Your property insurance deductible is one of the most important decisions you’ll make when protecting your home. It directly affects both your monthly premium and what you’ll pay out of pocket when damage occurs.

At Variant Insurance Group, we help Minnesota homeowners understand how deductibles work so you can choose the right amount for your situation. This guide walks you through the basics and shows you how to balance affordability with adequate coverage.

What Is a Property Insurance Deductible

Your deductible is the amount you pay out of pocket before your insurance company covers the rest of a claim. If a storm damages your roof and costs $8,000 to repair, and your deductible is $1,000, you’ll pay that $1,000 first. The insurer then covers the remaining $7,000 (subject to your policy limits and terms). This shared responsibility exists because it prevents small claims from flooding insurers with paperwork and keeps everyone’s premiums lower. In Minnesota, standard deductibles typically range from $500 to $2,000, though some homeowners choose higher amounts to reduce their monthly costs. The deductible applies per claim, meaning if you have two separate incidents in one year, you’ll owe the deductible for each one.

How Your Deductible Affects Monthly Costs

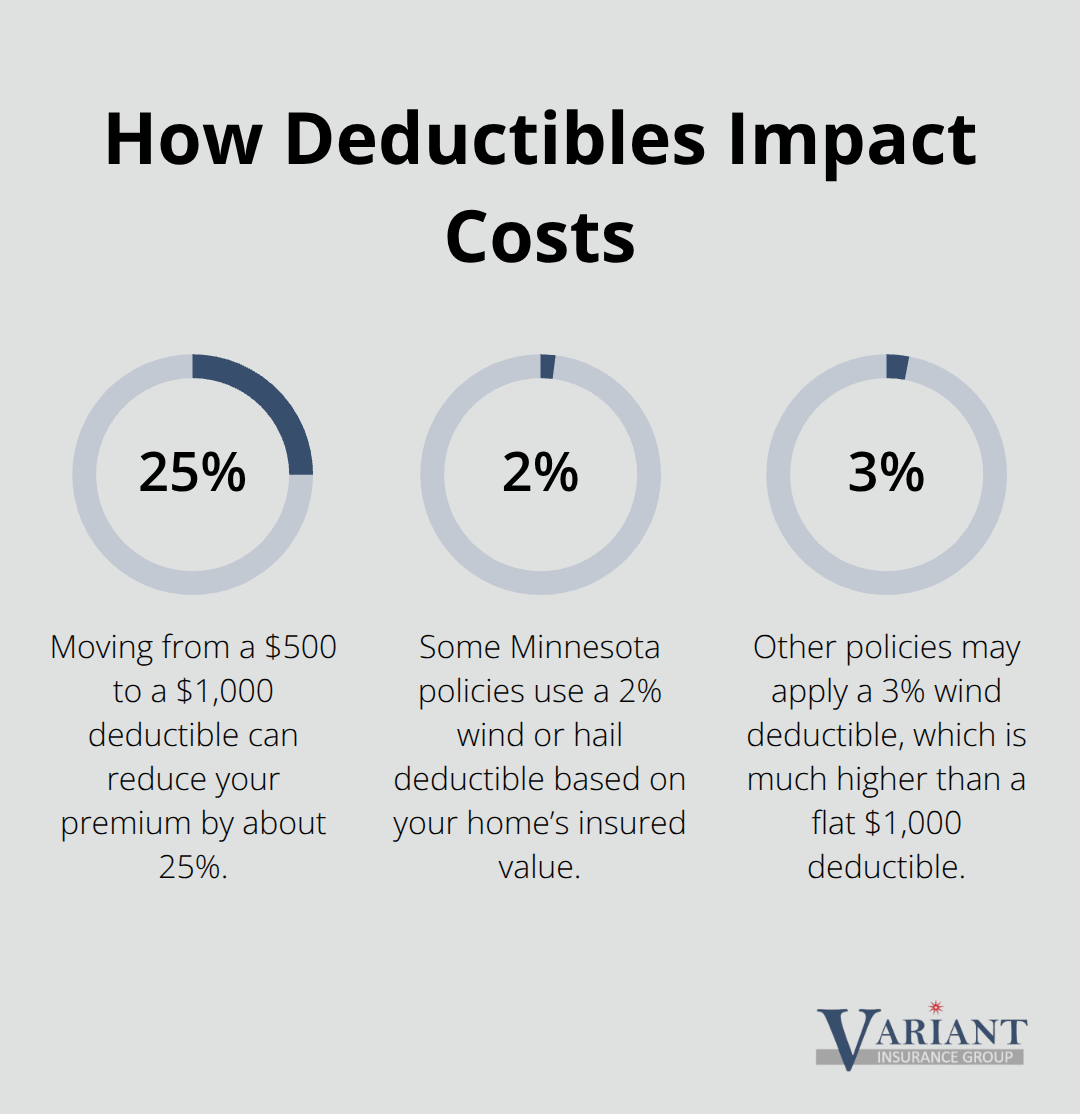

Raising your deductible lowers your premium, but the math matters more than the theory. An increase from $500 to $1,000 could result in premium savings of about 25%. On a $1,200 annual homeowners policy, that could save $120 to $180 per year. However, that savings only makes sense if you can actually afford to pay the higher deductible when damage occurs. A homeowner with $10,000 in emergency savings can comfortably handle a $2,000 deductible and pocket the premium savings.

Someone living paycheck to paycheck should stick with a $500 or $750 deductible, even if it costs more monthly, because they cannot absorb a large out-of-pocket hit.

Finding Your Break-Even Point

Calculate your break-even point to make the right choice. Divide the annual premium savings by the deductible increase to see how many years it would take for the savings to equal the higher deductible. If you’d need five years of premium reductions to break even on a $1,000 higher deductible, but you only plan to stay in your home for three years, the math does not work. This calculation prevents you from choosing a deductible that looks good on paper but creates financial stress in reality.

Deductibles for Specific Types of Damage

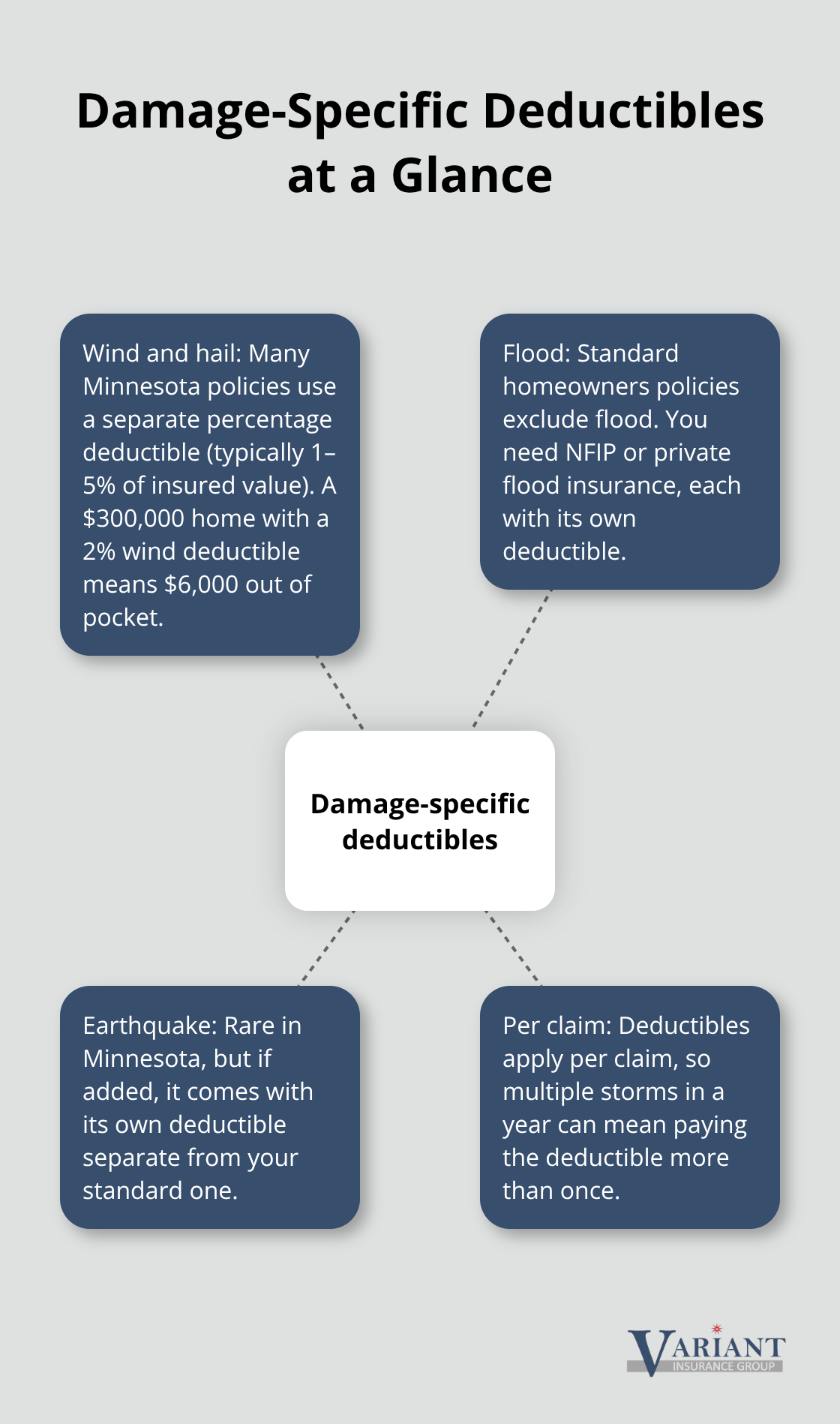

Not all damage follows the same deductible rules. Wind and hail claims in Minnesota often trigger a separate deductible, typically 1 to 5 percent of your home’s insured value. If your home is insured for $300,000 and you have a 2 percent wind deductible, a hail-damaged roof claim would cost you $6,000 out of pocket instead of your standard $1,000. Flood damage is excluded from standard homeowners policies entirely, so you must purchase separate flood insurance through the National Flood Insurance Program or a private carrier, each with its own deductible structure.

Earthquake coverage, though rare in Minnesota, also comes with its own deductible if you add it.

Reviewing Your Policy Before Claims Happen

Before you face a claim, review your policy documents to identify which perils have special deductible amounts and whether those separate amounts align with your financial comfort level. This detail often surprises homeowners during claims, so asking your agent upfront saves frustration later. Understanding these variations now means you won’t face unexpected out-of-pocket costs when you need your coverage most. With your deductible structure clear, you’re ready to explore how to select the right amount for your specific situation and financial goals.

Picking a Deductible That Matches Your Financial Reality

Start With Your Emergency Fund, Not Premium Savings

Your emergency fund, not industry standards, should determine your deductible. Minnesota homeowners often select deductibles based on what sounds reasonable rather than what they can actually afford to pay. If a hailstorm damages your roof tomorrow and costs $12,000 to repair, you’ll owe your deductible before the insurer pays anything. A $2,000 deductible saves you roughly $180 to $240 annually compared to a $500 deductible, but only if you have $2,000 sitting in savings right now.

Many homeowners live with less cash reserves than they realize. The Federal Reserve reports that many Americans cannot cover a $400 emergency without borrowing or selling something. If you fall into that group, a higher deductible to save money creates a trap: you’ll face either going into debt when damage occurs or skip the claim entirely and pay out of pocket anyway.

Start by honestly assessing your liquid savings. Can you pay $1,000 without adjusting your monthly budget? $1,500? $2,000? That number is your maximum deductible, regardless of the premium savings.

The Math Behind Deductible Increases

The annual savings from a higher deductible rarely justify the risk for most homeowners. A $1,000 deductible increase might save $150 to $200 per year, which sounds meaningful until you realize you need five to seven years of uninterrupted savings to break even financially if you file even one claim. Most Minnesota homeowners stay in their homes for seven to ten years, but not all do. If you plan to sell within five years, a higher deductible rarely makes mathematical sense.

Calculate your break-even point to make the right choice. Divide the annual premium savings by the deductible increase to see how many years it would take for the savings to equal the higher deductible. This calculation prevents you from selecting a deductible that looks good on paper but creates financial stress in reality.

Wind, Hail, and Flood Deductibles Complicate the Picture

Special deductibles for wind and hail claims complicate the picture significantly. In Minnesota, many insurers apply a separate wind deductible of 2 to 5 percent of your home’s insured value on top of your standard deductible. For a $350,000 home with a 3 percent wind deductible, that means you’d pay $10,500 out of pocket for hail damage, not your standard $1,000 or $1,500. This separate deductible applies per claim, so multiple storms in a single season mean multiple $10,500 hits.

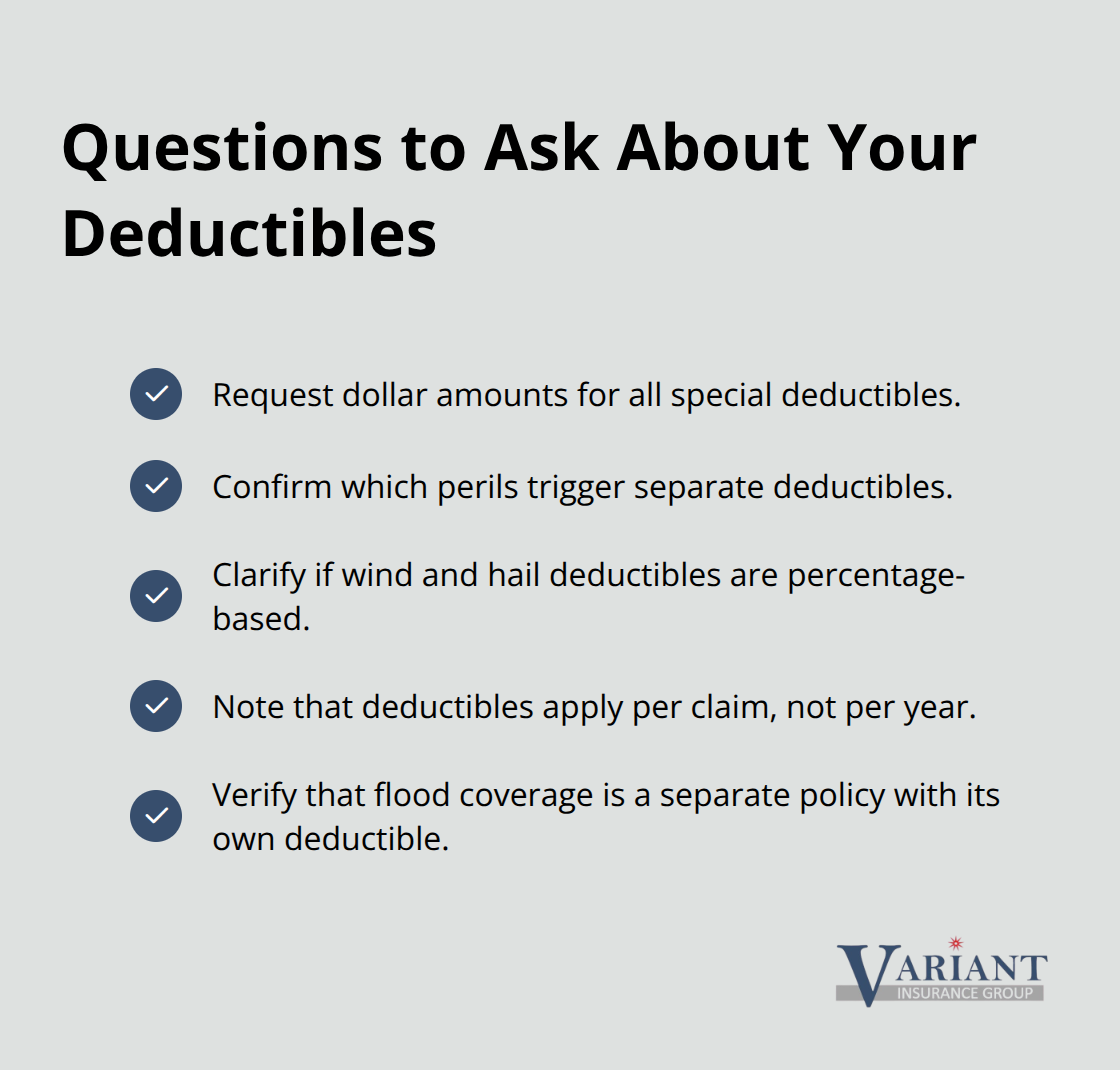

Flood insurance, which you must purchase separately through the National Flood Insurance Program or private carriers, carries its own deductible structure entirely. Ask your agent specifically which perils trigger separate deductibles and what those amounts are in dollar terms, not percentages. Once you understand the full picture of potential out-of-pocket costs across different damage types, you can make a deductible choice that actually protects your finances rather than just reducing your premium.

This understanding of your true financial exposure sets the stage for the next critical step: knowing exactly what happens when you file a claim and how your deductible applies to the specific damage your home sustains.

How Deductibles Actually Work When Damage Strikes

Your Deductible Applies Immediately When You File a Claim

When you file a claim, your deductible applies immediately and unavoidably. The moment you report a $15,000 roof replacement to your insurer, you cannot negotiate the deductible or request a waiver. If your policy specifies a $1,500 deductible, you owe that amount before the insurer pays a single dollar toward repairs. The insurer subtracts your deductible from the total damage cost, then pays you the difference (up to your coverage limits). This means a $15,000 claim with a $1,500 deductible results in a $13,500 payment to you, not $15,000.

Multiple Claims in One Year Mean Multiple Deductibles

Many homeowners underestimate how often multiple claims trigger multiple deductibles in the same year. A hailstorm in May that damages your roof costs you $1,500. A wind-driven rain event in August that damages your siding and interior costs you another $1,500. You pay two separate deductibles, not one. Minnesota homeowners in hail-prone areas like the Twin Cities suburbs face this scenario regularly, with the National Weather Service recording significant hail events nearly every summer. This reality matters far more than premium savings when you choose your deductible amount.

Wind and Hail Deductibles Cost Far More Than Standard Deductibles

Different types of damage apply different deductible rules, and this is where most Minnesota homeowners face surprises during claims. Your standard deductible covers general damage like theft or fire, but wind and hail claims trigger a separate deductible expressed as a percentage of your home’s insured value. A home insured for $500,000 with a 2% wind deductible means you pay $10,000 out of pocket for hail damage, not your standard $1,000 deductible. This separate deductible applies per claim, so a second hailstorm later that year costs another $10,000. The critical step is asking your agent to provide dollar amounts for all special deductibles, not percentages.

Percentages obscure the true out-of-pocket cost.

Flood and Earthquake Coverage Require Separate Insurance and Deductibles

Flood damage carries no standard deductible at all because flood insurance is excluded from homeowners policies entirely. You must purchase National Flood Insurance Program coverage or private flood insurance separately, each with distinct deductible options you select independently. An earthquake endorsement, though uncommon in Minnesota, also arrives with its own deductible if you add it to your policy. These separate policies function independently from your homeowners coverage, so you manage multiple deductible structures across different carriers and coverage types.

Named Peril and All-Risk Policies Handle Deductibles Differently

Named peril policies cover only specific listed events like fire or theft, and they apply your deductible to each covered peril separately. All-risk policies cover all damage except what is specifically excluded, but they still apply deductibles per claim and may impose higher deductibles for certain perils like wind or hail. Most Minnesota homeowners carry all-risk coverage because it provides broader protection, but the deductible structure remains the same regardless of policy type. The distinction matters less than understanding exactly which perils have special deductibles and what those amounts are in real dollars.

Final Thoughts

Your property insurance deductible represents a financial commitment you must be prepared to pay when damage strikes your home. Select a deductible that aligns with your actual emergency savings, not industry averages or what sounds reasonable. If you cannot comfortably pay $2,000 without disrupting your monthly budget, a higher deductible will create financial stress when you need it least.

Pull out your declarations page today and identify your standard deductible, then contact your agent about wind, hail, flood, and any other special deductibles that apply to your coverage. Write down the dollar amounts for each peril so you understand the true cost of your property insurance deductible. If those amounts exceed what you can afford to pay, adjust your deductible now rather than discovering the gap during a claim.

We at Variant Insurance Group work with Minnesota homeowners to review their deductible choices and match them to both financial situations and coverage needs. Contact Variant Insurance Group to review your property insurance deductible and confirm your coverage protects your home and your budget.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation