Most Minnesota drivers don’t realize that a single accident could expose them to thousands in liability claims. Property damage liability coverage protects you when you’re at fault for damaging someone else’s vehicle or property.

At Variant Insurance Group, we help drivers understand exactly how much auto insurance property damage liability they need. The right coverage limits can mean the difference between financial security and serious debt.

What Property Damage Liability Actually Covers

Property damage liability pays for damage you cause to someone else’s property when you’re at fault in an auto accident. This covers the other vehicle, fences, mailboxes, lampposts, buildings, and any other structures damaged in the crash. Minnesota law requires this coverage, with a minimum of $10,000 per accident. However, that minimum is dangerously low. The National Safety Council reports that the average cost of damage in property-damage-only crashes is about $5,700 per vehicle, meaning even a moderate accident could consume most of your minimum coverage. If repair costs exceed your limit, you pay the difference out of pocket. This coverage has no deductible, so your insurer pays claims directly up to your limit without you contributing at the time of claim.

Understanding What Property Damage Liability Doesn’t Cover

Property damage liability specifically does not cover damage to your own vehicle, injuries to people, or rental car costs. If another driver hits you, their property damage liability pays for your car repairs, but your own collision coverage handles your vehicle if you’re at fault. Your bodily injury liability covers injuries you cause to others, while your medical expense coverage protects you and your passengers. This distinction matters because many drivers mistakenly think property damage liability is their only protection, leaving massive gaps. For rental vehicles, Minnesota law requires your plan to extend property damage liability to rented cars, and if your PD limit is below $35,000, your rental coverage must be at least $35,000. Underinsured motorist property damage coverage is optional in many states and protects you when the other driver has insufficient coverage, though Minnesota law requires uninsured and underinsured motorist coverage minimums of $25,000 per person and $50,000 per accident for bodily injury.

Why Minnesota’s Minimum Falls Short

The $10,000 Minnesota minimum property damage limit makes sense only if you own nothing of value. A single accident involving a newer vehicle, multiple cars, or property damage to a building could easily exceed $10,000. Financial experts commonly recommend carrying limits of $50,000 to $100,000 per accident to actually protect your assets. Your net worth determines your real exposure: if you have savings, a home, or other property, an underinsured accident could result in a judgment against you. Location matters too. Driving in high-traffic areas or near expensive properties justifies higher limits. When you choose coverage, consider what you’d owe if you damaged a luxury vehicle worth $80,000 or caused significant structural damage to a building. Higher limits typically cost only slightly more in premiums but protect you from catastrophic financial exposure that state minimums leave uncovered.

Assessing Your Personal Risk Exposure

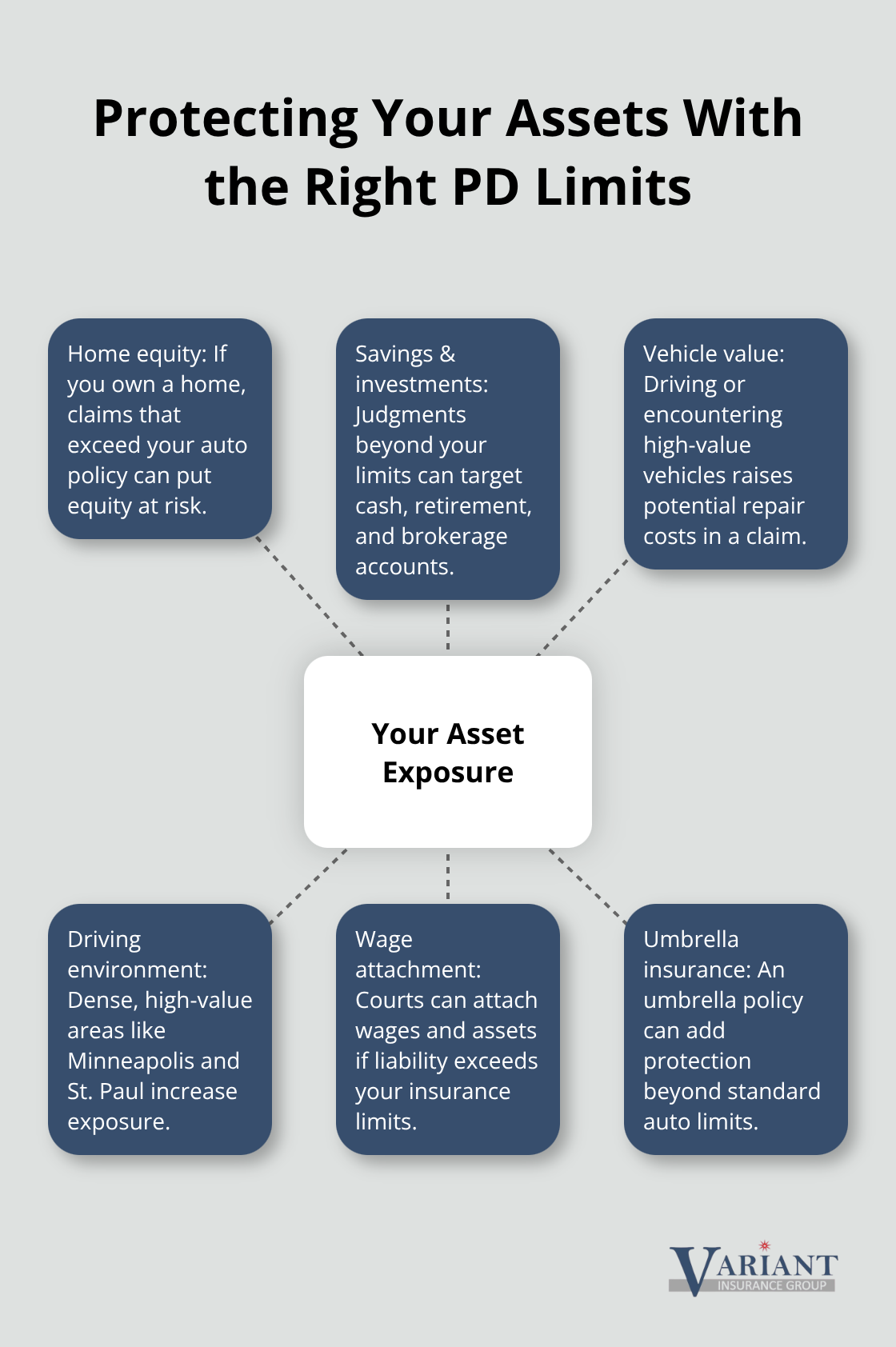

Your assets and financial situation should drive your coverage decision. If you own a home, have substantial savings, or carry significant investments, a $10,000 limit exposes you to serious liability. A judgment against you could attach your wages or assets for years. The type of vehicle you drive also affects your risk: drivers of luxury or high-value vehicles cause more expensive accidents simply because the property involved costs more to repair. Your driving patterns matter as well. Commuting through downtown Minneapolis or St. Paul, where traffic density and property values are higher, increases the likelihood of expensive claims. Consider also whether you allow others to drive your vehicle with permission-their accidents count against your coverage too. An independent insurance agency can help you evaluate these factors and find appropriate limits that match your actual exposure.

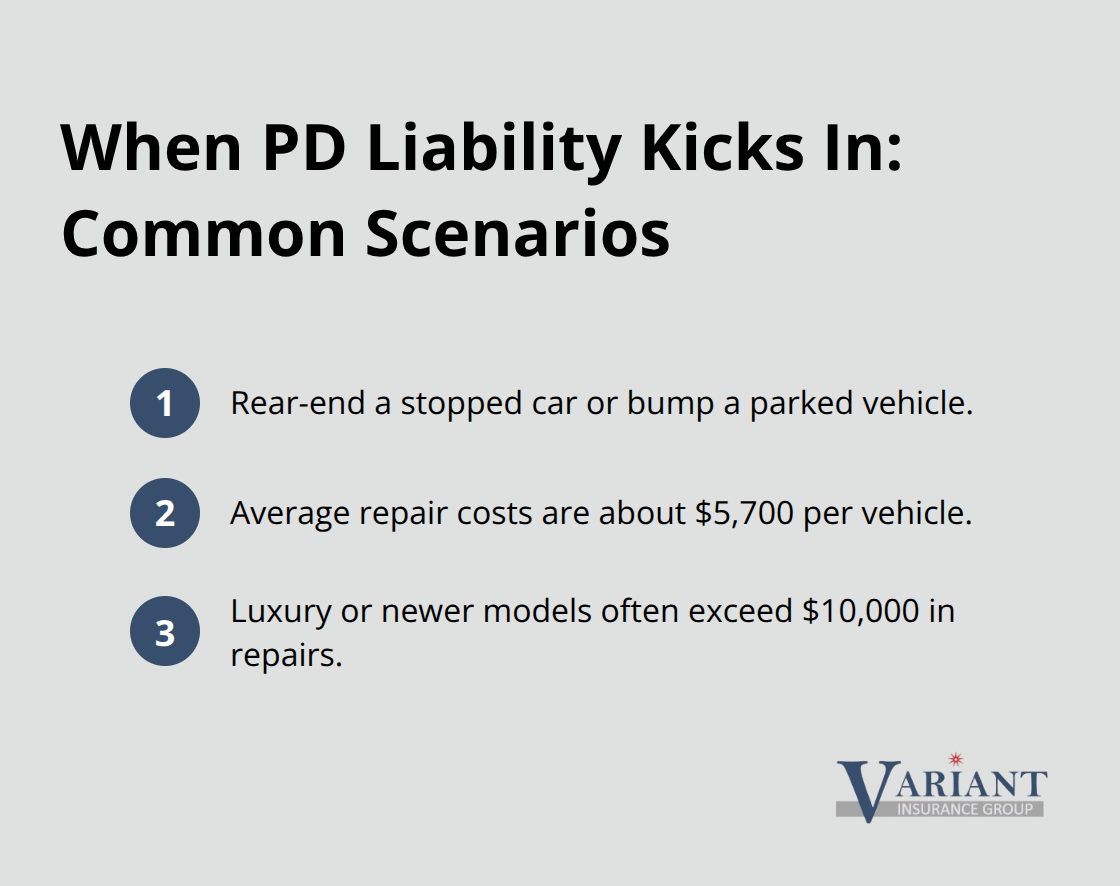

When Property Damage Liability Actually Kicks In

Most Minnesota drivers face property damage liability claims in situations they never anticipated. The most common scenario involves rear-ending another vehicle at a stoplight or hitting a parked car while backing out of a parking space. These accidents trigger your property damage liability immediately, and the other driver’s repair costs come straight from your coverage. A 2024 analysis found that average repair costs for vehicles involved in property-damage-only crashes reach approximately $5,700, though luxury vehicles and newer models frequently exceed $10,000 in repairs. Your $10,000 minimum coverage disappears quickly in these situations.

Multi-Vehicle Accidents and Escalating Costs

Multi-vehicle pile-ups create even steeper exposure. If you cause a five-car accident on Interstate 35, your property damage liability must cover damage to all vehicles involved, up to your per-accident limit. Some policies distinguish between per-accident and per-vehicle sublimits, so verify your exact coverage with your insurer. The math becomes brutal fast: five vehicles at $5,700 average damage each totals $28,500, which already exceeds your minimum by nearly three times. A single luxury vehicle in that pile-up could push costs well beyond $15,000 alone.

Property Damage Beyond Vehicles

Property damage extends far beyond vehicles in real collisions. Hitting a fence, mailbox, or lamppost triggers coverage. Crashing into a storefront or residential building activates your liability for structural repairs, which easily surpass vehicle damage costs. One Minnesota driver caused $18,000 in damage to a building facade after losing control in a downtown area, far exceeding the state minimum. The driver carried a $50,000 limit, so the insurer covered the full amount, but with only the $10,000 minimum, that driver would have owed $8,000 out of pocket. Building damage claims often involve not just structural repairs but also business interruption costs and code compliance upgrades that multiply the final bill.

Hit-and-Run Situations and Coverage Gaps

Hit-and-run situations create confusion about coverage. If you cause an accident and leave the scene, your property damage liability still applies to the damage you caused, though you face serious legal consequences for leaving. More relevant for your coverage: if an uninsured or underinsured driver hits you and leaves, your uninsured motorist property damage coverage helps only in specific states with that optional coverage. Minnesota requires uninsured motorist coverage for bodily injury at $25,000 per person and $50,000 per accident, but property damage protection varies depending on your specific policy. Many Minnesota drivers mistakenly believe their property damage liability protects them in hit-and-run situations when they’re the victim, but it doesn’t. You need comprehensive or collision coverage for your own vehicle damage, plus uninsured motorist coverage for the other driver’s liability exposure.

Why Minimum Coverage Fails in Real Accidents

Property damage liability activates whenever you’re at fault for damaging someone else’s property, and the claims mount faster than most drivers expect. A single accident involving multiple vehicles or property damage to structures can consume your minimum coverage within minutes. This reality explains why financial experts recommend $50,000 to $100,000 limits rather than relying on Minnesota’s $10,000 minimum. Your actual risk depends on where you drive, what vehicles share the road with you, and what property surrounds your typical routes. Understanding these real-world scenarios sets the stage for making an informed decision about your coverage limits-a choice that directly affects your financial security after an accident.

How Much Coverage Actually Protects Your Assets

Your net worth determines how much property damage liability you genuinely need. If you own a home valued at $350,000, have $50,000 in savings, or drive vehicles worth $60,000, a $10,000 property damage limit exposes all of that to a judgment against you.

Minnesota courts can attach wages and assets for years to satisfy a liability judgment that exceeds your insurance limits.

Calculate Your Total Assets

Start with your home equity, vehicles, retirement accounts, savings, and investments. Add these figures together to understand your actual exposure. If your total exceeds $100,000, carrying only the $10,000 minimum is financially reckless. Financial experts recommend property damage limits matching your net worth or at least $50,000 to $100,000 per accident. The cost difference between a $10,000 limit and a $100,000 limit on your premium typically runs $20 to $40 annually, making the upgrade absurdly cheap compared to your actual exposure. For those with substantial assets, umbrella insurance provides an additional layer of protection beyond standard policy limits.

Location Amplifies Your Risk

Drivers in Minneapolis and St. Paul navigate higher traffic density and encounter more expensive vehicles and properties than rural Minnesota drivers. A downtown accident involving a luxury vehicle or building damage creates exposure that state minimums cannot absorb. Even suburban drivers should evaluate their actual environment: school zones, shopping districts, and parking lots near retail areas all increase the probability of expensive claims. Your driving patterns matter too. Commuters who drive 40 miles daily face more accident risk than someone driving occasionally. High-mileage drivers face proportionally higher claim probability, which justifies higher limits even if your net worth is modest.

Align Underinsured Motorist Protection with Property Damage Limits

Your underinsured motorist protection works independently from your property damage liability choice, but the two decisions should align strategically. Underinsured motorist coverage protects you when another driver causes an accident but carries insufficient liability insurance to cover your damages. Minnesota requires uninsured and underinsured motorist minimums of $25,000 per person and $50,000 per accident for bodily injury, but this does not automatically extend to property damage unless your specific policy includes it. Many Minnesota drivers carry the state minimum for uninsured motorist coverage while ignoring property damage limits, creating an imbalanced protection strategy. If you increase your property damage liability to $100,000, try matching that with comparable uninsured motorist limits so you receive equal protection whether you cause an accident or become a victim.

Shop Multiple Minnesota Insurers for Competitive Pricing

Shopping for coverage across Minnesota insurers reveals significant variation in pricing and available limits. Some carriers offer property damage limits up to $250,000 or higher, while others cap options at $100,000. Premium differences between carriers for identical coverage can range from 15 to 40 percent, making comparison shopping essential.

Requesting quotes from multiple insurers takes roughly 30 minutes and reveals whether you are overpaying for inadequate limits or underpaying for robust protection.

Final Thoughts

Property damage liability coverage protects your financial future when you cause an accident, but Minnesota’s $10,000 minimum leaves most drivers dangerously exposed. The real cost of accidents-averaging $5,700 per vehicle and often exceeding $15,000 when property damage extends beyond vehicles-makes the state minimum inadequate for anyone with meaningful assets. Carrying $50,000 to $100,000 in auto insurance property damage liability costs only slightly more in premiums while protecting your home, savings, and wages from judgment claims that could follow an accident.

Your coverage decision should reflect your actual net worth and driving environment, not just legal minimums. Drivers in Minneapolis and St. Paul face higher accident costs than rural Minnesota residents, and commuters with longer daily driving distances face proportionally greater claim probability. Shopping multiple insurers reveals significant pricing variations and available limits that state minimums never capture.

We at Variant Insurance Group help Minnesota drivers evaluate their specific exposure and find appropriate property damage liability limits that match their assets and driving patterns. Contact Variant Insurance Group to request quotes and speak with an agent who works for you, not a single insurance company.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation