Property insurance is one of the largest expenses Minnesota homeowners face each year. Understanding what drives your average property insurance cost helps you make smarter decisions about coverage and savings.

At Variant Insurance Group, we’ve helped thousands of Minnesotans find affordable policies that actually protect their homes. This guide breaks down the real numbers behind property insurance premiums and shows you concrete ways to pay less.

What Drives Your Property Insurance Cost in Minnesota

Minnesota’s homeowners insurance market reflects real climate risks that directly impact your premiums. Severe weather events reshape costs across the state, with hail storms and convective weather causing significant property damage. According to Insurify’s analysis, Minnesota homeowners face projected premium increases of about 15% this year, pushing the average annual cost to $4,058 from $3,524 the previous year. Weather-related claims force insurers to raise rates to cover their losses. Andrew Whitman, an insurance professor at the University of Minnesota, notes that underwriters are increasingly cautious about new insurers due to higher claims experience-which means your current insurer may offer better renewal rates than shopping for a new policy.

How Your Home’s Age and Features Shape Premiums

Older homes cost more to insure than newer construction when coverage levels are identical. According to NerdWallet’s analysis, a home built in 1984 averages around $2,490 annually for standard coverage, while a 2025-built home averages just $1,425 for the same protection. The difference reflects higher rebuild costs and the expense of upgrading outdated electrical, plumbing, and heating systems to meet current building codes. Homes with recent roof replacements, updated systems, and wind-resistant features qualify for meaningful rate reductions. If you’ve invested in renovations that improve structural integrity or safety, your insurer likely offers discounts worth requesting during your next renewal conversation.

Coverage Limits and Deductible Decisions

Your choice of dwelling coverage amount directly determines your premium. NerdWallet data shows that a $200,000 dwelling limit costs roughly $1,480 annually, while $400,000 coverage runs about $2,490, and $600,000 reaches $3,510. Increasing your deductible from $1,000 to $2,500 typically saves around 9% annually according to NerdWallet research, translating to roughly $230 per year on a $2,490 baseline premium. Raising it further to $5,000 can save approximately 30%, though you must have emergency funds available to cover that higher out-of-pocket amount.

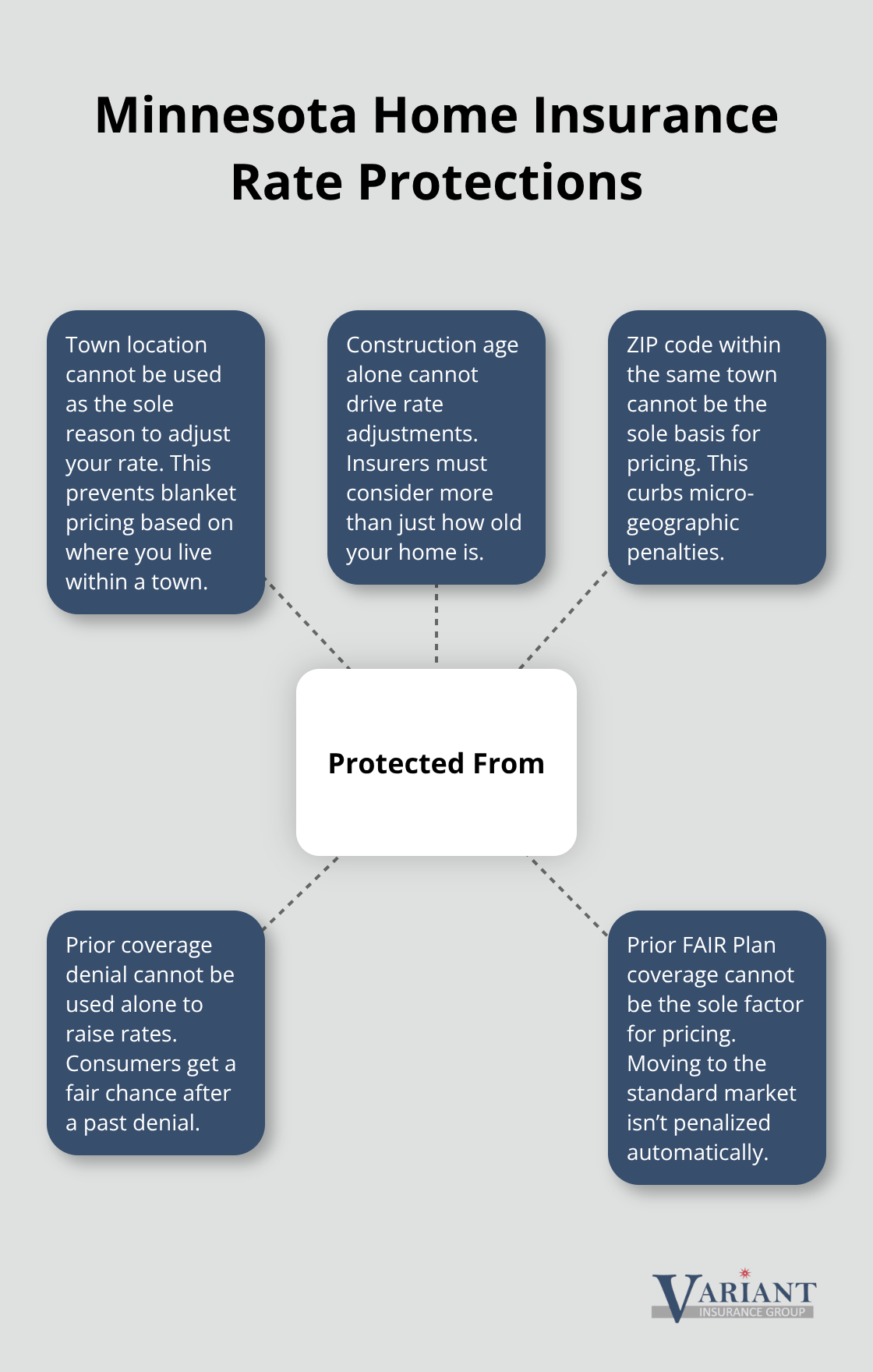

What Minnesota Law Protects You From

Minnesota law prohibits rate adjustments based solely on town location, construction age, zip code within the same town, prior coverage denial, or prior FAIR Plan coverage. These protections shield you from arbitrary geographic penalties and reward you for factors you actually control.

Focus your attention on coverage alignment with your home’s actual replacement cost, strategic deductible selection based on your financial capacity, and investments in safety features like fire alarms or sprinkler systems that most insurers reward with discounts. Your next step involves understanding which specific discounts apply to your situation and how bundling policies can further reduce your overall insurance expenses.

What You’ll Actually Pay for Property Insurance in Minnesota

How Dwelling Coverage Amounts Shape Your Premium

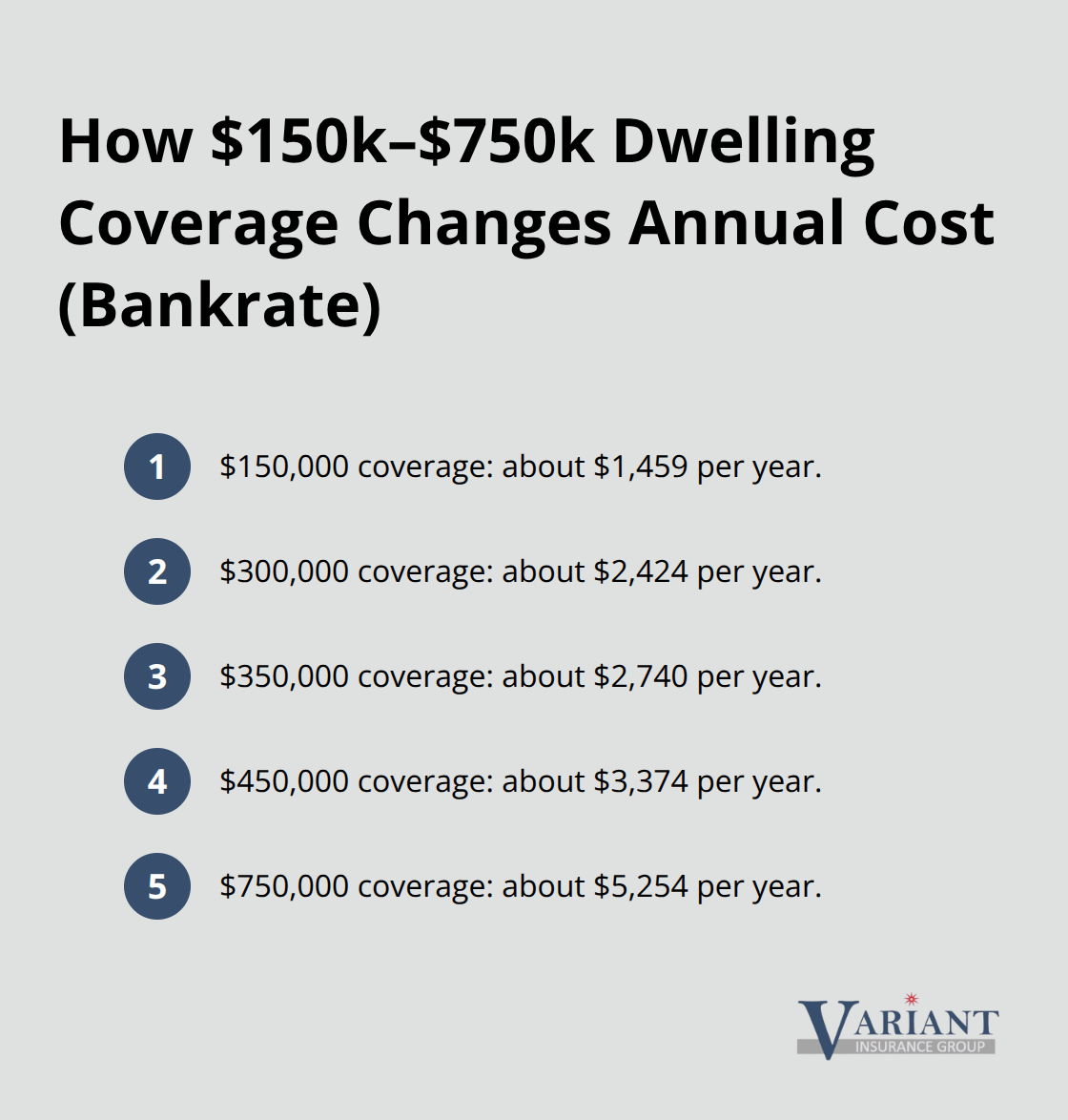

The gap between Minnesota’s average property insurance costs and national figures reveals how local weather patterns and market conditions directly impact your wallet. According to Bankrate’s November 2025 analysis, the national average for homeowners insurance with $300,000 dwelling coverage sits at $2,424 annually. Minnesota homeowners typically pay close to the national average or slightly above, depending on their specific location and home characteristics.

Your dwelling coverage amount directly determines your premium. Bankrate’s data shows that $150,000 dwelling coverage costs roughly $1,459 per year, $300,000 runs about $2,424, $350,000 reaches $2,740, $450,000 climbs to $3,374, and $750,000 dwelling coverage averages $5,254. This means your premium grows proportionally with the coverage you select, not exponentially.

The critical mistake Minnesota homeowners make involves underinsuring their homes to save money upfront, only to face catastrophic out-of-pocket costs when claims occur. The 80% coinsurance rule requires you to insure at least 80% of your home’s actual replacement cost; if you fall short, your payout gets scaled down proportionally on claims. For Minnesota homeowners, this matters enormously given convective storms caused over $50 billion in insured losses nationwide in 2025 alone, according to the Insurance Information Institute.

Deductible Choices Create Direct Savings

Your deductible choice creates the most direct path to savings without sacrificing protection. Moving from a $1,500 deductible to $5,000 can reduce your annual premium from approximately $2,366 to $1,989, saving nearly $400 yearly according to Bankrate’s data. The trade-off requires having emergency funds available to cover that higher deductible when damage occurs, which is why this strategy only works if your financial situation supports it.

How Home Age Affects Your Costs

Home age remains a substantial cost driver that many Minnesota homeowners overlook when evaluating their premiums. Homes built in 1959 average around $3,285 annually compared to 2020-built homes at approximately $2,182 for equivalent coverage, according to Bankrate research. This $1,103 annual difference persists because older homes require more expensive upgrades to meet current building codes and present higher reconstruction costs.

Credit History’s Significant Impact on Premiums

Credit history significantly influences your actual premium where state law permits it, with Bankrate’s analysis showing homeowners with poor credit paying approximately $5,122 more annually than those with excellent credit for identical $300,000 dwelling coverage. This $2,962 annual difference between good and poor credit represents a 72% premium increase on the same policy, making credit improvement one of the highest-return financial decisions you can make for insurance costs.

Minnesota’s Position in the National Cost Spectrum

Comparing Minnesota’s costs to the most expensive and cheapest states in America puts your situation in perspective. Nebraska tops the national list at $6,587 annually for $300,000 dwelling coverage, followed by Louisiana at $6,274 and Florida at $5,838, all driven by extreme weather exposure and higher rebuild costs. Meanwhile, Vermont leads the affordable end at just $827 per year for the same coverage, with Delaware at $966 and Alaska at $1,035. Minnesota’s positioning within this spectrum depends heavily on your specific ZIP code and home characteristics rather than blanket state averages.

Your actual premium ultimately depends on your location within Minnesota, your home’s specific construction details, your coverage selections, and factors you control like deductibles and safety features. Understanding these variables positions you to make informed decisions about which cost-reduction strategies work best for your situation-which brings us to the practical steps you can take to lower your premiums without compromising the protection your home truly needs.

How to Cut Your Property Insurance Costs

Reducing your property insurance premium requires actionable strategies that directly address what insurers charge for. Bundling your homeowners and auto policies stands as one of the most effective approaches Minnesota homeowners overlook. When you combine both policies with the same insurer, most carriers offer discounts ranging from 10% to 25% on your total premiums.

For a Minnesota homeowner paying $4,058 annually for homeowners insurance plus $2,315 for auto coverage, a modest 15% bundling discount saves roughly $950 per year. Many insurers layer additional discounts on top of bundling, such as paperless billing or automatic payment reductions that compound your savings.

Safety Features Lower Your Risk Profile

Safety and security features directly influence how insurers price your risk, making these investments financially rational beyond their protective value. Fire suppression systems like sprinklers, burglar alarms, and deadbolts on all exterior doors typically generate 5% to 15% discounts from most carriers. For homeowners in areas prone to hail damage like Minnesota, impact-resistant roofing materials and reinforced garage doors can reduce your premium by 10% to 20% according to insurance industry data. A homeowner spending $2,000 on a new impact-resistant roof recovers that investment through premium reductions within three to five years while gaining superior storm protection.

Your Claims History Shapes Future Rates

Your claims history shapes how insurers perceive your risk profile, with claims from the past three to five years influencing your rates most heavily. Homeowners without recent claims pay roughly $2,490 annually according to NerdWallet research, while those with a single claim pay around $2,750, representing a 10% premium increase for identical coverage. This means avoiding small claims often costs less than filing them, since your deductible absorbs the damage anyway and your premium increase persists for years. A $3,000 roof damage claim might trigger a $260 annual increase that compounds over multiple years, costing you far more than simply paying out of pocket. The strategic approach involves maintaining your home proactively to prevent claims rather than filing them reactively, which directly benefits your premium trajectory over time.

Final Thoughts

Your average property insurance cost in Minnesota reflects decisions you control and market factors you now understand. Dwelling coverage amounts, deductible choices, home age, and credit history drive your premium more than anything else, while weather risk in Minnesota pushes rates higher than many states. Strategic choices around bundling policies, installing safety features, and maintaining a clean claims history directly reduce what you pay annually.

Shopping quotes from multiple insurers matters more now than ever, since premium differences between carriers for identical coverage can exceed $1,000 annually. When you request quotes, match your desired dwelling coverage, liability limits, and deductible across all three quotes so you compare actual apples to apples rather than different policy structures. This single conversation with three different insurers potentially saves you hundreds of dollars per year.

We at Variant Insurance Group specialize in shopping Minnesota’s top-rated insurance companies to find policies that match your specific needs and budget. Our independent agency works for you rather than a single company, which means we compare protection and prices across carriers to deliver genuine value. Visit us at Variant Insurance Group to discuss how we can help you find affordable coverage that actually protects your home.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation