A lawsuit or accident can wipe out years of financial progress in Minnesota families. Standard home and auto insurance policies have limits that often fall short when serious claims arise. Personal umbrella insurance for families fills those dangerous gaps with additional liability protection that safeguards your assets.

We at Variant Insurance Group help families understand how this coverage works and why it matters for your financial security.

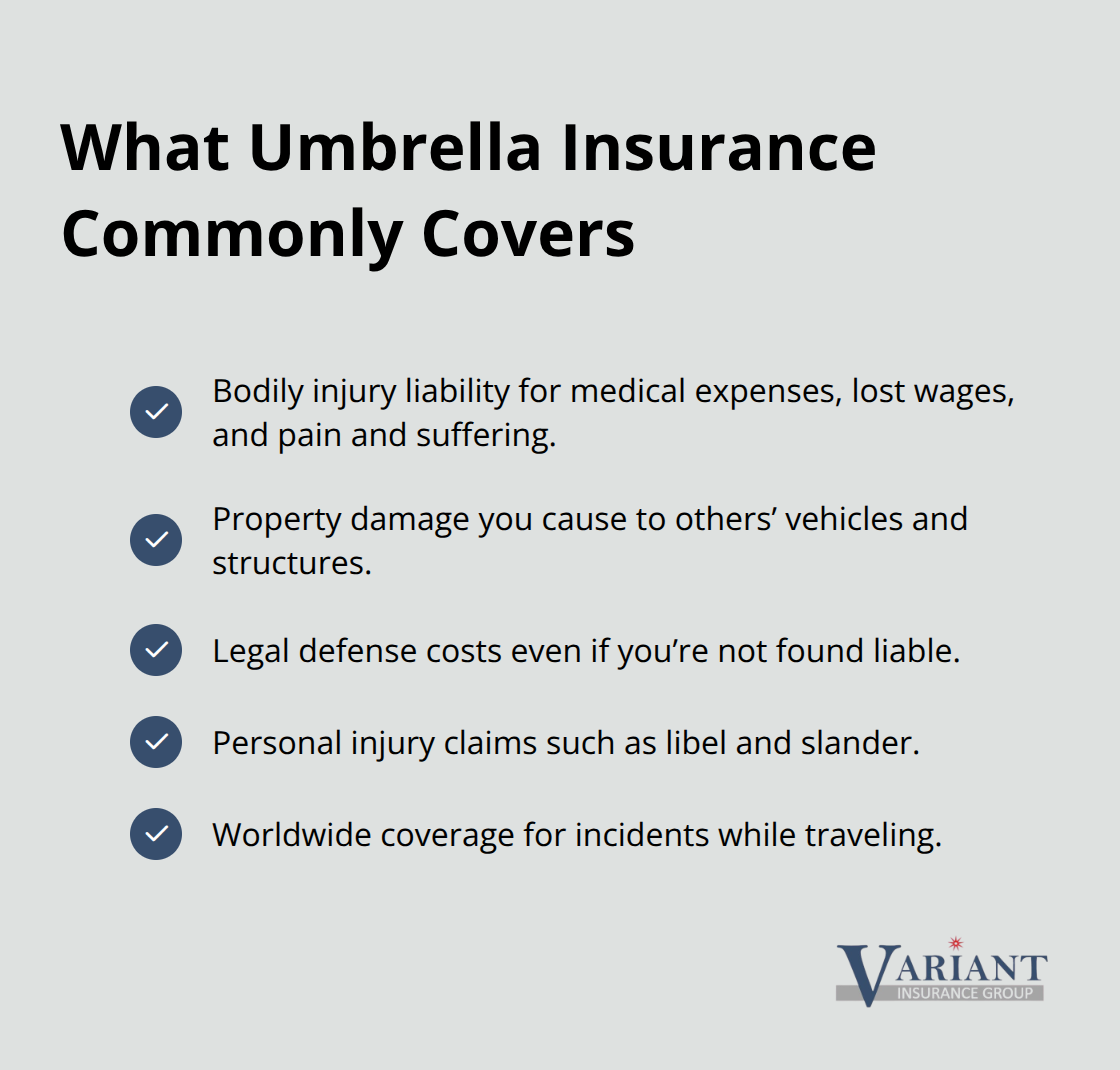

What Umbrella Insurance Actually Covers

A lawsuit or accident can wipe out years of financial progress. Personal umbrella insurance activates after your home and auto policies hit their limits, covering the excess liability you’re responsible for. When a serious accident happens-a guest injured on your property, a car crash you caused, or damage to someone else’s home-your standard homeowners or auto policy pays out first. Once that limit is exhausted, your umbrella policy kicks in and covers the remaining amount.

This matters because medical bills, property damage, and legal fees from a single incident routinely exceed $500,000 in Minnesota. A dog bite that requires multiple surgeries, a winter car crash with multiple injured parties, or a house fire that spreads to a neighbor’s garage can all generate claims well beyond what standard policies cover. Your umbrella policy doesn’t replace your home or auto coverage-it layers on top of it, protecting your paycheck, savings, and assets from being seized to pay a judgment.

What Gets Covered Beyond Your Standard Policies

Umbrella policies cover bodily injury claims when you’re found liable for someone’s medical expenses, lost wages, or pain and suffering. They also cover property damage you cause, like if a fire in your home spreads to neighboring properties or your vehicle damages another car. Your umbrella pays legal defense costs even if you’re found not liable, which means attorney fees and court expenses don’t come out of your pocket. Some umbrella policies extend to libel and slander claims, protecting you if someone sues over defamatory statements you made online or elsewhere. The coverage applies worldwide, so incidents that happen when your family travels are also protected.

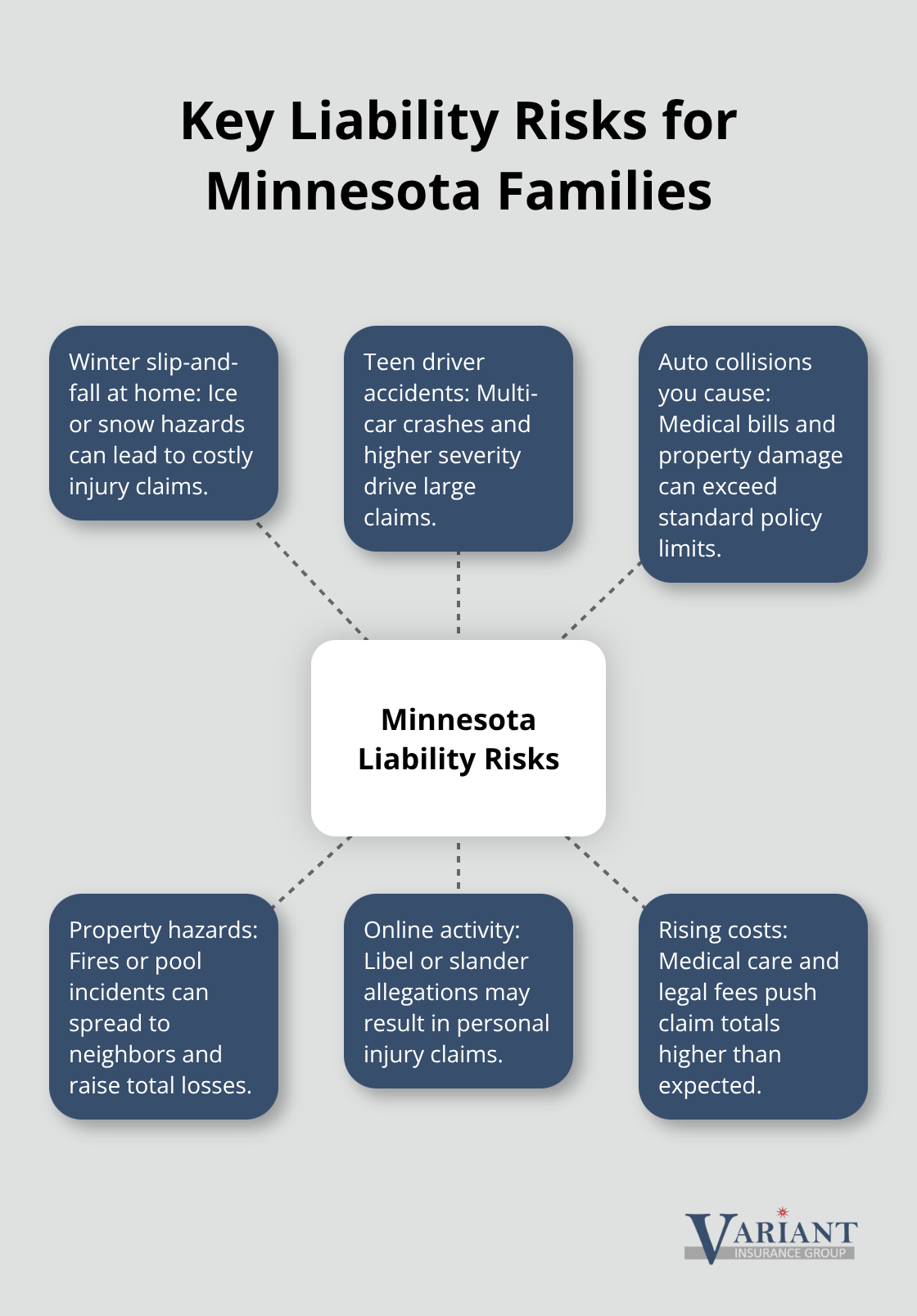

Minnesota families often face winter-specific liability risks-a guest slips on ice you failed to salt properly, or a teen driver causes a multi-car pileup-and umbrella insurance covers these situations after your auto or homeowners limits are exhausted.

Why Your Current Policy Limits Fall Short

Most homeowners policies cap liability at $300,000 to $500,000, while auto policies typically max out around $250,000 to $500,000 per incident. When you combine a serious injury with legal costs, those limits vanish quickly. According to the Wall Street Journal in July 2024, umbrella claim activity has pressured premiums higher because insurers are seeing larger payouts than expected. Liability claims can exceed standard policy limits in Minnesota-for example, if your auto policy maxes out at $300,000, umbrella insurance covers the remaining $700,000 in a $1 million claim.

Without umbrella coverage, you’d be responsible for paying the difference yourself, potentially liquidating investments, selling property, or having wages garnished. The cost of umbrella insurance-typically $200 to $400 annually for the first $1 million in coverage-is negligible compared to the financial devastation a six-figure judgment can cause to your family’s future. This protection becomes even more valuable when you consider that a single serious incident can threaten decades of financial security.

How Umbrella Coverage Layers With Your Existing Policies

Your umbrella policy works in coordination with your home and auto insurance, not in isolation. You must maintain minimum underlying coverage on your auto and homeowners policies before an umbrella policy activates. This requirement ensures that your umbrella sits on top of a solid foundation of primary coverage. When a claim arises, your home or auto policy pays first up to its limit, and then your umbrella policy covers the excess. Understanding how these policies coordinate with each other is essential to making sure you have no gaps in protection when you need it most.

Why Minnesota Families Face Real Umbrella Insurance Risks

Winter Weather Creates Specific Liability Exposures

Minnesota winters create specific liability exposures that standard policies simply don’t address adequately. A guest slips on ice you should have salted, a teen driver hydroplanes on a wet road and hits another vehicle, or a pool on your property becomes the site of a drowning-these incidents happen in Minnesota regularly, and the financial consequences exceed what most homeowners and auto policies cover. The Wall Street Journal reported in July 2024 that umbrella claim activity has pressured the entire market because actual claims run much larger than historical data suggested. This isn’t theoretical risk; it’s happening now, and your family’s financial security depends on understanding how exposed you actually are.

Medical Costs and Legal Fees Add Up Fast

Medical costs and legal fees in Minnesota are genuinely expensive. A single serious injury claim routinely reaches $500,000 to $1 million when you factor in emergency surgery, rehabilitation, lost wages, and attorney fees. If a guest suffers a spinal injury from a fall at your home, or if your teenage driver causes a multi-car crash on I-494, the medical bills alone can exceed $300,000. Your homeowners policy might cover $300,000 in liability, and your auto policy might cover $250,000-but once those limits are exhausted, the remaining $400,000 to $700,000 becomes your personal responsibility.

The Real Cost of Being Unprotected

Without umbrella insurance, you’d face liquidating retirement accounts, selling investments, or having future wages garnished to satisfy a judgment. The average cost of umbrella coverage is approximately $200 to $400 annually for $1 million in protection, making it one of the cheapest ways to prevent financial catastrophe. Minnesota families with significant assets-a home worth $400,000, investment accounts, or college savings-cannot afford to leave this gap unprotected. The decision to add umbrella coverage isn’t about whether you can afford it; it’s about whether you can afford not to have it when a serious claim arrives.

Understanding Your Actual Exposure

Your liability exposure extends beyond what you might initially recognize. Teen drivers, rental properties, social media activity, and even volunteer work can trigger claims that exceed standard policy limits. The combination of Minnesota’s winter hazards and the rising cost of medical care means that families across the state face genuine risk. As you evaluate your family’s protection, the next step involves assessing your total assets and determining how much umbrella coverage actually makes sense for your situation.

How to Choose the Right Umbrella Policy

Calculate Your Total Assets and Future Earnings

Selecting the right umbrella policy requires honest assessment of what you actually own and what could realistically be taken from you in a lawsuit. Start by listing your total assets: your home value, vehicles, investment accounts, retirement savings, and any rental properties. If your home is worth $450,000, you have $200,000 in investments, and you own two vehicles, your total exposure is roughly $650,000 before considering future earnings. Most Minnesota families underestimate their liability exposure because they overlook future income. If you earn $80,000 annually and have twenty-five years until retirement, your future earnings represent another $2 million in potential exposure. The math becomes clear quickly: a $1 million umbrella policy is the practical minimum for most families, and many Minnesota households benefit from $2 million in coverage given winter driving risks and property values in the Twin Cities area.

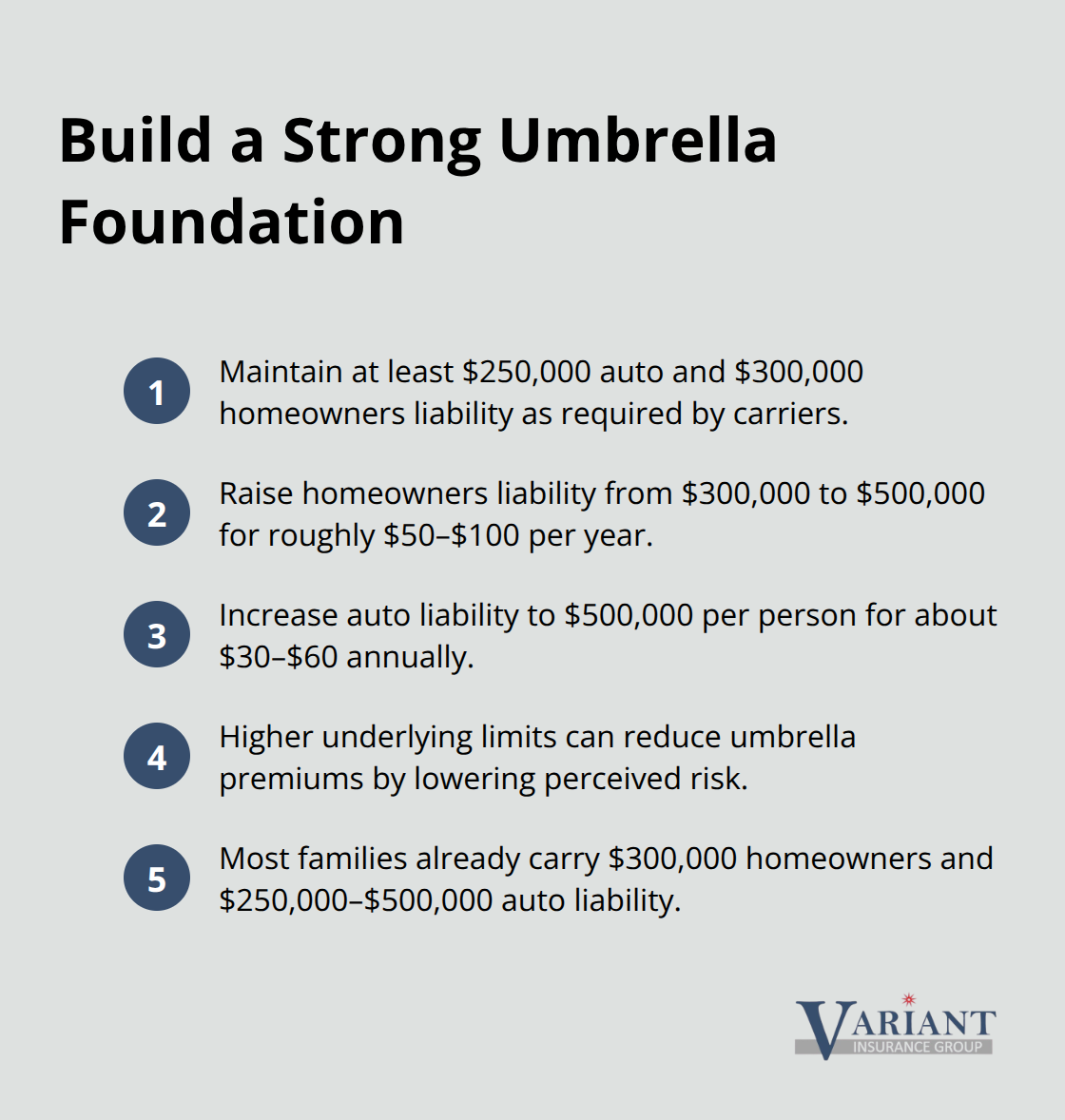

Build a Strong Foundation With Underlying Coverage

Your existing home and auto policies must serve as the foundation before umbrella coverage activates. Review your current homeowners policy limit and auto liability limits right now. Most Minnesota homeowners carry $300,000 in homeowners liability and $250,000 to $500,000 in auto liability. These limits are insufficient on their own, which is exactly why umbrella insurance exists. Insurance carriers require you to maintain minimum underlying coverage before approving an umbrella policy, typically $250,000 for auto and $300,000 for homeowners. Raising these underlying limits costs far less than you’d expect. Increasing your homeowners liability from $300,000 to $500,000 might cost only $50 to $100 annually, and bumping your auto liability to $500,000 per person might add $30 to $60 per year.

These small increases create a stronger foundation and can lower your umbrella premium because insurers view higher underlying limits as reduced risk.

Understand the Real Cost of Umbrella Coverage

The typical cost for $1 million in umbrella coverage ranges from $200 to $400 annually according to ACE Private Risk Services data cited by Forbes. Additional coverage beyond $1 million typically costs $50 to $75 per million. If you need $2 million total, expect to pay roughly $250 to $475 annually depending on your location, driving record, and claims history. Minnesota families with teen drivers may see slightly higher premiums because teenage drivers represent genuine risk. A single accident involving a teen driver can generate claims exceeding $500,000 when medical bills and property damage combine. Pricing varies significantly between insurers-some carriers charge $250 for $1 million coverage while others charge $400 for identical protection. Location matters too: families in the Twin Cities metro area sometimes pay slightly different rates than those in rural Minnesota due to claim frequency and medical cost variations.

Compare Policies on the Factors That Matter

When comparing umbrella quotes, focus on three specific factors: the policy limit, the coordination with your underlying policies, and any exclusions or endorsements. Ask each carrier whether the umbrella policy coordinates properly with your home and auto coverage, meaning it activates only after those policies are exhausted. Some carriers exclude certain activities or properties, so confirm whether rental properties, teen drivers, or volunteer work are covered under each policy you’re considering. Request quotes for both $1 million and $2 million limits so you can see the actual cost difference. The premium difference between $1 million and $2 million is usually $50 to $100 annually, which makes the decision straightforward for most families. Finally, verify that each quote assumes your current underlying coverage levels. If an insurer quotes you based on $250,000 auto liability when you actually carry $500,000, the quote won’t be accurate for comparison.

Final Thoughts

Personal umbrella insurance for families protects your financial future at a cost most Minnesota households can easily afford. Standard home and auto policies leave dangerous gaps when serious claims arise, and a single accident can threaten decades of financial progress. Umbrella coverage fills that gap for roughly $200 to $400 annually per $1 million in protection, making it one of the smartest financial decisions you can make.

The path forward requires three concrete actions. Calculate your total assets and future earnings to understand your actual exposure, review your current homeowners and auto policy limits, and request quotes from multiple carriers for both $1 million and $2 million in coverage. Most Minnesota families find that $2 million in umbrella protection costs only $50 to $100 more annually than $1 million, which makes the upgrade worthwhile given winter driving risks and rising medical costs in our state.

We at Variant Insurance Group help Minnesota families secure personal umbrella insurance that matches their actual needs. Our team compares protection and pricing across multiple carriers to find policies that coordinate properly with your existing coverage and fit your family’s situation. Contact us today to discuss your umbrella insurance needs and discover the coverage amount that protects your family’s financial security.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation