Leaving a home vacant creates insurance complications most standard policies don’t address. Insurers view empty properties as higher risk, which means gaps in coverage and potential claim denials when you need protection most.

At Variant Insurance Group, we help Minnesota homeowners understand that homeowners insurance for unoccupied homes requires specialized protection. The right coverage makes the difference between financial security and unexpected losses while your property sits empty.

Why Standard Policies Don’t Cover Vacant Homes

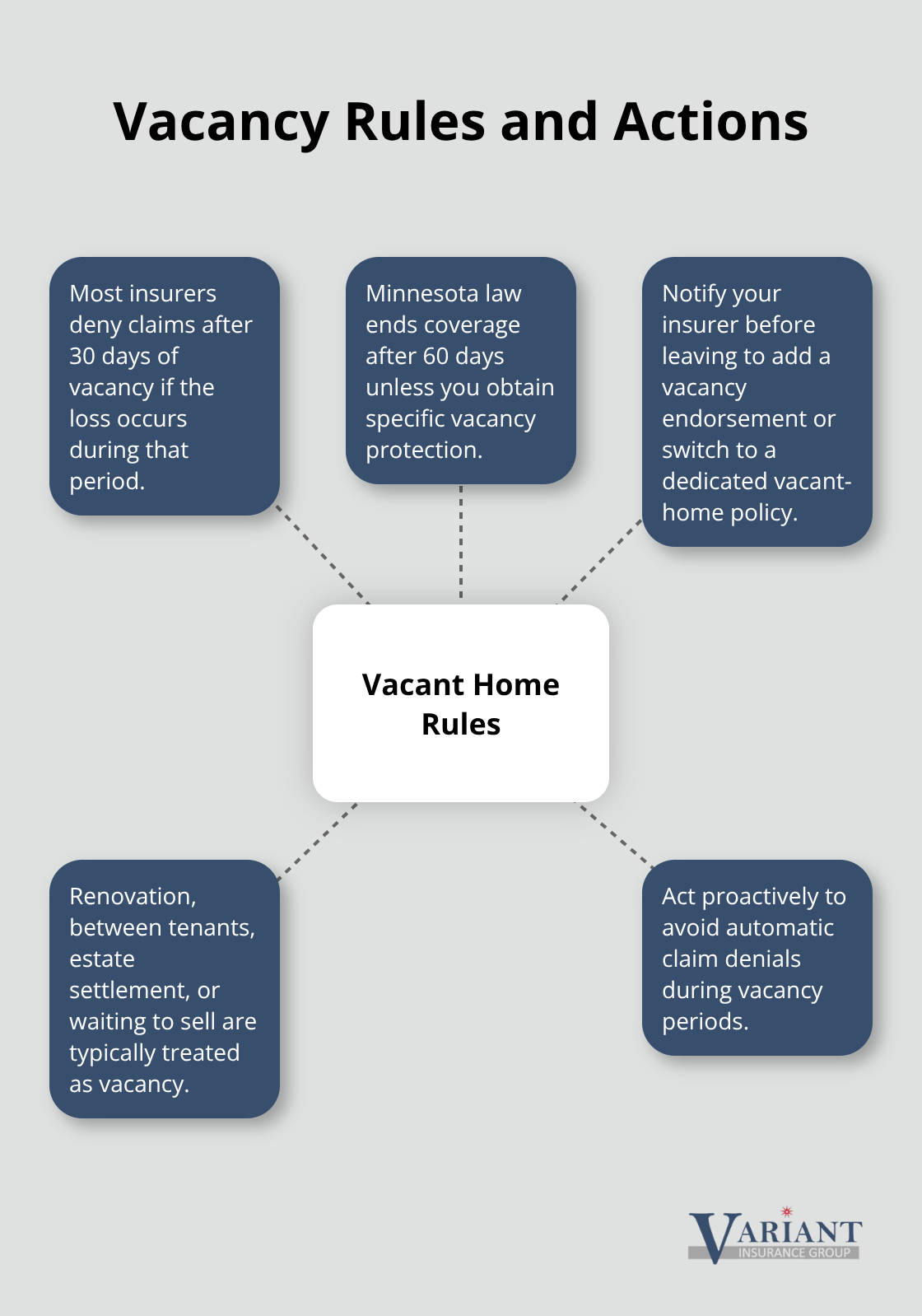

Your standard homeowners insurance policy has a hard cutoff. According to Minnesota Statutes 65A.01, if your home sits vacant or unoccupied for more than 60 consecutive days, the policy stops covering losses that occur during that vacancy period. Most insurers tighten this window even further, with many policies excluding coverage after just 30 days of vacancy. This isn’t a gray area or a technicality you can negotiate around-it’s a built-in exclusion that leaves your property unprotected exactly when it’s most vulnerable.

Why Insurers Exclude Vacant Properties

When you leave a home empty, insurers assume you won’t monitor it for problems. A burst pipe, electrical fire, or break-in can go undetected for weeks. That delay multiplies the damage and cost. Vandalism claims rank as the most commonly reported loss for vacant properties, followed by fire, smoke, lightning, water damage, and theft. A standard homeowners policy won’t pay for any of these while your home sits empty.

The Financial Impact of Coverage Gaps

The financial impact hits hard when a claim gets denied. You file a claim for water damage from frozen pipes, and the insurer denies it because you failed to notify them of the vacancy. You report a break-in and theft of appliances, only to learn that theft isn’t covered under your lapsed standard policy. These aren’t edge cases-they’re predictable outcomes that happen to Minnesota homeowners every year.

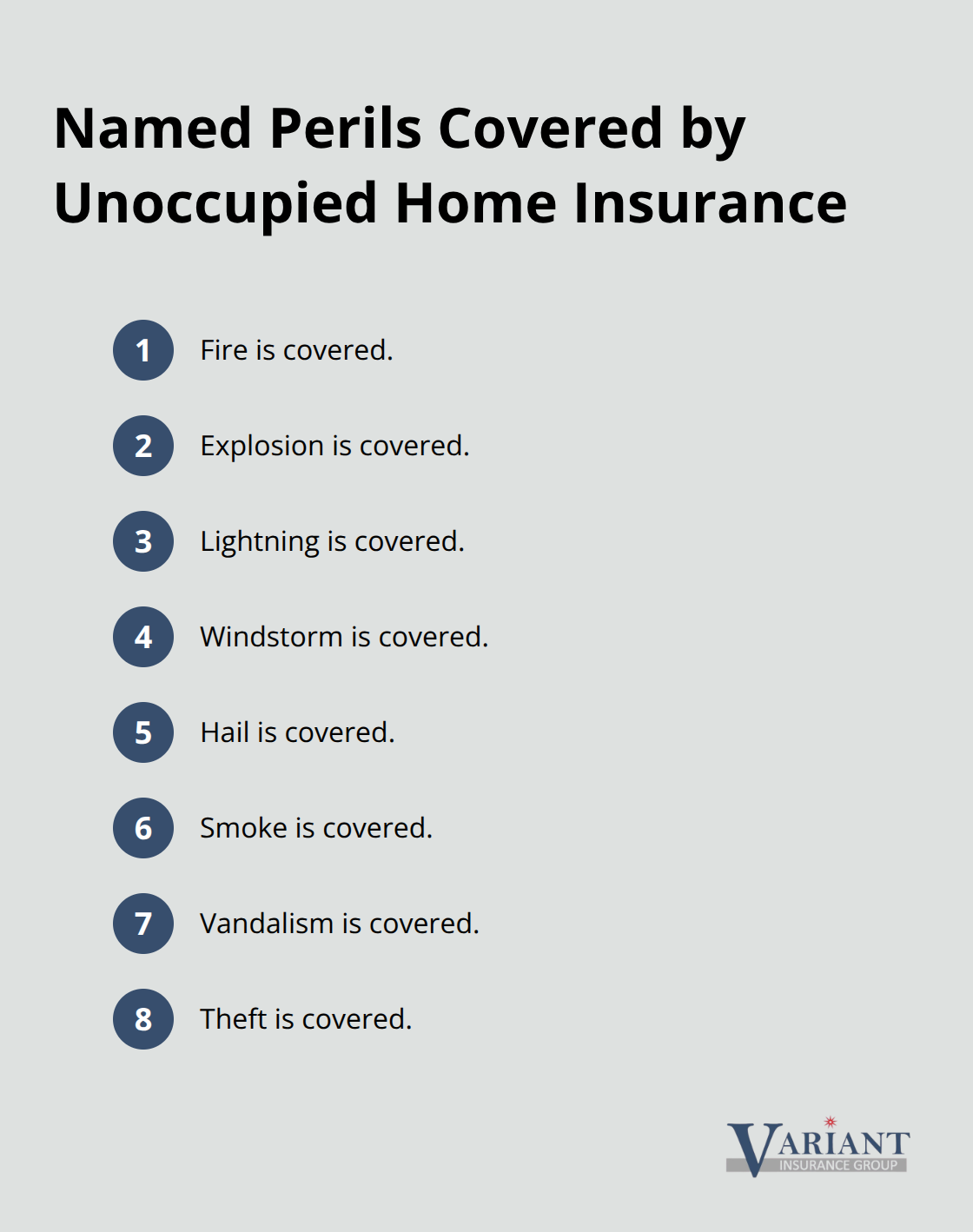

Vacant-home insurance costs roughly 50 to 60 percent more than standard homeowners coverage because the risk profile differs fundamentally. However, that premium buys you actual protection against named perils like fire, explosion, lightning, windstorm, hail, smoke, vandalism, and theft. Some vacant policies also include liability coverage if someone sustains an injury on the property and you face responsibility. The key difference is that vacant-home policies address your specific situation rather than force it into a standard framework that explicitly excludes it.

How Insurers Define Vacancy

Insurers classify homes as vacant based on occupancy status, not on whether utilities remain on or furniture stays inside. A home undergoing renovation, a property between tenants, an estate being settled, or a house waiting to sell all fall into this category. The moment you leave, the clock starts. At 30 days, most insurers will deny claims if they determine the home was vacant at the time of loss. At 60 days under Minnesota law, coverage terminates entirely unless you obtain specific vacancy protection.

You cannot rely on calling your agent after a loss occurs and expect retroactive coverage. The time to act is before you leave the property empty. Notifying your insurer in advance of a planned vacancy allows them to either add a vacancy endorsement to your existing policy or transition you to a dedicated vacant-home policy. This proactive step prevents the coverage denial that would otherwise be automatic and protects your investment while you prepare to winterize and secure the property.

What Unoccupied Home Insurance Actually Covers

Unoccupied home insurance addresses the specific perils that threaten empty properties. Named peril coverage typically includes fire, explosion, lightning, windstorm, hail, smoke, vandalism, and theft. This differs fundamentally from standard homeowners insurance, which either excludes these losses outright for vacant properties or limits them severely.

Vandalism claims represent the most commonly reported loss type for vacant homes, according to industry data on vacancy-related claims. If your Minnesota home will sit empty during renovation, between tenants, or while waiting to sell, you need a policy that treats these perils as insurable events rather than automatic exclusions. Some unoccupied policies also include liability coverage, which protects you if someone sustains an injury on the property and holds you responsible.

Theft and Vandalism Protection

Vacant homes attract criminals because nobody monitors them. Appliances disappear during renovations, copper pipes vanish from walls, and doors get kicked in by squatters. A standard homeowners policy denies these claims if the home was vacant when the loss occurred. Unoccupied home insurance covers theft of fixtures and personal property stored on site, though coverage limits and conditions vary by policy. Vandalism coverage pays for damage from break-ins, graffiti, and deliberate destruction.

The cost difference is real: unoccupied policies run 50 to 60 percent higher than standard coverage because the risk is genuinely elevated. However, you can reduce premiums through security measures. Alarm systems, motion-activated exterior lights, smart doorbell cameras, and window locks lower theft and vandalism risk enough that insurers may offer premium discounts. A neighbor or property manager checking the home weekly also signals active oversight, which some insurers reward with lower rates.

Weather Damage and Frozen Pipes

Winter poses a specific threat to unoccupied homes. Burst pipes from freezing cause more damage in vacant properties because nobody detects the water flow for days or weeks. Unoccupied policies cover fire damage, wind damage, and hail damage to the structure itself. Water damage from frozen pipes is covered if you maintain the heating system properly.

Minnesota Statutes 65A.01 specifies that coverage does not apply where the hazard is increased by means within your control or knowledge. If you shut off the heat entirely during winter, the insurer can deny a frozen pipe claim. Set the thermostat to at least 55 degrees Fahrenheit and drain water lines before extended vacancy to prevent this dispute. Unoccupied policies also cover ice dam damage and wind-driven rain if those perils cause structural damage. The key requirement is that you take reasonable steps to winterize the property (shutting off the main water supply, draining the lines, insulating exposed pipes, and maintaining minimal heating all demonstrate the diligence insurers expect).

Liability and Personal Injury Claims

Liability coverage on an unoccupied policy protects you when someone gets hurt on the property. A trespasser falls through a rotted deck, a neighbor’s child wanders onto the property and sustains an injury, or a contractor hired for repairs has an accident. Without liability coverage, you face medical bills and legal costs personally. Unoccupied policies typically include personal liability protection as standard, though coverage limits vary. Some policies offer $100,000 or $300,000 in liability protection depending on the option you select.

This matters because injury claims can exceed $50,000 quickly once medical treatment and legal fees accumulate. The policy also covers damage you cause to someone else’s property while the home is vacant. If a tree on your property falls and damages a neighbor’s fence, the liability portion covers the repair costs. Most unoccupied policies exclude coverage if the property is left in obviously dangerous condition, so maintaining the structure and securing it against trespassers protects both your liability exposure and your ability to collect on a claim. Understanding what your unoccupied policy covers sets the foundation for the next critical step: preparing your property and finding the right coverage option for your specific situation.

How to Prepare Your Vacant Home and Find the Right Coverage

Winterize Your Property to Prevent Water Damage

Preparing a vacant property requires specific actions before you leave and before you secure insurance. Most unoccupied home policies won’t pay for losses caused by negligence on your part, which means winterization and security aren’t optional extras-they’re conditions of coverage. Start with the heating system. Set your thermostat to at least 55 degrees Fahrenheit during winter months, even though nobody lives there. Shut off the main water supply and drain all water lines completely to eliminate frozen pipe risk. This single step prevents the most expensive and commonly reported damage claim for vacant properties. Insulate any exposed pipes in unheated areas, and leave cabinet doors under sinks open so warm air reaches the pipes. If your property has a sprinkler system, drain it before cold weather arrives.

Secure the Structure Against Weather and Intrusion

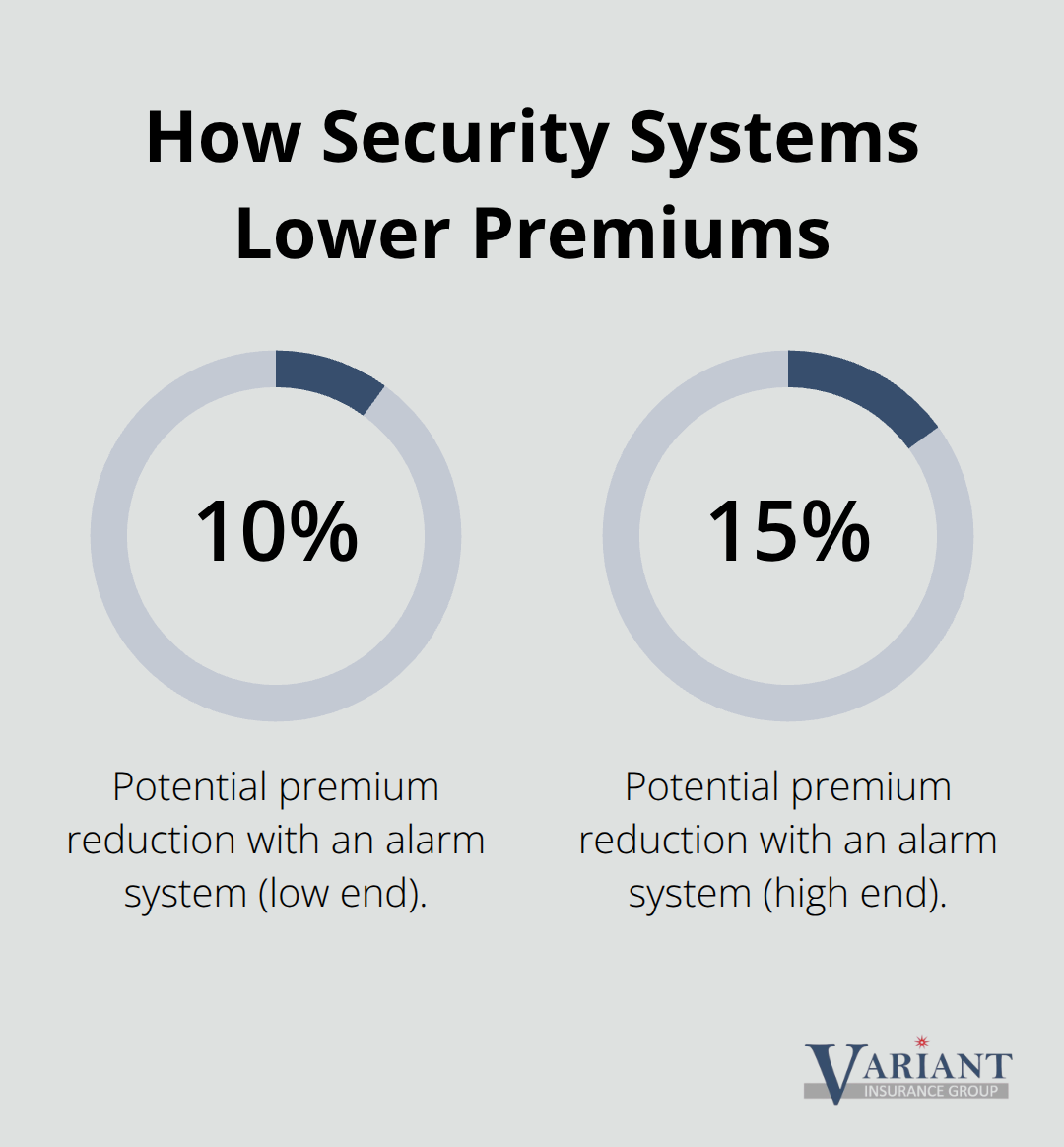

Check the roof for damaged shingles, clean gutters thoroughly, and trim tree branches hanging over the structure. Secure all windows and doors, repair broken locks, and board up any openings that invite entry. These maintenance actions aren’t just smart property management-they directly influence whether an insurer will cover water damage, weather damage, or theft claims when loss occurs. Install motion-activated exterior lights on all sides of the home. These cost between $20 and $60 each and make the property appear occupied while deterring criminals. Add a security system if possible, even a basic one with door and window sensors. Alarm systems can reduce your unoccupied insurance premium by 10 to 15 percent at many carriers because the risk profile improves measurably.

Add Technology and Arrange Regular Oversight

Smart doorbell cameras with video recording capability provide evidence if vandalism or theft occurs and cost around $100 to $200 installed. Arrange for a neighbor, friend, or professional property manager to check the home weekly. This person should look for broken windows, water leaks, fallen branches, and signs of intrusion. Weekly oversight demonstrates active risk management to insurers and often qualifies you for modest premium reductions.

Compare Multiple Carriers and Coverage Options

Finding the right coverage requires comparing multiple carriers and understanding how each defines vacancy, what perils they cover, and which endorsements fit your timeline. Premium costs and coverage limits vary dramatically across carriers. Some insurers offer only 3, 6, or 12-month terms for vacant properties, while others provide flexible periods. Some include personal property coverage for tools stored on site, while others exclude it entirely. Some policies cover all named perils including theft and vandalism, while others cover only fire, wind, and hail. An independent agent can explain these differences and identify which carrier aligns with whether your home will sit vacant for two months during renovation or twelve months while waiting to sell.

Understand Premium Costs and Discount Opportunities

Unoccupied home insurance does run 50 to 60 percent higher than standard homeowners coverage. However, premium costs depend heavily on property condition, security measures, location, and how long vacancy will last. A well-maintained home in a low-crime neighborhood with an alarm system will cost substantially less than a neglected property in a high-crime area without security. Higher deductibles ($2,500 instead of $1,000) can lower premiums significantly if you can absorb that cost in a claim situation. Bundling your vacant home policy with auto insurance at the same carrier often unlocks discounts of 10 to 25 percent. Request quotes from multiple carriers and compare coverage limits, deductibles, and exclusions side by side. An independent agent who works with multiple companies can obtain these quotes efficiently and explain the practical differences in plain terms so you understand what you’re actually buying.

Final Thoughts

Protecting a vacant property requires action before you leave, not after a loss occurs. Standard homeowners insurance explicitly excludes coverage once your home sits empty for 30 to 60 days, leaving you financially exposed during the exact period when risks peak. Homeowners insurance for unoccupied homes fills this gap by covering named perils like fire, theft, vandalism, and weather damage that standard policies deny.

The cost runs 50 to 60 percent higher than regular coverage because vacant properties attract greater risk, but that premium buys genuine protection for your investment. Winterizing your home by setting the thermostat to 55 degrees, draining water lines, and securing all entry points prevents the most expensive claims while satisfying insurer requirements for coverage. Installing motion-activated lights, alarm systems, and doorbell cameras reduces both your actual risk and your insurance premium.

Finding the right coverage means comparing multiple carriers because premium costs, coverage limits, deductibles, and exclusions vary significantly. An independent agent can explain these differences and identify which carrier aligns with your specific situation, whether you’re renovating, managing an estate, or waiting to sell. Contact Variant Insurance Group to discuss your vacant property situation and secure the right coverage before you leave your home empty.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation