A single accident on your property can lead to thousands of dollars in medical bills and legal fees. Personal liability coverage in homeowners insurance protects you financially when someone is injured at your home or when you accidentally damage someone else’s property.

At Variant Insurance Group, we help Minnesota homeowners understand how much protection they actually need. This guide walks you through coverage limits, real-world scenarios, and how to choose the right amount of liability protection for your situation.

What Personal Liability Coverage Actually Protects

Personal liability coverage is the part of your homeowners policy that activates when you become legally responsible for someone’s injury or property damage. It pays medical bills if a guest slips on your stairs, covers legal fees if you face a lawsuit, and funds settlements if you’re found at fault. This coverage applies to incidents on your property and sometimes even off your property-like if your dog bites someone at a neighbor’s house or you accidentally damage their fence with your lawnmower. The policy typically includes medical payments coverage, which pays a guest’s immediate medical expenses even if you’re not legally at fault, preventing small accidents from escalating into major disputes. Most Minnesota homeowners policies start with a $100,000 liability limit, though you can increase this to $300,000 or $500,000 depending on your assets and risk factors.

How Much Coverage Limits Actually Matter

Standard $100,000 liability limits work fine if your net worth is modest, but this amount fails to protect you adequately if you own significant assets. If you have $500,000 in home equity, investments, and savings, a $100,000 liability limit leaves you vulnerable to a lawsuit that could exceed your coverage and put your personal assets at risk. Umbrella coverage fills this gap by extending protection beyond your homeowners policy limits, typically starting at $1,000,000 in coverage, and costs far less than most people expect-annual premiums for $1 million in coverage range from $125 to $400. The real advantage of umbrella coverage is that it not only extends your liability limits but also covers personal injury claims like false arrest, defamation, and invasion of privacy, which your standard homeowners policy may not include. If you host frequent gatherings, own a pool, or maintain other attractive nuisances on your property, higher liability limits become increasingly important.

Where Personal Liability Falls Short

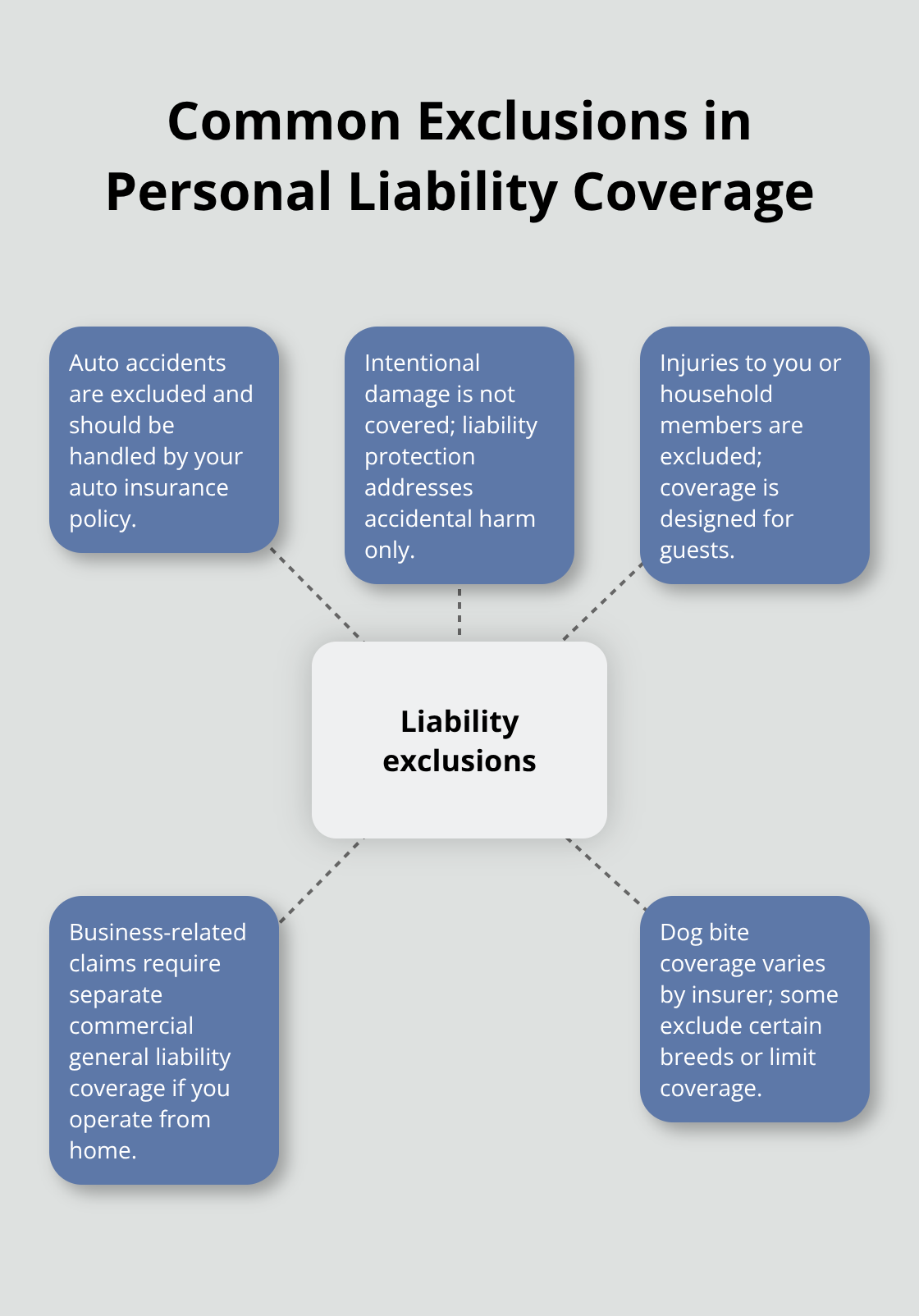

Personal liability coverage explicitly excludes auto accidents, which your auto insurance policy handles instead. It also won’t cover intentional damage you cause, injuries to you or your household members, and business-related claims if you operate a business from home. If you run a side business, you need separate commercial general liability coverage, not personal liability.

Dog bite coverage varies significantly by insurer-some exclude certain breeds entirely or limit coverage, so you must verify your specific policy language with your agent. These gaps matter because they prevent you from assuming you’re protected when you actually aren’t.

What Happens When You Face a Liability Claim

When someone files a claim against your personal liability coverage, your insurer pays for their medical expenses, property repairs, and legal defense costs up to your policy limit. Your insurer also handles the legal process, which means they cover attorney fees and court costs even if the lawsuit proves groundless. This protection extends to your household members as well-if your teenager accidentally damages a neighbor’s car, your liability coverage responds. The insurer negotiates settlements and defends you in court, removing much of the stress from the claims process. Understanding how this protection works helps you recognize why adequate limits matter far more than simply accepting whatever your agent initially recommends.

Choosing Limits That Match Your Situation

Your net worth determines how much liability protection you actually need. If you own a home worth $300,000 with $100,000 in savings and investments, a $300,000 liability limit provides reasonable protection. However, if your total assets exceed $500,000, that same limit leaves significant exposure. Umbrella coverage fills this gap by extending protection beyond your homeowners policy limits. The next section walks you through assessing your specific risk factors and understanding what Minnesota requires for adequate protection.

Real-World Scenarios Where Personal Liability Applies

Injuries on Your Property

A guest slips on your wet kitchen floor and breaks their wrist. Your teenager’s baseball crashes through a neighbor’s window. Your dog nips someone at the dog park. These situations happen constantly in Minnesota homes, and your personal liability coverage responds to each one differently.

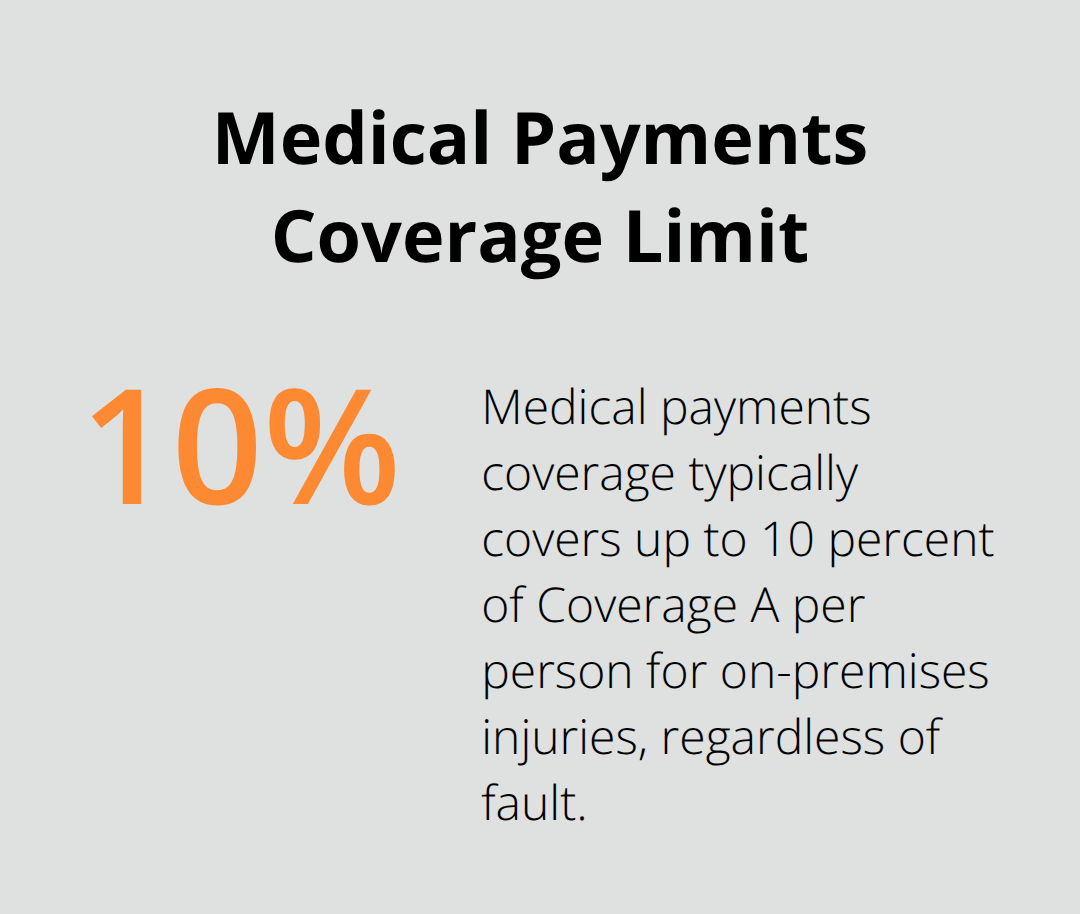

When someone is injured on your property and you’re found legally responsible, your coverage pays their medical bills immediately, even if the injury seems minor at first. Medical payments coverage typically covers up to 10 percent of Coverage A per person for injuries sustained on your premises, regardless of fault. This distinction matters significantly because it prevents minor incidents from festering into formal lawsuits without requiring you to prove negligence.

However, if injuries are severe and medical expenses exceed your medical payments limit, your liability coverage takes over and covers the full cost of treatment, rehabilitation, and ongoing care up to your policy limit. Swimming pools generate disproportionately high claims, with serious drowning or near-drowning incidents resulting in damages that frequently exceed $500,000. Installing safety features like fencing with locked gates and maintaining clear supervision reduces your risk, but it doesn’t eliminate the need for adequate coverage.

Damage You Cause to Others’ Property

Your lawnmower kicks up a rock and dents your neighbor’s car. A tree branch from your yard damages their roof during a storm you could have prevented. Your homeowners policy pays for these repairs through your liability coverage. Your policy also covers incidents that happen away from your property, such as your dog biting someone at a public park or you accidentally damaging someone’s property while visiting their home.

What many Minnesota homeowners overlook is that liability coverage includes all legal defense costs, meaning your insurer pays for an attorney, court fees, and expert witnesses even if the lawsuit against you is completely groundless. This protection removes the financial burden of defending yourself from the moment a claim is filed, not just if you ultimately lose the case.

Legal Costs and Financial Exposure

The financial exposure from a single incident can be substantial. A serious injury claim in Minnesota might result in medical expenses exceeding $50,000, plus additional damages for lost wages and pain and suffering that could total $200,000 or more. Your $100,000 liability limit covers the medical expenses but leaves you personally responsible for the remainder if you’re found at fault.

This is precisely why understanding your actual liability exposure matters more than accepting default coverage limits. If you frequently host gatherings, own a pool, or have other features that attract guests to your property, your liability risk increases dramatically. Your homeowners policy explicitly excludes auto-related incidents, so a guest injured in your driveway due to a vehicle accident falls under your auto policy instead. It also won’t cover intentional harm, injuries to household members, or business-related claims if you operate any business from your home.

Coverage Gaps You Need to Know

These exclusions mean you must carefully evaluate whether your specific situation requires additional coverage beyond standard personal liability protection. Dog bite coverage varies significantly by insurer-some exclude certain breeds entirely or limit coverage, so you must verify your specific policy language with your agent. If you run a side business, you need separate commercial general liability coverage, not personal liability. Understanding these gaps prevents you from assuming you’re protected when you actually aren’t, which becomes critical as you assess your actual risk factors and determine what coverage limits make sense for your Minnesota home.

Calculating the Right Liability Limit for Your Home

Start With Your Net Worth

Your net worth is the number that matters most when you decide how much liability coverage you actually need. Add up everything you own: your home value, retirement accounts, investments, savings, vehicles, and any other significant assets. If that total reaches $300,000, a $300,000 liability limit provides reasonable protection because a judgment against you could theoretically claim your entire net worth. However, most Minnesota homeowners underestimate their actual assets and carry inadequate limits instead. The standard $100,000 starting point works only if your net worth genuinely hovers around that amount, which is increasingly rare in Minnesota’s real estate market where median home values in many areas exceed $350,000. If you own a home worth $400,000 with $150,000 in savings and investments, your net worth already reaches $550,000, making a $100,000 liability limit dangerously insufficient. The math is straightforward: your liability coverage should match or exceed your total net worth to prevent a single lawsuit from destroying your financial stability.

How Risk Factors Push You Toward Higher Limits

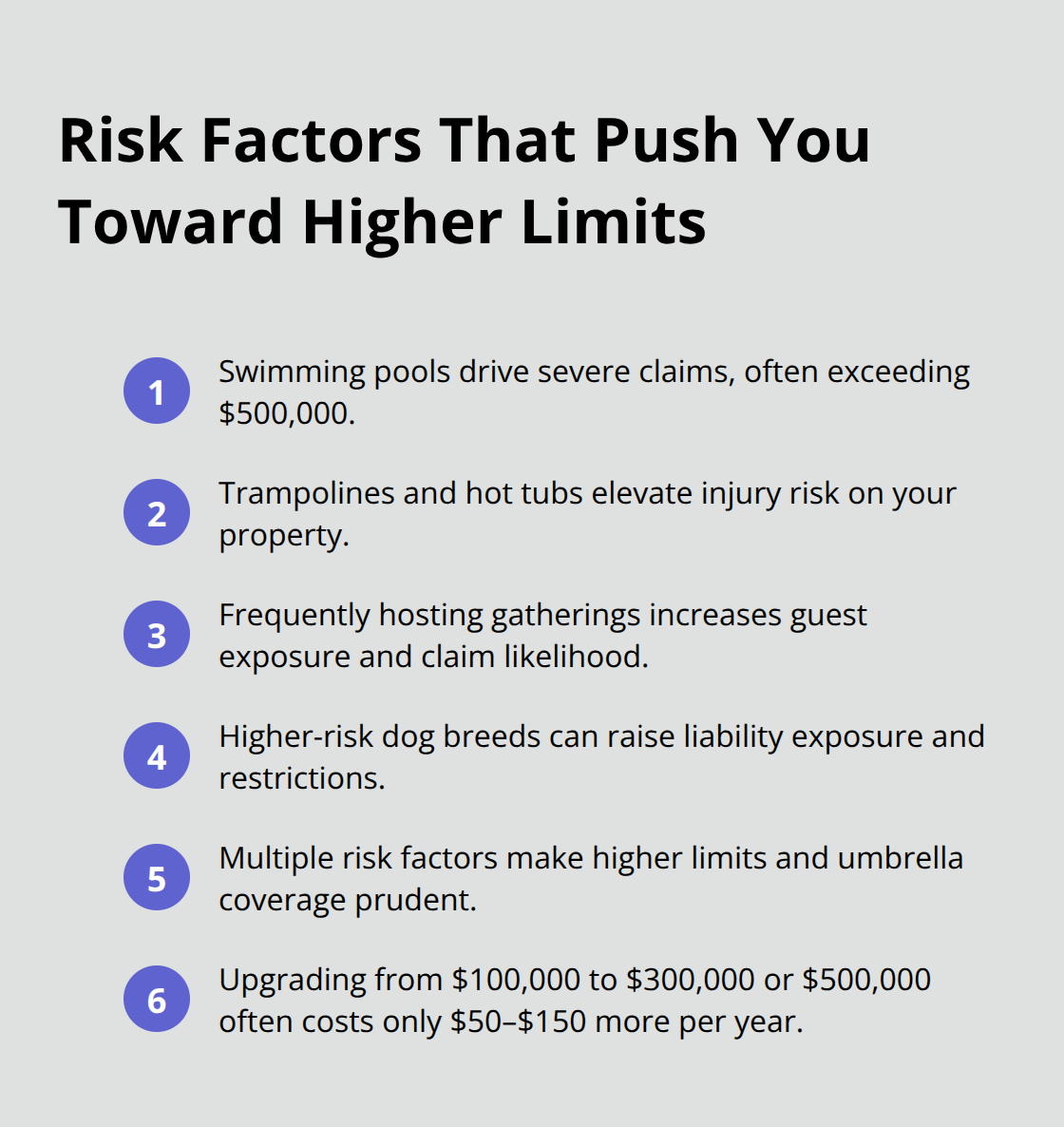

Risk factors on your property increase the likelihood of claims and should push you toward higher limits regardless of your net worth. Swimming pools generate the most serious claims in Minnesota, with severe injuries regularly resulting in liability coverage settlements exceeding $500,000. Trampolines, hot tubs, and properties where you frequently host gatherings also elevate your exposure significantly. Dog ownership matters too, particularly if you own breeds that insurance companies view as higher risk.

If you have multiple risk factors, the cost difference between $100,000 and $300,000 in coverage remains remarkably small because liability is among the least expensive components of homeowners insurance. The premium difference between $100,000 and $500,000 in coverage typically amounts to $50 to $150 annually, making the upgrade financially sensible for most Minnesota homeowners.

Understanding Minnesota’s Legal Requirements

Minnesota law does not mandate specific liability limits for homeowners, but mortgage lenders typically require minimum coverage (usually around $100,000). Beyond that legal requirement, your decision should rest entirely on what you actually have to lose. If your assets exceed $500,000, umbrella coverage becomes essential rather than optional, providing $1,000,000 or more in additional protection at costs ranging from $125 to $400 annually depending on your underlying limits and claims history.

Comparing Coverage Across Different Carriers

When you compare coverage options across carriers, focus on what each insurer excludes rather than their base limits, since exclusions create gaps that no amount of coverage fixes. Some insurers exclude certain dog breeds entirely while others simply increase premiums, making breed-related coverage a critical comparison point for pet owners. Dog bite coverage limits also vary substantially between carriers, so verify exact protection before you purchase a policy. This comparison process reveals which carriers align with your specific situation and which ones leave you exposed to unexpected gaps.

Final Thoughts

Personal liability coverage in homeowners insurance protects your finances when accidents happen, but only if you carry adequate limits that match your actual assets. The standard $100,000 starting point leaves most Minnesota homeowners dangerously exposed, particularly those with significant assets or properties that attract guests. Your net worth should determine your coverage limits, and if your assets exceed $500,000, umbrella coverage becomes essential rather than optional.

Review your current homeowners policy immediately by checking your declarations page for your actual liability limit and whether personal injury coverage is included. Many Minnesota homeowners discover they’ve been underinsured for years, carrying limits that haven’t increased despite rising home values and asset accumulation. If you own a pool, trampoline, or frequently host gatherings, higher limits should be non-negotiable, and dog owners must verify whether their specific breed faces exclusions or limitations.

Contact Variant Insurance Group to review your current coverage and determine whether your personal liability coverage homeowners insurance limits align with your actual assets and risk factors. We shop Minnesota’s top-rated insurance companies to find protection that matches your situation and safeguards what you’ve worked to build. Our team compares your options across multiple carriers to help you get the best possible value without gaps that could devastate your finances.