Most Minnesota homeowners underestimate what they actually own. When disaster strikes, that gap between what you think you’re covered for and what you really need can be devastating.

At Variant Insurance Group, we help people figure out exactly how much personal property insurance they need. The right coverage amount protects your belongings without paying for protection you don’t require.

What Should You Actually Count When Calculating Coverage

Start with everything you own that isn’t nailed down. Most people miss entire categories of belongings because they think about insurance in terms of big-ticket items like furniture and electronics. The National Association of Insurance Commissioners offers a free app called myHOME Scr.APP.book that makes it easy to create a record of all your belongings, including the ability to scan barcodes and upload photos of your items. This approach catches the things you’d otherwise forget: kitchen utensils, linens, clothing, sports equipment, tools, and decorative items.

Open your drawers and closets. Look inside cabinets. Check what sits in your garage and shed. A typical household has far more personal property than people estimate. In higher cost-of-living areas like the Twin Cities, replacement costs add up quickly. Someone might have $50,000 in furniture alone, then add $30,000 in electronics, $15,000 in clothing and accessories, and another $10,000 in kitchen items and décor. That totals $105,000 before you count anything else. If your current coverage limits sit at $50,000, you’re dramatically underinsured.

Handling Your Most Valuable Items

High-value possessions like jewelry, watches, art, firearms, and collectibles often hit policy sublimits under standard homeowners coverage. A standard policy might cap jewelry coverage at $1,500 or firearms at $2,500, even if your ring or gun collection is worth significantly more. You need scheduled endorsements or riders for these items, which require professional appraisals. Professional appraisers update valuations every three to five years as market values shift. You should keep receipts and photos for everything. When you file a claim, documentation speeds up the process and prevents disputes over replacement costs.

Protecting Items Outside Your Primary Home

Seasonal possessions and items you keep outside your primary home also need attention. If you own a cabin or vacation property, those belongings might not be covered under your main policy. If you store valuable equipment at a different location, you must verify that your policy covers it. Temporary possessions like rental equipment or borrowed items typically aren’t covered, so don’t assume they are.

The coverage gaps you identify now will shape what protection you actually need. Next, we’ll look at the specific factors that determine how much coverage makes sense for your situation.

Factors That Affect Your Coverage Amount

Location and Local Crime Rates

Where you live in Minnesota significantly shapes how much personal property coverage you need. Crime rates vary dramatically across the state, and insurers track this data carefully. Minneapolis and St. Paul neighborhoods with higher theft and burglary rates typically see higher premiums because claims occur more frequently in those areas. If you live in a neighborhood where break-ins happen regularly, you expose yourself to real financial risk if your limits don’t match your belongings’ value. Conversely, rural areas with lower crime rates may allow you to maintain slightly lower coverage amounts, though this doesn’t mean you should underestimate what you own.

Home Type and Construction Materials

The type of home you live in directly affects your coverage needs. Older homes with wood-frame construction in Minnesota face different risks than newer homes with concrete foundations and modern fire suppression systems. Wood-frame houses are more vulnerable to fire damage, which means your personal property inside faces higher risk. Construction materials and age determine how quickly a fire spreads and how much damage occurs. A 1920s wood-frame home in Northeast Minneapolis needs different coverage calculations than a 2010s brick home in Edina. Insurance companies factor these construction details into their risk assessments, and your coverage limits should reflect the actual vulnerability of your specific dwelling.

Your Lifestyle and Risk Exposure

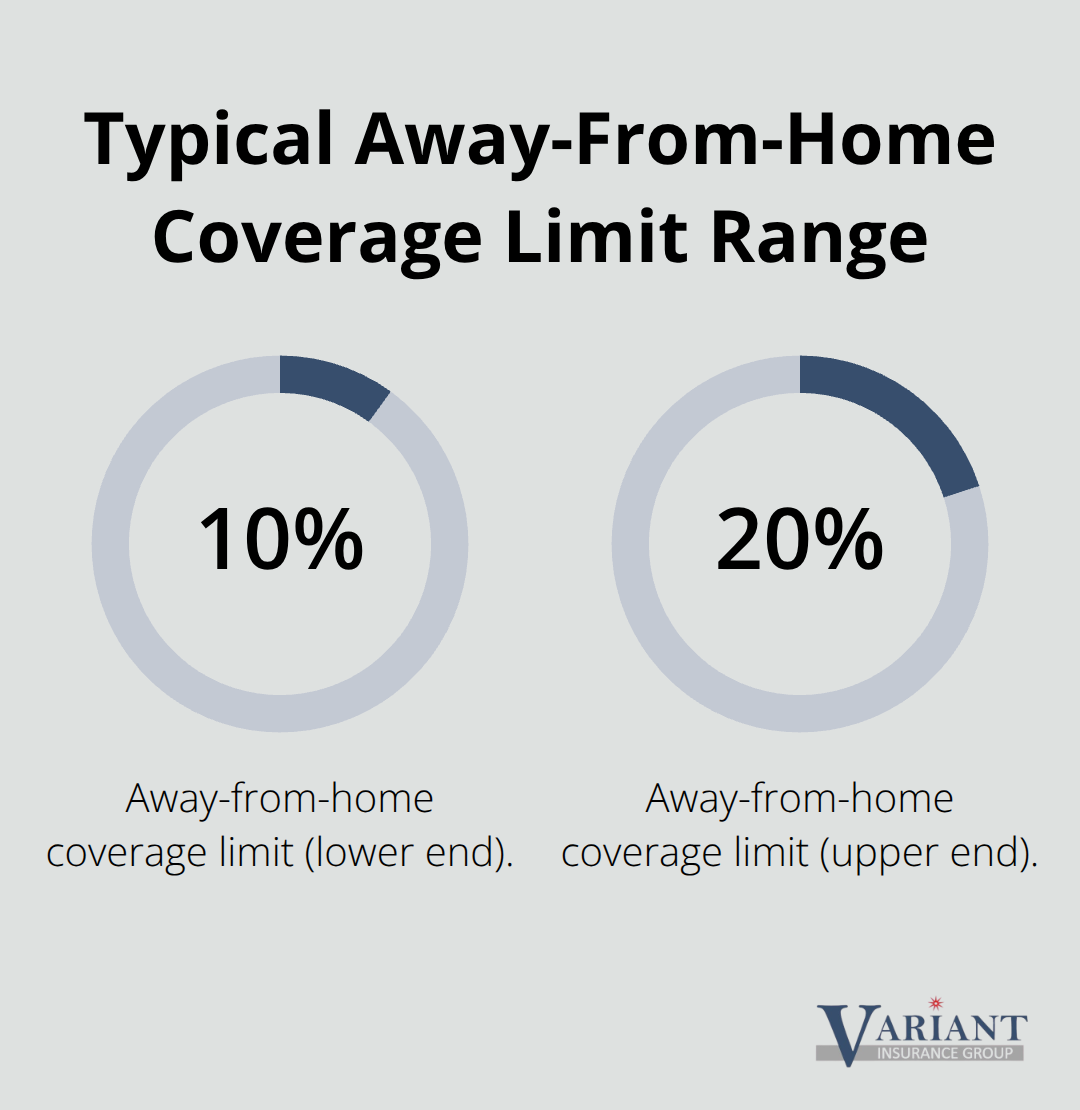

Your daily habits and lifestyle choices create coverage gaps that many people miss entirely. If you travel frequently for work or pleasure, you move valuable items outside your primary home regularly. A laptop, camera equipment, or jewelry that leaves your house multiple times per week faces different risk than items stored in your bedroom closet. Standard homeowners policies typically limit coverage for belongings away from home to 10–20% of your personal property limit, which often isn’t enough. If you work from home and store business equipment or inventory there, you need to verify coverage explicitly because many policies exclude business personal property.

Hobbies create additional coverage needs. Someone with an expensive golf club collection, an expensive mountain bike, or photography equipment needs scheduled endorsements because standard policies cap coverage on these items. Minnesota’s climate creates unique lifestyle risks as well. Heavy rainfall, ice dams, and winter storms cause water damage that varies by how your home is constructed and maintained. If you live in an area prone to basement flooding or have experienced water damage before, you need separate water backup coverage because standard homeowners policies don’t cover sewer backups. Your risk exposure isn’t just about what could happen-it’s about what has already happened to homes like yours in your neighborhood.

These location, construction, and lifestyle factors work together to determine your actual coverage needs. The next section examines the mistakes that prevent homeowners from getting the protection they truly require.

Common Mistakes When Choosing Coverage Limits

Most Minnesota homeowners make one critical mistake: they anchor their coverage limits to an arbitrary number rather than their actual belongings. You might have $75,000 in personal property coverage because that seemed reasonable five years ago, but you’ve purchased new furniture, upgraded your electronics, and acquired items you’ve forgotten about. That $75,000 limit stays fixed while your possessions grow. When a fire or theft occurs, you discover you’re short by $30,000 or $40,000. The insurance company pays your limit, not your loss. You absorb the difference. This happens constantly because people treat coverage amounts like they’re permanent decisions instead of numbers that need regular adjustment.

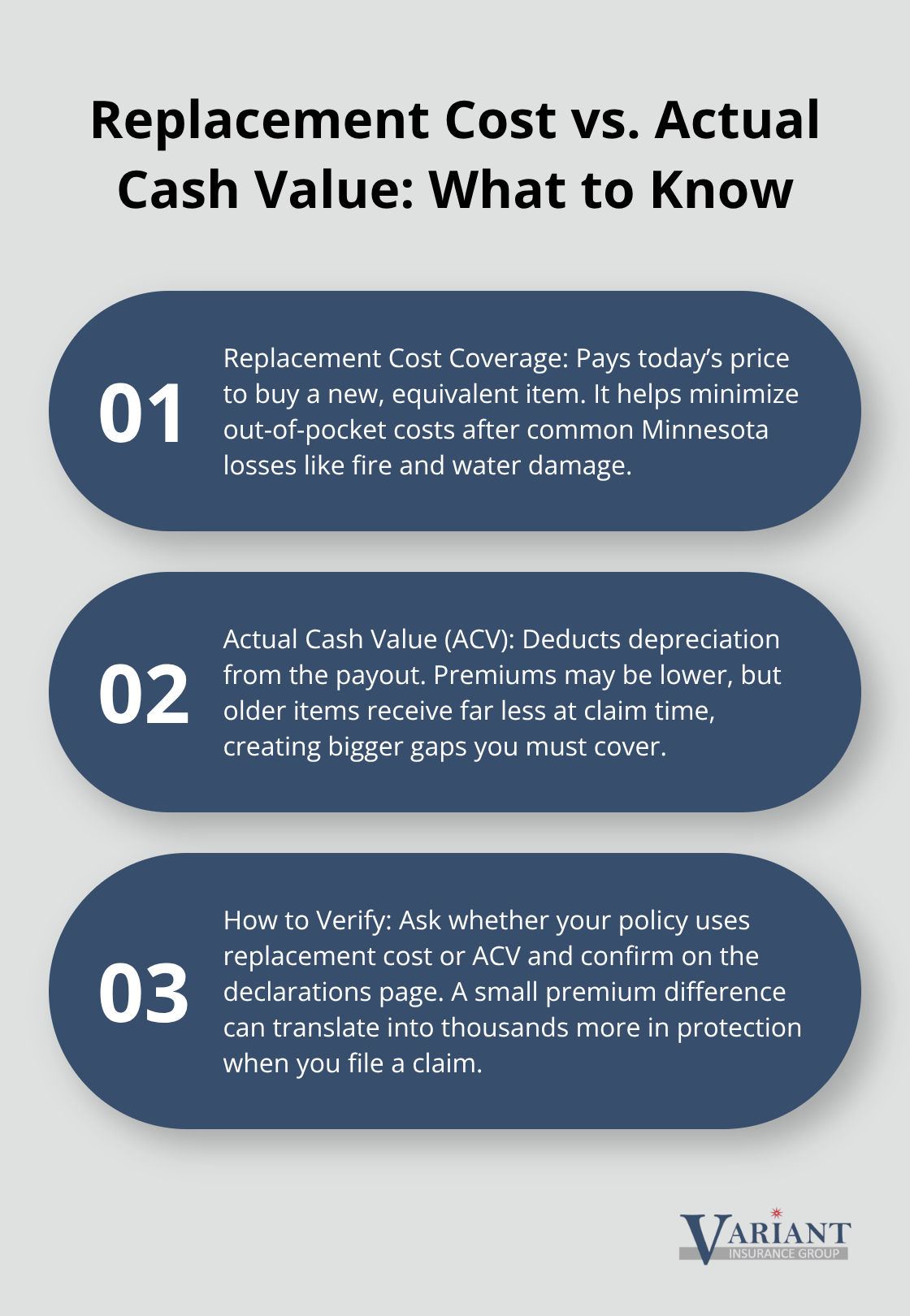

Replacement Cost vs. Actual Cash Value

The second mistake compounds the first: confusing replacement cost coverage with actual cash value. Replacement cost coverage pays what it costs to buy a new item today. Actual cash value subtracts depreciation, so a five-year-old laptop worth $1,200 new might be valued at $400 under actual cash value. In Minnesota, where homeowners face significant water damage and fire risk, the difference between these two approaches can mean thousands of dollars in out-of-pocket expenses. Standard HO-3 policies typically include replacement cost coverage, but some older policies or lower-cost options use actual cash value.

When you shop for coverage, verify which type you’re getting because the premium difference is usually modest while the protection difference is substantial. If an agent quotes you a policy significantly cheaper than competitors, check whether they’ve switched you to actual cash value coverage to lower the price.

Sublimits on High-Value Items

The third mistake involves items that don’t fit neatly into standard homeowners coverage. Jewelry typically caps at $1,500 under standard policies, but a wedding ring, engagement ring, and watch collection easily exceed that. Firearms cap at $2,500 in many policies despite the value of quality firearms and ammunition. Fine art, antiques, and collectibles face similar sublimits. Most homeowners discover these gaps only after a loss when they realize their $8,000 watch or $5,000 shotgun collection qualifies for only partial reimbursement. The solution requires scheduled endorsements, which means you need professional appraisals and must add those items to your policy explicitly. This costs money upfront but prevents catastrophic underinsurance when you actually need the coverage. Without scheduled endorsements, you essentially self-insure the difference between the sublimit and the actual value.

Coverage Gaps for Items Outside Your Home

Items stored outside your primary home create another coverage gap that’s easy to overlook. If you keep a boat, ATV, or trailer at a storage facility, your homeowners policy likely doesn’t cover it. If you have a cabin or vacation property, the belongings there might not be covered under your primary residence policy. Tools stored in a garage that you use for side work sometimes fall under business property exclusions, which means they’re not covered at all. Business inventory, equipment, or samples kept in your home face explicit exclusions in most homeowners policies. You need to ask your agent about each category of possessions and get written confirmation of what is and isn’t covered.

Water Damage and Minnesota-Specific Risks

Minnesota’s unique risks mean water damage from basement flooding, ice dams, and heavy rainfall cause significant losses, but standard policies exclude sewer backup damage. Water backup coverage costs $50 to $100 annually and protects against a common Minnesota problem that destroys personal property regularly. You should verify whether your current policy includes this protection and add it if it doesn’t. The cost is minimal compared to the potential loss from a backed-up sewer line or heavy rain event that floods your basement.

Final Thoughts

The answer to how much personal property insurance you need depends entirely on what you own, where you live, and what risks you face. Start by completing a thorough home inventory using the NAIC app or a detailed checklist, then document everything from kitchen utensils to collectibles with photos and receipts. This inventory becomes your foundation for calculating replacement costs at current prices and determining adequate coverage.

Once you know what you own, schedule a conversation with your insurance agent to review your current limits against your actual belongings. Ask specifically about replacement cost versus actual cash value, verify sublimits on high-value items like jewelry and firearms, and confirm coverage for anything stored outside your primary home. Minnesota-specific risks like water backup deserve explicit attention because standard policies exclude sewer damage and basement flooding-add water backup coverage if you don’t have it.

At Variant Insurance Group, we help Minnesota homeowners find coverage that matches their actual needs and budget. Contact Variant Insurance Group to review your personal property coverage and identify gaps before a loss occurs.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation