Property and casualty insurance protects your home, business, and assets from financial loss. Whether you own a house in Minneapolis or run a business across Minnesota, understanding what property and casualty insurance means is the first step toward real protection.

At Variant Insurance Group, we help Minnesota property owners and business operators find policies that match their actual needs. The right coverage can mean the difference between recovering quickly from damage and facing serious financial hardship.

What Property and Casualty Insurance Actually Covers

Property Coverage Protects Your Assets

Property coverage pays for damage to buildings, structures, and personal belongings-it shields the things you own from loss. In Minnesota, comprehensive coverage protects your home and possessions from theft, fire, hail, and wind damage. Collision coverage pays for vehicle damage that results from impacts with other vehicles or objects, while comprehensive coverage for vehicles covers theft, fire, vandalism, glass breakage, and animal collisions. These protections work together to restore your property after damage occurs.

Casualty Coverage Shields You From Liability

Casualty coverage protects you from liability when someone else is injured on your property or when you accidentally damage someone else’s property. It also covers legal defense costs if you face a lawsuit. The Minnesota Commerce Department notes that bodily injury liability helps cover others’ medical costs after an accident and may protect you if sued. This protection matters because liability claims can be substantial, and legal fees add up quickly. Umbrella policies protect against liability claims that standard policies often exclude, keeping your savings account safe from expensive lawsuits.

Essential Add-Ons That Close Protection Gaps

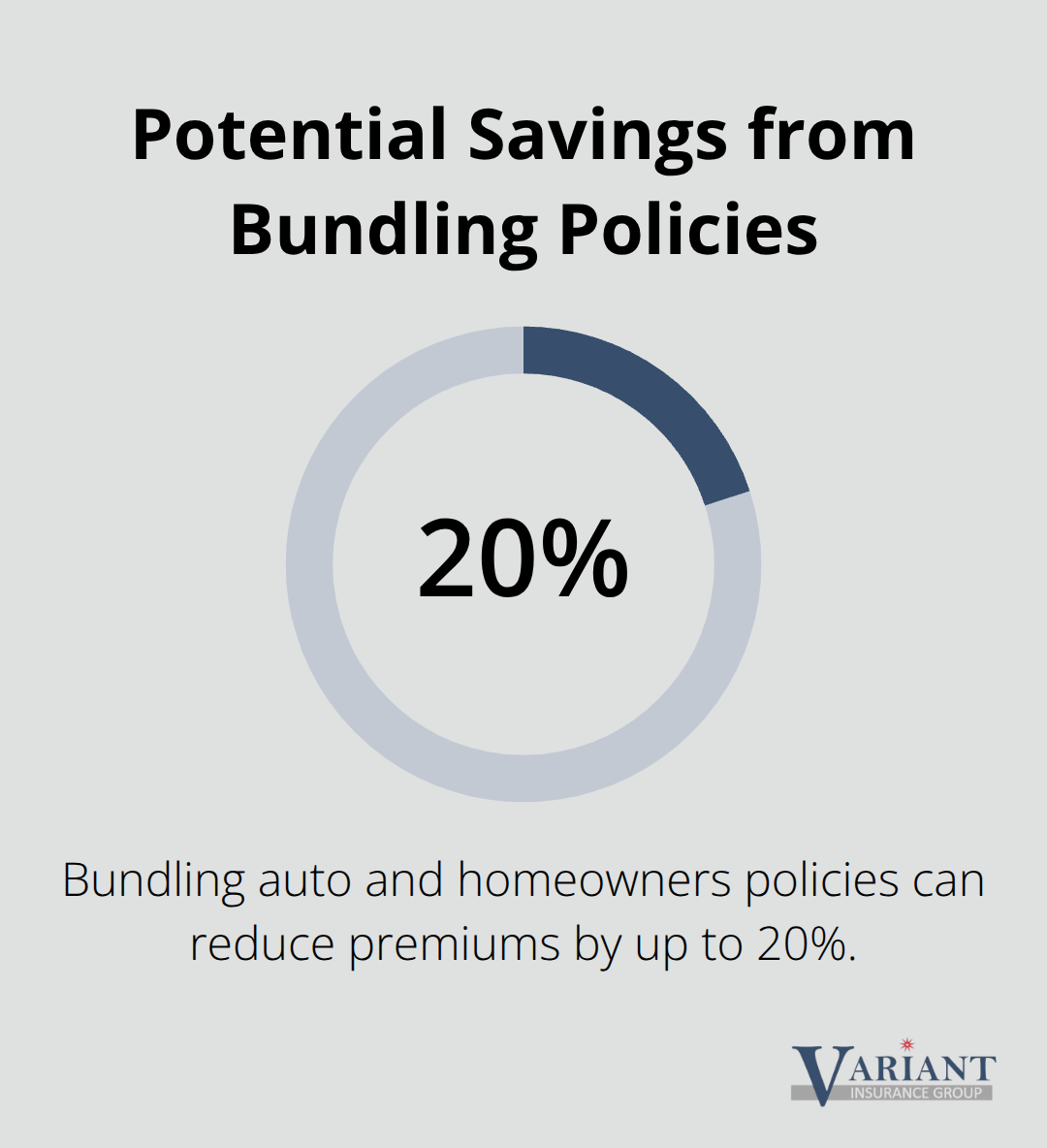

Uninsured and underinsured motorist coverage protects you if an at-fault driver lacks insurance or has insufficient coverage to pay your damages. Personal Injury Protection reimburses medical expenses and wage loss for you and your passengers regardless of fault, covering everything from emergency room visits to rehabilitation. Rental reimbursement coverage pays for a temporary vehicle while yours undergoes repair after a covered loss, keeping your life moving forward without transportation disruption. Roadside assistance provides tow service, lockout help, and fuel delivery when your car breaks down. Bundling auto and homeowners insurance can save you up to 20 percent on premiums according to industry data, making comprehensive coverage more affordable than you might expect.

Why These Protections Matter in Minnesota

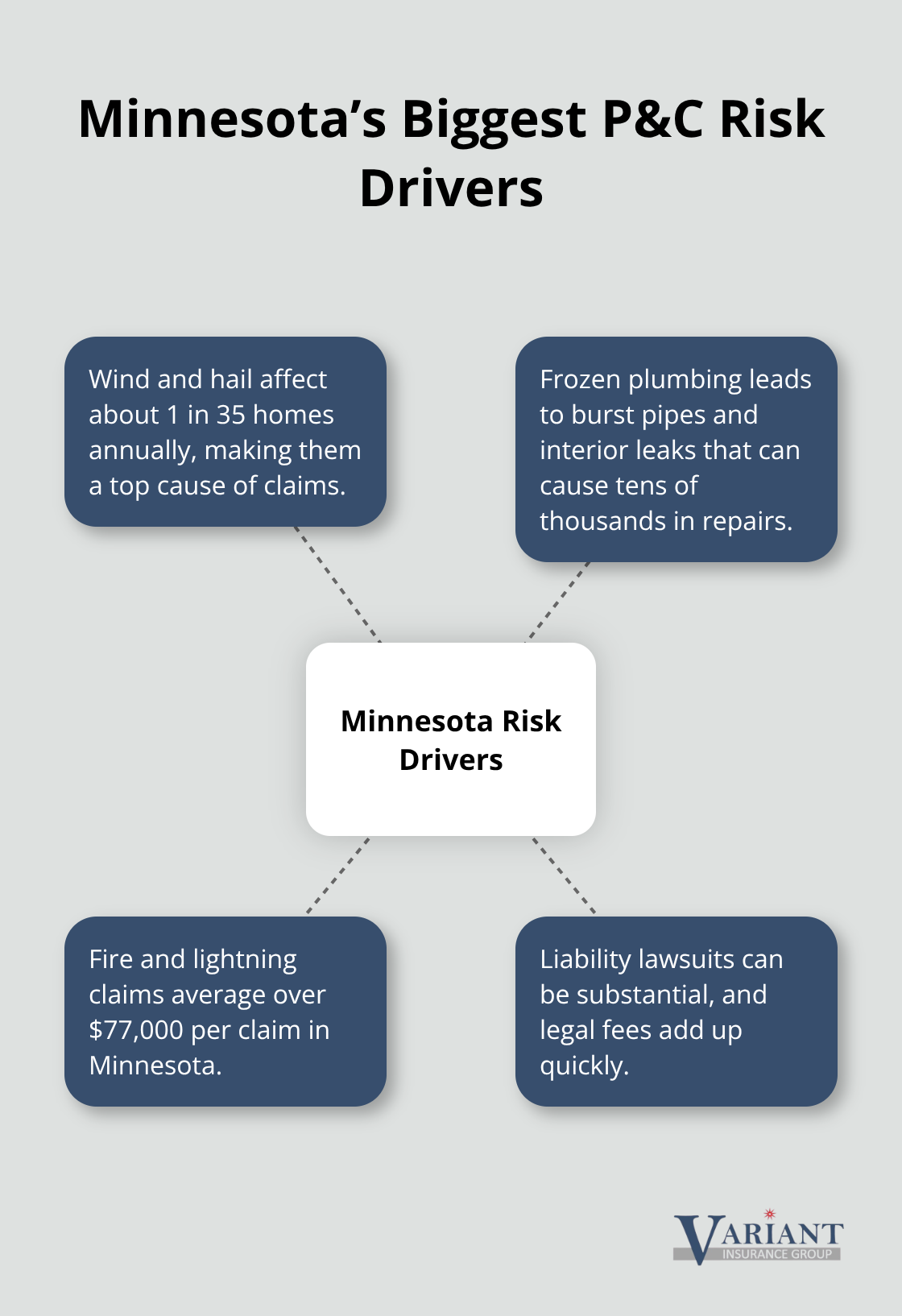

Minnesota weather creates specific risks that property and casualty insurance addresses directly. Wind and hail damage rank among the top home insurance claims year after year, affecting about 1 in 35 homes annually. Water damage from burst pipes and interior plumbing leaks drives significant claims, particularly during harsh winters when temperatures drop below freezing. Fire and lightning claims average over $77,000 per claim according to the Insurance Information Institute, making fire protection essential. The right combination of property and casualty coverage means you recover quickly from these events instead of facing financial hardship.

Finding the Right Coverage for Your Situation

The key is matching these protections to your actual situation rather than accepting standard policies that may leave gaps. Your home’s age, location, and construction materials affect which coverages matter most. Your driving habits, vehicle type, and claims history shape your auto insurance needs. At Variant Insurance Group, we shop Minnesota’s top-rated insurance companies to find policies that fit your exact circumstances. Understanding what property and casualty insurance covers helps you make informed decisions about which protections you truly need.

Why Minnesota Winters and Weather Make P&C Insurance Non-Negotiable

Wind and Hail Damage Hits Minnesota Homes Regularly

Minnesota’s climate creates property damage patterns that make comprehensive coverage essential rather than optional. Wind and hail affect about 1 in 35 homes annually across the state, ranking among the top insurance claims year after year. A single severe storm can strip shingles from your roof, shatter windows, and dent siding-damage that costs thousands to repair. Property coverage pays for these losses directly, transforming what could be a financial catastrophe into a manageable deductible. Without comprehensive protection, you absorb the full cost of storm damage from your own savings.

Winter Brings Burst Pipes and Water Damage

Winter brings burst pipes and water damage from frozen plumbing, with interior leaks driving significant claims that can reach tens of thousands of dollars in repairs. Minnesota’s harsh winters create ideal conditions for pipe freezing, especially in unheated spaces like basements and crawl spaces. A single burst pipe can flood your home and damage flooring, walls, and personal belongings within hours. Property coverage protects against these losses, but prevention matters too-insulating exposed pipes and maintaining adequate home heating reduce your risk substantially. The financial reality is stark: water damage claims often exceed $10,000, and comprehensive coverage prevents that loss from depleting your emergency fund.

Fire and Lightning Claims Reach Devastating Levels

Fire and lightning claims average over $77,000 per claim according to the Insurance Information Institute, making fire protection genuinely critical. Cooking accidents, faulty wiring, and heating equipment cause most residential fires in Minnesota. A house fire destroys not just the structure but also irreplaceable personal belongings and creates months of displacement while repairs occur. Property coverage rebuilds your home and replaces your possessions, allowing you to recover rather than start over from scratch. These aren’t theoretical risks-they happen to Minnesota homeowners regularly, and property coverage directly determines whether you recover financially or face serious hardship.

Liability Claims Protect Your Personal Assets

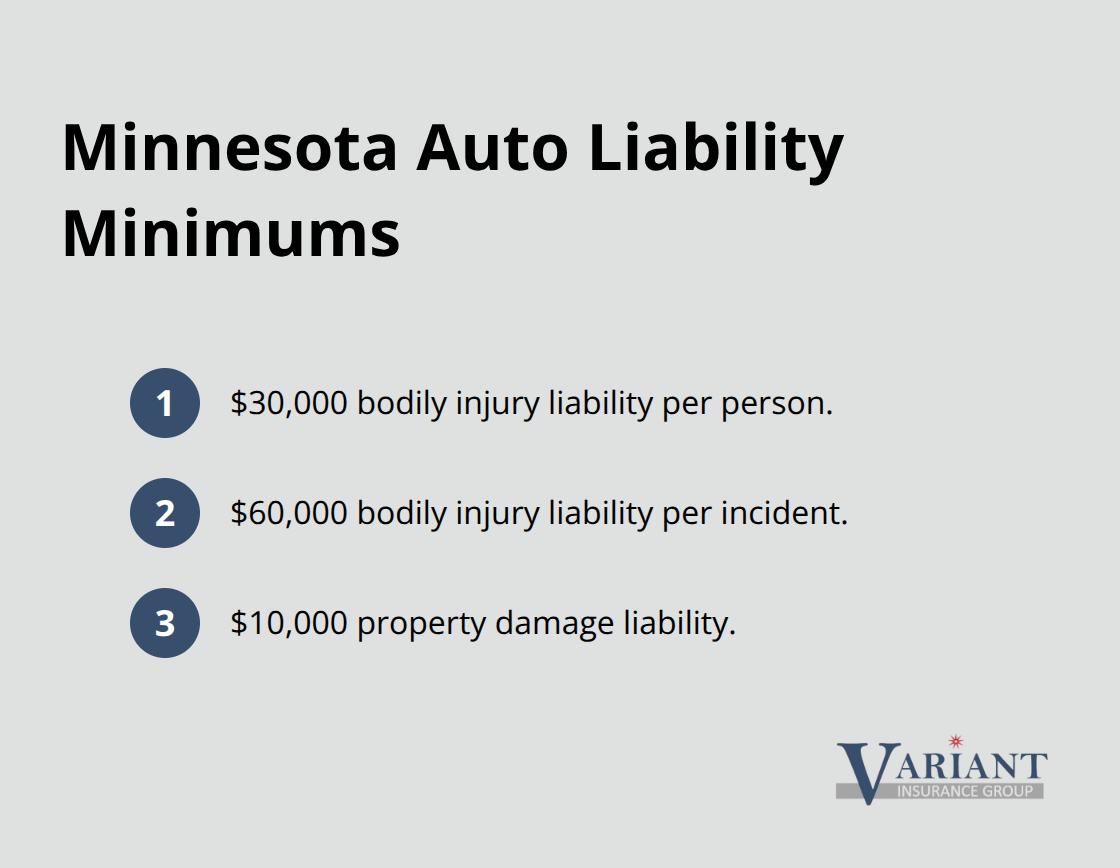

Liability claims add another layer of necessity that many homeowners overlook. If someone gets injured on your property or you accidentally damage someone else’s belongings, casualty coverage protects your personal assets from lawsuits. Minnesota law requires minimum liability coverage for vehicles, with bodily injury minimums of $30,000 per person and $60,000 per incident, plus $10,000 for property damage. Homeowners face similar legal expectations, and businesses operating in Minnesota must carry commercial property insurance to protect their operations and meet lender requirements.

Without proper coverage, a single accident or weather event can wipe out your savings and create decades of financial consequences.

Coverage Requirements and Financial Protection

The financial reality is straightforward: property and casualty insurance transforms catastrophic losses into manageable deductibles. When you own a home or operate a business in Minnesota, you face exposure to weather damage, liability claims, and unexpected events that occur without warning. Skipping comprehensive coverage saves a few dollars monthly but exposes you to losses that could exceed hundreds of thousands of dollars. Most mortgage lenders and business financing require proof of adequate coverage before approving loans, meaning proper P&C insurance is often a condition of homeownership and business operation. The key is ensuring your specific property and situation receive appropriate protection rather than accepting generic policies that leave gaps exactly where you need coverage most. As you evaluate your options, understanding which types of policies actually fit your circumstances becomes the next critical step.

Types of Property and Casualty Insurance Policies

Homeowners Insurance Covers Your Residential Property

Homeowners insurance protects residential buildings, personal belongings inside your home, and liability if someone gets injured on your property or you damage their possessions. The Minnesota Commerce Department notes that comprehensive coverage protects against theft, fire, hail, wind damage, and animal collisions, while collision coverage addresses impact damage from vehicles or objects. If you own a home in Minnesota, your mortgage lender requires proof of homeowners coverage before approving your loan, making this protection a non-negotiable condition of homeownership rather than an optional add-on.

Water damage from burst pipes, wind and hail damage affecting about 1 in 35 Minnesota homes annually, and fire losses averaging over $77,000 per claim according to the Insurance Information Institute make these protections genuinely necessary rather than theoretical. The coverage you select should match your home’s actual exposure-older homes with aging roofs face different hail and wind risks than newer construction, while homes in flood-prone areas need additional water damage protection beyond standard policies.

Commercial Property Insurance Protects Business Operations

Commercial property insurance operates differently because businesses face exposure that residential homeowners never encounter. Your commercial building, equipment, inventory, and business interruption losses all require separate protection from homeowners policies, which explicitly exclude business operations. If you operate a business from your home, standard homeowners coverage leaves you entirely unprotected for business property and liability-a dangerous gap that creates serious financial exposure.

Auto Insurance Addresses Vehicle and Driving Liability

Auto insurance completes the P&C picture by protecting your vehicle from collision damage, comprehensive losses like theft or weather, and liability if you injure someone or damage their property while driving. Minnesota requires minimum auto liability insurance of $30,000 per person and $60,000 per incident for bodily injury, plus $10,000 for property damage, but these minimums often fall short of actual damages from serious accidents. Adding uninsured and underinsured motorist coverage protects you when the at-fault driver lacks sufficient insurance, while Personal Injury Protection reimburses your medical expenses and wage loss regardless of fault.

Matching Coverage to Your Actual Situation

The practical reality is straightforward: homeowners policies protect residential property, commercial policies protect business operations and assets, and auto policies protect vehicles and driving liability. Bundling multiple policies with the same carrier saves up to 20 percent on premiums according to industry data, making comprehensive protection more affordable than purchasing policies separately. Understanding which coverage type addresses each area of your life prevents dangerous gaps where you assume you’re protected but actually carry no coverage whatsoever.

Final Thoughts

Property and casualty insurance meaning boils down to financial protection against the specific risks you face as a Minnesota property owner or business operator. Property coverage rebuilds your home and replaces your belongings after damage, while casualty coverage shields your personal assets when someone gets injured on your property or you accidentally damage theirs. Together, these protections transform catastrophic losses into manageable deductibles instead of financial devastation.

The practical challenge most Minnesota residents face isn’t understanding what property and casualty insurance covers-it’s finding the right combination of protections at a price that fits your budget. Standard policies often leave gaps exactly where you need coverage most, while over-insuring costs money you don’t need to spend. At Variant Insurance Group, we shop Minnesota’s top-rated insurance companies to find policies that match your actual situation rather than accepting generic coverage that may not fit your needs.

Contact Variant Insurance Group today to review your current coverage or start fresh if you’re uninsured. We work for you, not a single company, which means we can find the right carrier and pricing to fit your exact needs as your life changes. Our experienced professionals are ready to answer your questions and help you understand what you’re actually protected against.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation