Property damage, liability claims, and unexpected losses can derail your financial security. We at Variant Insurance Group help Minnesota residents understand the different types of property and casualty insurance that protect what matters most.

Whether you own a home, drive a car, or run a business, knowing your coverage options makes a real difference. This guide walks you through the main policies available and how to pick the right protection for your situation.

What Property and Casualty Insurance Actually Protects

How Property and Casualty Coverage Works

Property and casualty insurance protects two distinct areas that safeguard your finances when accidents happen. Property coverage pays for damage to buildings, vehicles, personal belongings, and inventory from events like theft, fire, weather, or collisions. Casualty coverage handles liability when you bear responsibility for someone else’s injury or property damage, plus it covers medical expenses if someone gets hurt on your property. In Minnesota, where winters bring ice storms and spring thunderstorms cause significant damage, these two protection types work together to keep your assets safe from the specific risks our state faces.

Coverage Types Match Your Assets

Auto insurance protects your vehicle and covers liability if you cause an accident. Homeowners insurance shields the structure, contents, and liability exposure of your house. Business insurance combines property and liability protection tailored to your industry’s actual risks. Each policy type addresses the specific assets and exposures you face in your daily life.

How Property and Casualty Differs from Other Insurance

The critical difference between property and casualty coverage and life or health insurance comes down to what triggers a payout. Liability insurance covers responsibility you face, while life insurance pays a death benefit and health insurance covers medical expenses. Property and casualty insurance also differs fundamentally from general financial protection because it addresses specific perils and exclusions. Your homeowners policy won’t cover flood damage unless you add flood insurance as a separate policy, and your auto insurance won’t protect your business equipment parked at your office.

Why Minnesota Residents Face Real Exposure

Minnesota residents need property and casualty coverage because our state’s weather patterns create genuine exposure. The National Weather Service reports Minnesota experiences an average of 40 severe thunderstorms annually, and winter storms regularly cause property damage worth millions of dollars statewide. Without proper coverage, a single event like a house fire, vehicle collision, or liability claim could eliminate years of savings.

A gap in protection leaves you financially vulnerable when you need it most.

Understanding what each policy actually covers prevents costly gaps that expose your finances to risk. The next section walks you through the most common types of property and casualty coverage available to Minnesota residents and what each one protects.

Common Types of Property and Casualty Coverage

Homeowners Insurance: What Actually Gets Protected

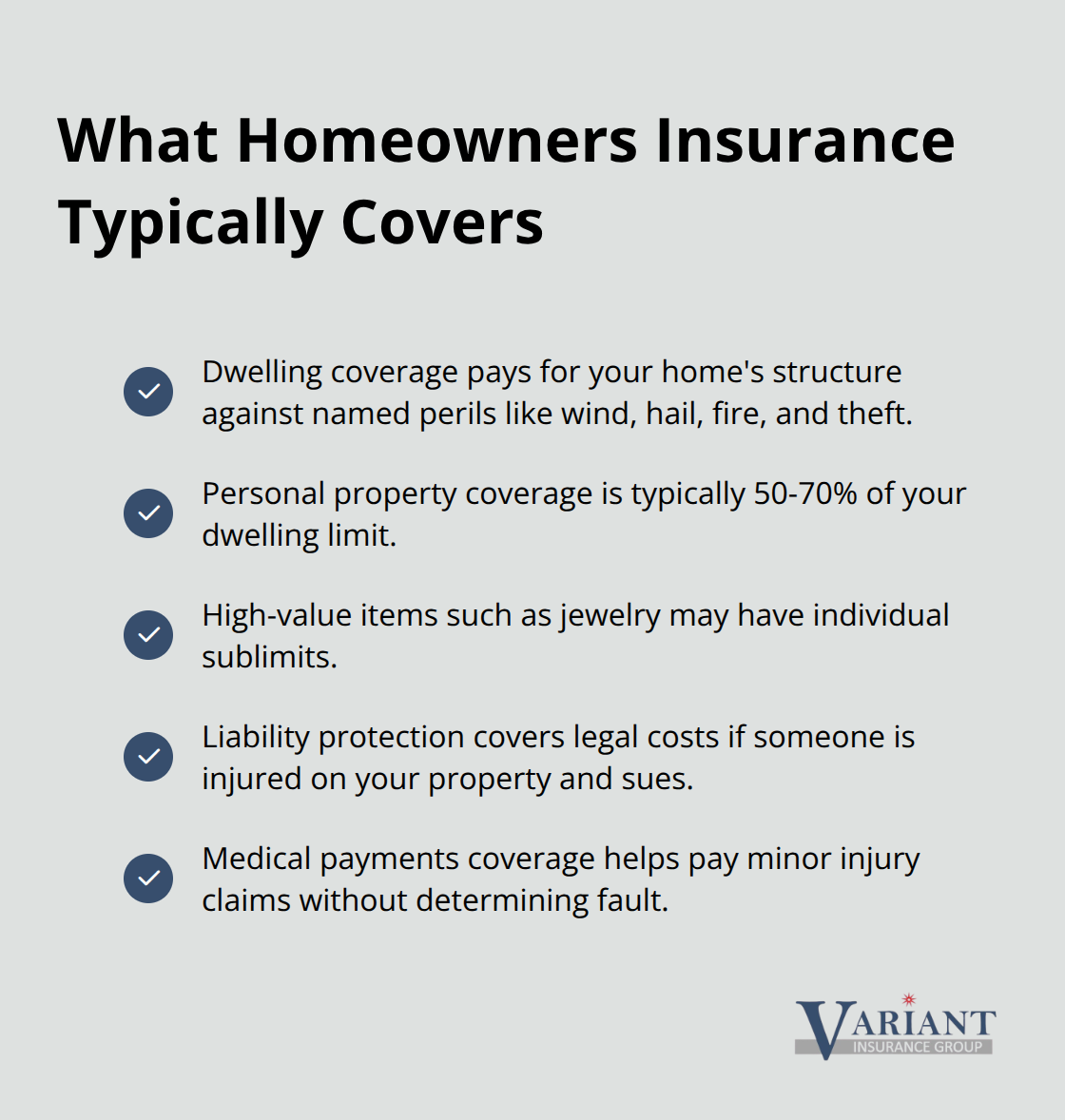

Homeowners insurance in Minnesota covers three critical areas that most people misunderstand. The dwelling protection pays for your home’s structure, but only for the specific perils listed in your policy-wind, hail, fire, and theft are standard, while floods and earthquakes require separate policies. Personal property coverage reimburses you for belongings inside your home, typically up to 50-70% of your dwelling limit, though high-value items like jewelry often hit individual limits. Liability protection covers legal costs if someone injures themselves on your property and sues you, and medical payments coverage pays minor injury claims without determining fault, which speeds up resolution.

Minnesota homeowners should verify whether their policy includes water damage from burst pipes, since winter conditions make this exposure real-standard homeowners policies do cover this, but sump pump failures and foundation seepage typically don’t.

Auto Insurance: Meeting Minnesota’s Requirements and Beyond

Auto insurance requirements vary by state, but Minnesota requires minimum liability limits of $40,000 per person for bodily injury. Collision and comprehensive coverage protect your vehicle itself, though these are optional if you own the car outright. Collision covers accidents and rollovers, while comprehensive handles theft, weather, and vandalism. If you financed or leased your vehicle, your lender requires both.

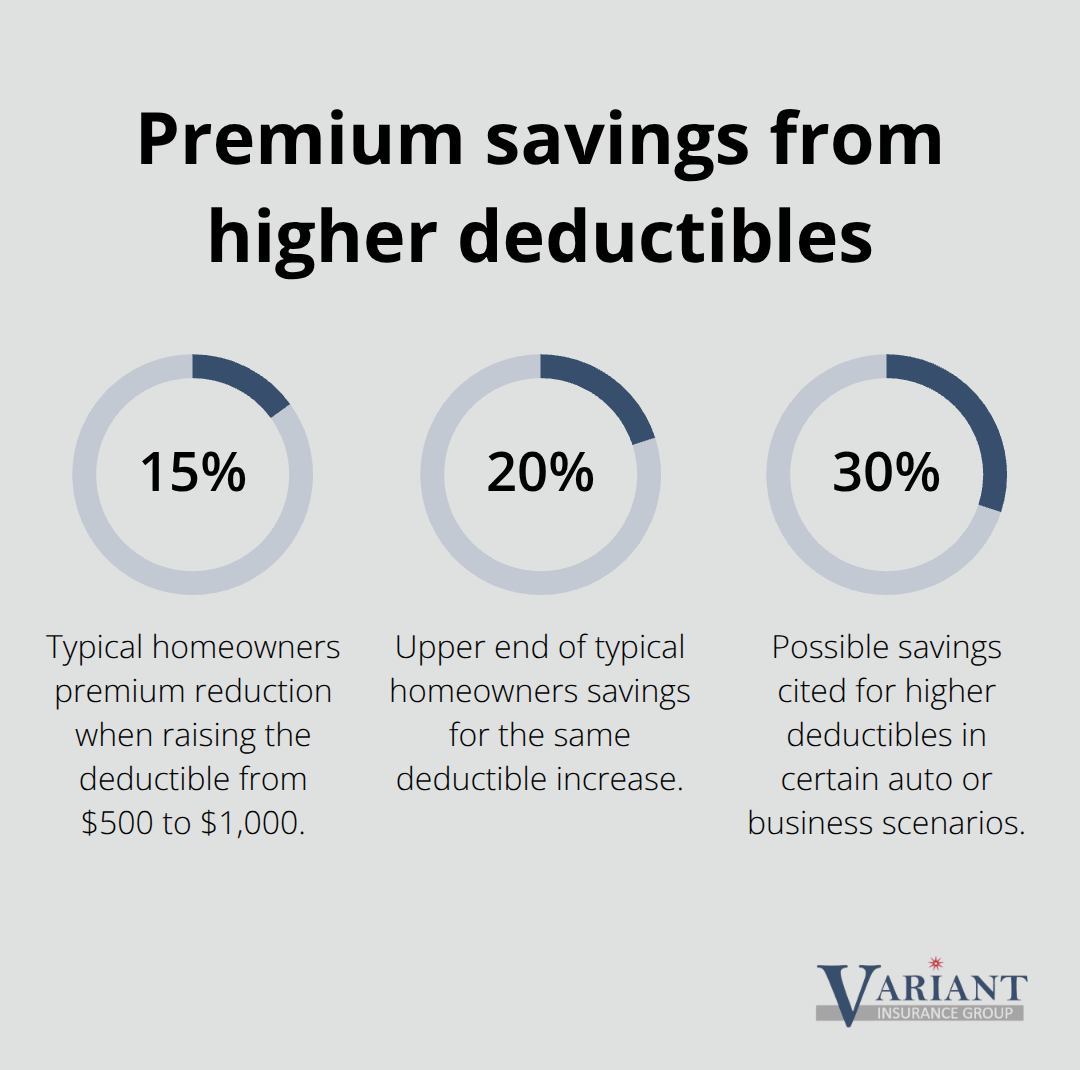

Choosing higher deductibles like $1,000 instead of $500 can lower your premium 15-30%, which makes sense if you have emergency savings set aside.

Business Insurance: A Legal Requirement with Real Teeth

Business insurance becomes mandatory the moment you operate as a sole proprietor or LLC, since your homeowners and auto policies exclude business activities. A small business needs property coverage for equipment and inventory, general liability for customer injuries or property damage claims, and workers’ compensation if you have employees. Minnesota requires workers’ compensation coverage for any business with employees, with no exemptions. The cost varies dramatically by industry-a landscaping company pays far more than a consulting firm due to injury risk.

Umbrella Policies: Affordable Protection Against Major Claims

Umbrella policies sit above your existing auto and homeowners limits, typically adding $1 million in liability coverage for $150-300 annually. These policies are underpriced relative to their protection; they cover gaps left by underlying policies and handle excess claims that exceed your standard limits. A Minnesota resident with significant assets should carry at least $1 million in umbrella protection, and families with teenage drivers should prioritize this coverage (given the elevated accident risk that age group faces).

Your specific situation determines which combination of these coverage types makes sense. The next section walks you through how to assess your actual assets and exposures so you can match the right policies to your real needs.

How to Match Your Coverage to What You Actually Own

Start With an Honest Inventory of Your Assets

Picking the right coverage starts with listing everything you own that needs protection: your house and its replacement cost, vehicles and their values, business equipment if you’re self-employed, and personal property inside your home. Minnesota residents often underestimate their exposure or overestimate their coverage limits, which creates gaps that cost thousands when claims happen. Replacement cost matters more than what you paid years ago-a house that cost $200,000 to build in 2010 might cost $350,000 to rebuild today due to labor and material inflation. Use online calculators or contact a local agent to estimate your home’s reconstruction cost, not its market value, since market value includes the land. For vehicles, check current market prices on Kelley Blue Book or NADA Guides rather than guessing. For business assets, inventory your equipment, tools, and stock at current replacement prices.

This step alone prevents the common mistake of underinsuring by 20-40%, which leaves you absorbing significant losses after a total loss event.

Match Your Deductible to Your Financial Cushion

Coverage limits and deductibles create a direct tradeoff that most people get wrong. Raising your deductible from $500 to $1,000 typically cuts your homeowners premium 15-20% annually, which means you break even on that higher deductible in five to seven years if you never file a claim-and most homeowners don’t file claims. However, a $2,500 deductible only makes sense if you have emergency savings to cover that amount without hardship. For auto insurance, Minnesota drivers with clean records should consider $1,000 collision deductibles if they have $5,000+ in emergency funds, since the premium savings compound over time.

Business owners face different math: a $5,000 deductible on property insurance might save 25-30% compared to $1,000, but a single equipment failure could cost more than those annual savings.

The key principle is matching your deductible to your financial cushion, not to what sounds reasonable.

Work With a Local Agent to Spot Coverage Gaps

An independent agent can shop multiple carriers simultaneously and show you exactly how different limit and deductible combinations affect both your premium and your actual protection. An agent also identifies coverage gaps you’d miss alone-like whether your homeowners policy covers sump pump failure or whether your business auto policy protects against liability costs. Local agents understand Minnesota’s specific risks, from hail damage frequencies by region to winter-related water damage patterns, which shapes smarter recommendations than national online quote systems that treat all states identically. Your financial situation and asset values change year to year, so these numbers warrant annual review.

Final Thoughts

Property and casualty insurance protects your finances when accidents happen, but only if you understand what each policy actually covers. The types of property and casualty insurance available to Minnesota residents address specific risks your home, vehicles, and business face throughout the year. Start by calculating your home’s replacement cost, not its market value, and list your vehicles at current market prices.

Determine whether your emergency savings can cover a higher deductible, since raising deductibles typically saves 15-30% annually on premiums. Review your existing policies to identify coverage gaps, particularly around flood damage, earthquake risk, or business-related exposures that your homeowners and auto policies exclude. Annual reviews matter because your assets, family situation, and financial cushion change year to year.

We at Variant Insurance Group work with Minnesota residents to match coverage to their actual needs rather than selling generic policies. Contact Variant Insurance Group to discuss your coverage needs with someone who knows your community and can help you make informed decisions about protecting what matters most.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation