A waiver of subrogation is a clause that stops your insurance company from going after a third party to recover money after paying your claim. This protection matters more than you might think, especially if you rent property, work with contractors, or have business partners.

At Variant Insurance Group, we see Minnesota property owners overlook this detail regularly-and it costs them. Understanding when you need this waiver can save your business relationships and protect your wallet.

What Subrogation Really Means for Your Property

How Subrogation Works in Property Insurance

Subrogation is the legal right your insurance company gains to pursue a third party for money after paying your claim. When your insurer pays you for property damage, they step into your shoes and can sue whoever caused the loss to recover what they spent. A waiver of subrogation stops this process entirely. Once you sign a waiver, your insurer cannot go after the responsible party, even if that party’s negligence caused the damage.

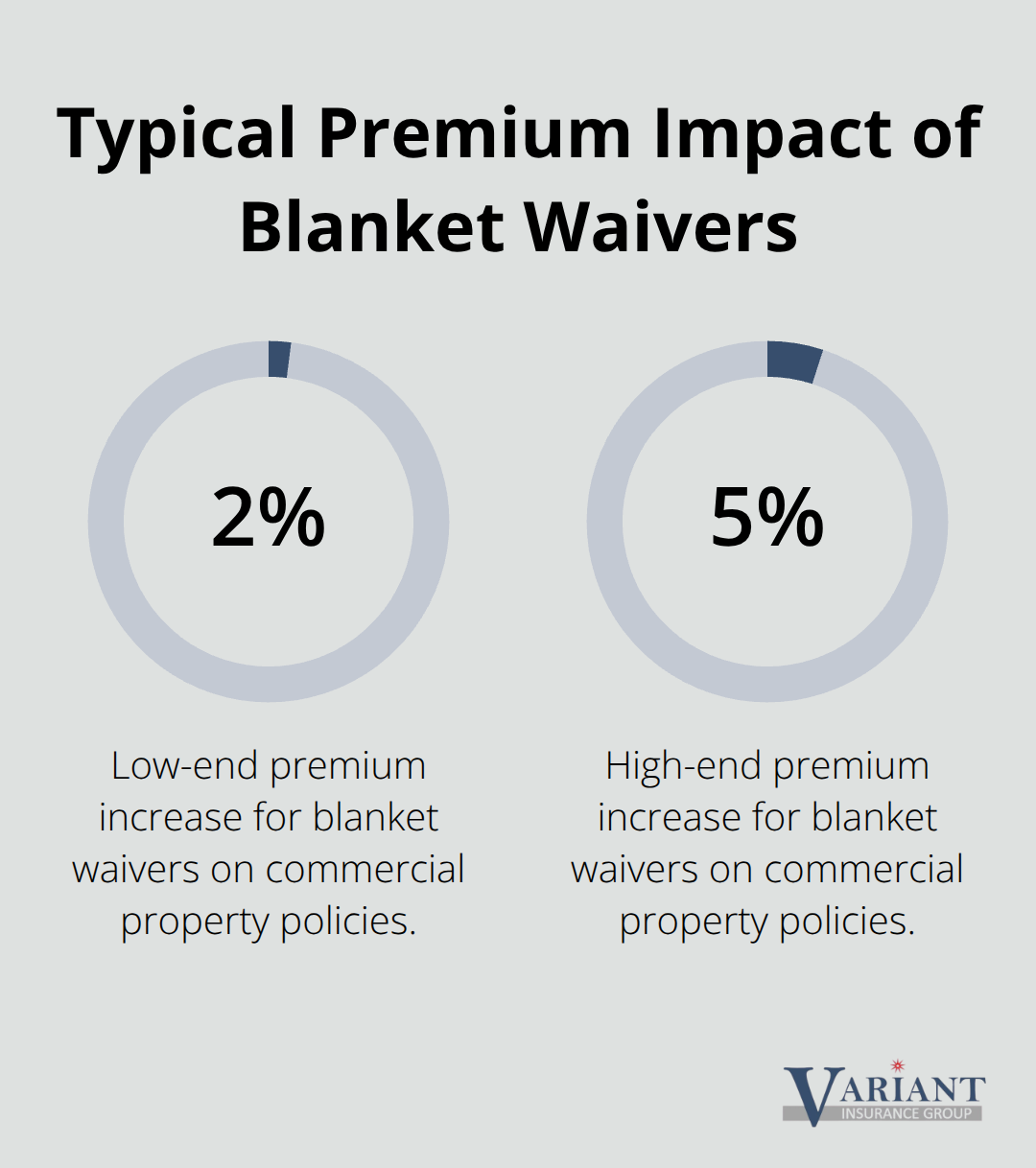

This matters because it shifts financial risk. Without a waiver, the insurer absorbs the loss and pursues recovery. With a waiver, the insurer absorbs the loss and has no path to recover it. The cost difference is real: adding a waiver of subrogation endorsement typically runs $75 to $200 per endorsement for commercial property coverage, or a 2 to 5 percent premium increase for blanket waivers that cover multiple contracts.

Why Property Owners Face Pressure to Sign Waivers

Minnesota property owners often face pressure to sign waivers without understanding what they’re giving up. A landlord might require a tenant to waive subrogation. A contractor might demand one before starting work. A business partner might make it a condition of the relationship. The problem is that once you agree, your insurer cannot recover from the responsible party if something goes wrong.

The real danger emerges when you sign a waiver without telling your insurer first. Signing a contract with waiver language but failing to notify your insurance company can breach policy conditions and lead to claim denial or reduction. You must contact your broker or insurer with the contract before signing anything. Most endorsements process within 24 to 48 hours, so delay is not an excuse.

Mutual Waivers Versus One-Sided Agreements

Mutual waivers, where both parties give up the right to sue each other, offer better protection than unilateral waivers where only you waive your rights. Tenants should push back against one-sided waivers that prevent them from suing landlords while landlords retain the right to sue tenants. In construction projects, mutual waivers among the owner, contractor, and subcontractors prevent costly cross-litigation and speed claims handling.

What You Must Do Before Signing

The key actionable step is this: before signing any contract that mentions waiving subrogation, forward it to your insurance broker with a request to add the waiver endorsement. Verify that your policy permits the waiver type and confirm the exact conditions. Do not assume your current policy allows waivers, and do not assume the cost will be negligible. Waivers affect your coverage rights permanently, so treating them as routine paperwork is a mistake Minnesota property owners make repeatedly.

Your broker can clarify whether the waiver aligns with your specific coverage and identify any gaps that could leave you exposed. This step takes minimal time but prevents costly surprises later. Once you understand the financial impact and coverage implications, you can make an informed decision about whether to accept the waiver or negotiate different terms with the other party.

Where Waivers Show Up in Real Minnesota Contracts

Landlord-Tenant Waivers in Minnesota Leases

Landlords in Minnesota routinely demand that tenants sign waivers of subrogation as part of lease agreements, and most tenants accept without pushback. The reason is straightforward: landlords want to protect themselves from their own insurance company pursuing recovery from the tenant if property damage occurs. When a tenant’s negligence damages the building, the landlord’s insurer pays the claim but cannot recover from the tenant if a waiver is in place.

Tenants should recognize this as a one-sided arrangement and push for mutual waivers instead, where both parties waive rights against each other for insured losses. A mutual waiver protects the tenant from the landlord’s insurer coming after them while preventing the tenant’s insurer from pursuing the landlord. This balanced approach is fairer and increasingly common in longer-term leases. If a landlord insists on a unilateral waiver, the tenant absorbs all the risk while the landlord loses nothing.

Construction Contracts and Multiple-Party Waivers

Construction contracts in Minnesota create the most complex waiver situations because multiple parties are involved. The property owner, general contractor, subcontractors, and their respective insurers all have competing interests. Mutual waivers in construction contracts among all parties prevent expensive cross-litigation if something goes wrong on the job site.

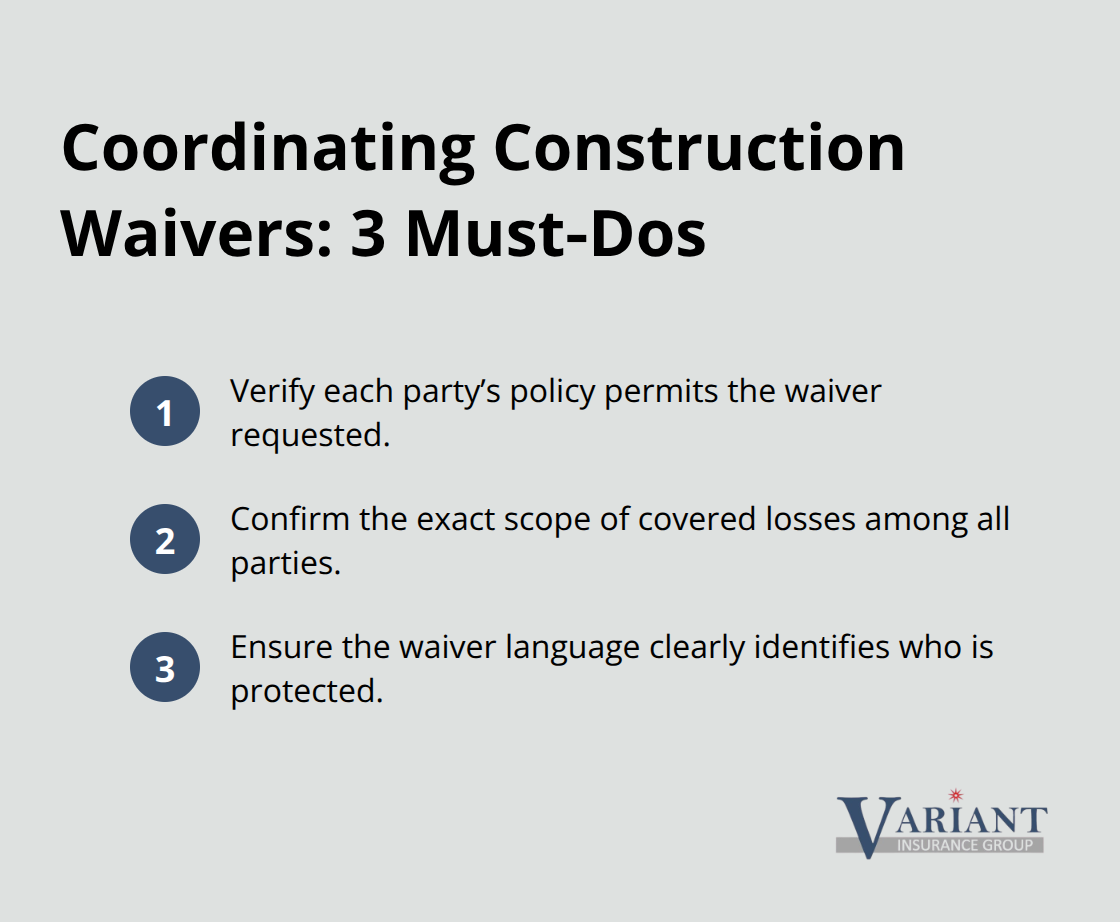

For example, if a subcontractor’s negligence damages the building and the general contractor’s insurer pays for repairs, that insurer cannot pursue the subcontractor for recovery when a mutual waiver exists. This arrangement protects relationships and speeds claims settlement, which is why mutual waivers have become standard in Minnesota construction contracts. You must coordinate waivers carefully: verify that each party’s policy permits the waiver, confirm the exact scope of covered losses, and ensure the waiver language clearly identifies who is protected.

Vendor Relationships and Commercial Partnerships

Commercial partnerships and vendor relationships often require waivers when one party wants protection from the other’s potential negligence. A vendor supplying materials or services might demand a waiver so your insurer cannot sue them if their product causes damage. Before you accept, confirm whether the waiver is mutual or one-sided and whether your policy allows it.

Contact your broker with the contract language before you commit to any waiver arrangement, regardless of the business relationship involved. This step protects you from hidden costs and coverage gaps that could surface months or years later when a loss occurs.

What Waivers Actually Cost Your Bottom Line

The Direct Premium Impact

Adding a waiver of subrogation endorsement to your commercial property policy involves additional endorsements like the CG 24 04 in Minnesota. That upfront expense seems manageable until you factor in what happens when a loss occurs. Your insurer cannot recover from the negligent party because you signed a waiver, which means your deductible stays with you instead of being recovered through subrogation. Excluded coverage gaps remain uninsured losses you absorb personally. Incidental costs like emergency repairs, temporary facilities, or business interruption losses fall entirely on your shoulders when the responsible party cannot be pursued.

For property damage worth $50,000, a waiver might cost you $150 upfront, but if that loss occurs, you could lose $10,000 or more in unrecovered costs depending on your deductible and coverage structure. The visible premium increase masks the real financial exposure that emerges only after a claim.

Policy Restrictions Create Hidden Traps

The bigger trap is negotiating waivers without understanding what your policy actually permits. Some insurers restrict certain waiver types or prohibit blanket waivers altogether, meaning you could sign a contract agreeing to a waiver your policy does not allow. This creates a coverage gap where you promised a waiver you cannot legally deliver. Your broker must review the contract language before you commit because policy restrictions vary significantly between carriers.

Contact your broker with the exact contract language before signing anything. This conversation takes 15 minutes and prevents thousands in unrecovered losses later. Your broker can clarify whether the waiver aligns with your coverage and identify any gaps that could leave you exposed.

Mutual Waivers Offer Better Financial Protection

Mutual waivers offer better financial protection than one-sided arrangements, yet many Minnesota property owners accept unilateral waivers without questioning fairness. Try for mutual terms whenever possible, especially in longer-term leases or construction projects where the relationship matters. If a landlord or contractor demands a one-sided waiver, that signals they want maximum protection while shifting all risk to you.

Negotiate limited-scope waivers instead, restricting the waiver to specific activities or loss types rather than accepting blanket language. A limited waiver protects your business relationship while preserving your right to recover losses in other scenarios. This balanced approach reduces your financial exposure without destroying the partnership.

What You Must Verify Before Committing

Ask your broker directly whether the waiver aligns with your coverage and what financial exposure you face if a loss occurs. Request that your broker identify which losses the waiver covers and which losses remain your responsibility. Confirm whether your policy permits the specific waiver type the other party demands (mutual, unilateral, or blanket). Verify the exact scope of covered losses and ensure the waiver language clearly identifies who is protected and under what circumstances.

Your broker can also explain how the waiver affects your ability to recover costs beyond the policy limits. Some waivers extend only to damages covered by insurance, while others may extend to all bodily injury and property damage regardless of insurance. Understanding this distinction prevents costly surprises when a loss exceeds your coverage limits and you cannot pursue the responsible party for the difference.

Final Thoughts

A property insurance waiver of subrogation fundamentally changes your financial exposure after a loss occurs. Before you sign any contract containing waiver language, contact your insurance broker with the specific contract terms to verify whether your policy permits the waiver type and what financial impact a loss would create. This conversation prevents claim denials and unrecovered losses that surface only after damage happens.

When a landlord, contractor, or business partner demands a waiver, push for mutual terms whenever possible instead of accepting one-sided arrangements that shift all risk to you. Limited-scope waivers that restrict coverage to specific activities or loss types offer better protection than blanket language, and negotiating these details upfront costs nothing but prevents thousands in unrecovered costs later. Review your current property insurance policies to identify any existing waivers already in place, then forward any recent contracts mentioning waiver language to your broker for confirmation.

At Variant Insurance Group, we work with Minnesota property owners to review their insurance options and compare protection against actual risk. Contact us to discuss your property insurance needs and ensure your policies align with your contracts, or visit our insurance agency blog to learn more about endorsements and coverage details.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation