If you own rental property in Minnesota, understanding whether homeowners insurance is tax deductible on rental property can save you thousands at tax time. The IRS has clear rules about what counts as a deductible business expense, and homeowners insurance premiums often qualify-but only under specific conditions.

We at Variant Insurance Group help landlords navigate these tax questions every day. Getting this right means the difference between claiming deductions you’re entitled to and missing out on legitimate savings.

Understanding Rental Property vs. Your Primary Home

The IRS draws a sharp line between your primary residence and rental property, and this distinction determines everything about tax deductibility. According to IRS Publication 527, homeowners insurance premiums on your primary residence are not tax deductible under any circumstance. But the moment you rent out that same property-whether it’s a single-family home, condo, or part of your house-the rules change completely. The property transforms into an income-producing asset, and your insurance becomes a legitimate business expense. This shift happens regardless of whether you rent the entire property or just a portion of it. Many Minnesota landlords miss this opportunity because they assume their insurance situation stays the same, when in reality the tax treatment flips entirely once rental income enters the picture.

What Makes a Property Rental in the IRS’s Eyes

The IRS considers a property rental the moment you hold it primarily for producing income through rent payments. This doesn’t require a formal lease agreement or a professional property management company. If you collect rent-whether it’s monthly payments, advance rent, or even amounts paid to cancel a lease-the IRS views it as rental activity. This matters because IRS Publication 527 treats all expenses tied to producing that rental income as potentially deductible business costs. Your homeowners insurance premium becomes part of your rental expenses, reported on Schedule E alongside mortgage interest, property taxes, maintenance, and utilities. The key is that the expense must be ordinary and necessary for operating the rental. For Minnesota landlords, this means you must track every insurance premium payment and maintain documentation that proves the property produced rental income during the tax year. If you rented the property for only part of the year, you can deduct the portion of insurance that applies to the rental period-not the full annual premium.

Documentation That Protects Your Deduction

The IRS doesn’t take your word for rental expenses. You need concrete proof that you paid those premiums and that the property actually produced rental income. Keep your insurance policy declarations, premium payment receipts, and bank statements showing when you paid the insurance company. Lease agreements and rent payment records establish that the property was genuinely held for rental purposes. Many Minnesota landlords lose deductions during audits simply because they lack organized documentation. The IRS expects you to maintain these records for at least three years after filing, though six years is safer. If you use accounting software or work with a tax professional, they can help you organize these expenses and generate a Schedule E that clearly shows your rental insurance among other deductible costs. The effort you put into documentation now prevents complications later and strengthens your position if the IRS ever questions your deductions.

How State-Specific Rules Affect Your Deductions

Minnesota landlords operate within both federal and state tax frameworks, and understanding how these interact matters for your bottom line. While the IRS sets the federal rules for rental property deductions, Minnesota’s tax code generally aligns with federal guidelines for rental expenses. This means your homeowners insurance deduction on a Minnesota rental property follows the same Schedule E reporting structure that applies nationwide. However, Minnesota offers additional tax relief through programs like the Renter’s Credit (available to tenants, not landlords), which shows the state’s focus on rental housing. As a landlord, you benefit from the same federal deduction rules, but you should verify that your state tax return properly reflects all deductible expenses. Working with a local tax professional or insurance agent who understands Minnesota’s rental market can help you identify deductions specific to your situation and avoid costly mistakes when you file.

When Your Rental Insurance Becomes Tax Deductible

How Rental Status Changes Your Insurance Tax Treatment

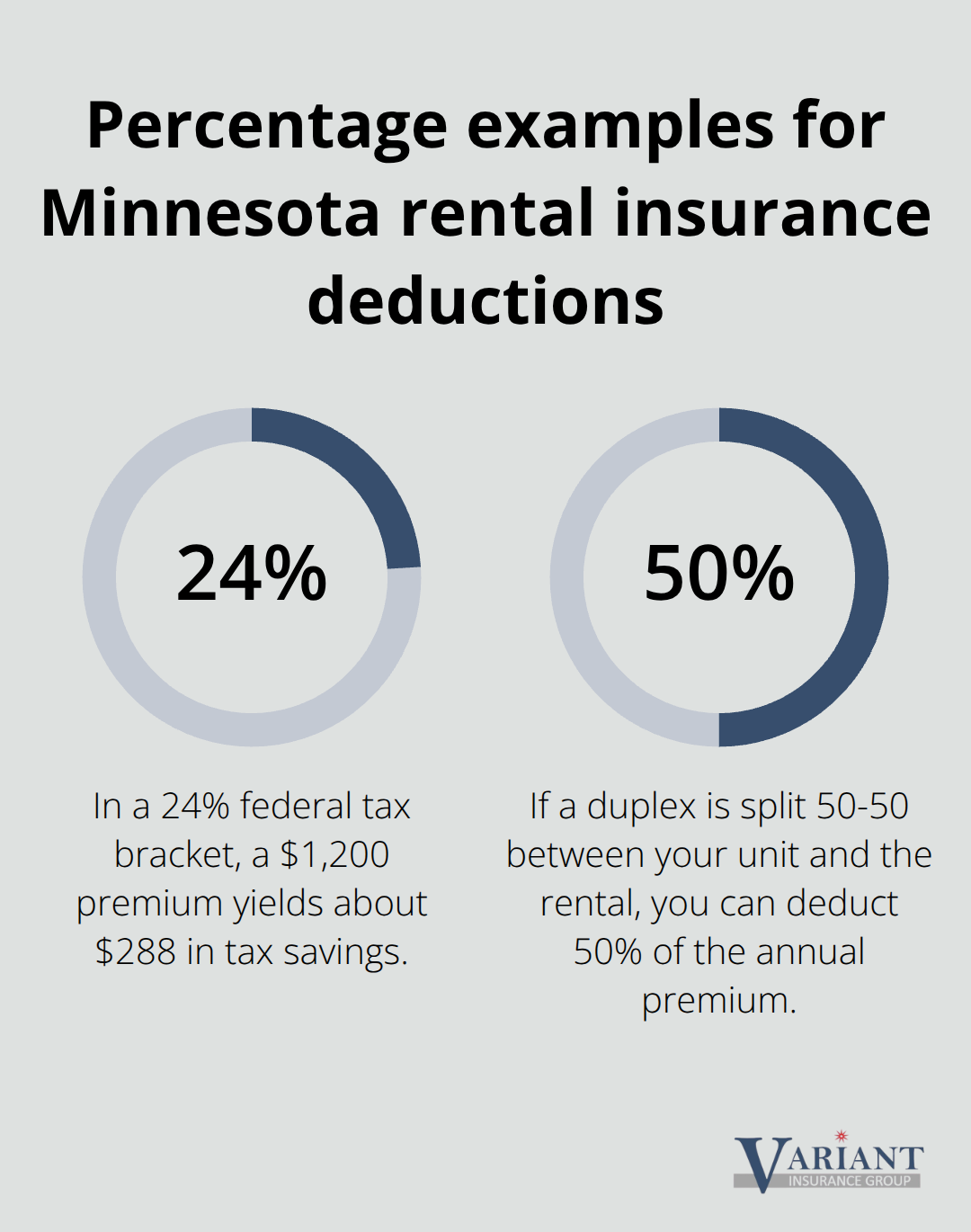

The moment you convert a property to rental status, your homeowners insurance transforms from a personal expense into a business cost. The IRS allows you to deduct the full premium on Schedule E as a rental expense, provided you can prove the property generated rental income during the tax year. This deduction reduces your taxable rental income dollar-for-dollar, which means a $1,200 annual insurance premium directly lowers your taxable income by $1,200. If you’re in the 24% federal tax bracket, that deduction saves you approximately $288 at tax time.

Minnesota landlords often overlook this opportunity because they fail to recognize that insurance status changes when rental income begins.

The critical requirement is that your property must be genuinely held for producing income-not just listed for rent or occasionally occupied by a tenant. If you rented the property for only nine months of the year, you can deduct only the proportional insurance cost for those nine months, not the full annual premium. This partial-year calculation matters when you convert a primary residence to a rental or sell a rental property mid-year.

What Documentation You Must Maintain

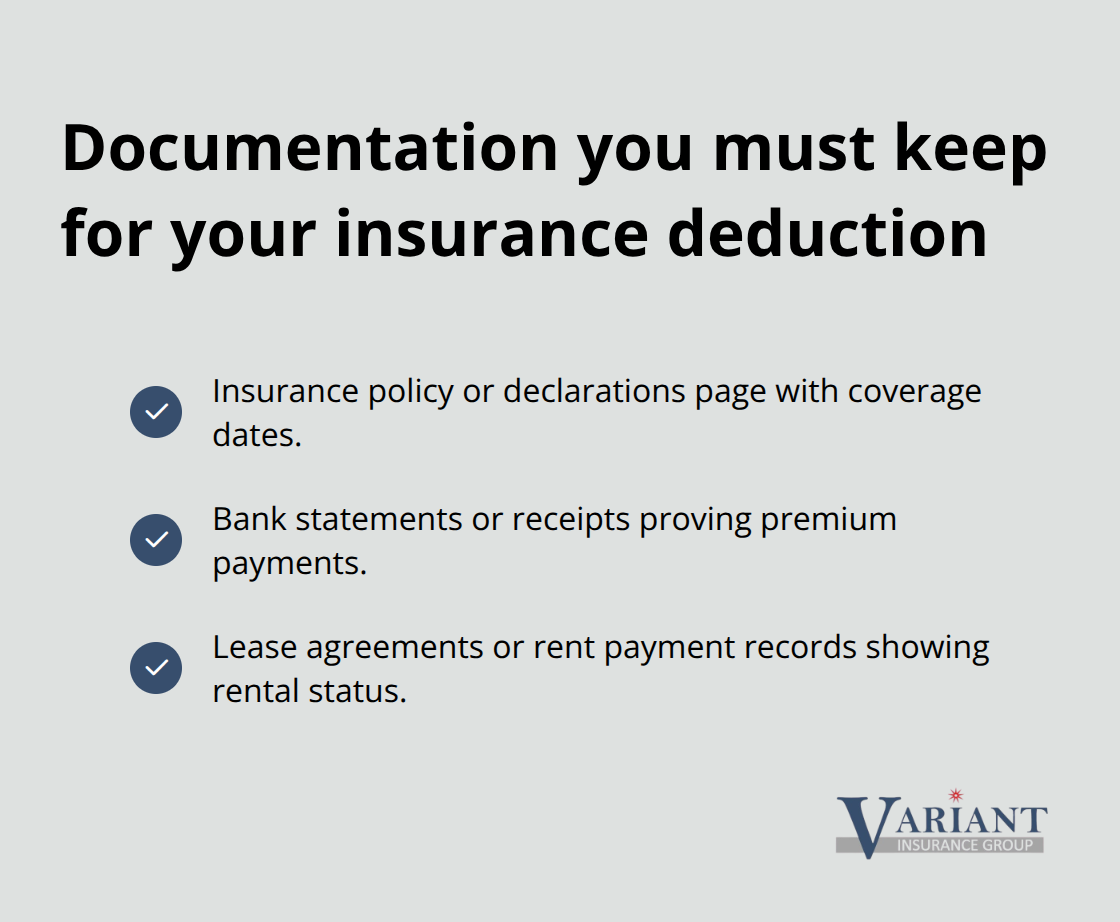

Documentation determines whether the IRS accepts your deduction or rejects it during an audit. You need three specific documents: the insurance policy or declarations page showing coverage dates, bank statements or receipts proving you paid the premiums, and lease agreements or rent payment records establishing the property’s rental status. The IRS expects these records to align perfectly-if your lease shows the tenant moved in March but your insurance deduction begins January, you’ll face questions about whether the property was truly held for rental purposes during those first two months.

Store these documents separately from your general files and maintain them for at least six years after filing. Many Minnesota landlords create a simple spreadsheet tracking each insurance payment by date and amount, which becomes invaluable if you need to defend your deduction. Your insurance agent can provide annual summaries of premiums paid, which simplifies the documentation process and demonstrates your commitment to accurate record-keeping.

How Accounting Tools Strengthen Your Position

When you work with a tax professional or use accounting software designed for rental property owners, these tools automatically categorize insurance expenses and generate the Schedule E documentation the IRS expects. The investment in organization now prevents far costlier complications later. Proper record-keeping also positions you well if questions arise about your deductions, as the IRS views organized documentation as a sign of legitimate business activity rather than casual expense claims.

Understanding these deduction rules sets the foundation for maximizing your rental property’s tax benefits, but the rules shift significantly when your property doesn’t fit the standard rental category. Mixed-use properties and situations where you occupy part of the rental create gray areas that demand careful attention to avoid costly mistakes.

Where Your Homeowners Insurance Loses Tax Deductibility

Your primary residence homeowners insurance will never qualify as a tax deductible expense, regardless of how you structure your finances or what the IRS allows for other properties. The moment you occupy a property as your main home, the IRS classifies insurance premiums as personal expenses, not business costs. This applies even if you work from home, run a side business, or use part of your house for commercial purposes. The IRS distinguishes sharply between properties held primarily for producing rental income and properties where you live, and homeowners insurance on your primary residence falls squarely into the non-deductible personal category.

Why Your Primary Home Insurance Never Qualifies

Minnesota homeowners often attempt creative workarounds, such as claiming home office deductions or business-use percentages, but these strategies do not extend to homeowners insurance itself. You cannot deduct any portion of your primary residence insurance premium on your federal tax return. This rule stands firm because the IRS views homeowners insurance as protection for personal assets, not business assets that generate income. The tax code makes no exceptions for primary residences, even when you operate a business from that home.

The Duplex Trap: Mixed-Use Properties

Mixed-use properties create genuine complications that trap many Minnesota landlords. If you live in one unit of a duplex and rent the other unit, you face a partial deduction situation that demands precise documentation. You can deduct the insurance portion attributable to the rental unit, but not the portion covering your personal living space. The challenge lies in calculating this split accurately and defending it if audited.

Insurance companies typically issue one policy covering the entire building, so you must determine what percentage of the premium applies to the rental portion. If your duplex is split 50-50 between your residence and the rental unit, you can deduct 50 percent of the annual premium. However, the IRS expects you to document how you arrived at this percentage and maintain records proving the property was genuinely operated as a rental. The safest approach involves working with your insurance agent to obtain separate quotes for the rental portion and the owner-occupied portion, then using those figures to support your deduction claim.

Timing Mistakes That Cost Real Money

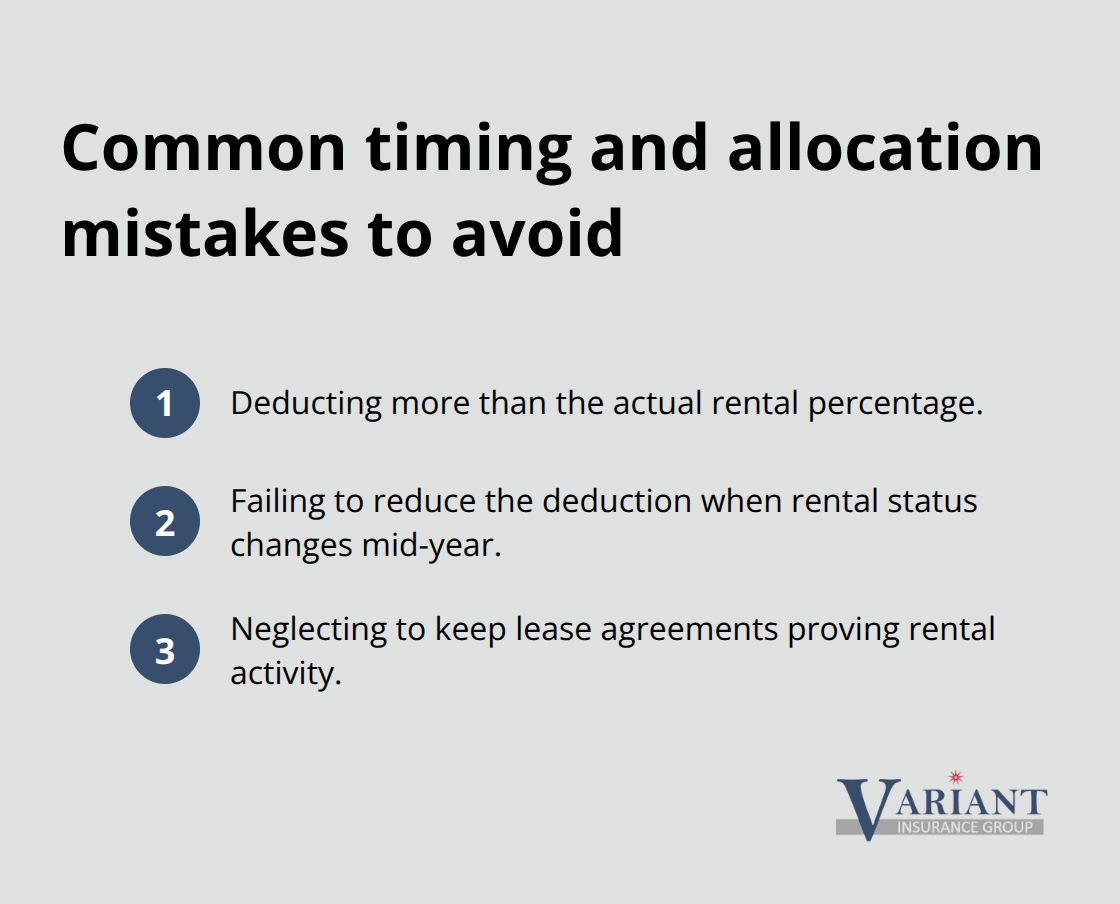

Many landlords guess at calculations and lose their entire deduction during audits when they cannot justify their math. Common mistakes include deducting more than the actual rental percentage, failing to reduce the deduction when the rental status changes mid-year, and neglecting to maintain lease agreements proving the property was held for rental income.

Minnesota landlords also frequently fail to account for timing when they convert a primary residence to a rental property mid-year. If you lived in the house for six months and rented it for six months, you deduct exactly half the annual premium. You can only deduct insurance for the months the property actually generated rental income. Miscalculating these timing issues costs landlords real money at tax time and creates audit risk that extends far beyond the insurance deduction itself. Work with your insurance agent to establish the exact dates your property status changed, then calculate your deduction based on those precise dates rather than estimates.

Final Thoughts

The answer to whether homeowners insurance is tax deductible on rental property is straightforward: yes, but only when your property genuinely produces rental income. The IRS allows you to deduct the full premium on Schedule E as a rental expense, reducing your taxable income dollar-for-dollar. A $1,200 annual insurance premium saves approximately $288 at tax time if you’re in the 24% federal tax bracket, and proper documentation protects your deduction during an audit.

Working with a local insurance agent who understands Minnesota’s rental market transforms tax planning from guesswork into strategy. Your agent helps you establish exact dates when your property status changes, provides documentation supporting your deduction claims, and identifies other rental expenses you might overlook. Contact Variant Insurance Group at variantinsurance.com to discuss how your rental property insurance fits into your overall tax planning strategy.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation