Your homeowners insurance personal property coverage protects the belongings inside your home-from furniture and electronics to clothing and kitchen appliances. Most Minnesota homeowners don’t realize how much their possessions are actually worth until they need to file a claim.

At Variant Insurance Group, we’ve seen firsthand how confusing personal property protection can be. This guide walks you through what’s covered, how much protection you need, and practical steps to maximize your claim if disaster strikes.

What Your Personal Property Coverage Actually Protects

Personal property coverage in your homeowners policy protects the contents inside your home, from furniture and electronics to clothing and kitchen appliances. Standard policies cover everyday items, but the specifics matter far more than most Minnesota homeowners realize. Your policy typically caps coverage for certain high-value items. Jewelry, for example, is often limited to $1,500 to $2,500 unless you add additional protection. Electronics, firearms, and collectibles face similar caps.

According to ISO data covering 2019 through 2023, property damage and theft account for 97.3% of homeowners losses. Wind and hail damage to your belongings represents roughly 38% to 47% of all homeowners losses, while water damage and freezing account for approximately 20% to 29%. Fire and lightning cause about 18% to 22% of losses. The average homeowners claim severity sits at $17,059, so understanding what’s actually covered matters when you face a real loss.

How Your Coverage Limit Works

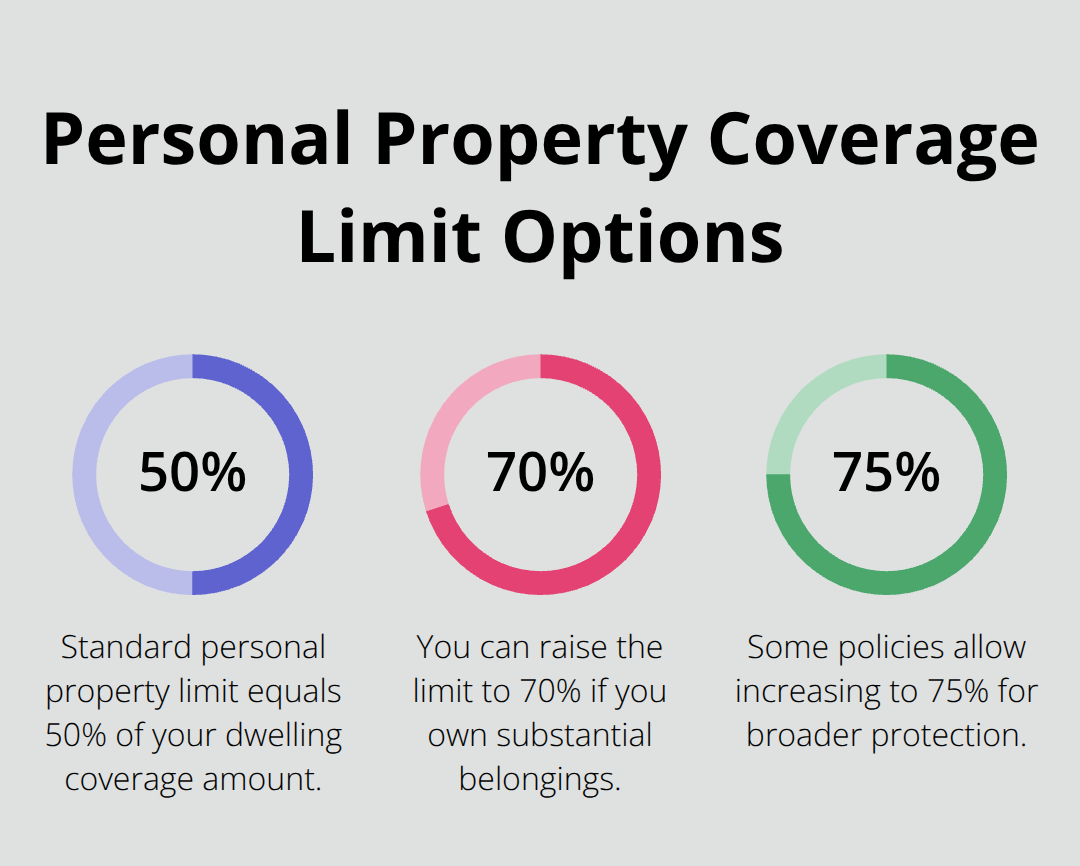

Your personal property coverage limit typically equals 50% of your dwelling coverage amount. If your home is insured for $100,000, your personal property coverage is usually $50,000. You can adjust this percentage upward to 70% or 75% if you own substantial belongings, but most people never make this change.

The deductible you choose for your personal property coverage applies per loss event, not per item. If you select a $1,000 deductible and experience a fire that damages $15,000 worth of belongings, you pay $1,000 and receive $14,000. That same deductible applies whether one item or one hundred items are damaged. Higher deductibles lower your premium, but they also mean larger out-of-pocket costs when losses occur.

What Stays Unprotected

Certain items are explicitly excluded from standard personal property coverage. Vehicles, including cars, motorcycles, and ATVs, require separate auto insurance. Pets need their own coverage. Items used for business purposes don’t qualify unless you have a home business endorsement. Flood damage is notably absent from standard all-risk coverage, which surprises many Minnesota homeowners who experience basement water intrusion. Earthquake and hurricane damage are also excluded in most policies. Tornadoes are typically not covered either, though wind damage from regular storms is protected.

Replacement Cost Versus Actual Cash Value

The Minnesota Department of Commerce recommends reviewing your policy declarations page to confirm whether personal property coverage uses replacement cost value or actual cash value. Replacement cost value pays to replace items at current prices, while actual cash value reduces payouts based on depreciation. Replacement cost value costs more upfront but delivers substantially better protection when you file a claim.

If you live in an area prone to water intrusion or flooding, you need to ask your agent about water backup coverage or separate flood insurance. Maintaining a home inventory can prove beneficial in case of theft or damage to your belongings, helping you document exactly what protection your belongings actually need.

How Much Personal Property Coverage Do You Actually Need

Most Minnesota homeowners underestimate their belongings by 30% to 50%. You walk through your home and think your furniture, electronics, and clothing are worth $25,000. Then a house fire strikes and you realize you owned three televisions, two laptops, a closet full of winter coats, kitchen appliances, and countless other items you forgot about.

Start With a Home Inventory

The Minnesota Department of Commerce recommends conducting a detailed home inventory before calculating your coverage needs. This means photographing every room, documenting serial numbers on electronics, and gathering receipts for major purchases. According to the Triple-I and Munich Re Consumer Survey from 2023, only 47% of homeowners maintain an inventory, which explains why so many underbuy coverage.

Walk through your home with your phone camera and record video of each room, opening closets and drawers. This video becomes your proof of ownership when you file a claim. For high-value items like jewelry, artwork, or firearms, obtain written appraisals from qualified professionals. Store these documents separately from your home, either digitally in cloud storage or in a safe deposit box.

Calculate Your Real Replacement Costs

Your standard personal property limit typically sits at 50% of your dwelling coverage. If your home replacement value is $200,000 and you have $100,000 in dwelling coverage, your automatic personal property limit is $50,000. Most people never question whether $50,000 actually covers their possessions.

Calculate your real replacement costs by adding up furniture prices, electronics, clothing, and household items at current retail prices. You will almost certainly exceed 50% of dwelling coverage. At that point, you can increase your personal property limit during your policy renewal.

Choose Replacement Cost Over Actual Cash Value

The choice between replacement cost value and actual cash value dramatically affects your payout after a loss. Replacement cost value pays what it costs to replace items today, while actual cash value subtracts depreciation. A five-year-old television purchased for $1,200 might be worth only $400 at actual cash value but cost $900 to replace new. Over a household of hundreds of items, this depreciation compounds into thousands of dollars in reduced claims payments.

Replacement cost value coverage for personal property offers substantially better protection, even though it costs more upfront. The premium difference typically amounts to $100 to $300 annually, but the protection difference is substantial.

Consider Scheduled Personal Property Coverage

For items with extremely high replacement costs or those that depreciate slowly, scheduled personal property coverage (sometimes called a floater) insures specific items separately at agreed-upon values, bypassing depreciation calculations entirely. Jewelry, collectible firearms, art, and antiques qualify as excellent candidates for scheduled coverage.

Update Your Coverage as Life Changes

Your belongings change as life unfolds. You purchase new electronics, inherit furniture, or acquire collectibles. These changes mean your coverage needs shift too. Review your personal property limits annually during policy renewal, especially after major purchases or life events. If you recently furnished a new home office, upgraded your kitchen appliances, or inherited valuable items, your 50% limit may no longer provide adequate protection.

Adjusting coverage takes minutes but prevents catastrophic gaps when loss occurs. Many homeowners discover too late that their coverage falls thousands of dollars short of actual replacement needs. Once you understand your coverage amount, the next step involves protecting that coverage through proper documentation and strategic endorsements.

How to Protect Your Claim When Loss Happens

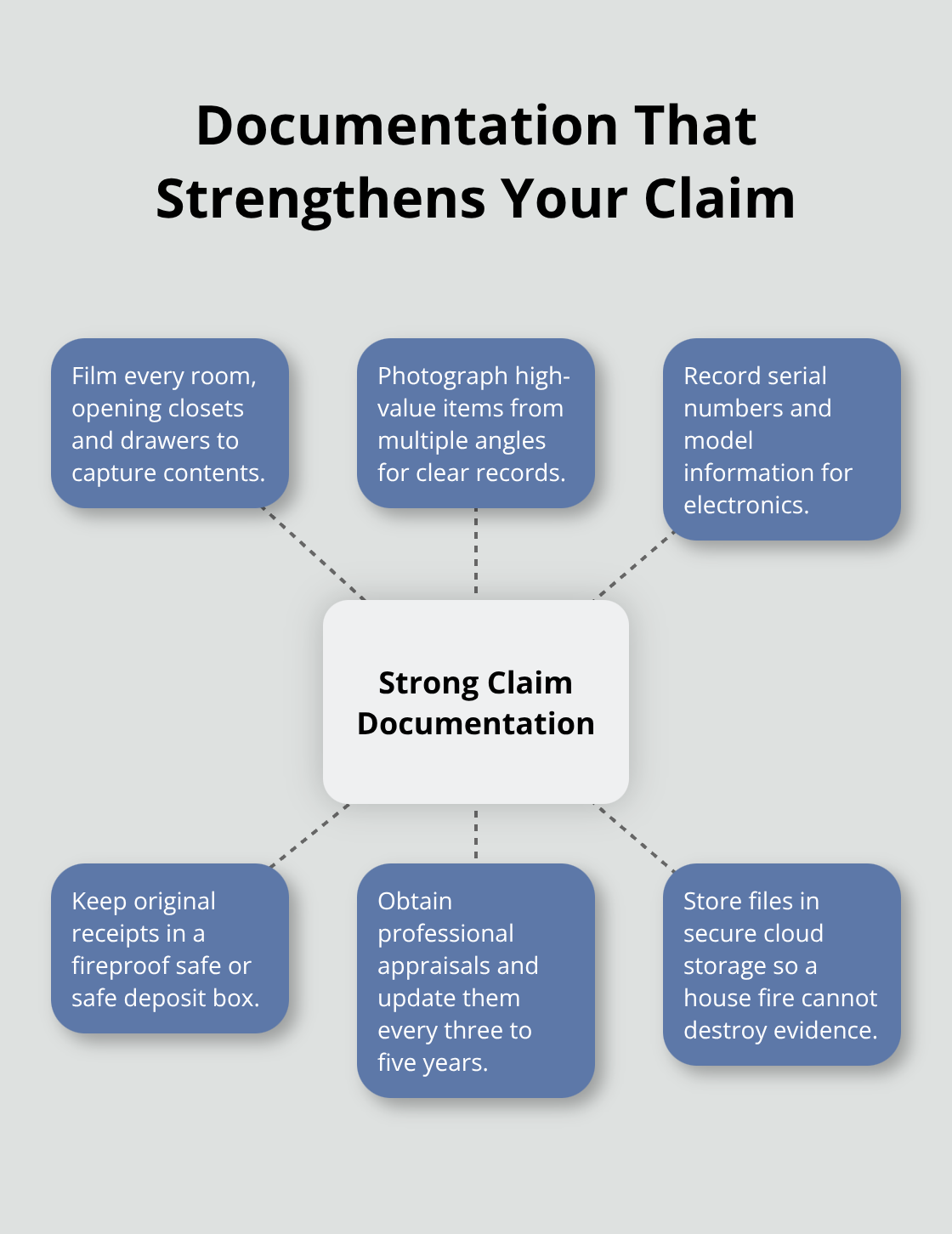

Documentation separates successful claims from denied ones. Most Minnesota homeowners discover this truth only after filing a claim, which is far too late. Proper documentation proves what you owned when loss strikes. Start now by filming every room in your home with your smartphone, opening closets, drawers, and cabinets to capture the actual contents. This video becomes irrefutable proof of ownership when adjusters question your claim. Photograph high-value items from multiple angles and store these files in cloud storage like Google Drive or Dropbox so a house fire cannot destroy your evidence.

For electronics, write down serial numbers and model information. For furniture, capture manufacturer tags and condition details. This process takes roughly three to four hours for a typical home but saves thousands of dollars during claims. Store original receipts for major purchases in a fireproof safe or safe deposit box, separate from your home.

Appraisals for jewelry, artwork, firearms, and collectibles should come from certified professionals and receive updates every three to five years as values fluctuate. The Triple-I and Munich Re Consumer Survey found that 47% of homeowners maintain inventories, meaning the majority of people leave themselves vulnerable to undercompensation.

Strategic Coverage for High-Value Possessions

Standard personal property limits fail to protect expensive items adequately. Your policy likely caps jewelry at $1,500 to $2,500, firearms at similar amounts, and fine art at $2,500 or less, regardless of actual replacement costs. Scheduled endorsements allow you to add extra coverage in order to insure high-value items beyond the limits imposed by a standard homeowners policy. A wedding ring appraised at $8,000 gets insured for exactly $8,000, not the $1,500 standard limit. Firearms collections, original artwork, and vintage instruments qualify as excellent candidates because replacement costs remain stable or appreciate.

This coverage costs roughly $150 to $400 annually depending on item values, which pales against potential loss. Without scheduled coverage, a fire destroying a $12,000 camera collection leaves you with a $2,500 payout and a $9,500 gap.

Annual Coverage Reviews Matter

Your belongings change constantly, yet most homeowners review coverage only at renewal or never at all. A kitchen renovation, new furniture purchase, or inherited items means your 50% limit may no longer match reality. Conduct a quick inventory update annually by reviewing major purchases from the past year and adjusting your personal property limit if necessary. If you spent $15,000 on home improvements, electronics, or furnishings, your coverage needs shifted significantly.

Replacement cost value coverage remains superior to actual cash value because depreciation compounds across hundreds of items. A five-year-old couch, television, and laptop all depreciate substantially, yet replacement cost value ignores this depreciation entirely. The premium difference between these options typically ranges from $100 to $300 annually for most Minnesota homes, making replacement cost value the clear financial choice.

Final Thoughts

Personal property protection forms the foundation of a complete homeowners insurance personal property policy, yet most Minnesota homeowners treat it as an afterthought. Your belongings represent thousands of dollars in assets that deserve proper coverage, and standard policies cap high-value items at amounts far below replacement costs. Without scheduled endorsements or floaters, you face significant financial loss when disaster strikes.

The steps outlined in this guide work together to build comprehensive protection. A detailed home inventory reveals what you actually own, choosing replacement cost value over actual cash value ensures depreciation doesn’t slash your claim payments, and scheduled personal property coverage protects expensive items beyond standard limits. Documentation through photos, videos, and receipts transforms vague claims into concrete proof of ownership. Regular policy reviews prevent coverage gaps from widening as your life changes-a kitchen renovation, new furniture, or inherited items shift your protection needs immediately.

Contact Variant Insurance Group to review your current coverage and identify any gaps in your protection. Our experienced professionals answer questions about scheduled endorsements, coverage limits, and documentation strategies that strengthen your claim when loss occurs.