Mold in your Minnesota home can be costly and stressful. But here’s the reality: most standard homeowners insurance policies don’t cover mold damage, which leaves many homeowners vulnerable.

At Variant Insurance Group, we help Minnesota residents understand their coverage gaps. This guide explains what your policy actually covers, why mold claims get denied, and how to protect your home before problems start.

What Causes Mold in Homes

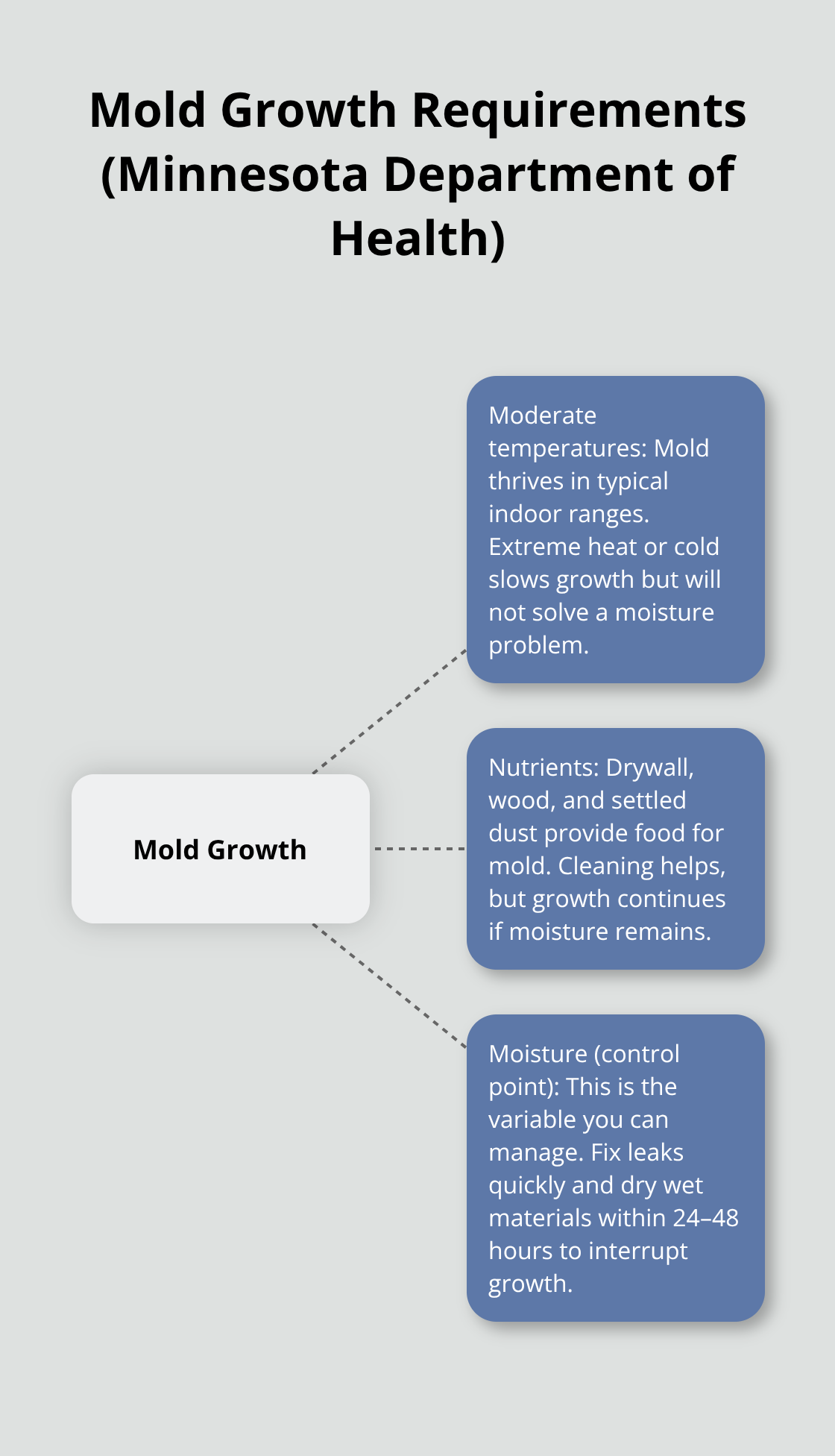

Water intrusion drives mold growth in Minnesota homes, and it comes from multiple sources that homeowners often overlook until damage spreads. Burst pipes, failed water heaters, and plumbing failures rank among the most common culprits-a single burst pipe can saturate walls and floors within hours, creating ideal conditions for mold to colonize. According to the Minnesota Department of Health, mold requires three elements to grow: moderate temperatures, nutrients, and moisture. You control moisture most effectively, which makes it the most powerful prevention strategy since it eliminates the one variable you can actually manage. Heavy rainfall and roof failures also drive mold growth, particularly in basements and crawlspaces where water seeps through foundations.

Minnesota’s seasonal temperature swings and freeze-thaw cycles increase the risk of burst pipes and ice dam damage, both of which create moisture problems that lead directly to mold.

Indoor Humidity and Ventilation Failures

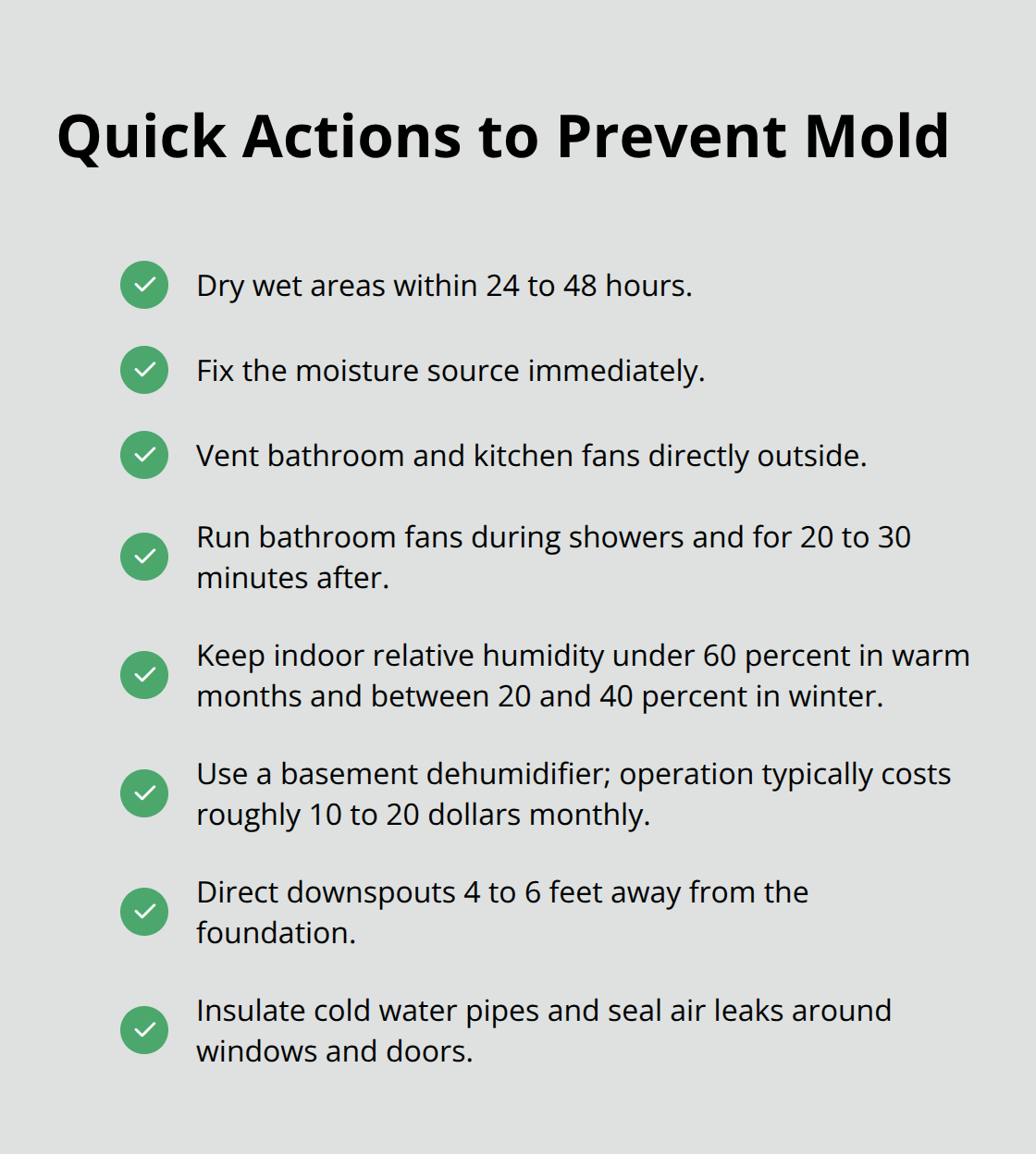

Poor ventilation and high humidity create persistent moisture that supports mold growth over weeks and months. Minnesota winters trap moisture inside homes when exhaust fans vent into attics or crawlspaces instead of outdoors, and bathroom and kitchen humidity accumulates when fans are inadequate or unused. The Minnesota Department of Health recommends you maintain indoor relative humidity between 20 to 40 percent in winter and under 60 percent the rest of the year-an inexpensive humidity meter helps you monitor levels in problem areas like basements and bathrooms. Condensation on windows and walls signals that humidity is too high; address it immediately because mold will follow within days. Many Minnesota homeowners skip dehumidifiers in basements, but a dehumidifier in damp areas ranks as one of the most cost-effective mold prevention tools available (roughly 10 to 20 dollars monthly to operate).

Why Floods and Foundation Water Matter

Flooding from heavy rainfall or sump pump failure introduces large volumes of water that standard homeowners insurance typically excludes. Minnesota experiences occasional extreme weather events-a 1 in 500 year storm illustrates how unpredictable water damage can be-and water that seeps through foundations during these events almost never receives coverage under standard policies. If you live in a flood-prone area or have a history of basement water, you need separate flood insurance or water backup coverage. Water backup coverage protects against damage from sewer backups or sump pump overflow, both common triggers for mold in basements (and both preventable with proper maintenance). You must dry any water in your home within 24 to 48 hours to minimize mold growth, and you should repair water sources the moment you discover them.

Understanding what causes mold in your Minnesota home is the first step toward protection, but knowing whether your policy covers mold damage requires a closer look at your actual coverage.

What Your Homeowners Policy Actually Covers for Mold

Standard homeowners insurance covers mold only when it results from a sudden, accidental event specified in your policy-not from gradual moisture buildup or neglect. Burst pipe mold coverage qualifies for coverage under most policies. A water heater failure, frozen and burst pipes, or a malfunctioning appliance like a refrigerator that leaks trigger mold coverage. Fire damage extinguished with hose water that creates dampness may also be covered. However, mold from ongoing leaks, humidity and condensation, poor ventilation, or water seeping through your foundation almost never receives coverage because insurers classify these as maintenance issues or gradual damage. The distinction matters enormously: if mold has been present for weeks or longer, your claim will likely face denial regardless of how visible the problem is. Minnesota policies vary by insurer, so the coverage your neighbor has may differ significantly from yours.

What Insurers Exclude from Mold Coverage

Farm Bureau Financial Services explicitly excludes coverage for mold resulting from neglect, ongoing leaks, or humidity and condensation, and this exclusion appears across most standard policies statewide. Water damage from floods is typically excluded entirely, which is why separate flood insurance becomes critical if you live in a flood-prone Minnesota county. Mold that develops over weeks or months receives no coverage because insurers treat it as a maintenance failure rather than a covered peril. Your policy language determines what qualifies as sudden and accidental-vague terms like water damage can mean different things depending on how your insurer interprets them.

Coverage Limits and What Gets Paid

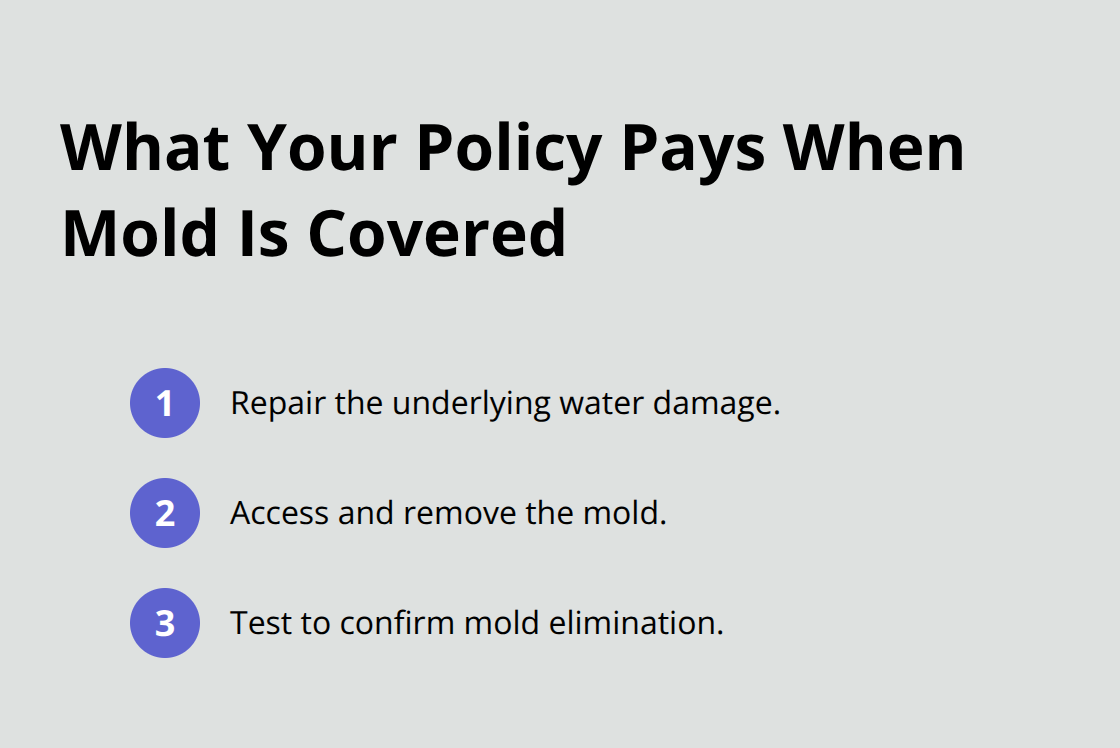

When mold is covered under a sudden water damage claim, your policy reimburses three specific costs: the expense to repair the underlying water damage, the cost to access and remove the mold, and the cost of testing to confirm elimination. However, most policies cap mold coverage between 5,000 and 10,000 dollars, far below what extensive remediation actually costs in Minnesota. If mold extends behind walls or into attic spaces, removal expenses escalate rapidly-professional remediation for hidden mold can exceed 25,000 dollars.

Your deductible applies to the entire water damage claim, not just the mold portion, so a 1,000 dollar deductible reduces your reimbursement significantly. You cannot add mold coverage retroactively once water damage has occurred, which means you must address coverage gaps before problems arise.

Water Backup Coverage and Sump Pump Protection

Adding water backup coverage to your policy protects against mold from sewer backups or sump pump failure, both common basement scenarios in Minnesota. This optional endorsement costs roughly 50 to 100 dollars annually depending on your insurer. If you have a sump pump, water backup coverage becomes essential protection rather than optional luxury because sump pump failure introduces large volumes of water that standard policies exclude.

Minnesota Requirements and Your Next Step

Minnesota does not mandate mold coverage in homeowners policies, leaving decisions entirely to insurers and policyholders. The Minnesota Insurance Commissioner allows insurers substantial flexibility in how they define covered water damage and mold exclusions. Your policy document contains specific language about what water damage qualifies and what mold scenarios are excluded. Contact your agent immediately to clarify whether mold from burst pipes, appliance failure, and water backup scenarios receives coverage under your current policy. Ask your agent directly: does my policy cover mold from a burst pipe, and if so, what is the dollar limit? Most Minnesota homeowners discover coverage gaps only after damage occurs, which is far too late. If your current policy lacks adequate mold protection, you need to explore carriers offering higher mold limits or more favorable coverage terms that fit your actual risk profile. Understanding your current coverage gaps sets the stage for the most effective mold protection strategy: prevention.

How to Stop Mold Before Water Damage Spreads

The most effective mold prevention strategy stops water before it becomes a problem. Most Minnesota homeowners wait until they see mold to act, but by then the damage extends behind walls and into structural components where professional remediation costs thousands of dollars. Water intrusion happens fast-a burst pipe saturates drywall within hours, and condensation on basement walls signals moisture accumulation that will fuel mold growth within days. The Minnesota Department of Health emphasizes that controlling moisture eliminates the single variable you can actually manage, which makes it your strongest defense. Start with monthly inspections for water leaks around pipes under sinks, behind toilets, and near water heaters; catching a slow leak early costs nothing compared to the thousands you might spend on mold remediation later.

Inspect Your Home’s Water Vulnerabilities

Check your roof for missing shingles or damaged flashing after heavy rain, particularly in spring when Minnesota’s freeze-thaw cycles crack roofing materials. Direct downspouts at least 4 to 6 feet away from your foundation to prevent water from seeping into basements. If you find standing water or wet spots in your basement, dry the area completely within 24 to 48 hours and identify the moisture source immediately-waiting even one week allows mold spores to colonize and spread rapidly.

Control Humidity in High-Risk Areas

Humidity control in basements and bathrooms matters more than most homeowners realize because it addresses the moisture that feeds mold growth before water damage even occurs. Install a humidity meter in your basement and monitor it weekly; if readings exceed 60 percent, mold will develop within weeks regardless of visible water. A dehumidifier in your basement costs roughly 10 to 20 dollars monthly to operate and prevents the musty odor that signals mold is already growing.

Manage Ventilation and Condensation

Exhaust fans in bathrooms and kitchens must vent directly outside your home, never into attics or crawlspaces where moisture accumulates and creates hidden mold problems. Run bathroom fans during showers and for 20 to 30 minutes afterward to remove moisture before it settles on walls and windows. Insulate cold water pipes and seal air leaks around windows and doors to prevent condensation buildup during Minnesota winters. If you notice condensation on windows or walls, wipe it dry immediately and increase ventilation because condensation indicates humidity is too high.

Address Mold Growth Professionally

Professional mold remediation should happen only after you eliminate the moisture source, otherwise mold will return within weeks and you waste remediation costs. If mold covers an area larger than 10 square feet or extends into walls and attic spaces, hire a licensed mold remediation company rather than attempting cleanup yourself-hidden mold growth spreads faster than visible growth and requires professional equipment and expertise to remove safely. Confirm whether your policy covers mold remediation costs if water damage occurs, then schedule a professional inspection of your roof, foundation, and plumbing to identify vulnerabilities before Minnesota’s heavy spring rains arrive.

Final Thoughts

Mold damage in your Minnesota home creates real financial and health risks, but whether homeowners insurance covers mold damage depends entirely on how the mold started. If mold results from a sudden, accidental event like a burst pipe or appliance failure, your policy likely covers removal and repair costs up to your policy limit. If mold develops from gradual moisture buildup, poor ventilation, or foundation seepage, your claim will face denial because standard policies exclude these scenarios.

If you discover mold in your home, stop the moisture source immediately and dry the affected area within 24 to 48 hours to prevent rapid spread. Document the water damage with photos and notes about when you discovered it, then contact your insurance agent to report the loss. Do not delay this step because insurers require prompt notification, and waiting weeks weakens your claim.

Your best protection against mold damage combines prevention with the right coverage. Contact Variant Insurance Group today to review your homeowners policy and confirm you have adequate mold protection in place.