Running an Airbnb in Minnesota exposes you to risks that standard homeowners insurance won’t cover. Guest injuries, property damage, and business liability gaps can cost thousands.

We at Variant Insurance Group see hosts face major financial losses when they rely solely on personal policies. The right insurance for Airbnb hosts protects your investment and income stream.

What Insurance Gaps Leave Airbnb Hosts Exposed

Homeowners Insurance Falls Short for Rentals

Standard homeowners insurance in Minnesota contains a business use exclusion that automatically voids coverage when you rent your property short-term. Insurance companies classify Airbnb hosting as commercial activity, not personal use. This means guest injuries, property damage, and liability claims get denied under your existing policy. The Minnesota Department of Commerce requires disclosure of rental activity to your insurer, and failure to do so can result in policy cancellation.

Most carriers limit coverage to 30 days of rental activity per year through home-sharing endorsements. These endorsements typically cost $200-400 annually but provide minimal protection. State Farm and Allstate offer these add-ons, but they exclude guest-caused damage and provide no business income protection.

Guest Damage Creates Major Financial Exposure

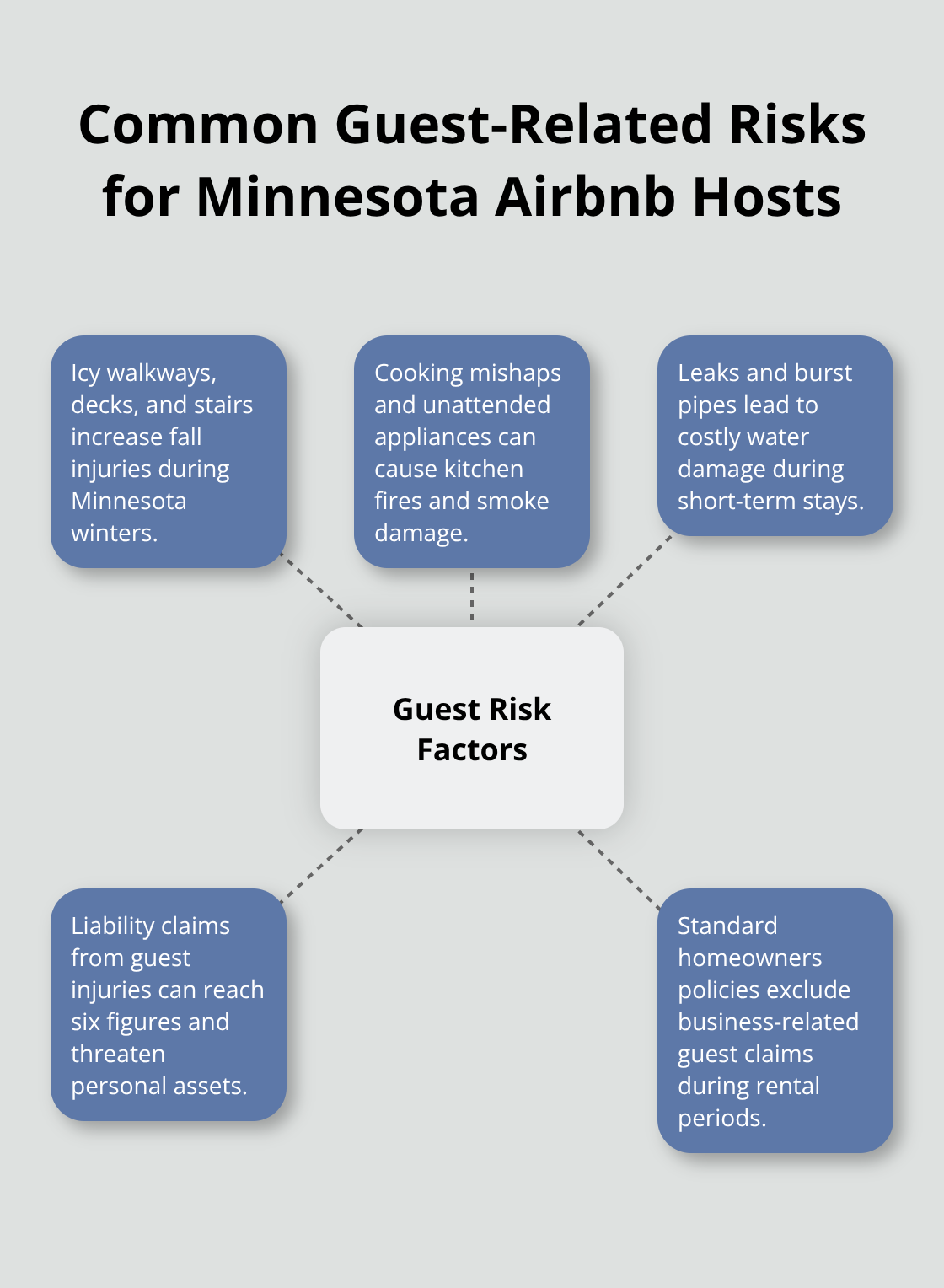

Guest-related incidents create the highest financial exposure for Minnesota hosts. Property damage averages $1,500 per incident according to Airbnb data, while liability claims can reach six figures. Slip-and-fall accidents, kitchen fires, and plumbing disasters happen frequently in short-term rentals. Your homeowners policy excludes these business-related claims entirely.

Minnesota’s dram shop laws make hosts liable for alcohol-related incidents, even when guests bring their own liquor. Hot tubs, fire pits, and lake access increase liability exposure significantly. Winter conditions add slip hazards that standard policies won’t cover during rental periods (especially on icy walkways and decks).

Liability Risks Multiply with Short-Term Guests

Guest theft of electronics, artwork, and furnishings represents another uncovered risk that can cost thousands per incident. Seasonal renters often damage heating systems, leave windows open during freezing weather, or cause water damage through negligence. Standard policies exclude coverage for these business-related losses.

Medical payments coverage also gets voided during rental periods, which leaves guests to pursue hosts directly for injury costs. This creates a double exposure where hosts face both property damage and potential lawsuits from the same incident.

Business Exclusions Void All Policy Benefits

Personal insurance policies contain explicit business use exclusions that void coverage during commercial activity. Even occasional Airbnb hosting triggers these exclusions in Minnesota. Insurers investigate claims thoroughly and deny coverage when they find rental activity (through social media, booking platforms, or neighbor reports). This leaves hosts personally liable for damages and legal costs that can exceed $100,000.

The exclusion applies to all policy benefits including dwelling coverage, personal property protection, and liability insurance. These gaps make specialized short-term rental insurance essential for protecting your investment and income stream.

What Insurance Options Actually Protect Airbnb Hosts

Minnesota Airbnb hosts need specialized coverage that fills the gaps left by standard homeowners policies. Commercial short-term rental insurance provides unmatched property, business liability and lost revenue coverage for short-term rental hosts, including owners and arbitrageurs.

Commercial Short-Term Rental Insurance Delivers Complete Protection

Proper Insurance offers policies that start at $200-400 annually with $1 million in liability coverage and protection against guest-caused damage up to $2 million. These policies include bed bug coverage, squatter protection, and liquor liability that standard policies exclude entirely. CBIZ and Farmers also offer dedicated short-term rental policies, but Proper Insurance remains the preferred provider endorsed by Vrbo for its comprehensive coverage and specialized claims process.

We at Variant Insurance Group can help you compare these specialized policies from Minnesota’s top-rated insurance companies to find the perfect coverage for your short-term rental property. Our team reviews your specific situation and compares protection levels and prices across multiple carriers.

Airbnb Host Protection Has Major Limitations

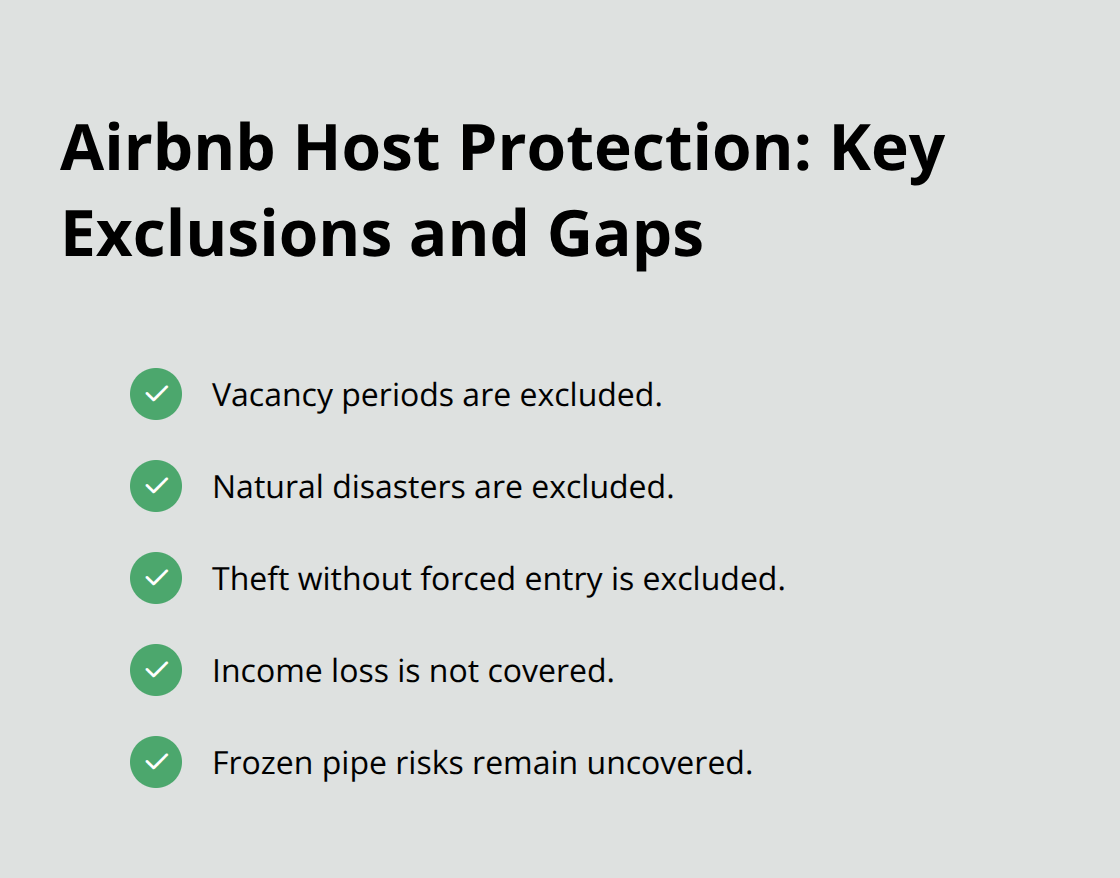

Airbnb’s Host Protection Insurance provides $1 million in liability coverage, but it functions as secondary insurance with significant restrictions. The program excludes coverage for intentional damage, normal wear and tear, and incidents that involve pets or smoking (claims must be filed within 14 days). While sites like Airbnb do offer some property protection for hosts against damage by a guest, it does not include liability insurance.

The program also excludes coverage when properties are vacant, during natural disasters, or for theft when no forced entry occurs. Minnesota hosts who rely solely on Airbnb’s protection face major gaps, particularly for income loss and specialized risks like frozen pipes during winter months.

Umbrella Policies Require Commercial Classification

Personal umbrella policies exclude business activities and make them worthless for Airbnb liability claims in Minnesota. Commercial umbrella insurance extends liability coverage beyond base policy limits and typically adds $1-5 million in protection for $300-600 annually. These policies require commercial coverage and won’t attach to personal homeowners insurance.

State Farm and Travelers offer commercial umbrella policies that stack on top of short-term rental insurance and provide extra protection against catastrophic claims. The coverage applies to guest injuries, property damage lawsuits, and defense costs that can reach $50,000 even for frivolous claims.

Understanding these coverage options helps you make informed decisions, but the actual cost depends on several factors specific to your property and location.

What Does Short-Term Rental Insurance Actually Cost

Short-term rental insurance costs 2-4 times more than standard homeowners coverage, but the protection justifies the expense. Commercial policies range from $800-2,400 annually for properties worth $200,000-500,000, while homeowners insurance averages $1,200-1,800 for the same properties. Proper Insurance quotes start at $200-400 annually for basic coverage, but comprehensive policies with $2 million property protection and business income coverage cost $1,500-3,000 per year. The premium difference reflects the higher risk exposure and specialized coverage that protects against guest damage, liability claims, and lost rental income that standard policies exclude entirely.

Minnesota Requirements Drive Up Costs

Minnesota municipalities have specific requirements for short-term rental operators that vary by city. These municipal requirements force hosts into commercial policies since personal insurance won’t meet the thresholds. Properties in Duluth face additional requirements for seasonal weather protection, while lake properties need specialized water liability coverage that adds $300-600 annually. The Minnesota Department of Commerce mandates disclosure of rental activity to insurers (which makes it impossible to hide commercial use under personal policies). Hosts who attempt this face policy cancellation and claim denials that can cost tens of thousands.

Property Value and Location Create Major Rate Variations

Lake properties in Brainerd and Grand Rapids pay 40-60% higher premiums due to water liability and seasonal access challenges. Downtown Minneapolis properties face theft and vandalism risks that increase rates by 25-35% compared to suburban locations. Properties worth over $500,000 require higher coverage limits and pay premiums of $3,000-5,000 annually for comprehensive protection.

Rural cabins in northern Minnesota get lower liability rates but need specialized coverage for propane systems, well water, and septic issues that add $400-800 to annual premiums. Winter sports areas like Lutsen command premium rates due to injury risks from activities that standard policies won’t cover.

Coverage Limits Affect Premium Calculations

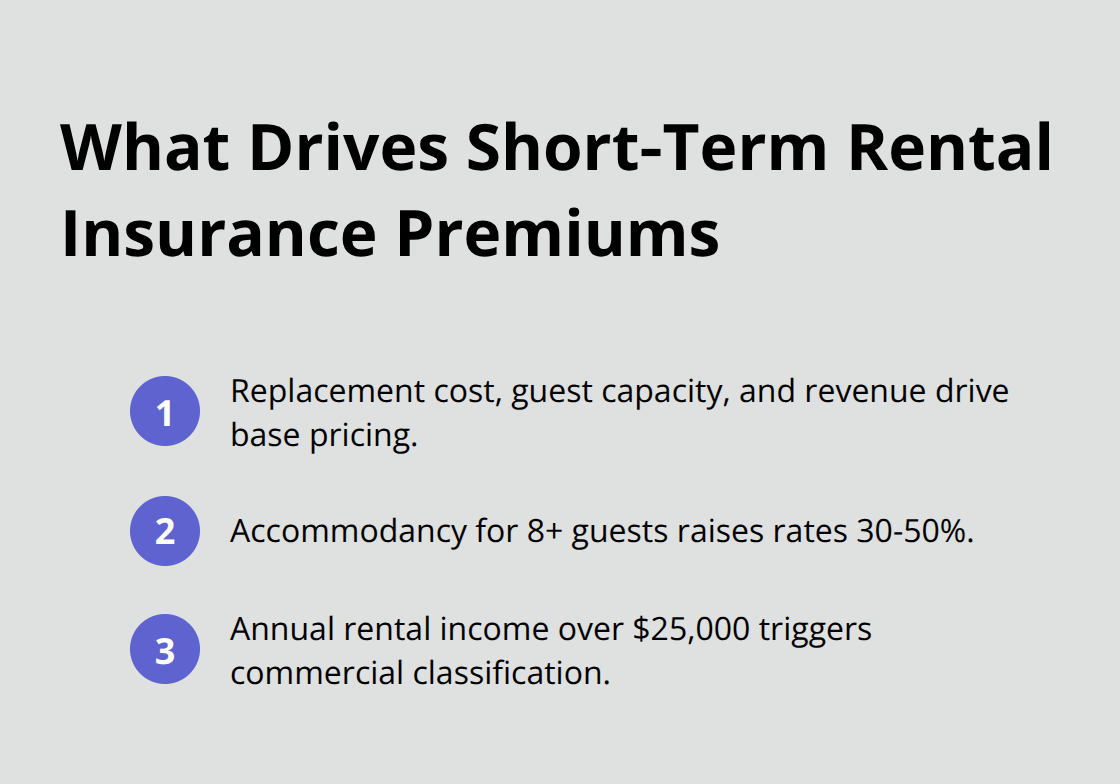

Insurance companies calculate premiums based on property replacement cost, guest capacity, and revenue potential. Properties that accommodate 8+ guests pay 30-50% higher rates than smaller units due to increased liability exposure. Hosts who generate over $25,000 annually in rental income face commercial classification requirements that double their insurance costs (but provide comprehensive business protection).

Deductibles range from $1,000-5,000 for property damage claims, with higher deductibles reducing annual premiums by 15-25%. Most carriers require minimum $1 million liability limits, but hosts with significant assets should consider $2-5 million coverage to protect against catastrophic claims.

Final Thoughts

Minnesota Airbnb hosts require commercial short-term rental policies that deliver $1-2 million in liability coverage, guest damage protection, and business income replacement. Standard homeowners insurance excludes rental activity entirely and exposes hosts to catastrophic financial losses. The right insurance for Airbnb hosts costs $800-3,000 annually but protects against claims that exceed $100,000.

Properties near lakes, in downtown areas, or those that accommodate large groups face higher premiums but need this specialized coverage to operate legally and safely. Commercial policies provide comprehensive protection that personal insurance cannot match. These policies cover guest injuries, property damage, and lost rental income that standard homeowners policies exclude completely.

We at Variant Insurance Group work with Minnesota carriers to find comprehensive short-term rental policies that fit your property and budget. Our team compares coverage options from multiple companies and helps you secure proper protection without excess costs (while handling the application process and claims support). Contact Variant Insurance Group to compare specialized policies that protect your investment and income stream from the risks that come with short-term rental operations in Minnesota.