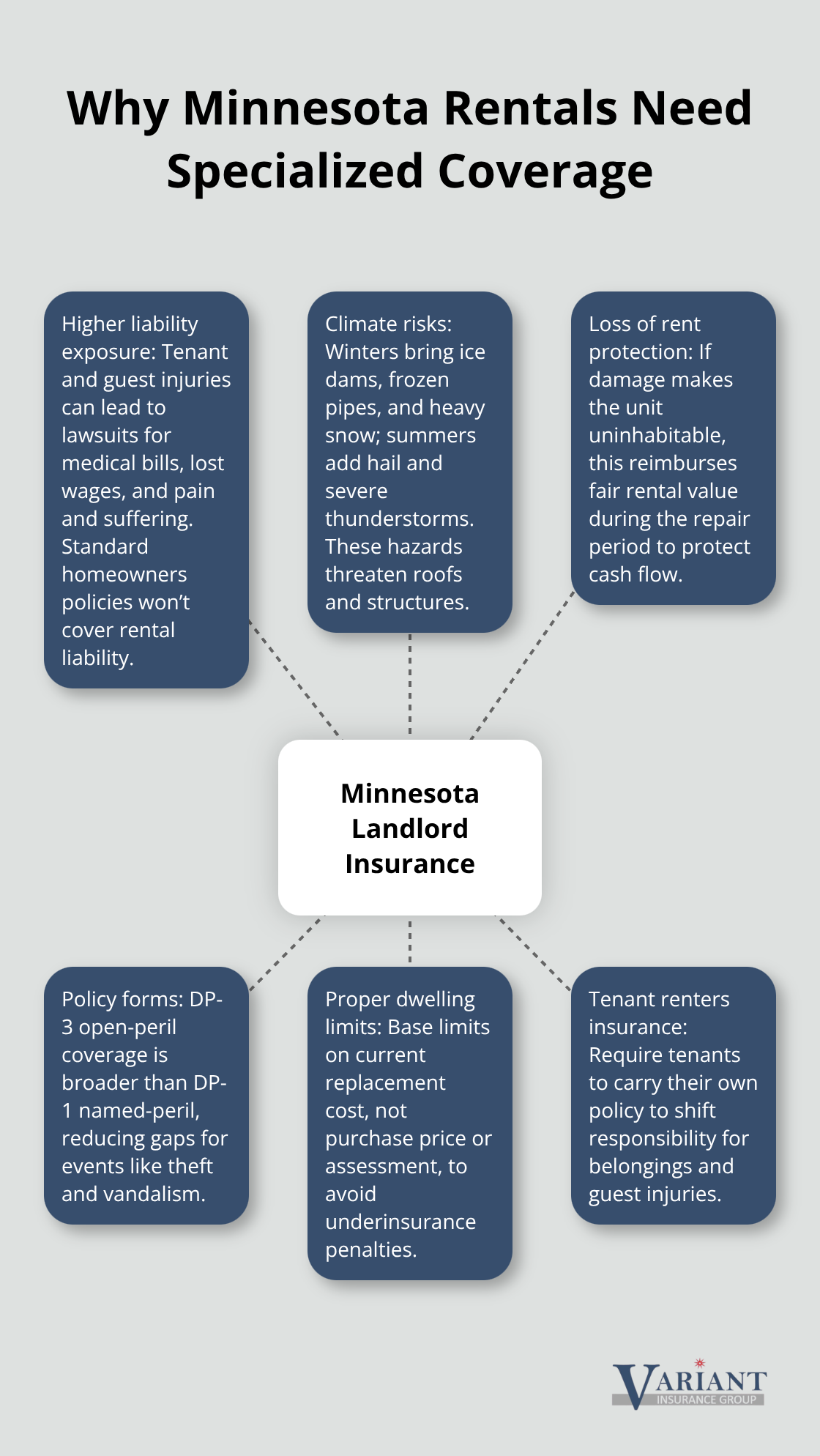

Owning a rental property in Minnesota comes with real financial exposure. Standard homeowners insurance won’t protect you against the unique risks landlords face, from tenant-related liability to lost rental income.

We at Variant Insurance Group see landlords make costly coverage mistakes every year. The right home insurance for rental property can be the difference between protecting your investment and facing devastating losses.

What Is Landlord Insurance

How Landlord Insurance Differs from Homeowners Insurance

Landlord insurance is a specialized property policy designed specifically for rental properties, and it differs fundamentally from standard homeowners insurance in both coverage and purpose. Homeowners insurance protects an owner-occupied primary residence and covers the dwelling, personal belongings, liability, and additional living expenses if you must leave temporarily. Landlord insurance protects the rental dwelling structure and covers liability for tenant and guest injuries, but it does not cover tenants’ personal property-that responsibility falls to them through renters insurance. The most critical difference is loss of rent coverage, which reimburses you for lost rental income when a covered event makes the property uninhabitable. In Minnesota, landlord insurance is not legally required by state law, but if your property has a mortgage, your lender almost certainly requires it.

Coverage Costs and Policy Types

Average annual premiums in Minnesota range from around $800 to $2,000 depending on location, property condition, age, and the specific coverages you select. A DP-3 dwelling policy, which is standard for rental properties, typically offers broader protection with open-peril coverage for the building itself, meaning it covers all perils except those specifically excluded. Older DP-1 policies use named-peril coverage and often require costly add-ons for water damage, theft, and vandalism.

Why Rental Properties Demand Higher Coverage

The core reason landlords need this coverage is straightforward: rental properties carry higher liability exposure and income risk than owner-occupied homes. A tenant or guest injured on your property can sue you for medical bills, lost wages, and pain and suffering-liability claims that standard homeowners insurance will not cover for a rental property. Minnesota’s harsh winters create persistent climate risks including ice dams, frozen pipes, and heavy snow loads, while summer brings hail and severe thunderstorms that can damage roofs and structures.

If your property sustains damage from fire, storm, or vandalism and requires repairs, loss of rent coverage pays your fair rental value for the shortest reasonable repair period, protecting your cash flow during downtime.

Setting Proper Dwelling Limits and Roof Considerations

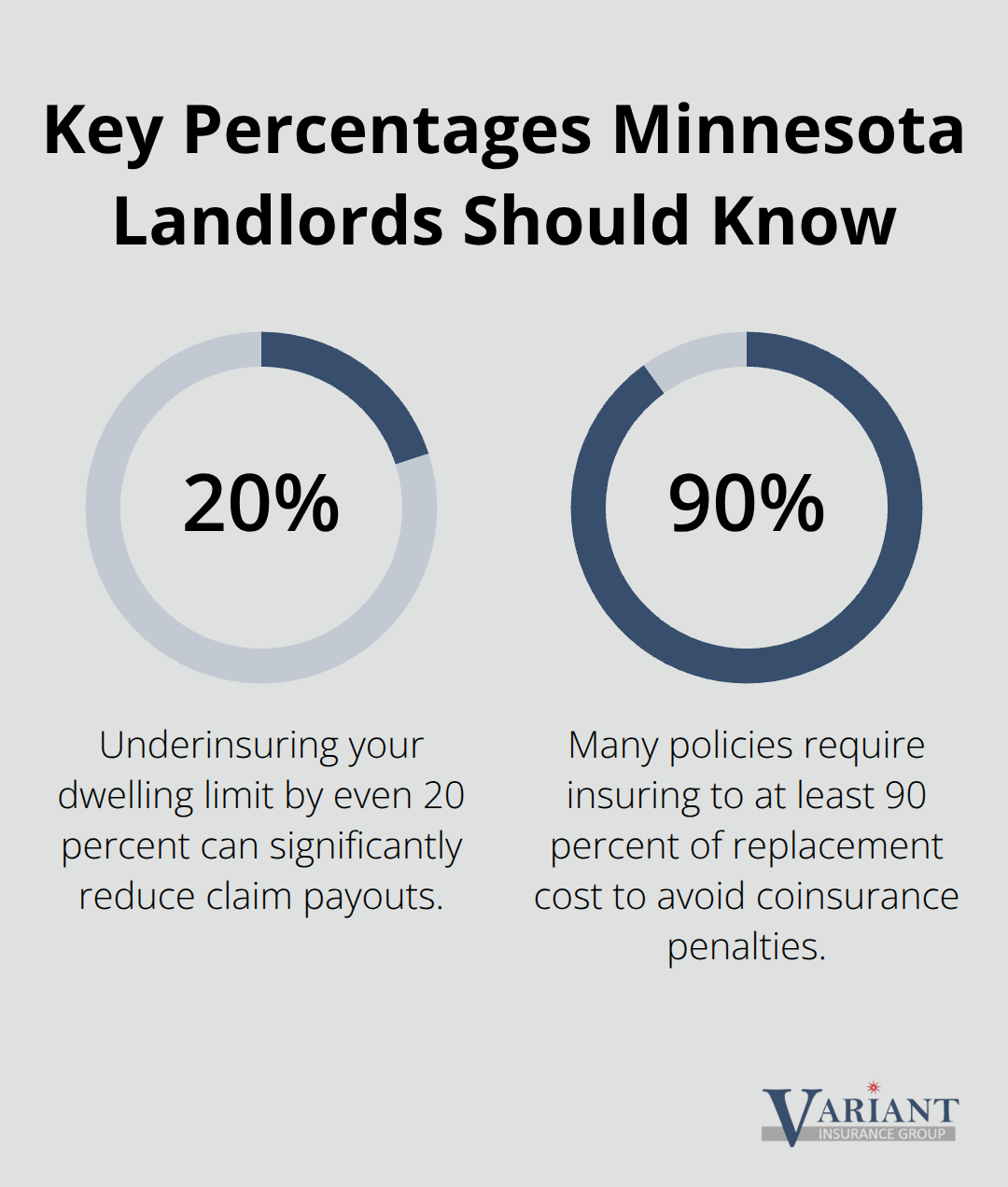

You must verify your dwelling limits reflect current rebuild costs, not just the property’s purchase price or assessed value-underinsuring by even 20 percent can significantly reduce claim payouts. Property condition matters: older roofs may settle for actual cash value rather than replacement cost under some policies, so clarify how your roof age affects claim settlements. Detached structures like garages or sheds should be explicitly included in your coverage or added as endorsements to avoid gaps.

What Comes Next

Understanding the specific coverage options available in Minnesota helps you move beyond the basics and select the protections that match your property’s actual risks and your financial situation.

What Coverage Do You Actually Need for a Minnesota Rental Property

Dwelling Coverage Protects Your Building Structure

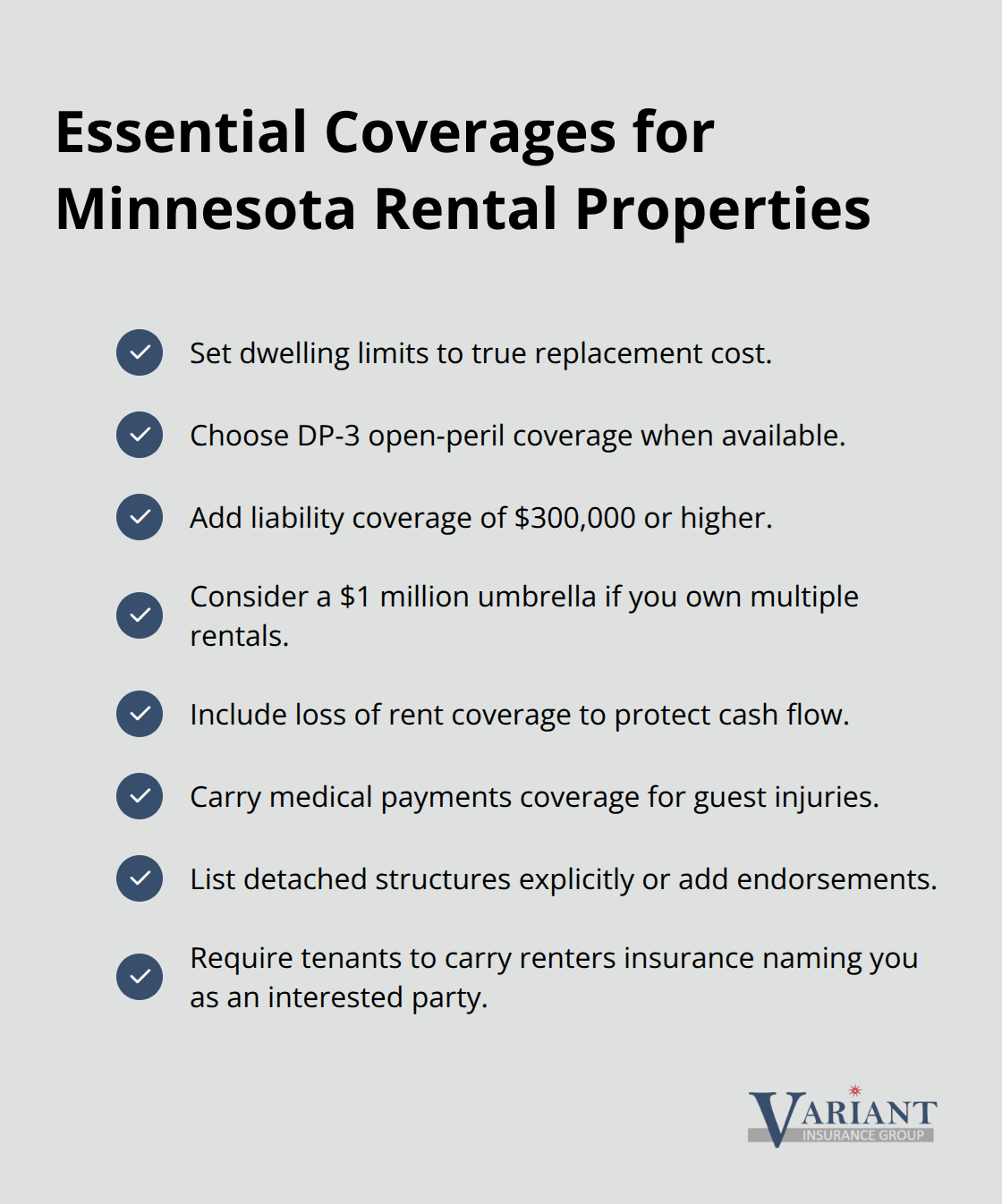

Dwelling coverage protects the physical structure of your rental property, including the walls, roof, foundation, and permanently attached systems like electrical and plumbing. In Minnesota, this coverage matters intensely because winter damage alone can cost thousands-ice dams cause interior water damage, frozen pipes burst unexpectedly, and heavy snow loads stress roof structures. When you select dwelling limits, base the amount on current replacement costs, not your purchase price or property tax assessment. A 1,500-square-foot home in the Twin Cities might cost $250,000 to $350,000 to rebuild depending on finishes and location, so your dwelling limit should reflect that number.

Open-Peril vs. Named-Peril Protection

DP-3 policies cover these perils under open-peril protection, meaning the insurer pays for damage from any cause unless specifically excluded-fire, wind, hail, theft, and vandalism are standard. Actual cash value settlements on older roofs may disappoint you after a loss, so request replacement cost coverage if available; this pays what it actually costs to rebuild or repair, not what the damaged item is worth on the resale market. Detached structures like garages or sheds require explicit inclusion in your coverage or endorsements to avoid gaps.

Liability Coverage Shields You from Tenant and Guest Injuries

Liability coverage on a landlord policy protects you when a tenant or guest is injured on your property and sues for medical expenses, lost income, or pain and suffering. Minnesota courts have awarded substantial judgments in premises liability cases, making this protection non-negotiable. Most DP-3 policies include $100,000 to $300,000 in liability coverage, but if you own multiple properties or have significant assets, umbrella liability coverage extending $1 million or more across all your rentals is worth the modest premium cost.

Medical Payments and Loss of Rent Coverage

Medical payments coverage, typically $1,000 to $5,000 per person, pays a guest’s immediate medical bills without requiring a lawsuit-this goodwill gesture often prevents litigation. Loss of rent coverage reimburses your fair rental value during repairs after a covered event; if your property rents for $1,500 monthly and sits vacant for three months due to fire damage, this coverage pays $4,500. This protection directly shields your cash flow and separates landlord policies from homeowners insurance, which offers no income replacement.

Tenant Renters Insurance Requirements

Require tenants to carry renters insurance naming you as an interested party; this shifts responsibility for their belongings and guest injuries to them, reducing your exposure significantly. The right combination of dwelling, liability, and loss of rent coverage creates a foundation that protects your investment, but common mistakes can undermine even the best policy structure.

What Landlords Get Wrong About Coverage

Underinsuring Based on Purchase Price, Not Rebuild Costs

The most expensive mistake landlords make involves setting dwelling limits based on what they paid for the property or what the county assessor values it at, rather than what it actually costs to rebuild. A property purchased for $280,000 in 2015 might cost $380,000 to rebuild today due to inflation in labor and materials, yet the owner still carries a $280,000 limit. When fire destroys that home, the insurance company applies coinsurance penalties for underinsurance, which means the property must be insured to at least 90 percent of the replacement cost. Contact a local contractor or use online rebuild cost estimators specific to your property type and location, then set your dwelling limit to match that figure, not the purchase price.

Treating Liability Coverage as an Afterthought

Liability coverage often gets treated as secondary, with landlords accepting whatever minimum the insurer offers without question. A single serious injury claim can exceed $500,000 in medical costs plus pain and suffering awards, yet many Minnesota landlords carry only $100,000 in liability protection. If a tenant’s guest slips on ice in your entryway and breaks their spine, you face a lawsuit that can attach your personal assets. Umbrella liability coverage extending to $1 million across all your properties costs roughly $200 to $400 annually and should be non-negotiable if you own more than one rental.

Failing to Update Coverage When Property Use Changes

Landlords fail to notify their insurance company when property circumstances change, creating gaps that leave claims vulnerable to denial. When you convert a long-term rental to short-term Airbnb hosting, switch from a single-family rental to a duplex, add a new detached structure, or change tenant occupancy types, your existing coverage may no longer apply. Insurance companies investigate occupancy and use carefully during claims, and if your property is listed on Airbnb but your policy covers only long-term rentals, expect the claim to be rejected. Minnesota landlords must contact their agent immediately whenever property use changes, not months later when filing a claim. The cost to adjust coverage is minimal compared to having a major claim rejected due to occupancy misrepresentation.

Working with Local Expertise to Prevent Costly Errors

An experienced local agent who understands Minnesota’s rental landscape helps prevent these costly errors before they happen. At Variant Insurance Group, we shop Minnesota’s top-rated insurance companies to find policies that match your specific property risks and occupancy type. Our team reviews your options and compares protection and prices to help you avoid the coverage gaps that lead to denied claims.

Conclusion

Protecting a Minnesota rental property requires the right home insurance for rental property that shields your investment from tenant liability, weather damage, and lost income when repairs force vacancy. Underinsuring, ignoring liability exposure, and failing to update coverage when circumstances change cost landlords thousands in denied claims and out-of-pocket losses. Contact Variant Insurance Group for a personalized review of your rental property coverage.

Our local agents walk through your dwelling limits, liability protection, and loss of rent coverage to confirm you have adequate protection. We shop Minnesota’s top-rated insurance companies to find policies that match your property type, occupancy classification, and financial situation. We work for you, not a single insurance company, which means we find the right carrier and pricing to fit your exact needs as your rental business grows or changes.

Your investment deserves protection that actually covers what matters. Whether you own a single-family rental in the Twin Cities, a multi-unit property in Rochester, or a short-term rental near the University of Minnesota, we compare protection and pricing to help you avoid coverage gaps. Reach out to our team today to get started.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation