Your homeowner’s or business liability insurance has limits. Once you exceed those limits in a lawsuit, you’re personally responsible for the rest.

That’s where liability umbrella protection comes in. At Variant Insurance Group, we see Minnesota residents and business owners face unexpected liability claims every year-from dog bites to pool accidents to vehicle incidents. A single serious claim can wipe out years of savings.

This guide walks you through how much coverage actually makes sense for your situation.

How Umbrella Coverage Works and Why You Need It

What Umbrella Protection Actually Does

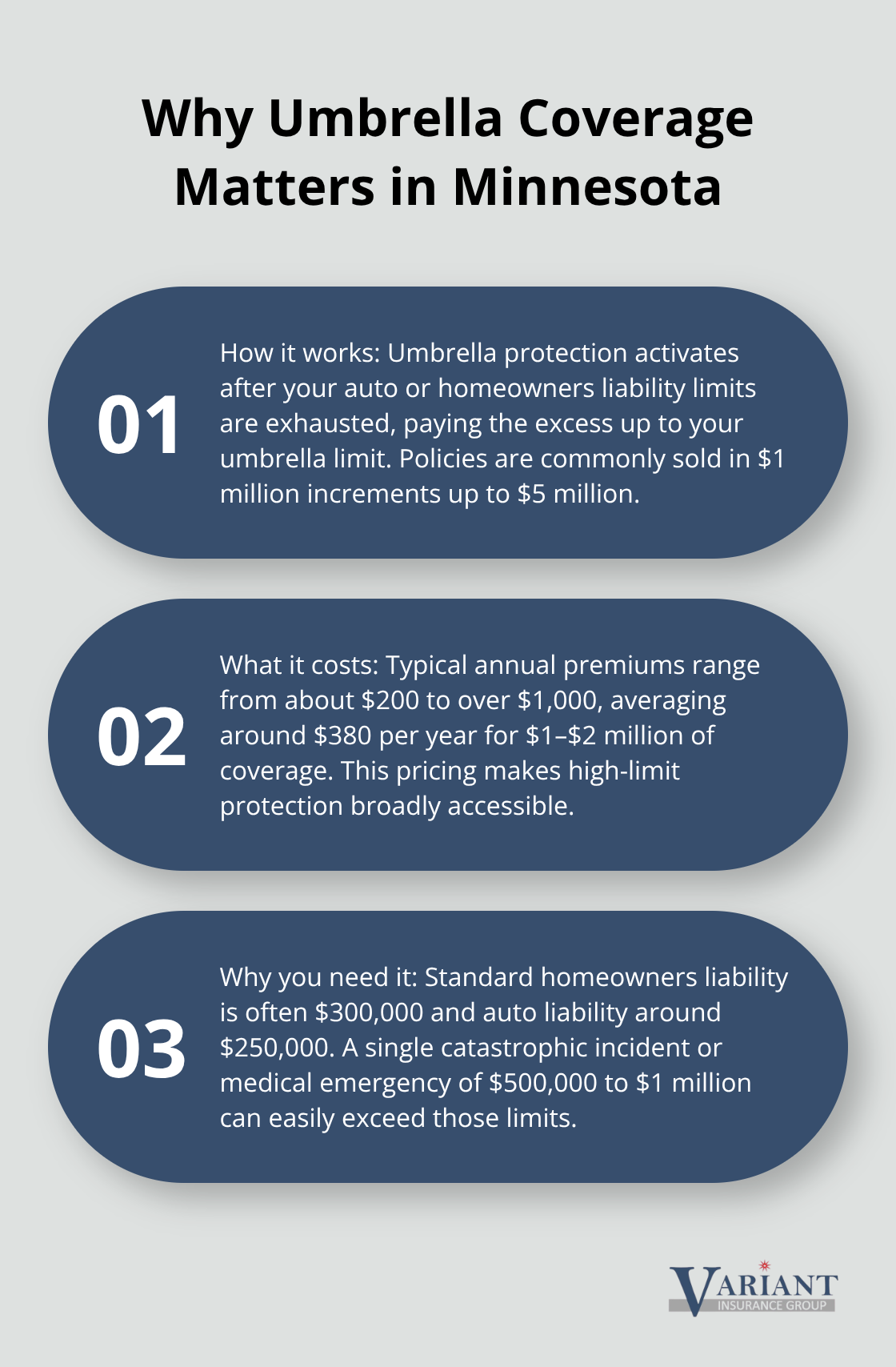

Liability umbrella protection operates on a simple principle: it activates after your auto or homeowners liability limits are exhausted, covering the excess amount up to your umbrella limit. When you face a lawsuit and the judgment exceeds what your underlying auto or home policy covers, your umbrella steps in to pay the difference. Kiplinger reports that umbrella policies are sold in $1 million increments up to $5 million, with typical annual costs ranging from about $200 to over $1,000, averaging around $380 per year for $1–$2 million of coverage.

This affordability matters because most Minnesota homeowners and business owners severely underestimate their exposure. Your standard homeowners policy typically covers $300,000 in liability; your auto policy covers around $250,000. A single catastrophic incident-a guest injured on your property, a serious car accident you cause, or a defamation lawsuit-can easily exceed these limits. One medical emergency can cost $500,000 to $1 million in hospital bills alone, before legal fees and pain-and-suffering damages accumulate.

What Umbrella Covers

Kiplinger notes that umbrella covers bodily injury, property damage, and defense costs; many policies also cover defamation claims like slander or libel. If you own rental property, umbrella provides additional coverage beyond your landlord policy. Umbrella insurance coverage helps protect you from the costs of covered claims when those costs exceed the limits of your home, auto or boat insurance policies, protecting you across state and international borders.

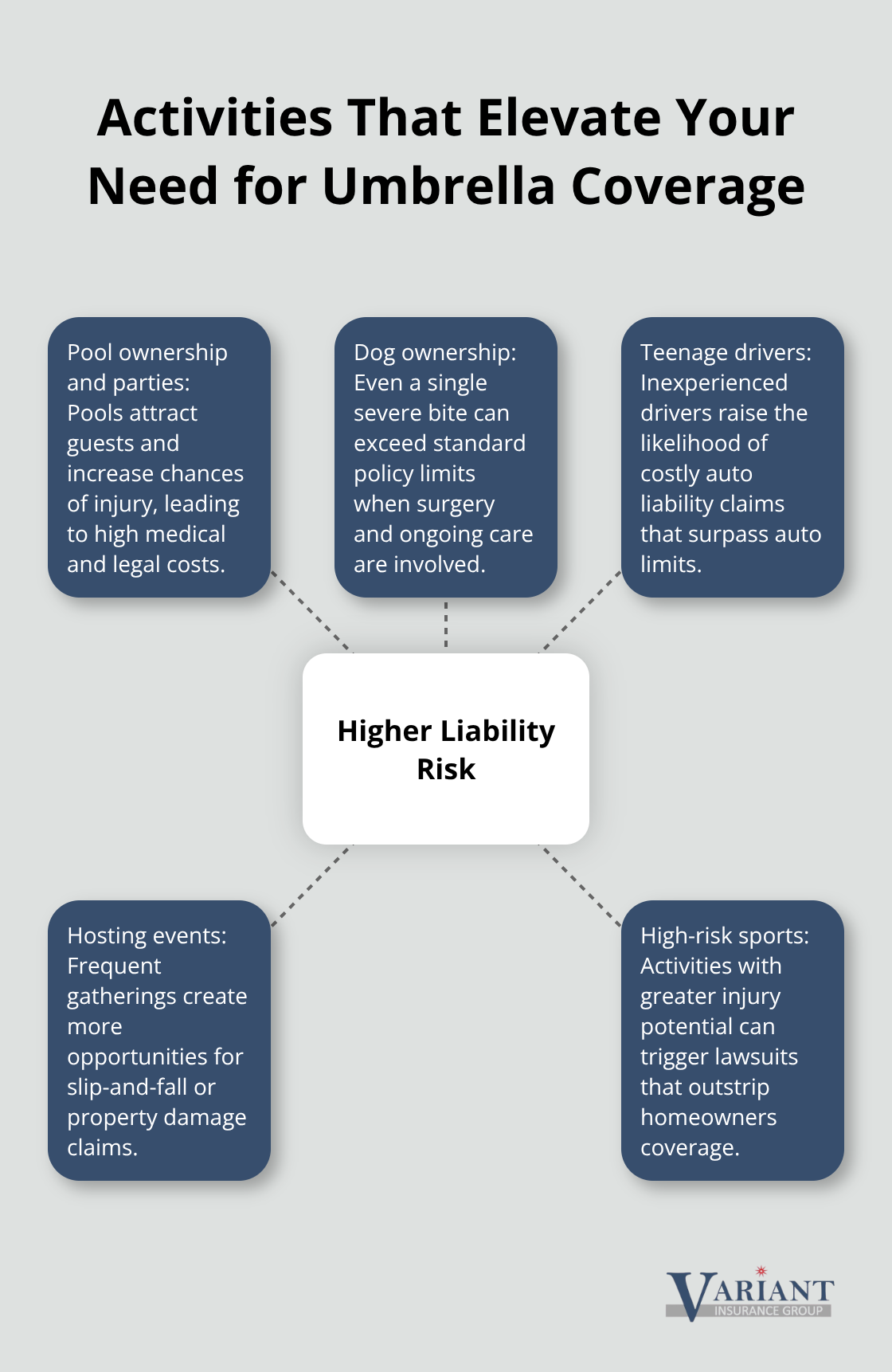

Standard homeowners and auto policies are designed to protect against ordinary risks. Umbrella protection addresses catastrophic liability that exceeds ordinary coverage limits. Minnesota homeowners with pools, multiple drivers, or frequent gatherings face elevated risk. According to the Insurance Information Institute, certain activities significantly raise your need for umbrella: pool ownership and parties, dog ownership, teenage drivers, hosting events, and high-risk sports.

Identifying Your Risk Level

If you have two or more of these risk factors, you almost certainly need umbrella coverage. To qualify, you must maintain minimum underlying liability: Kiplinger confirms you typically need auto liability of at least $250,000 and homeowners liability of at least $300,000. Many Minnesota residents bundle umbrella with their existing home and auto policies to receive discounts of 10–15% off umbrella premiums, plus additional savings on bundled policies.

Using the same insurer for all liability coverages helps prevent coverage gaps and consolidates defense costs under one set of attorneys. This matters because gaps between policies can leave you personally exposed. The next step involves calculating your actual net worth and determining what coverage amount truly protects your assets.

How Much Umbrella Coverage Matches Your Actual Assets

Calculate Your Net Worth First

The most common mistake Minnesota homeowners make is guessing at umbrella coverage instead of calculating it. Your umbrella limit should reflect what you actually own and what you could lose in a lawsuit. Start by adding up your liquid assets: savings accounts, investment accounts, and retirement funds accessible without penalty. Then add home equity (your home’s current market value minus your mortgage balance), vehicle values, and any other significant property. This total is your net worth, and it’s the baseline for determining umbrella coverage.

Progressive recommends this net-worth-based approach because it directly ties your coverage to what creditors could pursue if you lose a major lawsuit. The math is straightforward: without sufficient umbrella limits, a single judgment can force you to liquidate investments, sell property, or face wage garnishment for years.

Understand Which Assets Count

Some assets deserve special treatment in this calculation. ERISA-protected retirement accounts like your 401(k) and pension are generally shielded from civil lawsuits under federal law, so you can exclude these from your umbrella calculation. Individual Retirement Accounts offer varying protection depending on Minnesota state law, so most advisors recommend including IRA balances to be safe.

Home equity protection depends on whether you’ve filed a Homestead Declaration in Minnesota; if your home equity falls below Minnesota’s homestead exemption threshold, that portion may already have legal protection and requires less umbrella coverage.

Match Coverage to Your Net Worth

Kiplinger’s research shows that typical umbrella policies start at $1 million in $1 million increments, costing roughly $150 to $300 per year for $1 million of coverage. For a Minnesota homeowner with $800,000 in net worth, a $1 million umbrella policy costs less than $300 annually and closes the gap entirely. For someone with $2.5 million in assets, a $2.5 million umbrella policy still costs only about $400 to $500 per year when bundled with auto and homeowners coverage.

The key actionable step: calculate your exact net worth this month, then select an umbrella limit that matches or exceeds that number. If your net worth grows significantly (through home appreciation, inheritance, or investment gains), increase your umbrella limit accordingly. Once you understand your coverage needs, the next step involves identifying which specific liability scenarios pose the greatest risk to your Minnesota household.

Common Liability Scenarios and Coverage Gaps

Dog Bites and Pet-Related Incidents

Minnesota homeowners face real liability exposure in specific situations where standard policies fall short, and umbrella coverage becomes the financial buffer between manageable costs and catastrophic loss. Dog bites represent one of the most common triggers for umbrella claims because homeowners policies typically limit dog liability to $100,000 to $300,000, yet a severe bite requiring reconstructive surgery, infection treatment, and ongoing care easily reaches $500,000 or more. Dog ownership elevates your need for umbrella protection, and Minnesota’s comparative negligence laws mean you could face liability even if your dog’s behavior seemed minor beforehand.

A single incident-your dog injures a neighbor’s child during an unsupervised moment-can generate medical bills exceeding $1 million when you factor in surgical costs, physical therapy, psychological counseling, and the family’s pain-and-suffering damages. If your homeowners policy maxes out at $300,000, you personally owe the remaining $700,000 or more unless umbrella coverage steps in.

Swimming Pools and Property Accidents

Swimming pools and property-related accidents create similar exposure gaps because they attract liability claims from both family gatherings and unexpected incidents. A guest slips on your deck, fractures their spine, and faces $800,000 in medical costs plus lost wages-your homeowners policy covers the first $300,000, leaving you responsible for $500,000. Property damage claims follow the same pattern: a small fire spreads to your neighbor’s garage, destroying their vehicle and outdoor structures, totaling $600,000 in damages that exceed your policy limits.

Vehicle-Related Liability Claims

Vehicle-related liability claims often exceed standard auto limits when serious injuries occur; a crash you cause injures three people with combined medical bills and settlements reaching $1.5 million against your $250,000 auto liability limit. Kiplinger research confirms that umbrella coverage applies to liability claims occurring while you travel outside Minnesota, meaning a car accident during a family road trip to Wisconsin or a slip-and-fall incident at a vacation rental triggers the same protection.

Why Standard Policies Fall Short

The practical reality for Minnesota residents is that one significant claim in any of these scenarios-pet incidents, property accidents, or vehicle collisions-can consume your entire net worth without umbrella protection. Your standard policies were designed for typical claims, not catastrophic ones, which is precisely why umbrella coverage exists as affordable catastrophe insurance costing $150 to $300 annually for $1 million in protection.

Final Thoughts

Your net worth determines the umbrella coverage amount you need. If you calculated your total assets while reading this guide, you already know what that number is-your liability umbrella protection limit should match or exceed it. A Minnesota homeowner with $1.2 million in assets needs at least $1.2 million in umbrella coverage, while someone with $2.8 million in net worth should carry $3 million in umbrella limits.

Most Minnesota residents pay between $150 and $300 annually for $1 million in coverage, and bundling with your existing auto and homeowners policies typically reduces that cost further through multi-policy discounts. When you consider that a single serious liability claim can exceed $1 million in damages, the annual premium represents genuine financial security at a fraction of what you’d lose without it. This affordable protection closes the gap between what your standard policies cover and what you actually stand to lose.

Contact an insurance professional to review your current auto and homeowners coverage and confirm you meet the minimum underlying liability requirements (typically $250,000 for auto and $300,000 for homeowners). If your current insurer doesn’t offer umbrella coverage, an independent agent can locate options from multiple carriers. We at Variant Insurance Group work with Minnesota families and business owners to build comprehensive protection plans that fit their actual needs and budgets-contact us for a personalized review of your liability exposure and a quote that reflects your specific situation.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation