Your standard homeowner and auto insurance policies have limits. When someone sues you for damages exceeding those limits, you’re personally responsible for the rest.

Umbrella insurance coverage examples show how quickly liability can spiral beyond what most people expect. A serious accident, a guest injured on your property, or a business-related incident can result in six or seven-figure claims that wipe out your savings.

At Variant Insurance Group, we’ve seen Minnesota families and business owners face financial devastation because they lacked this protection. This guide walks through real scenarios where umbrella coverage made the difference between recovering and losing everything.

When Liability Exceeds Your Policy Limits

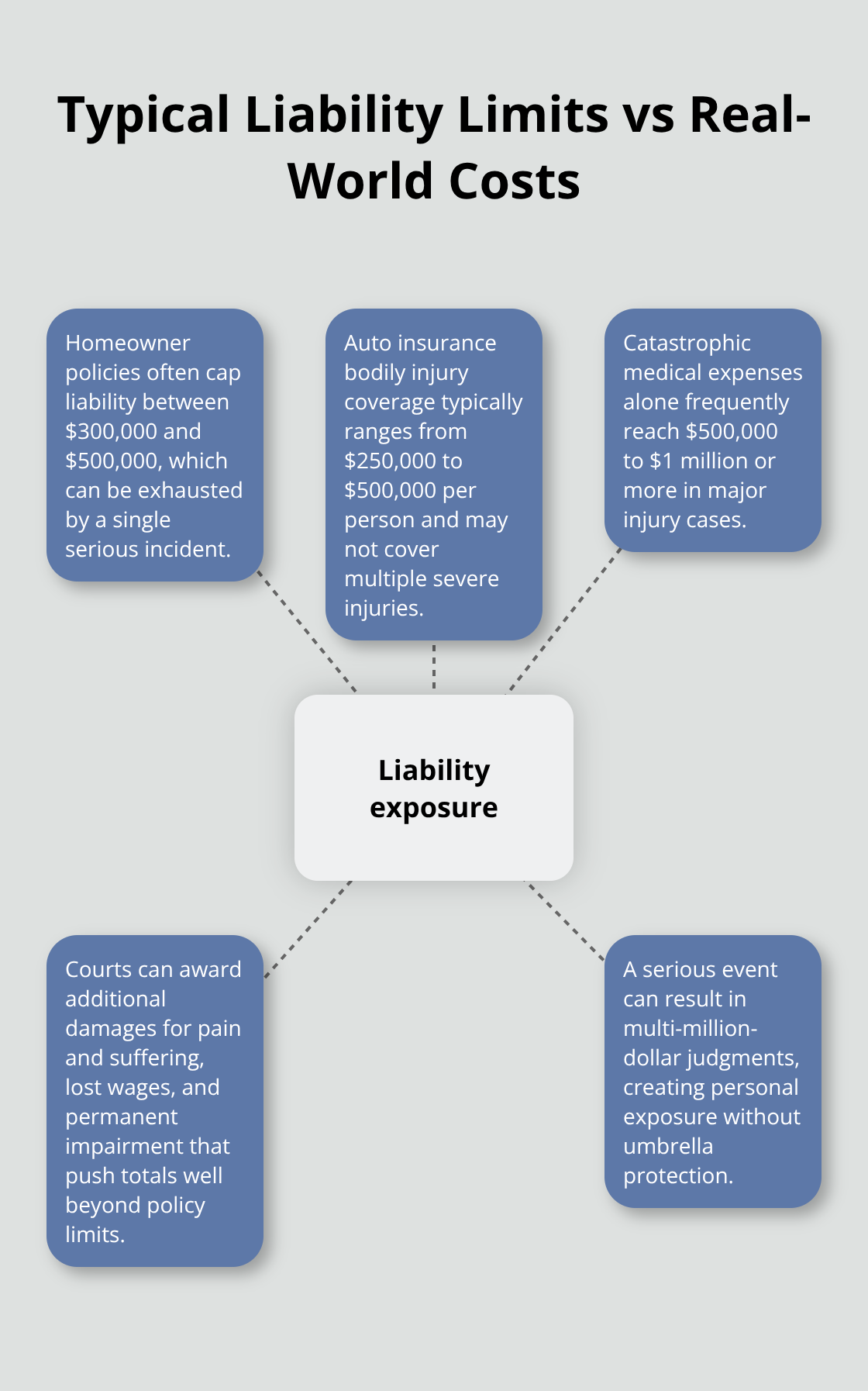

Your homeowner’s policy typically caps liability at $300,000 to $500,000. Your auto insurance might offer $250,000 to $500,000 in bodily injury coverage per person. These limits sound substantial until a single incident produces a $2 million judgment against you.

Minnesota’s statute of limitations for civil claims is six years, meaning a serious injury can result in years of legal exposure and mounting costs. A multi-car pileup on an icy Minnesota winter road, a guest suffering permanent disability after falling on your property, or a contractor injured while working at your home can all produce damages far exceeding standard policy limits. Medical expenses alone for catastrophic injuries often run $500,000 to $1 million or more, and courts regularly award additional damages for pain and suffering, lost wages, and permanent impairment. Without umbrella coverage, the difference between your policy limit and the final judgment becomes your personal liability-paid from your savings, investments, or forced sale of assets.

Property Owners Face the Highest Exposure

Homeowners with swimming pools, trampolines, or other recreational features attract significantly higher liability risk. A drowning incident or spinal injury from a trampoline accident can result in seven-figure settlements. Rental property owners face even steeper exposure because tenant injuries, visitor accidents, or property damage claims can accumulate across multiple units. Professional liability matters too-contractors, doctors, dentists, and therapists regularly face claims exceeding $1 million when their work causes injury or financial loss. Self-employed professionals often operate without business liability insurance, leaving personal assets completely exposed. Minnesota’s statute of limitations means a medical malpractice claim or construction defect case could emerge years after the incident occurred, catching you without adequate protection.

Vehicle Accidents and Winter Driving Risks

A single serious auto accident in Minnesota can produce catastrophic costs. If you face liability for injuries to multiple occupants in another vehicle, medical bills plus pain and suffering judgments accumulate quickly. A crash involving a commercial vehicle or a driver with high medical expenses can easily produce a $1.5 million to $3 million judgment. Winter conditions make Minnesota particularly vulnerable-icy roads increase accident severity, and pedestrians struck by vehicles suffer severe injuries. If you cause a multi-vehicle pile-up on a snowy highway, you could face claims from numerous injured parties simultaneously. Your auto policy’s $500,000 limit covers only the first portion of damages. Everything beyond that becomes your responsibility, and umbrella insurance starting at $1 million provides the protection that prevents financial ruin from a single winter incident.

These scenarios illustrate why standard policies leave Minnesota families and business owners exposed. The next section examines real cases where umbrella coverage made the difference between financial recovery and devastating loss.

How Umbrella Insurance Covers Real Claims That Destroyed Finances

Winter Accidents on Minnesota Roads

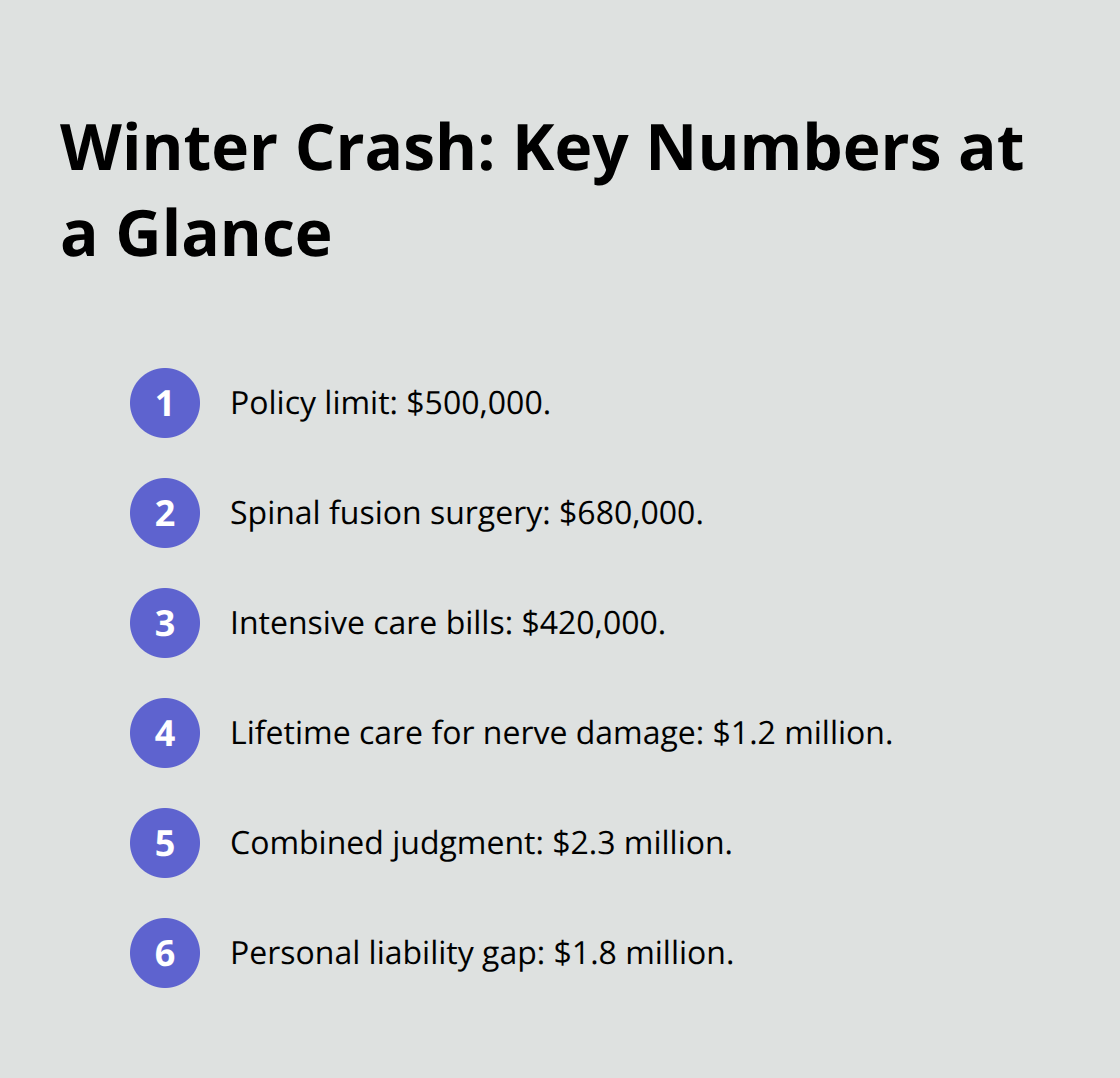

A winter morning in Minnesota turned catastrophic when a driver lost control on black ice and struck a sedan head-on, then collided with two additional vehicles. The at-fault driver’s auto policy capped bodily injury liability at $500,000. Three occupants in the struck vehicles suffered severe injuries: one required spinal fusion surgery costing $680,000, another spent six weeks in intensive care with $420,000 in medical bills, and the third faced permanent nerve damage resulting in $1.2 million in lifetime care costs. The combined judgment reached $2.3 million. The driver’s $500,000 policy covered only the first claim, leaving a personal liability of $1.8 million that forced asset liquidation and decades of wage garnishment.

An umbrella policy starting at $1 million would have covered the gap entirely, protecting the driver’s home, retirement savings, and future earnings. This scenario repeats regularly on Minnesota roads during winter months when accident severity spikes dramatically.

Swimming Pool and Water-Related Injuries

A suburban Minneapolis homeowner installed an in-ground swimming pool without realizing the liability exposure it created. A neighbor’s teenage son attended a summer gathering and dove into the shallow end, suffering a cervical spine fracture that resulted in partial paralysis. The homeowner’s policy provided $300,000 in liability coverage. Medical treatment, rehabilitation, and lifetime care for spinal cord injury can reach substantial amounts. The injured teen’s family pursued a $2.8 million settlement covering immediate medical costs, pain and suffering, and future care needs. The homeowner’s $300,000 policy exhausted within weeks, leaving a $2.5 million personal obligation. An umbrella policy of $1 million would have eliminated this exposure entirely.

Pet-Related Incidents and Contractor Injuries

Pet-related incidents follow similar patterns: a dog bite results in facial reconstruction surgery, infection complications, and psychological trauma that routinely produces $500,000 to $1.5 million in claims. A contractor bitten by a homeowner’s dog while performing roof repairs faced $890,000 in medical and reconstructive costs plus lost income during recovery. The homeowner’s standard liability coverage capped at $300,000, creating a $590,000 shortfall that umbrella insurance would have covered completely. These incidents demonstrate how quickly liability claims exceed standard policy limits and threaten personal financial security.

These real-world examples reveal the financial devastation that occurs when claims exceed policy limits. The next section examines how umbrella insurance fills the gaps that standard homeowner and auto policies leave unprotected.

How Umbrella Insurance Fills the Gaps Your Other Policies Leave Behind

Standard Policy Limits Fall Short in Real Claims

Standard homeowner and auto insurance policy liability limits often prove inadequate in real claims. These limits sound sufficient until you face a genuine claim. A three-vehicle pile-up with four injured occupants means your $500,000 limit spreads thin across multiple claimants, and subsequent injured parties receive nothing from your policy. Homeowners insurance excludes certain high-risk incidents entirely-intentional acts, business operations conducted from your home, and some rental property liabilities fall outside standard coverage. A contractor running a small business from a home office, a landlord managing rental units, or someone operating a home-based service discovers too late that their standard policy won’t cover business-related injuries or property damage.

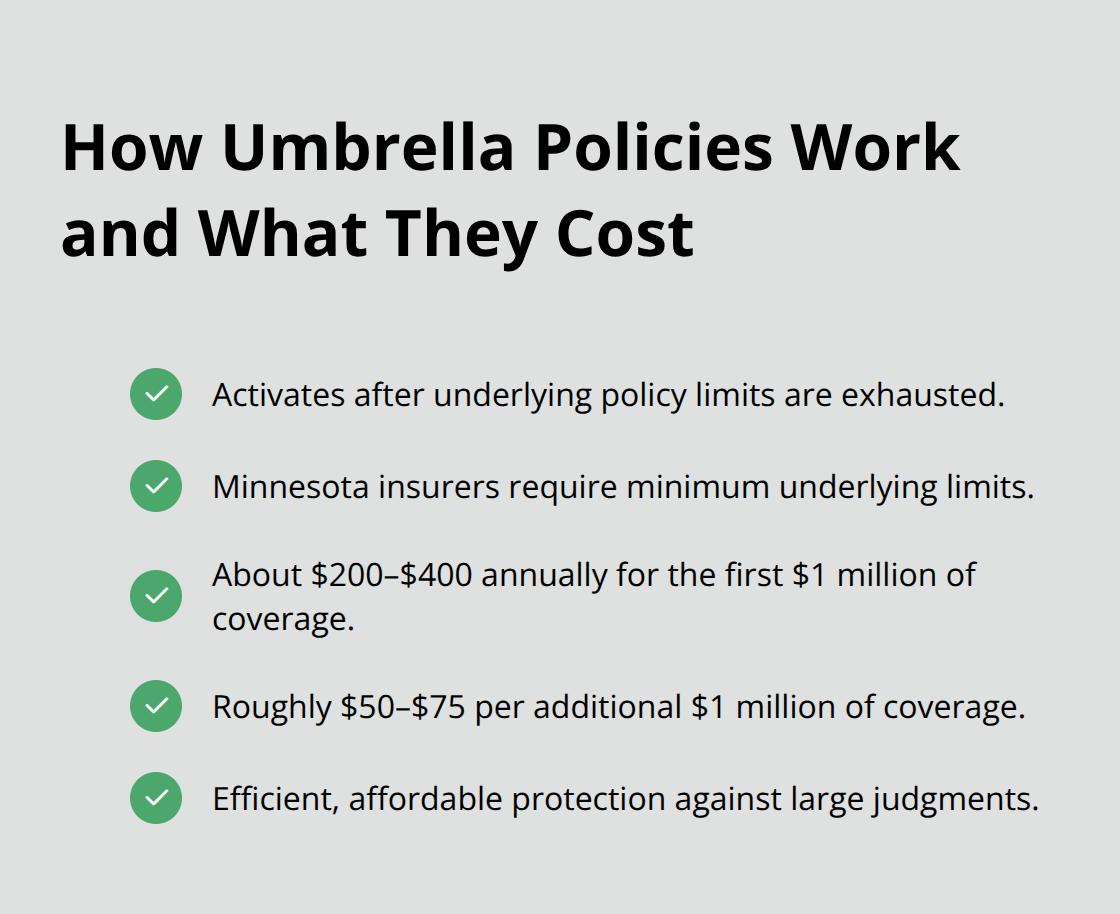

Auto insurance creates additional gaps: it covers accidents you cause, but limits reset per claim, meaning multiple injured parties in one accident can exhaust your coverage across several claims simultaneously. When claims exceed your policy limits, you become personally responsible for the difference. Umbrella insurance activates only after your underlying coverage exhausts, which is why Minnesota insurers require minimum underlying limits before issuing umbrella protection. This structure makes umbrella policies remarkably efficient and affordable-coverage starts around $200 to $400 annually for $1 million in protection, then adds roughly $50 to $75 per additional $1 million.

Business Operations and Professional Work Create Exposure

Self-employed professionals face the steepest exposure because they often operate without business liability insurance while simultaneously carrying higher personal risk. A therapist, contractor, medical professional, or consultant working independently holds personal assets vulnerable to claims arising from their professional work. Standard homeowner policies exclude professional services entirely, and many professionals mistakenly believe their work falls under their personal liability coverage when it absolutely does not.

Umbrella insurance for professionals requires customized endorsements that account for their specific occupation and risk profile. Once properly structured, it protects personal assets from professional liability claims that would otherwise devastate personal finances. A dentist sued for a botched procedure, a contractor facing a negligence claim for faulty installation, or a consultant accused of providing damaging advice can all face six-figure claims that umbrella coverage addresses completely. The additional cost for professional endorsements typically runs $100 to $200 more annually than standard umbrella policies-a modest investment compared to the exposure it eliminates.

Why Underlying Coverage Requirements Matter

Minnesota insurers require minimum underlying limits before issuing umbrella protection because umbrella policies work as excess coverage. Your homeowner and auto policies must meet specified minimums before umbrella coverage activates. This requirement protects both you and the insurer by establishing a solid foundation of primary coverage. Without adequate underlying limits, you lack the initial protection layer that umbrella insurance supplements. At Variant Insurance Group, we review your existing policies to confirm they meet these minimums and recommend adjustments if necessary, ensuring your umbrella coverage functions as intended when you need it most.

Final Thoughts

The umbrella insurance coverage examples throughout this guide reveal a consistent reality: Minnesota families and business owners face financial devastation when liability claims exceed their standard policy limits. A winter accident, a pool injury, or a professional liability claim produces judgments of $1 million to $3 million or more, wiping out decades of savings and forcing asset liquidation. Your existing policies leave dangerous gaps that umbrella insurance fills efficiently and affordably.

For Minnesota homeowners, umbrella coverage starting at $1 million offers protection at a remarkably affordable cost-typically $200 to $400 annually for the first million dollars. Rental property owners, contractors, and medical professionals face steeper exposure and benefit significantly from customized umbrella policies that address their specific occupational risks. The six-year statute of limitations for civil claims in Minnesota means liability exposure extends years beyond an incident, making long-term protection essential.

At Variant Insurance Group, we review your current coverage and identify the umbrella protection that fits your actual risk exposure and budget. Contact our team to discuss your coverage needs and receive a free quote. Don’t wait for a claim to discover you’re underprotected.