Your foundation is one of your home’s most critical structural components, yet many homeowners are unsure about what their insurance actually covers when problems arise.

At Variant Insurance Group, we’ve seen firsthand how foundation damage can create confusion and financial stress for Minnesota homeowners. The answer to whether homeowners insurance covers foundation issues isn’t straightforward-it depends on what caused the damage and what your policy includes.

What Actually Causes Foundation Problems

Soil Movement and Settlement

Foundation damage in Minnesota homes stems from three distinct categories, and understanding which one affects your home matters enormously for your insurance claim. Soil movement beneath your foundation causes the most widespread problems across the state. Minnesota’s clay-heavy soil expands when wet and contracts when dry, creating constant shifting that stresses your foundation year-round. During drought periods, soil pulls away from the foundation, leaving gaps that allow water to seep in once rain returns.

Tree roots extending 20 to 40 feet from the trunk actively seek moisture and exert tremendous pressure on foundations, particularly in older neighborhoods where mature trees surround homes. Burrowing animals like voles and moles tunnel under foundations and remove soil support, creating settlement zones. Standard homeowners insurance does not cover this type of damage because it results from normal earth movement rather than a sudden accident.

Water Intrusion and Freeze-Thaw Damage

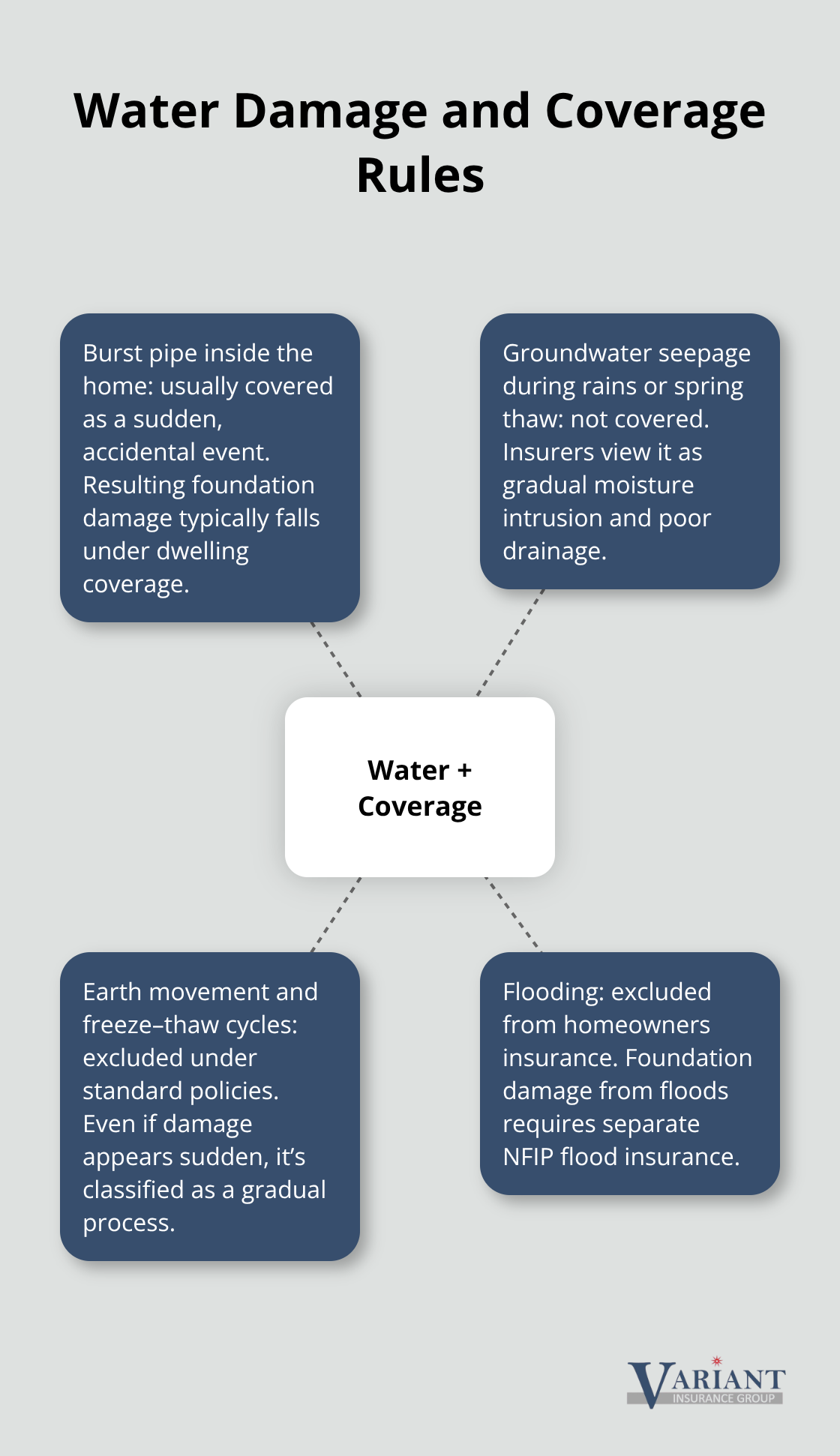

Water-related foundation damage presents a second major threat, but coverage depends entirely on what caused the water to enter. A burst water pipe inside your home that floods the basement and cracks the foundation is typically covered as sudden water damage. A foundation crack that allows groundwater to seep in during heavy rains is not covered, since it results from poor drainage and gradual moisture accumulation rather than a specific covered event.

Freeze-thaw cycles unique to Minnesota winters create particular risk. Water enters small cracks, freezes, expands, and widens the damage. Most standard policies specifically exclude this damage from ice expansion. These water-related exclusions apply even when the damage seems sudden to you, because insurers distinguish between sudden events and gradual processes.

Cracks from Age Versus Sudden Impact

Concrete naturally shrinks as it cures and cracks with temperature fluctuations, but these age-related cracks are considered maintenance issues, not insurable events. However, if a severe storm causes a tree to fall on your home and crack the foundation, or if a vehicle impacts your house and damages the foundation, that sudden accidental damage from a covered peril is typically covered under the dwelling portion of your policy, minus your deductible.

The distinction between gradual deterioration and sudden accident determines whether your claim receives payment. This is why the next step-understanding exactly what your policy covers-becomes so important for protecting your home and your finances.

What Your Policy Actually Covers

Sudden Damage from Covered Perils

Your homeowners insurance policy covers foundation damage only when a sudden, accidental event causes it. If a severe storm topples a tree onto your home and cracks the foundation, or if a vehicle crashes into your house and damages the foundation structure, that sudden damage typically falls under your dwelling coverage, minus your deductible. Similarly, if a gas explosion inside your home ruptures and cracks the foundation, or if a fire weakens the structural integrity, these covered perils trigger protection. Homeowners insurance may cover foundation repairs damaged by covered perils, such as tornados or falling trees. However, this protection only applies to the damage itself-not to the underlying cause if that cause is excluded from your policy.

Water Damage: The Critical Distinction

Water damage from a specific event inside your home receives different treatment than gradual water intrusion. If a water pipe bursts and floods your basement, damaging the foundation in the process, that sudden water event is usually covered. But here’s where most Minnesota homeowners encounter problems: if your foundation cracks and groundwater seeps in during spring thaw or heavy rains, your policy will not cover that damage. Gradual moisture accumulation and poor drainage do not qualify as sudden covered events.

Standard policies exclude damage from earth movement, settling, and freeze-thaw cycles-all common culprits in Minnesota. They also exclude flood damage entirely, which means foundation damage from flooding requires separate flood insurance through the National Flood Insurance Program.

Coverage Gaps You Need to Address

Water backup from sewer systems and sump pump failures typically fall outside standard coverage unless you add a specific endorsement to your policy. Tree root damage, even when it causes foundation cracks, falls outside standard coverage because it results from natural growth rather than a sudden accident. These exclusions create real financial exposure for Minnesota homeowners, particularly those with basements, mature trees on their property, or properties in flood-prone areas. Your agent can explain which specific perils your policy covers and whether water backup, earth movement, or flood endorsements make sense for your property’s drainage patterns and soil conditions. Understanding these gaps now prevents costly surprises later when foundation problems emerge.

Protecting Your Foundation Before Damage Happens

Schedule Professional Inspections

Foundation problems in Minnesota homes are expensive to fix, but they’re far cheaper to prevent. The key is catching problems early through regular inspections and maintaining the drainage systems around your home. Most foundation damage starts small, with minor cracks or subtle settling that homeowners miss until the problem requires thousands of dollars in repairs. A professional foundation inspection costs between $300 and $500 and typically takes two to three hours. This inspection identifies cracks, settlement patterns, moisture intrusion points, and drainage failures before they become major structural issues. You should schedule a professional inspection if you notice doors or windows sticking, new cracks in basement walls, uneven floors, or water pooling around your foundation during heavy rains. Many structural engineers recommend inspections every three to five years for homes built before 1980 and every five to ten years for newer construction, though Minnesota’s freeze-thaw cycles and clay soils make more frequent checks worthwhile in our state.

Control Water Around Your Foundation

Drainage is your foundation’s best defense against water damage and settlement. Water pooling against your foundation is the single most controllable risk factor you face as a Minnesota homeowner. Install gutters and downspouts that direct water at least four to six feet away from your foundation, and maintain them by clearing leaves and debris each spring and fall. Slope the soil around your home away from the foundation at a grade of at least one inch per foot for the first ten feet, then level it out.

This simple grading prevents water from settling against your foundation walls. During dry periods, use a soaker hose around your home’s perimeter to keep soil from drying out and shrinking away from the foundation, which creates gaps where water enters when rain returns.

Manage Trees and Vegetation

Trim vegetation and grass close to the foundation to reduce moisture and discourage burrowing animals that tunnel under foundations and remove soil support. If you have mature trees within 20 feet of your home, have a certified arborist assess whether their root systems threaten your foundation. Tree root damage isn’t covered by insurance, so prevention through professional tree management is far more cost-effective than dealing with foundation cracks later.

Address Early Warning Signs Immediately

When you notice early warning signs like minor cracks or small water seepage, address them immediately with temporary repairs and professional assessment rather than waiting. Small cracks respond well to concrete sealant for under $100, while ignoring them allows water infiltration that worsens the damage exponentially over Minnesota winters. These proactive steps (inspections, drainage maintenance, and tree management) protect your home’s structural integrity and your wallet.

Final Thoughts

Foundation damage creates real financial stress for Minnesota homeowners, and whether homeowners insurance covers foundation issues depends entirely on what caused the problem. Sudden damage from covered perils like storms, fires, or vehicle impacts typically receives coverage under your dwelling protection, while gradual damage from soil movement, freeze-thaw cycles, tree roots, and poor drainage does not. This distinction matters enormously when you file a claim.

Your policy likely has significant gaps in foundation protection. Standard coverage excludes earth movement, water backup, and flood damage-yet these are precisely the threats Minnesota homeowners face most often. Water seeps through cracks during spring thaw, soil settles beneath your foundation during drought, and freeze-thaw damage from harsh winters all fall outside typical coverage. Adding endorsements for water backup and flood insurance through the National Flood Insurance Program fills these gaps and protects your home when problems arise.

The most effective strategy is prevention. Regular inspections catch small cracks before they become expensive repairs, proper drainage and grading around your foundation prevent water from settling against your walls, and managing trees and vegetation reduces moisture and pest damage. These steps cost far less than foundation repairs, which easily exceed $10,000 depending on damage severity. Contact Variant Insurance Group today for a personalized quote that addresses your foundation protection needs.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation