Property owners in Minnesota often confuse landlord insurance with standard homeowners coverage. These policies serve different purposes and offer distinct protections.

We at Variant Insurance Group see this confusion regularly among our clients. Understanding the key differences between landlord insurance vs homeowners insurance helps you choose the right protection for your specific property situation.

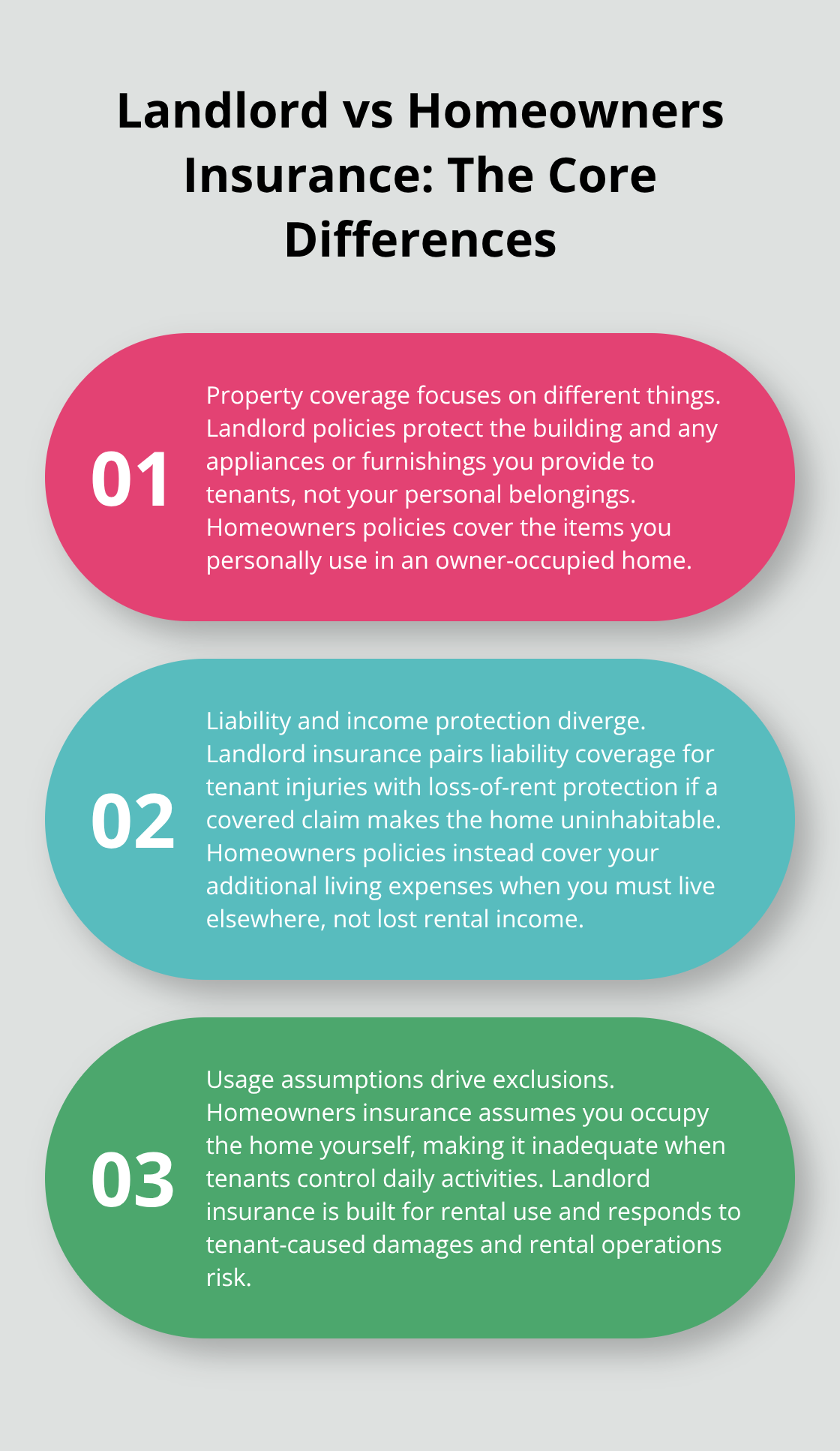

Key Coverage Differences Between Landlord and Homeowners Insurance

Landlord insurance protects the physical structure of your rental property plus any appliances or furnishings you provide for tenants. Homeowners insurance covers your personal belongings like furniture, electronics, and clothing that you actually use. The Insurance Information Institute reports that landlord policies typically cost 15% to 25% more than homeowners insurance because rental properties face higher risks from tenant activities and property vacancy periods.

Property Protection Scope and Limitations

Standard homeowners policies exclude coverage when you rent out your home to tenants. Your tenant breaks the washing machine in a rental unit? Landlord insurance covers it. Your tenant damages the hardwood floors? That falls under landlord coverage too. Homeowners insurance assumes you live in the property and use it personally, which makes it inadequate for rental situations where tenants control daily activities.

Liability Coverage for Tenants vs Personal Use

Landlord insurance includes liability coverage for tenant injuries on your property, plus loss of rental income if the property becomes uninhabitable after covered damage. According to the National Association of Insurance Commissioners, this income replacement typically covers 6 to 12 months of lost rent during repairs. Homeowners insurance provides additional expenses for you to live elsewhere temporarily (hotel costs, restaurant meals), but offers zero protection for lost rental income.

Loss of Rental Income vs Additional Expenses

Minnesota landlords who skip proper coverage face significant financial exposure when tenants get injured or major repairs halt rental income for months. Landlord policies usually include two types of coverage: property and liability protection, both designed to help protect you from financial losses. Homeowners policies focus on your personal displacement costs, while landlord policies protect your investment income stream. This difference becomes critical when you consider how property damage affects your monthly cash flow versus your temporary housing needs.

The cost structure between these policies reflects these different risk profiles, which leads directly to how insurers assess premiums for each property type.

Cost Factors and Premium Considerations

Insurance companies charge higher premiums for landlord policies because rental properties present measurably higher risks than owner-occupied homes. Property damage claims affect rental properties at elevated rates, primarily from tenant-related incidents, delayed maintenance reports, and higher vacancy exposure. Minnesota rental properties face additional winter risks when tenants fail to maintain proper heat or report frozen pipe issues promptly.

Risk Assessment Differences for Rental Properties

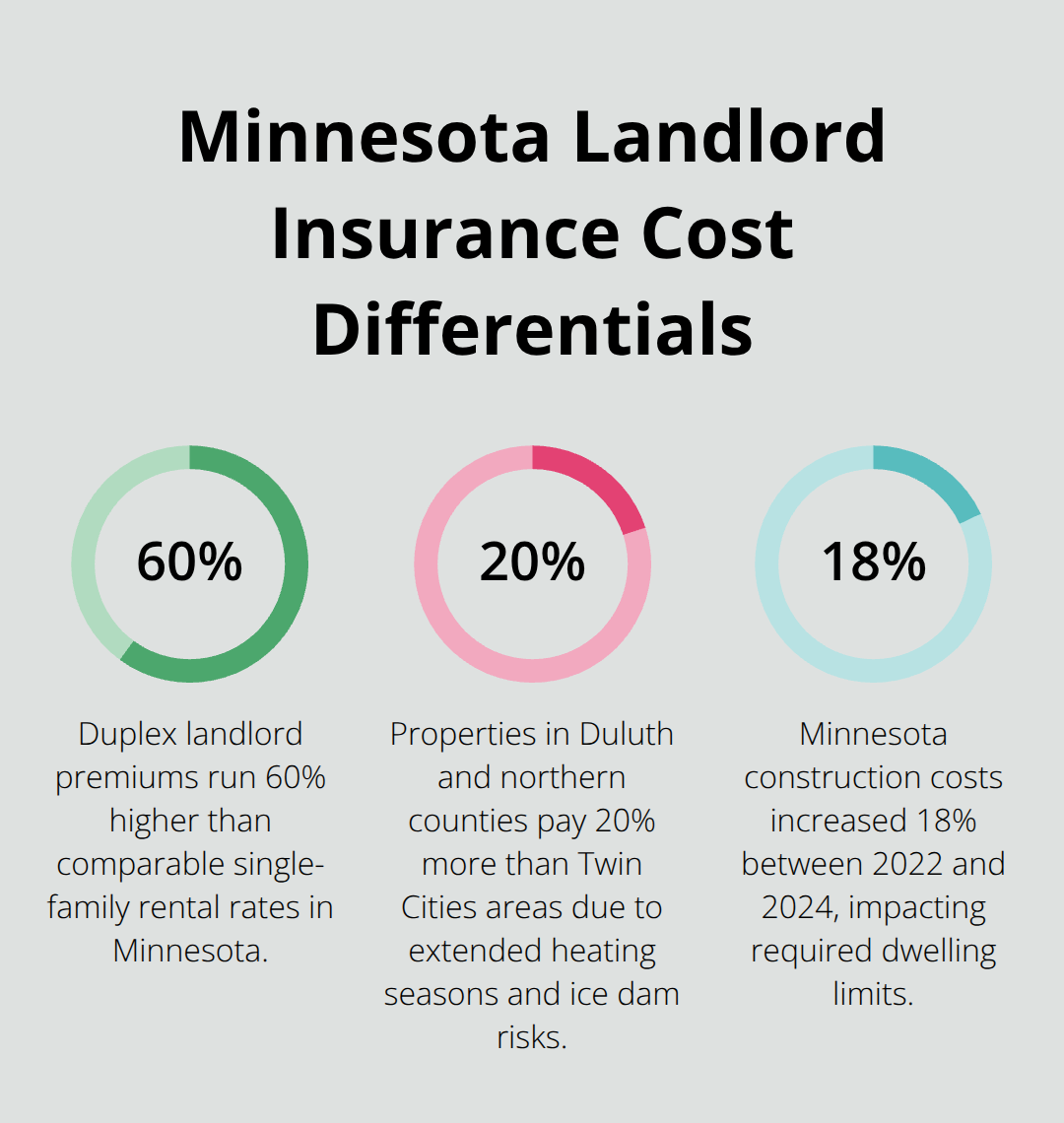

Insurers calculate landlord insurance premiums with different risk models than homeowners policies. Single-family rental homes in Minnesota typically cost $1,200 to $2,400 annually for landlord coverage compared to $800 to $1,600 for similar homeowners policies. Multi-unit properties see even steeper increases, with duplex coverage that runs 60% higher than single-family rates. Property age significantly impacts prices – homes built before 1970 face surcharges of 15% to 25% due to outdated electrical, plumbing, and heating systems that create higher claim frequencies.

Location and Property Type Impact on Pricing

Minnesota’s harsh winters create regional price variations within landlord insurance markets. Properties in Duluth and northern counties pay 20% more than Twin Cities metropolitan areas due to extended heating seasons and ice dam risks (particularly severe in areas with heavy snowfall). Coverage limits for dwelling protection should match current replacement costs, not purchase prices, as Minnesota construction costs increased 18% between 2022 and 2024 according to state building industry reports.

Deductible Options and Coverage Limits

Deductible selections dramatically affect annual premiums – property owners who choose a $2,500 deductible instead of $1,000 typically reduce costs by 25% to 30%. Higher deductibles work well for landlords who maintain emergency funds for property repairs. Lower deductibles benefit owners who prefer predictable out-of-pocket expenses when claims occur. These cost variations make it essential to understand what factors insurance companies evaluate when they determine your specific premium rates, which creates potential gaps that landlords must understand.

Common Exclusions and Coverage Gaps

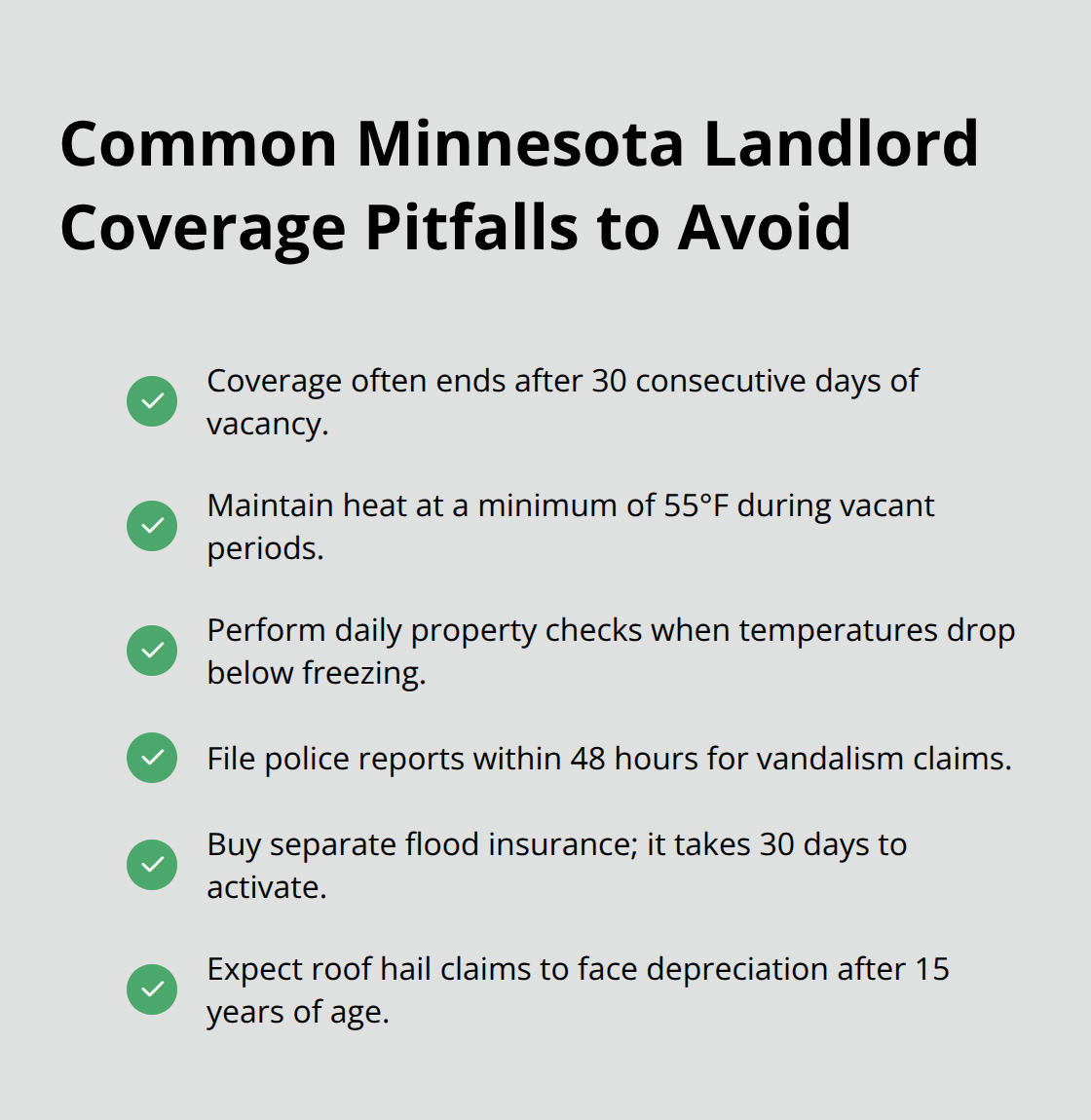

Landlord insurance policies contain specific exclusions that catch Minnesota property owners off guard when they file claims. Insurance companies deny tenant-caused damage beyond normal wear and tear if they determine the damage was intentional or resulted from lease violations that property owners failed to address. Properties that remain vacant for more than 30 consecutive days lose coverage automatically under most policies – a significant issue for Minnesota landlords during winter months when tenant turnover peaks between November and February.

Tenant-Caused Damage and Vandalism

Insurance companies reject claims when landlords fail to conduct regular property inspections or ignore tenant-reported maintenance issues. Minnesota landlords who skip quarterly inspections face claim denials for water damage, mold growth, and structural problems that develop over time. Vandalism coverage requires police reports within 48 hours of discovery, but many landlords wait weeks before they visit rental properties. Properties with security deposits below $1,500 signal higher risk to insurers and may face coverage restrictions for intentional tenant damage.

Vacancy Periods and Unoccupied Property Rules

Most policies require heat maintenance at 55 degrees minimum during vacant periods, with daily property checks when temperatures drop below freezing. Minnesota’s freeze-thaw cycles between March and April create pipe burst risks that insurers scrutinize heavily – properties without winterization procedures face automatic claim denials. Weather-related damage from ice dams, frozen pipes, and roof collapses from snow loads face strict maintenance requirements that many landlords overlook.

Natural Disaster and Weather-Related Limitations

Flood damage from spring snowmelt requires separate flood insurance policies that take 30 days to activate (making advance planning essential for properties near rivers or lakes). Standard landlord policies exclude earthquake damage, even though Minnesota experiences minor seismic activity that can affect older rental properties. Wind damage from severe thunderstorms gets covered, but hail damage to roofs faces depreciation schedules that reduce payouts significantly for properties over 15 years old.

Final Thoughts

The landlord insurance vs homeowners insurance decision affects your financial protection and property investment success in Minnesota. Landlord policies cost 15% to 25% more but provide rental income protection, tenant liability coverage, and property damage protection specifically designed for rental situations. Homeowners insurance excludes rental activities and leaves you exposed to significant financial losses when tenants cause damage or injuries occur on your property.

Minnesota property owners who choose incorrect coverage face claim denials, lost rental income during repairs, and personal liability for tenant injuries. Properties that remain vacant for 30 days lose coverage automatically, while tenant-caused damage beyond normal wear gets excluded from homeowners policies entirely. These coverage gaps create substantial financial risks that many landlords discover only after they file claims.

We at Variant Insurance Group help Minnesota property owners compare coverage options from multiple insurance companies to find policies that match their specific rental property needs. Our team reviews protection levels and rates to identify appropriate coverage for your investment properties (whether single-family homes or multi-unit buildings). Contact Variant Insurance Group today to review your current coverage and protect your rental property investments with appropriate insurance solutions.