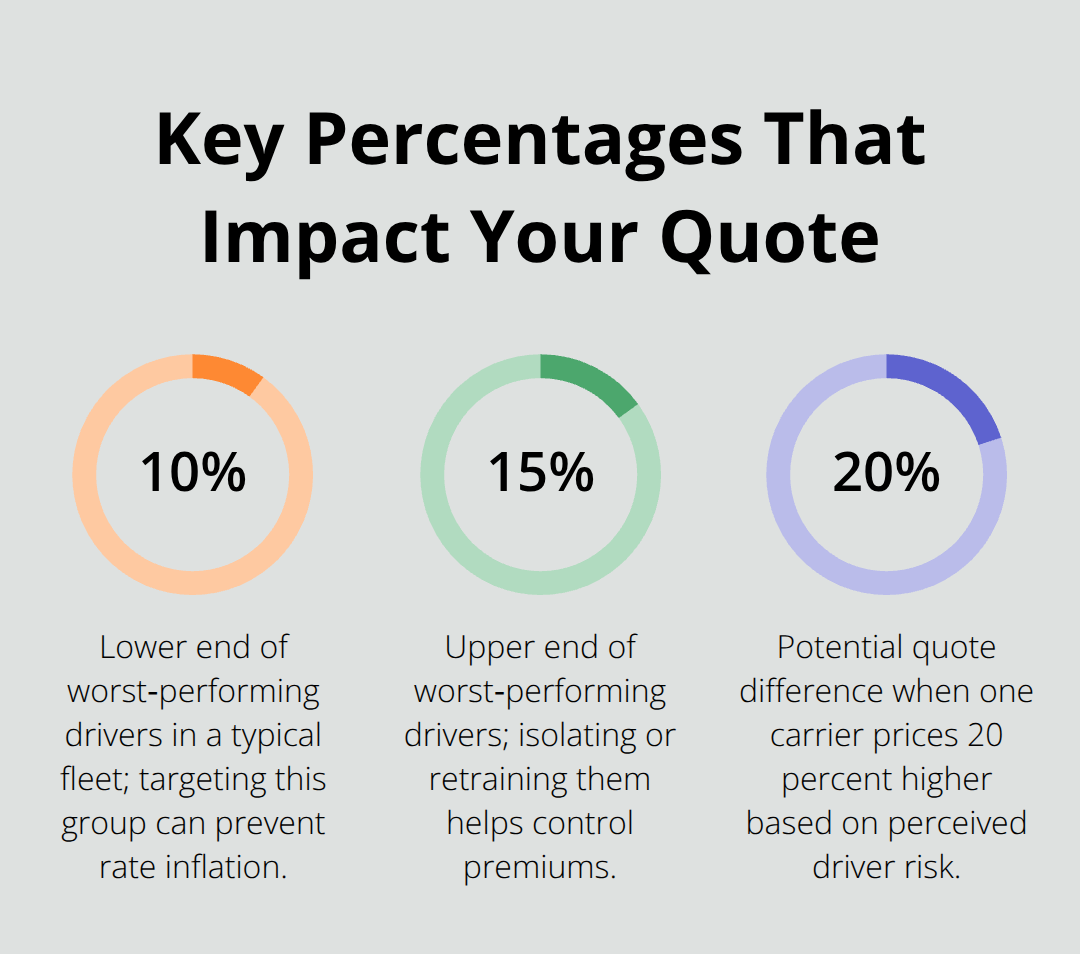

Vehicle maintenance affects rates more than many business owners realize; a well-maintained fleet experiences fewer breakdowns and crashes, signaling to insurers that you take risk seriously. Telematics data has become a powerful negotiating tool with carriers. When you share fleet data showing reduced incident frequency or improved driver behavior, insurers often lower premiums based on documented improvements rather than broad assumptions. Consider isolating your worst-performing drivers (roughly 10–15% of any fleet) for targeted training or separate policy handling to prevent them from inflating rates for your entire operation.

The strategy works because it demonstrates active risk management rather than passive acceptance of high-incident drivers, and it positions you well when you sit down to compare quotes from multiple carriers.

Comparing Quotes Without Wasting Time

Provide Complete Fleet Information

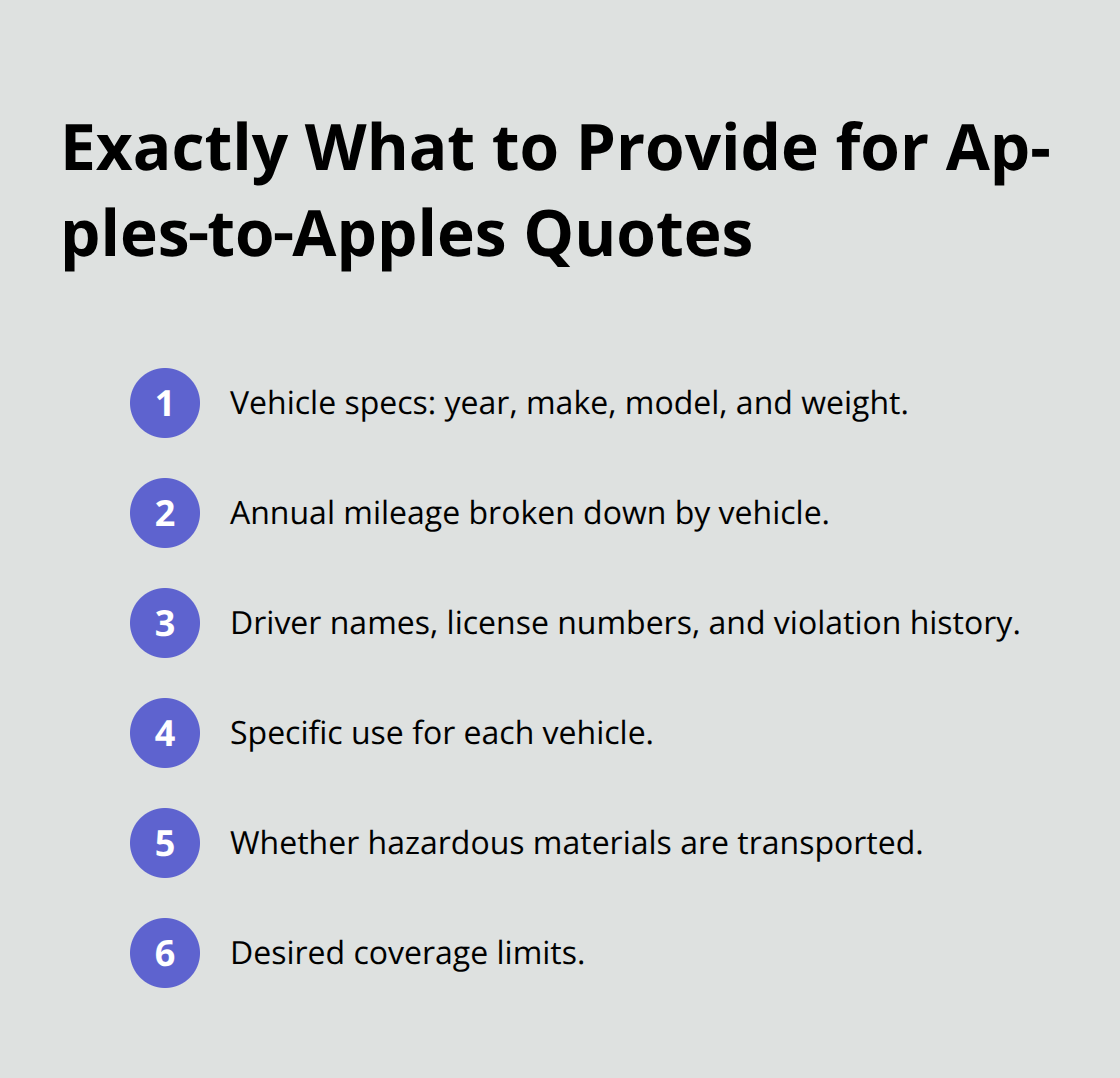

Gathering quotes from multiple insurers is non-negotiable if you want competitive rates, but the process only works when you provide identical information to each carrier. Most Minnesota businesses submit vague applications that produce wildly inconsistent quotes, making comparison impossible. When you request quotes, supply exact details about your fleet: vehicle specifications including year, make, model, and weight; annual mileage broken down by vehicle; driver names with license numbers and violation history; the specific uses for each vehicle; whether you transport hazardous materials; and your desired coverage limits.

Reputable Minnesota carriers like Liberty Mutual, Nationwide, Travelers, and Progressive will ask for this level of detail, and their willingness to dig deeper signals serious underwriting.

Understand the Numbers Behind Each Quote

According to Insureon data, their average customer pays about $147 per month for commercial auto coverage, while The Zebra reports Minnesota averages around $135 monthly-but these figures mean nothing for your quote without accounting for fleet size, vehicle type, and usage patterns. Request quotes in writing and ask each insurer to itemize coverage limits, deductibles, and any discounts they’re applying so you can see exactly what drives their pricing. Understanding what each quote actually covers separates informed decisions from expensive mistakes.

Compare Coverage and Limits Carefully

Minnesota requires minimum liability of $30,000 per person and $60,000 per accident for bodily injury, plus $10,000 for property damage, but most Minnesota businesses correctly opt for higher liability limits to protect assets from serious claims. Your quotes should clearly show whether they include collision, comprehensive, uninsured/underinsured motorist coverage, personal injury protection, towing and roadside assistance, and any industry-specific add-ons like hired and non-owned auto liability if employees use personal vehicles for work. Bundling multiple policies with one insurer typically yields discounts around $57 monthly according to Insureon data, so ask each carrier what bundling options they offer with general liability, workers’ compensation, or commercial property coverage.

Identify and Stack Discounts

Never skip asking about discounts for safety training programs, driver education initiatives, fleet telematics systems, and vehicle security features like alarms or immobilizers, as these can meaningfully reduce your premium. If your worst-performing drivers represent 10–15% of your fleet, some insurers allow policy separation that prevents those individuals from inflating rates for your entire operation. Request a detailed breakdown of what each discount saves you rather than accepting vague percentages, then cross-check that the final quoted rate reflects all applicable reductions.

Test Different Deductible Levels

Higher deductibles lower premiums substantially if your claims history supports it, so compare quotes at multiple deductible levels to find the sweet spot between monthly cost and financial risk tolerance. This comparison reveals which carriers offer the most flexibility and which ones penalize higher deductibles more aggressively than others. Once you’ve narrowed your options based on price and coverage, the next step involves evaluating which insurer actually delivers the service and support your business needs when claims occur.

How to Actually Lower Your Premiums

Stop Being a High-Risk Operation

The most direct way to reduce what you pay is to stop being a high-risk operation in your insurer’s eyes. A single at-fault accident on one driver’s record can spike your entire fleet’s premium, which is why Minnesota businesses serious about cost control implement continuous monitoring before quotes go out. If you’re comparing rates and one carrier comes in 20 percent higher than others, that difference likely reflects their assessment of your driver risk, not underwriting disagreement. Pull your MVR (motor vehicle record) data for every driver before requesting quotes, then address violations through targeted training or driver reassignment.

Target Younger Drivers and Maintenance

Younger drivers between 18 and 25 create predictable rate increases, so if that demographic makes up significant portions of your fleet, documented safety training becomes non-negotiable-insurers actively reward this with premium reductions because the data shows it works. Your maintenance records also factor in heavily; insurers see well-maintained fleets as managed operations rather than chaotic ones, so photograph regular service and share those records when discussing rates. Telematics data from dashcams or fleet monitoring systems gives you ammunition in rate negotiations because you’re showing insurers actual behavior rather than asking them to trust your word. The carriers understand that businesses tracking their drivers’ performance take risk seriously, and that documentation often results in lower quotes than operations flying blind.

Bundle Policies Across Your Business

Bundling policies across your business creates the single largest discount available to most Minnesota operations-combining auto, general liability, and workers’ compensation with one carrier typically saves around $57 monthly according to Insureon data, which compounds to nearly $700 annually. Before finalizing any quote, ask each insurer what bundling options exist and request itemized savings from each bundle configuration, then calculate your total cost across all policies rather than evaluating auto insurance in isolation.

Test Deductible Levels and Negotiate at Renewal

Higher deductibles reduce premiums substantially if your claims history supports the risk, so test quotes at $1,000, $2,500, and $5,000 deductible levels to find where your monthly savings justify your financial exposure. The worst mistake Minnesota business owners make is locking into annual policies without reviewing whether their risk profile has changed. If your worst-performing drivers represent 10 to 15 percent of your fleet and you’ve addressed their behavior through retraining or separation, your insurer needs to know that because it justifies a rate reduction at renewal. Schedule a formal review conversation 60 days before your policy renews, bring your telematics data and claims history showing improvement, and explicitly ask what rate adjustment you qualify for based on documented changes.

Carriers often build conservative assumptions into renewal quotes, so demonstrating actual performance improvements gives you leverage to negotiate down rather than passively accepting higher rates.

Final Thoughts

Getting the best rate on commercial auto insurance quotes requires you to understand what insurers measure and then demonstrate that you’ve addressed those risk factors before you shop. Vehicle type, driver records, maintenance practices, and annual mileage form the foundation of every quote you receive, but the real savings come from actively managing these variables rather than accepting them as fixed costs. Minnesota businesses that pull their MVR data early, implement driver monitoring systems, and document maintenance schedules arrive at quote conversations with leverage because they show insurers concrete evidence of risk management instead of asking carriers to trust assumptions.

Shopping around for quotes matters only when you provide identical information to each carrier so comparisons actually mean something. Request itemized breakdowns showing coverage limits, deductibles, and specific discounts applied to each quote, then test different deductible levels to find where your monthly savings justify your financial exposure. Bundling policies across your business typically saves around $57 monthly, so evaluate your total cost across auto, general liability, and workers’ compensation rather than looking at commercial auto insurance in isolation.

If your claims history improves or you address driver behavior through training and separation, schedule a formal review conversation 60 days before your policy expires and bring your telematics data and performance improvements to the table. Carriers often build conservative assumptions into renewal quotes, so documented improvements give you real negotiating power to reduce what you pay. Variant Insurance Group works with Minnesota’s top-rated insurance companies to find the coverage and pricing that fit your business, and our team compares options across multiple carriers so you get the best value without wasting time on quotes that don’t match your needs.