Minnesota homeowners face unique insurance challenges, from heavy winter snow loads to unpredictable spring storms. Understanding your property insurance coverage types helps you protect what matters most without overpaying for unnecessary protection.

We at Variant Insurance Group created this guide to help you navigate dwelling coverage, personal property protection, and liability options specific to Minnesota’s climate and housing market. Let’s walk through what you actually need.

Dwelling Coverage and Structural Protection

What Dwelling Coverage Actually Protects

Dwelling coverage reimburses the cost to repair or rebuild your home’s structure after damage from covered perils. In Minnesota, this means protection against fire, lightning, windstorms, hail, theft, and vandalism according to the National Association of Insurance Commissioners. However, standard policies exclude flood and earthquake damage, which requires separate policies. Your dwelling coverage limit should equal your home’s full replacement cost, not its market value. Many Minnesota homeowners underbuy this coverage by basing limits on what they paid for the property years ago, then face a gap when rebuild costs surge. If your home cost $250,000 to purchase but would cost $350,000 to rebuild today due to labor and material inflation, your limit must reflect that higher number. Lenders require replacement cost coverage, not actual cash value, so verify your policy meets this standard. Attached structures like garages and decks fall under dwelling coverage, while detached sheds and fences typically require separate other structures coverage. Minnesota’s heavy snow loads and ice dams create specific damage patterns that your adjuster will assess under dwelling coverage, so photograph your home’s condition before winter arrives.

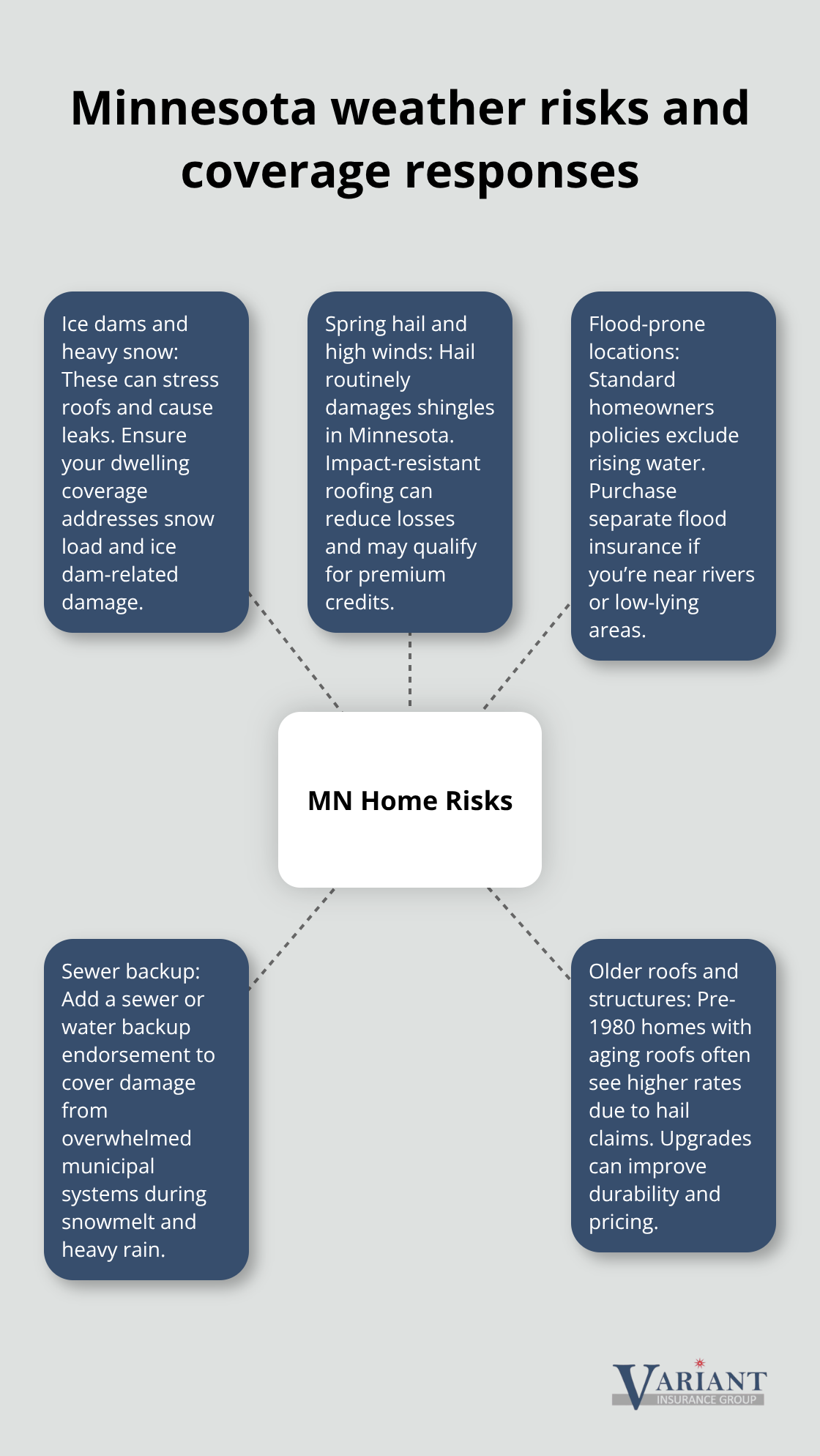

How Minnesota Weather Shapes Your Coverage Needs

Minnesota’s climate creates predictable damage patterns that affect both your coverage strategy and premiums. Winter storms cause roof damage from ice dams and snow weight, spring brings hail and high winds, and basement water intrusion happens year-round in certain areas. If your home sits in a flood-prone zone like areas near the Mississippi River or low-lying neighborhoods in the Twin Cities, flood insurance becomes essential because standard dwelling coverage excludes water damage from rising water. Sewer backup coverage, available as an endorsement in Minnesota, protects against spring snowmelt and heavy rain that overwhelm municipal systems. The Minnesota Department of Commerce notes that weather and geography drive higher claim frequency in certain areas, so your location directly affects both the coverage limits you need and your premium costs. Homes built before 1980 with aging roofs face higher rates because hail damage claims spike in Minnesota.

If you’ve upgraded to impact-resistant shingles or reinforced roof trusses, ask your insurer whether premium reductions apply, as these improvements lower your risk profile. Recent renovations also justify higher dwelling limits if you’ve added square footage or upgraded systems.

Setting the Right Dwelling Limit Without Overpaying

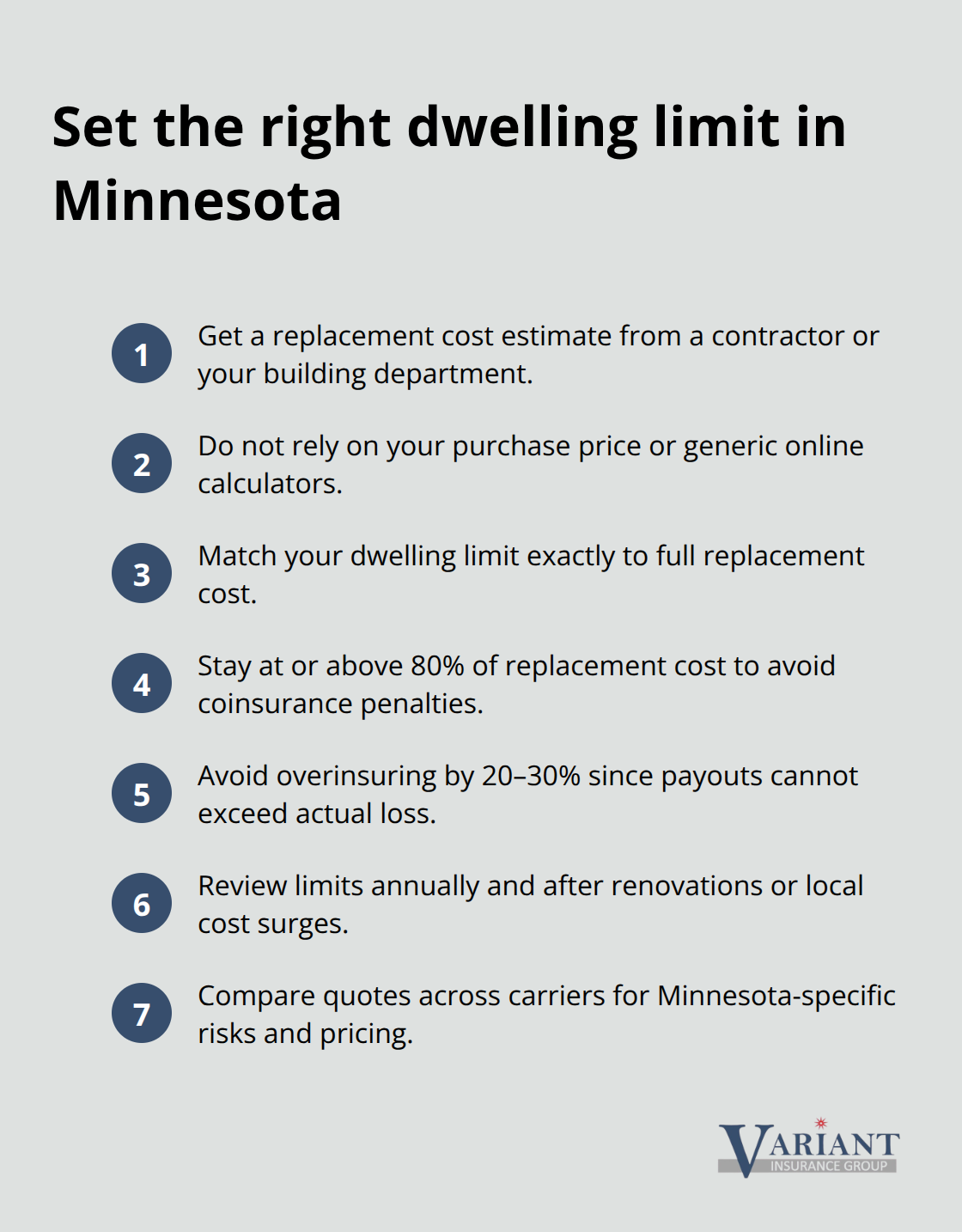

Start with a replacement cost estimate from a contractor or your municipality’s building department to understand current rebuild costs for your specific home type and size. Don’t rely on online calculators or your home’s purchase price. Minnesota homes built with wood frame construction typically cost $150 to $250 per square foot to rebuild, depending on finishes and location, according to construction industry data. A 2,000-square-foot home in the Twin Cities might require $300,000 to $500,000 in dwelling coverage depending on materials and complexity. Once you know the replacement cost, set your dwelling limit to match it exactly. Underinsuring creates a coinsurance penalty where the insurer pays less than your claim’s actual value if your limit falls below 80 percent of replacement cost.

If your home’s replacement cost is $400,000 but you insure it for only $320,000, and you suffer a $50,000 fire loss, the insurer might pay only $40,000 because you failed to insure to value. Overinsuring by 20 or 30 percent wastes premium dollars since you cannot collect more than actual damage costs. Review your dwelling limit annually, especially after home improvements or if your area experiences construction cost inflation. Multiple carriers price dwelling coverage differently based on how each assesses Minnesota-specific risks like ice dam damage and seasonal weather patterns, so comparing quotes across insurers helps you find the best value.

Understanding Coverage Limits and Valuation Options

Your policy offers two main valuation approaches: replacement cost (what it costs to rebuild today) and actual cash value (market value minus depreciation). Replacement cost coverage pays significantly more because it reflects current labor and material prices, while actual cash value leaves you short when rebuilding. Lenders require replacement cost coverage to protect their investment in your property. If you carry actual cash value coverage instead, you’ll face substantial out-of-pocket costs when you rebuild. Your dwelling limit also determines how much coverage you receive for other structures and personal property, since these typically calculate as percentages of your dwelling limit. A $400,000 dwelling limit might provide $40,000 for other structures (10 percent) and $200,000 for personal property (50 percent), so setting the correct dwelling limit cascades through your entire policy. Construction cost inflation in Minnesota has accelerated in recent years, making annual reviews essential to prevent coverage gaps. If your contractor estimates rebuild costs at $425,000 but your policy limit sits at $350,000, you face a $75,000 shortfall that no insurer will cover.

Moving Forward With Your Coverage Assessment

Once you’ve established the correct dwelling limit and valuation method, you’re ready to evaluate what personal property coverage and liability protection your household actually needs. Your dwelling foundation is solid, but your belongings and liability exposure require equally careful attention to avoid gaps in protection.

Personal Property and Liability Protection

What Your Belongings Actually Cost to Protect

Your dwelling coverage protects the structure, but your belongings inside that home require separate protection through personal property coverage, which typically covers 50 to 70 percent of your dwelling limit. If your dwelling limit is $400,000, standard personal property coverage provides around $200,000 to $280,000 for everything inside: furniture, electronics, clothing, kitchen appliances, and tools. This percentage-based approach works for average households, but Minnesota homeowners with valuable collections often discover they’re significantly underinsured.

High-value items like jewelry, art, firearms, or collectibles hit coverage caps that leave you short. A single piece of jewelry worth $8,000 might have a $2,500 limit under standard coverage, meaning you absorb the $5,500 loss yourself. The solution is scheduling these items separately on your policy, which removes the cap and insures them at their appraised value. Obtain professional appraisals for anything worth more than $5,000 and update them every three to five years as values change.

Your replacement cost and actual cash value refer to how your homeowners insurance policy reimburses you for property damage after a covered loss. A five-year-old laptop worth $400 new might fetch only $150 under actual cash value because depreciation reduces its value. Replacement cost eliminates this depreciation penalty and costs 10 to 15 percent more in premiums but protects your actual financial loss. Minnesota homeowners should strongly prefer replacement cost coverage for personal property since the premium difference is modest compared to the claim protection you gain.

Liability Coverage: Protecting Your Assets and Future Earnings

Liability and medical payments coverage protect you when someone else gets injured or their property gets damaged due to your actions. Personal liability coverage typically starts at $100,000 and covers legal costs and judgments if a guest slips on your icy driveway or your dog injures someone, while medical payments coverage pays minor medical bills for injured guests regardless of fault, usually capping at $1,000 to $5,000 per person.

A $100,000 liability limit sounds substantial until you realize that a serious injury lawsuit can easily exceed that amount; medical costs alone for major injuries often run $200,000 to $500,000. An umbrella liability policy providing $1 million in additional coverage costs only $150 to $300 annually and protects your home equity and future wages if a judgment exceeds your underlying liability limit. Minnesota homeowners with significant assets should carry at least $1 million in total liability protection across their homeowners and umbrella policies combined.

Water Damage Endorsements for Minnesota Homes

Sewer backup coverage, available as a Minnesota-specific endorsement, protects against spring snowmelt and heavy rain overwhelming municipal sewer systems-a genuine risk in many Twin Cities neighborhoods where backups cause thousands in basement damage. This endorsement typically costs $100 to $200 annually and covers $5,000 to $25,000 in damages, making it essential if your home has a basement or if your neighborhood has experienced backup issues.

Water backup from sump pump failure deserves similar attention: if your sump pump fails during a heavy rain event, water intrusion damages everything in your basement, and standard coverage excludes this scenario. Adding sump pump failure coverage protects against this specific Minnesota risk. Flood insurance remains separate from homeowners policies entirely and becomes mandatory if your property sits in a designated flood zone or if your lender requires it, covering water damage from rising water that standard policies explicitly exclude.

Your personal property and liability protections now form a complete picture of what happens inside your home and when accidents occur. The next step involves matching these coverage types to your specific household situation and understanding how deductibles and premium trade-offs affect your final policy design.

Choosing the Right Coverage for Your Situation

Assess Your Home’s Value and Risk Factors

Your dwelling limit and personal property coverage now rest on a foundation, but connecting these limits to your actual household risk requires honest assessment of what could happen and what you can afford to absorb. Minnesota homeowners often misjudge their risk by assuming their situation matches national averages, when in fact your neighborhood’s flood history, your roof age, and your claims history create a unique profile that demands specific coverage decisions.

Start by documenting what you own: walk through your home room by room and photograph high-value items, then add up replacement costs for furniture, electronics, clothing, and tools. Most Minnesota households discover their actual belongings exceed standard personal property limits by 20 to 40 percent, forcing a choice between increasing coverage or accepting underinsurance on certain items.

Your home’s construction type directly affects your premium and available coverage options. Wood frame homes cost less to insure than masonry or stone construction in Minnesota, but they face higher wind damage risk during spring storms. Homes built before 1970 with original wiring and plumbing systems pay substantially higher premiums because electrical fires and water damage claims increase with age.

Update Your Insurer After Home Improvements

If you’ve recently upgraded your roof, electrical panel, or plumbing, inform your insurer immediately because these improvements can reduce your premium by 5 to 15 percent depending on the carrier’s underwriting guidelines. Your claims history matters enormously: homeowners with zero claims in the past five years often qualify for loyalty discounts or better rates when shopping new insurers, while even one prior claim signals higher risk to underwriters and can increase premiums by 10 to 25 percent across the market.

Understand Deductibles and Premium Trade-Offs

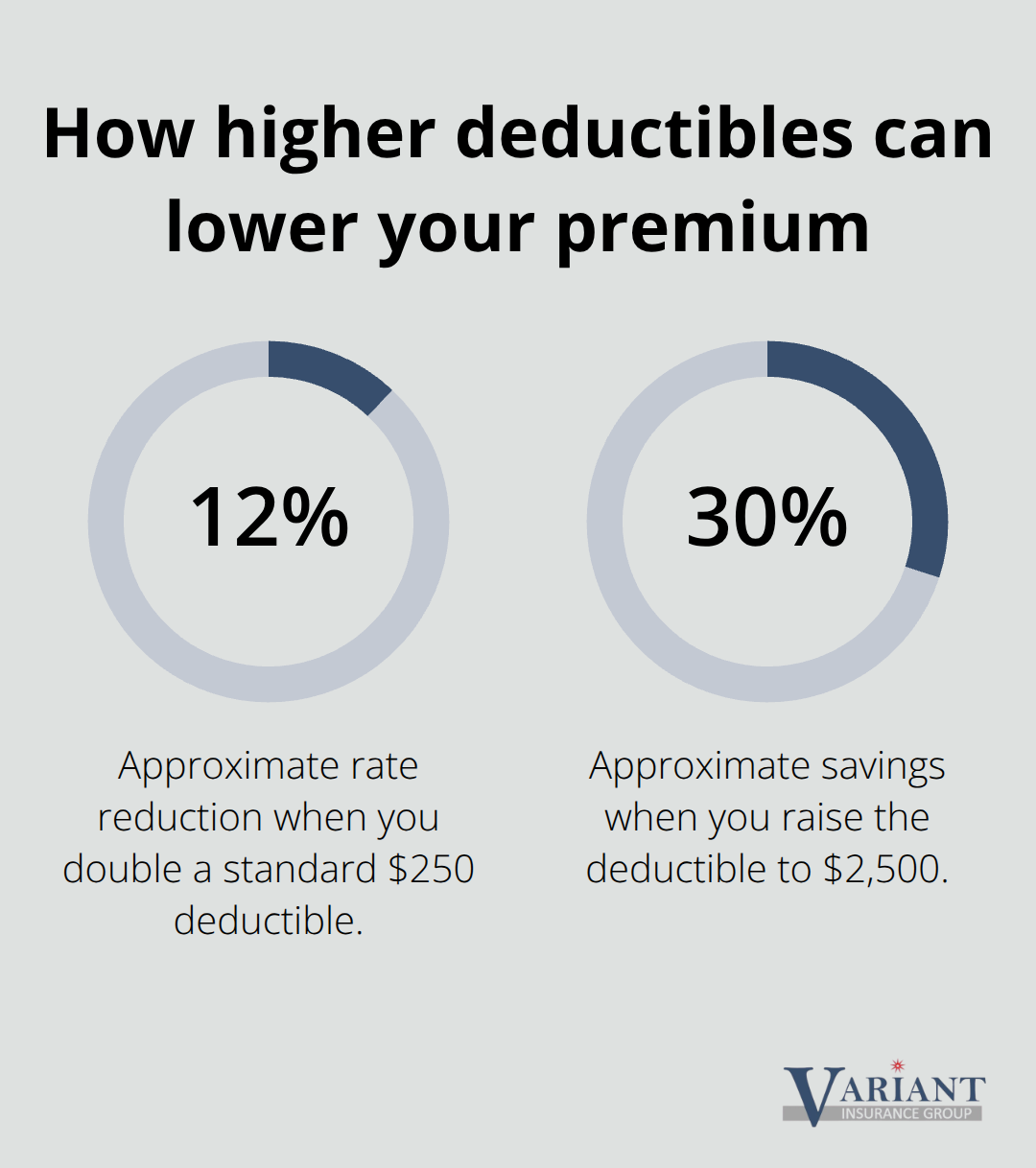

Deductibles represent the amount you pay out of pocket before insurance coverage kicks in, and this choice creates the most direct trade-off between monthly premium and actual protection. Doubling your deductible from the standard $250 can often reduce your rates about 12 percent; increasing the deductible to $2,500 can often save about 30 percent.

Minnesota homeowners with stable finances should seriously consider $1,000 or $1,500 deductibles because the premium savings compound over years of claim-free coverage. If you suffer one major loss, that deductible becomes irrelevant compared to the total claim payout, but if you never file claims, you’ve saved thousands in premiums while carrying adequate protection.

Conversely, choosing a $250 deductible costs you significantly more annually but only protects you during the rare event of a small claim; most insurers see claims averaging $15,000 to $25,000 in Minnesota, making the deductible nearly meaningless in real loss scenarios.

Compare Quotes Across Multiple Carriers

Obtain quotes at multiple deductible levels from at least three different carriers because each insurer prices these trade-offs differently based on their claims experience and underwriting appetite. Some carriers heavily discount high deductibles while others show minimal savings, so comparing actual numbers rather than assuming standard rate structures prevents you from overpaying.

Once you’ve selected appropriate dwelling and personal property limits with a deductible that matches your financial capacity, add umbrella liability coverage if your household income exceeds $75,000 annually or if you own significant assets, because this protection costs remarkably little for the exposure it covers.

Final Thoughts

Property insurance coverage types work together to create a complete safety net for your Minnesota home, but only when you match each component to your actual situation. Dwelling coverage protects your structure, personal property coverage protects your belongings, and liability coverage protects your assets when accidents happen. Most Minnesota homeowners treat these decisions as one-time events rather than annual reviews that reflect changing home values, renovation investments, and life circumstances.

Your dwelling limit must equal your home’s full replacement cost, not its purchase price from years ago, and your personal property coverage should reflect what you actually own with scheduled endorsements for high-value items that exceed standard limits. Minnesota’s climate creates specific risks that generic national insurance advice misses entirely: ice dams, spring flooding, sewer backups, and hail damage follow predictable patterns in our state, making sewer backup endorsements and flood insurance essential for many properties. Your location within Minnesota matters enormously (a home near the Mississippi River faces different flood exposure than a home in western Minnesota), and these differences should drive your coverage decisions.

We at Variant Insurance Group work with Minnesota homeowners to review their current coverage against their actual risk profile and rebuild costs. Contact us to schedule a coverage review and ensure your property insurance coverage types protect what matters most without leaving gaps or overpaying for unnecessary protection.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation