Trampolines are fun, but they come with real liability risks that most standard homeowners policies don’t cover. A single injury on your trampoline can lead to expensive medical bills and lawsuits that exceed your policy limits.

At Variant Insurance Group, we help Minnesota homeowners understand their coverage gaps and find solutions that protect both their families and their finances. The right homeowners insurance for trampoline owners requires some extra planning, but it’s manageable once you know what to look for.

Why Trampolines Create Real Insurance Problems

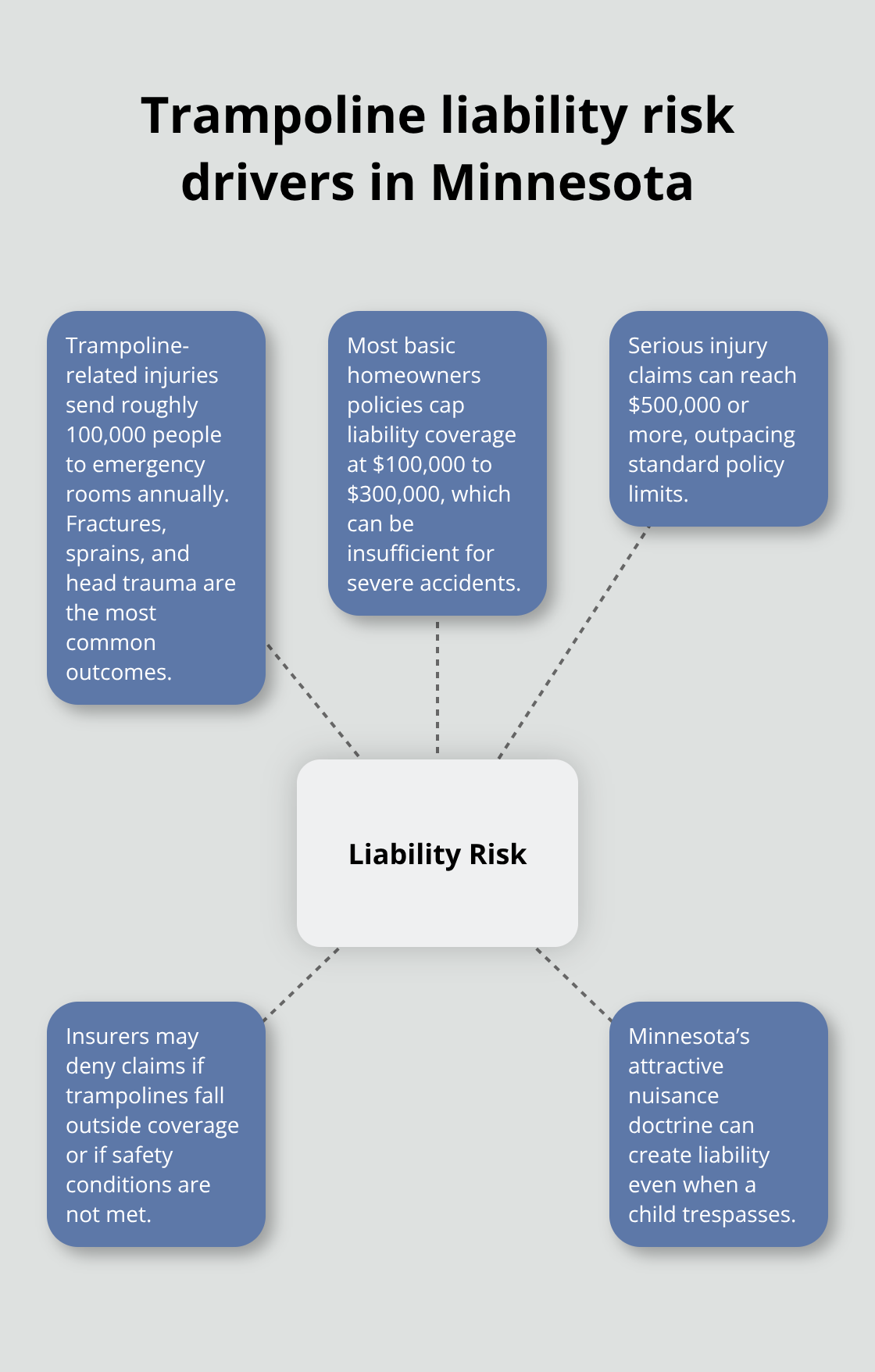

Trampolines cause more injuries than most homeowners realize. The American Academy of Pediatrics reports that trampoline-related injuries send roughly 100,000 people to emergency rooms annually, with fractures, sprains, and head trauma being the most common outcomes. A single serious injury on your trampoline can trigger a liability claim that far exceeds your standard homeowners policy limits. Most basic homeowners policies cap liability coverage at $100,000 to $300,000, but a severe injury case involving permanent disability or long-term medical care can easily reach $500,000 or more in damages. Your insurance company may deny the claim entirely if they determine that trampolines fall outside your coverage, leaving you personally responsible for every dollar. This gap between what your policy covers and what you actually owe is exactly why trampoline owners face financial exposure that keeps them up at night.

The Attractive Nuisance Problem in Minnesota

Minnesota courts recognize the attractive nuisance doctrine, which means you have heightened legal liability if a child trespasses on your property and gets injured by something that naturally draws children in-like a trampoline. Under the Restatement of Torts Section 339, a property owner can be liable if a child is harmed by a hazard on the land, the owner knew children were likely to trespass, and the owner failed to take reasonable precautions. A neighbor’s child who sneaks into your yard and breaks an arm on your trampoline could trigger a lawsuit against you, even though the child was technically trespassing. Your homeowners policy may exclude or severely limit coverage for injuries involving trespassing children, or the insurer might claim you violated policy conditions by not securing the trampoline adequately. This legal exposure makes trampoline coverage a serious gap in protection for Minnesota homeowners.

What Standard Policies Actually Exclude

Most insurers either exclude trampolines entirely from coverage or require expensive endorsements and strict safety conditions to keep them covered. Some carriers will drop your entire homeowners policy if you install a trampoline without notifying them first. Even when trampolines are covered, the policy may only protect you for injuries to invited guests on your property, not trespassing children. Damage caused by your trampoline to your own home-like high winds launching it through a window-might be covered under dwelling or personal property coverage, but injuries to third parties often fall into a coverage gap. Annual surcharges for trampoline coverage typically range from $40 to $100 per year, but this is only if your insurer will cover them at all. The bottom line is that standard homeowners policies were not designed with trampolines in mind, and relying on your current coverage without verification could leave you seriously exposed.

Why You Need to Act Now

The financial stakes are too high to wait. Once you install a trampoline, your existing policy may no longer apply to trampoline-related claims, and some insurers will not add coverage retroactively. If an injury happens before you notify your insurer, you could face a claim denial that leaves you liable for the full amount. The cost of adding trampoline coverage upfront (typically $40–$100 annually) is far less than the cost of defending a lawsuit or paying damages out of pocket. Taking action now protects your family and your finances, and it also ensures that your coverage remains valid if an accident occurs. The next step is to review what your current policy actually says about trampolines and explore your options with an agent who understands Minnesota’s specific liability landscape.

How to Protect Your Trampoline Investment

Pull out your homeowners policy and read the section on coverage exclusions and endorsements. Most Minnesota homeowners have no idea whether their policy covers trampolines until they call their agent or file a claim. Look for language about trampolines, attractive nuisances, or premises liability limitations. If your policy is silent on trampolines, that silence is dangerous-it typically means your insurer hasn’t evaluated the risk and may deny claims later.

Contact your agent immediately and ask three specific questions: Does my current policy cover trampoline-related injuries? If yes, what are the limits and exclusions? If no, what options exist to add coverage? Some insurers will add trampoline coverage through an endorsement for $40–$100 annually, while others refuse entirely. If your carrier won’t cover trampolines, you need to know that now, not after an accident. Document your agent’s response in writing so you have proof of what was discussed.

Layer Protection with Umbrella Coverage

Standard homeowners liability limits of $100,000 to $300,000 are insufficient for trampoline owners in Minnesota. A serious injury case involving permanent disability, lost wages, and medical care can easily reach $500,000 or more. This is where umbrella insurance becomes essential.

An umbrella policy sits above your homeowners coverage and provides additional liability protection, typically in increments of $500,000 to $1,000,000. The cost is surprisingly affordable-most umbrella policies run $150–$300 annually for $500,000 in extra coverage. If your homeowners policy covers your trampoline but only to $100,000, and a lawsuit demands $400,000, your umbrella policy covers the $300,000 gap. Without it, you personally owe that difference.

Any Minnesota homeowner with a trampoline should carry at least $500,000 in umbrella coverage. This single step removes most of your financial exposure and protects your home and savings from a single accident.

Install Safety Measures That Insurers Require

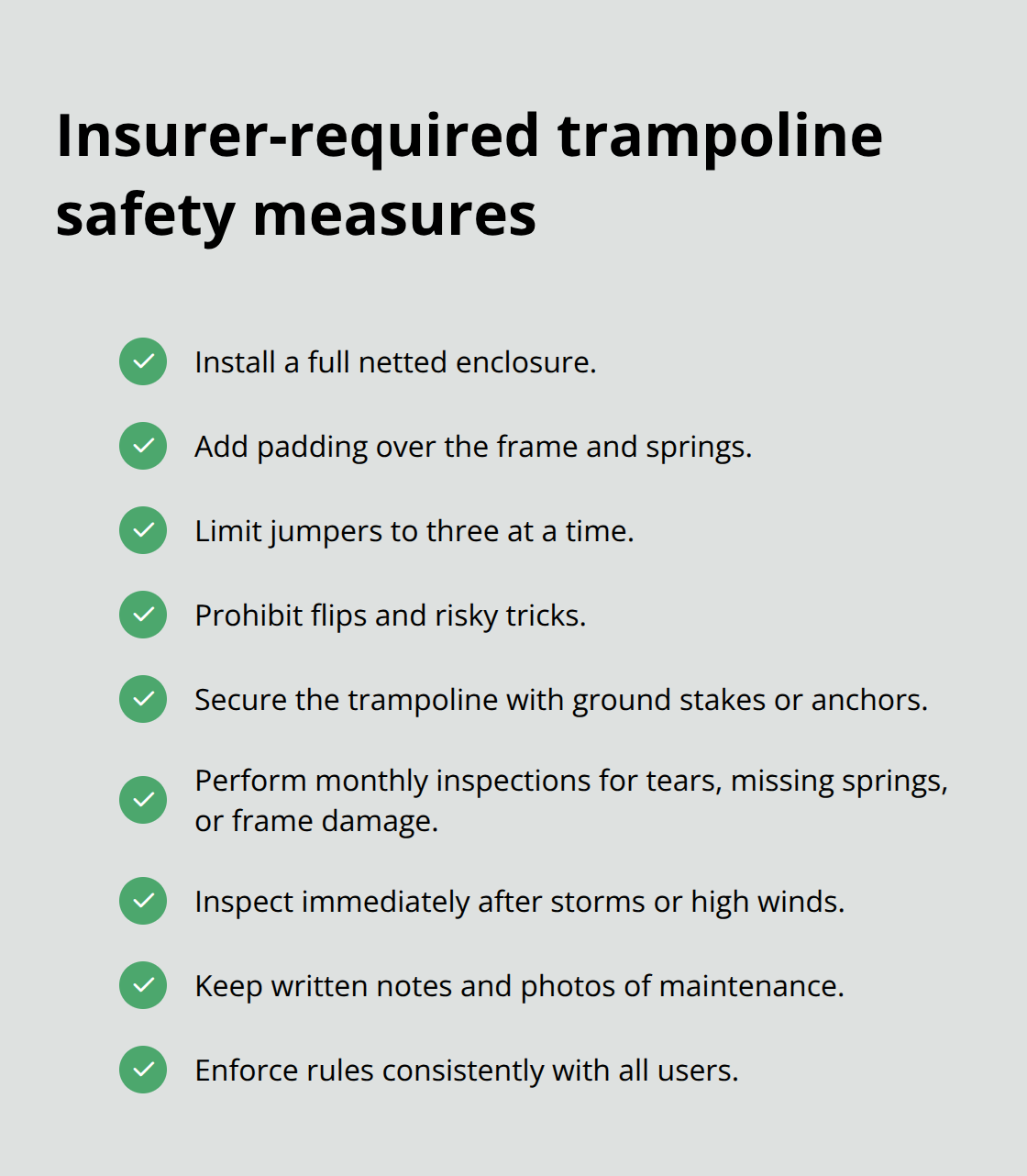

Many insurers will only cover trampolines if you install specific safety equipment and follow usage rules. A netted enclosure is the most common requirement-it prevents users from bouncing out and reduces fall injuries significantly. Padding around the frame and springs is also standard.

Establish and enforce clear usage rules: limit jumpers to three at a time, prohibit flips and tricks, secure the trampoline to the ground with stakes or anchors, and perform monthly inspections for tears, missing springs, or frame damage. After storms or high winds, inspect immediately for damage that could create additional hazards. These practices do more than satisfy your insurer-they reduce injury risk and demonstrate that you take safety seriously.

If you fail to maintain the trampoline or allow unsafe use, your insurer can deny a claim based on policy violations. Document your maintenance with photos and notes. If a child is injured on your trampoline, your insurer will investigate whether you followed safety conditions. Proper maintenance and clear rules are your strongest defense against claim denial and your best protection for your family.

Your next step involves finding the right insurance partner who understands Minnesota’s trampoline liability landscape and can shop multiple carriers to find the coverage that fits your specific situation.

Finding the Right Agent for Your Trampoline Coverage

Most Minnesota homeowners make a critical mistake when shopping for trampoline coverage: they call their current insurance agent, get a yes or no answer, and stop there. This approach leaves money on the table and often results in inadequate protection.

Why Independent Agents Outperform Captive Agents

Independent insurance agents have access to multiple carriers, which means they can compare rates and coverage options across 10, 15, or even 20 different insurers instead of being locked into a single company’s underwriting rules. Some carriers flatly refuse trampoline coverage, while others offer it with reasonable rates and minimal restrictions. An independent agent knows which insurers in Minnesota actively write trampoline coverage and which ones will deny claims or drop policies.

When you work with a captive agent representing one insurance company, you get that company’s answer. When you work with an independent agent, you get the market’s answer. The difference in price and coverage quality is often substantial.

How to Request and Compare Quotes

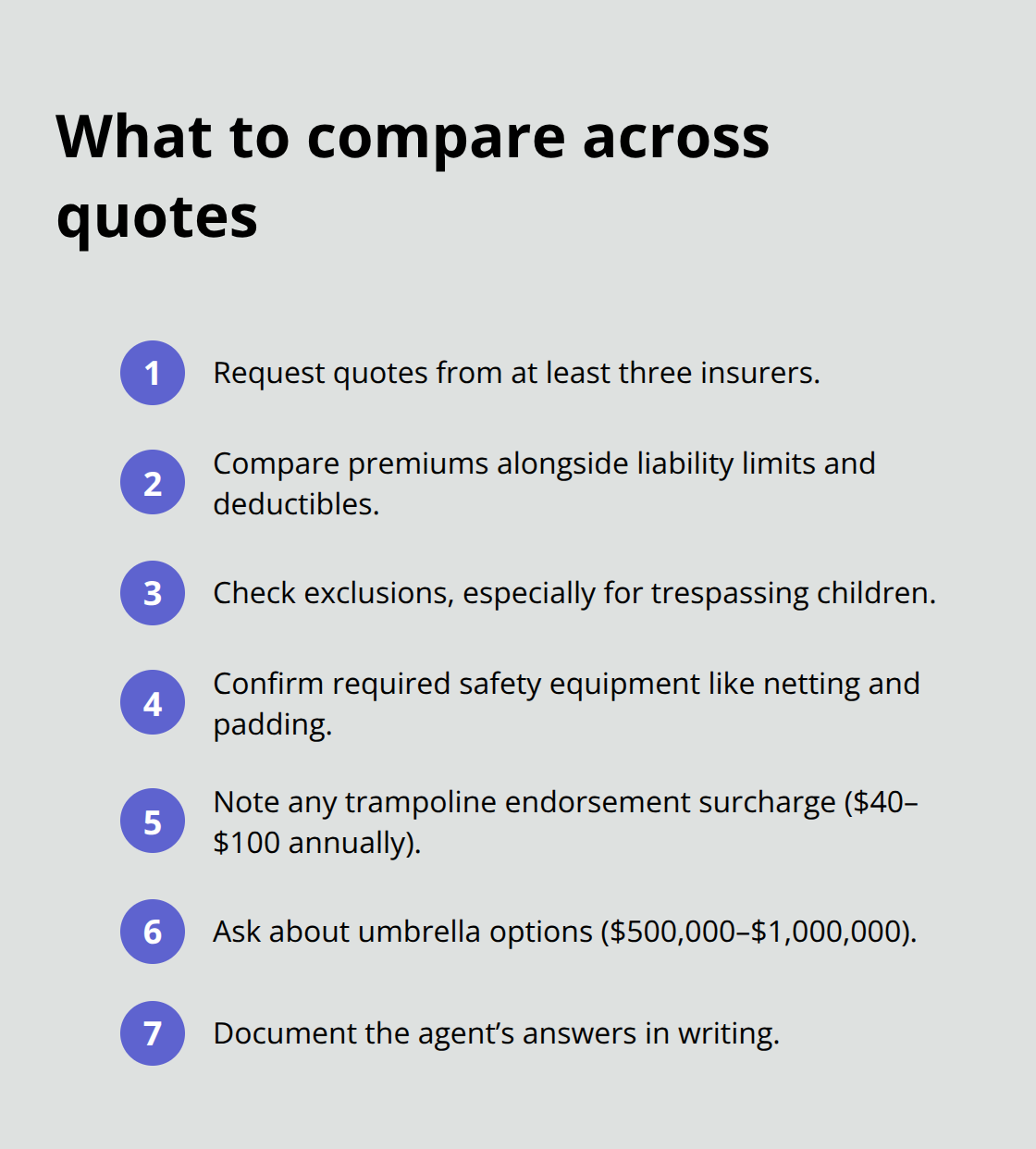

Start by contacting an independent agent and explicitly state that you own or plan to install a trampoline. Ask them to quote coverage from at least three different insurers. Most agents can provide quotes within 24 to 48 hours.

Compare not just the premium cost but also the coverage limits, deductibles, safety requirements, and any exclusions. A cheaper policy that excludes trespassing children provides less actual protection than a slightly more expensive policy with broader liability coverage. Pay close attention to whether the insurer requires specific safety equipment like netting or padding, because these requirements affect both your costs and your ongoing liability exposure.

Combine Homeowners and Umbrella Coverage Strategically

The conversation with your agent should address umbrella insurance as part of your total protection strategy. Many independent agents can bundle your homeowners trampoline coverage with an umbrella policy, sometimes at a discounted rate. Ask your agent whether adding umbrella coverage at the time you implement trampoline coverage qualifies for any multi-policy discounts.

Your agent should also walk you through the specific safety conditions your chosen insurer requires and confirm that you understand what actions could void your coverage. If an insurer requires a netted enclosure but your trampoline lacks one, that’s a claim denial waiting to happen.

Document Requirements and Maintain Your Coverage

A good independent agent documents these requirements in writing and follows up to confirm you’ve implemented them. After you’ve selected a carrier and implemented coverage, schedule a follow-up conversation with your agent annually, ideally before summer when trampoline use peaks.

Your situation may change-your home value might increase, your liability exposure might grow if neighborhood children frequent your yard, or new coverage options might become available from your insurer. An agent who stays engaged with your account catches these changes and adjusts your coverage proactively rather than waiting for a problem to emerge.

Final Thoughts

Trampoline ownership in Minnesota exposes you to liability that standard homeowners policies simply don’t address. The combination of high injury rates, Minnesota’s recognition of the attractive nuisance doctrine, and widespread coverage gaps means you face potential liability reaching hundreds of thousands of dollars. Protecting yourself requires action, but the steps are straightforward once you commit to them.

Three concrete actions transform trampoline ownership from a financial gamble into manageable risk. First, review your current homeowners policy and contact your agent to understand what your insurer will and won’t cover regarding trampolines. Second, add umbrella insurance to bridge the gap between your homeowners liability limits and the actual cost of a serious injury claim. Third, install the safety equipment your insurer requires and maintain it consistently throughout the year. An independent agent makes this process far easier than navigating it alone, because they have access to multiple Minnesota carriers and know which ones actively write homeowners insurance for trampoline owners at reasonable rates.

At Variant Insurance Group, we specialize in shopping Minnesota’s top-rated insurance companies to find the right coverage for trampoline owners. Contact Variant Insurance Group or another independent agent in your area and schedule a conversation about your trampoline coverage. Bring your current homeowners policy, describe your trampoline setup and safety measures, and ask for quotes from multiple carriers.