Your home contains thousands of dollars worth of belongings-from furniture to electronics to clothing. Most people don’t realize what personal property insurance covers until they file a claim.

At Variant Insurance Group, we help Minnesota homeowners understand their protection options. This guide breaks down exactly what’s included, what’s excluded, and how to choose the right coverage for your situation.

What Personal Property Insurance Actually Covers

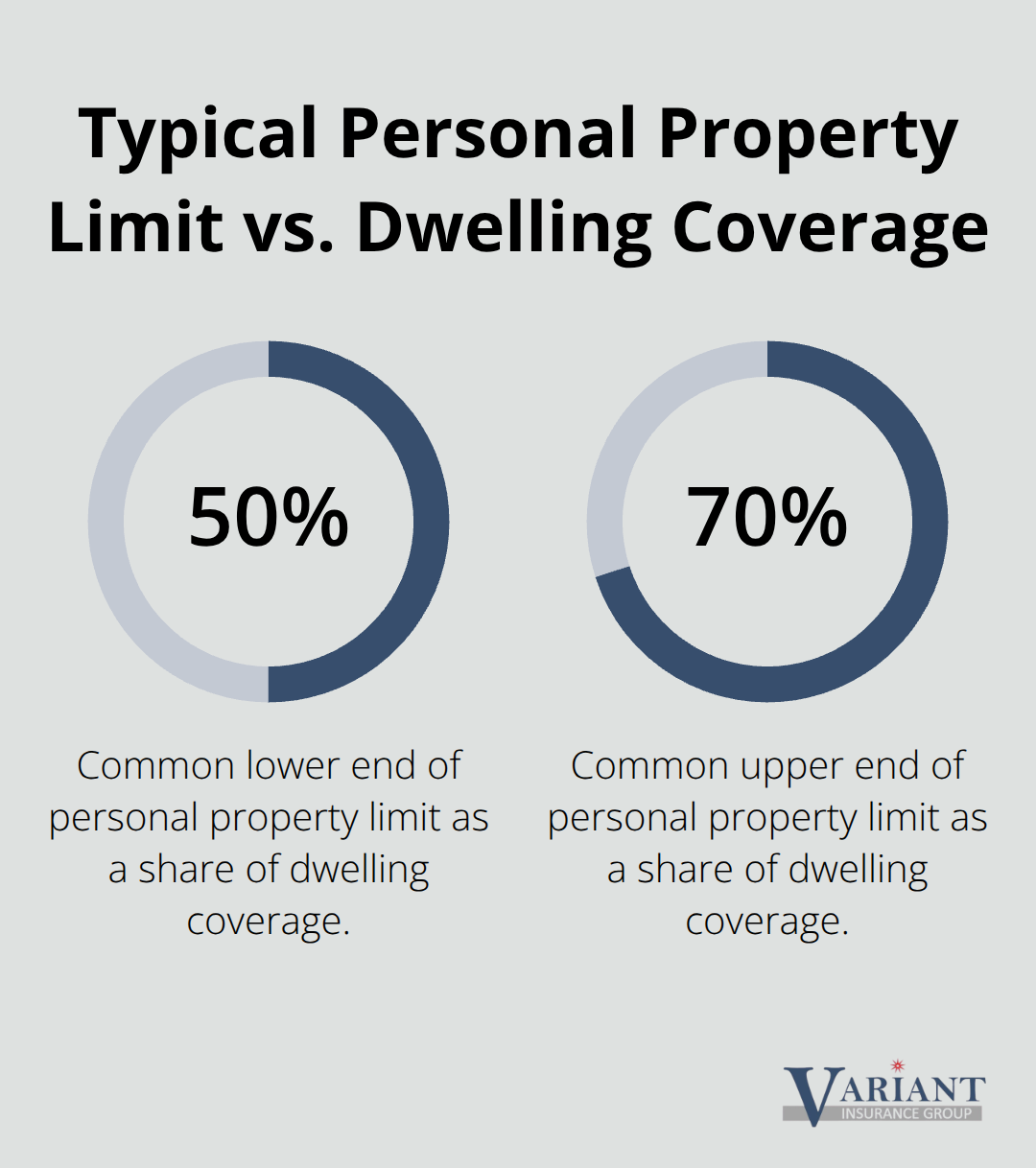

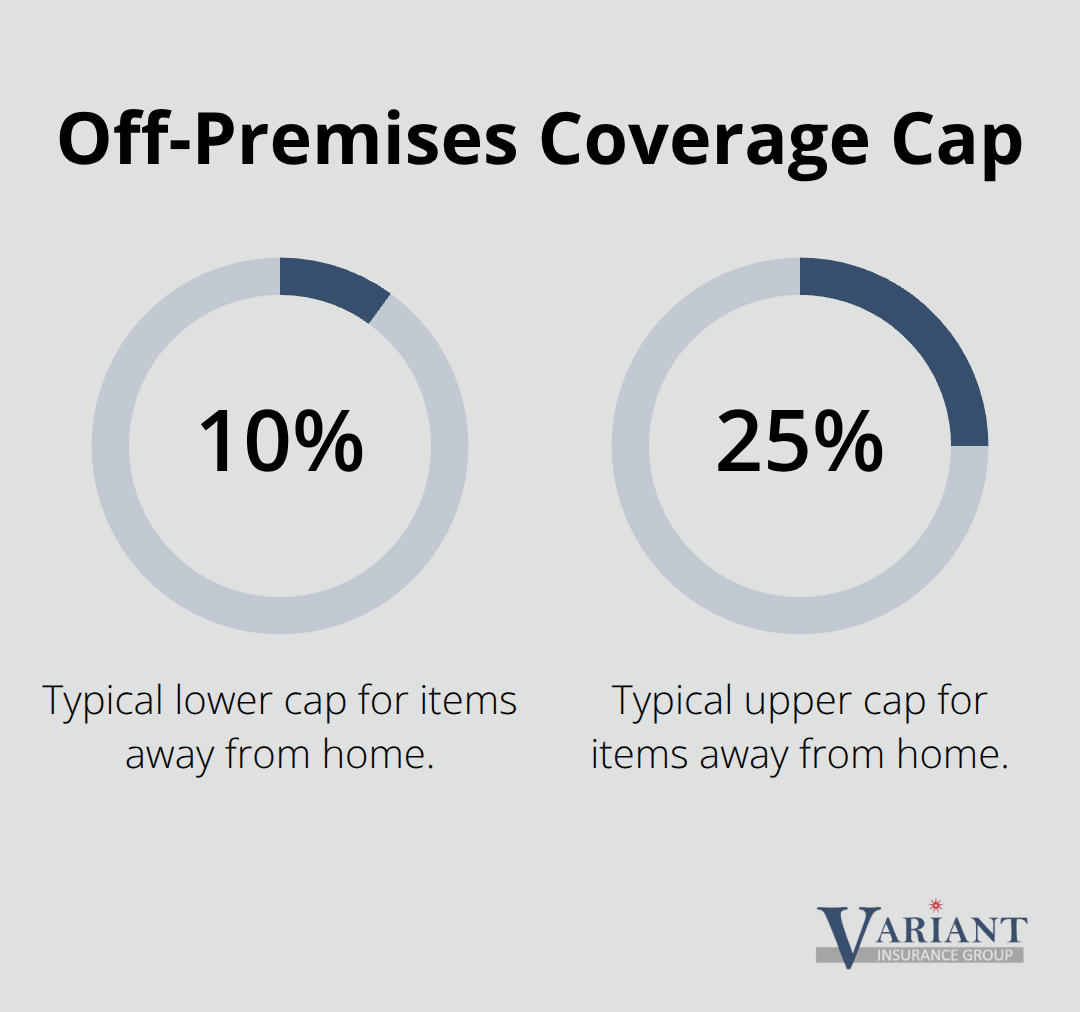

Personal property coverage protects the belongings inside your home from covered losses like fire, theft, and wind damage. This includes furniture, electronics, clothing, appliances, tools, and dinnerware. The coverage applies whether items are damaged at home or taken with you-though off-premises coverage typically caps at a percentage of your total personal property limit, often around 10 to 25 percent depending on your policy. Personal property limits are usually set at 50 to 70 percent of your dwelling coverage amount, but you can adjust this percentage to match what your belongings are actually worth.

Most Minnesota homeowners don’t realize they can customize these limits, which means many people end up either over-insured or dangerously under-protected. The key is calculating replacement cost, not what you originally paid. If your couch cost $800 five years ago but would cost $1,500 to replace today, the replacement cost is what matters for coverage purposes.

Setting the Right Coverage Limit

Your personal property limit directly affects your premium. The trade-off is real, but being under-insured is worse. Start by documenting what you own-photograph items in each room, note approximate replacement costs, and keep receipts for major purchases. Many people discover they own far more than they thought when they actually inventory their home. Your deductible also matters significantly. Choose a deductible you can actually afford to pay without financial strain.

Understanding Your Policy Type and Coverage

Coverage depends on which type of policy you have. HO-3 policies, the most common homeowners policy in Minnesota, provide all-risk coverage for personal property, meaning nearly everything is covered except for specific exclusions like flood, earthquake, and certain high-value items. HO-2 policies offer named-peril coverage, protecting against roughly 16 specific perils including fire, wind, and theft, but leaving gaps for other damage types. Water damage from burst pipes or appliance leaks is covered, but external floodwaters are not-you’ll need a separate flood policy through the National Flood Insurance Program for that protection.

Protecting High-Value Items

High-value items like jewelry, watches, and fine art typically have sublimits ranging from $500 to $2,500 unless you add a scheduled personal property endorsement. A professional appraisal is required to schedule items, but this approach guarantees full replacement cost coverage for those specific valuables. Business property and vehicles are always excluded from personal property coverage, even if stored at home. Understanding these exclusions helps you identify what additional coverage you may need to protect your most valuable possessions.

Common Items Covered Under Personal Property Insurance

Furniture, electronics, clothing, and household goods form the backbone of personal property coverage, but the specifics matter more than most Minnesota homeowners realize. Standard homeowners policies cover your couch, television, kitchen appliances, winter coat, and dishes as long as a covered peril like fire, wind, or theft damages or steals them. Water damage from a burst pipe in your basement also triggers coverage for belongings destroyed in that incident. The Insurance Information Institute notes that personal property coverage applies to items away from home too, though the coverage amount typically caps at 10 to 25 percent of your total personal property limit. This means if you have $100,000 in personal property coverage, you might only have $10,000 to $25,000 of protection for items you take on vacation or leave at a friend’s house.

That gap matters if you travel with expensive electronics or sporting equipment.

What Your Belongings Actually Cost to Replace

Most people drastically underestimate their belongings’ replacement value. A typical three-bedroom Minnesota home contains replaceable items when you account for current retail prices by multiplying your home’s square footage by average building costs per square foot in your area. Furniture alone adds up fast: a quality bedroom set runs $3,000 to $8,000, a living room sofa costs $2,000 to $5,000, and kitchen appliances like a refrigerator or range each exceed $1,500. Electronics compound this quickly-a laptop, television, and smartphone easily total $4,000 to $6,000. Clothing inventories surprise people too; a modest wardrobe with winter coats, work clothes, and casual wear reaches $5,000 to $10,000 in replacement cost.

The only accurate way to determine your real coverage needs is to photograph items room-by-room and estimate what it would cost to replace them today at current prices, not what they cost when you bought them. Keep those photos and receipts in a safe location outside your home (such as cloud storage or a safe deposit box) so you have proof if you need to file a claim.

High-Value Items and Sublimits

Certain high-value items within these categories often hit sublimits that leave you dangerously under-protected. Jewelry and watches typically cap at $500 to $2,500 under standard coverage, even if your total personal property limit is much higher. A single engagement ring or watch collection can exceed that threshold instantly. Fine art, collectibles, and antique furniture face similar restrictions. If you own items worth more than your policy’s sublimit, a scheduled personal property endorsement is your only real option for full replacement cost protection.

This requires a professional appraisal, which costs $100 to $500 depending on the item’s complexity, but it guarantees you receive the full appraised value if loss occurs. Without scheduling, you’re gambling that you won’t experience a loss or that your insurer will cover more than the sublimit allows-a bet you’ll lose if damage happens. Some items that look ordinary also carry restrictions; expensive tools, sporting equipment, and musical instruments sometimes face sublimits or exclusions entirely.

Identifying Your Coverage Gaps

Review your policy or contact your agent to identify which of your possessions fall into restricted categories. The difference between standard coverage and scheduled protection can mean thousands of dollars in a claim. Understanding these gaps helps you decide whether additional endorsements make sense for your situation and what items truly need that extra layer of protection.

What Isn’t Covered by Personal Property Insurance

Your homeowners policy has hard limits on what personal property coverage actually protects. Vehicles, motorized equipment, and business inventory face complete exclusion regardless of your coverage amount. A car in your garage, a motorcycle in your shed, or a lawn mower in your basement receives zero protection under personal property coverage, even though these items sit inside your home. You need separate auto insurance for vehicles and recreational equipment policies for items like ATVs or jet skis. Business property faces the same complete exclusion. If you run a home-based business, equipment, inventory, tools, and supplies used for that business fall outside personal property protection. A photographer’s camera equipment, a consultant’s computer setup, or a crafter’s materials stored at home all lack coverage under your homeowners policy. The Insurance Information Institute confirms that personal property coverage explicitly excludes cars and equipment used for home business purposes. This gap surprises Minnesota homeowners who assume their homeowners policy protects everything inside the walls. It does not.

The Sublimit Problem with High-Value Items

High-value items create a different problem than outright exclusions. Rather than being completely off-limits, items like jewelry, watches, fine art, and collectibles receive coverage but only up to sublimits that rarely match their actual value. Standard homeowners policies typically cap jewelry at $500 to $2,500 total, which means a single engagement ring or inherited watch collection instantly exceeds your protection. Fine art and antiques face similar restrictions, often capped at $1,500 to $2,500 regardless of their market value. Scheduled personal property endorsements allow you to add extra coverage in order to insure high-value items beyond the limits imposed by a standard homeowners policy. Without scheduling, you absorb the loss above your sublimit yourself.

How Scheduled Personal Property Works

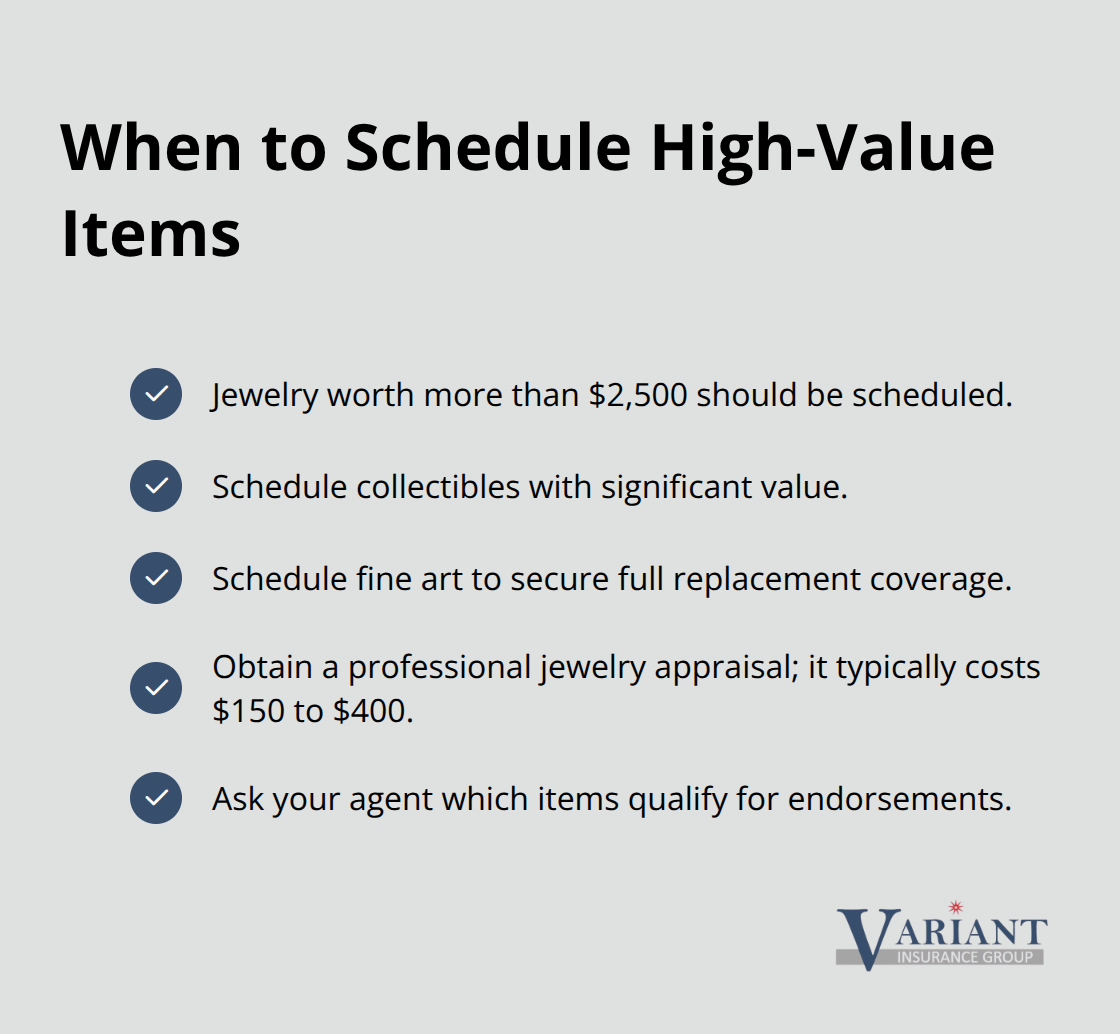

A jewelry appraisal costs $150 to $400 and takes a few hours, but scheduling that engagement ring for its appraised value guarantees full replacement coverage if theft or damage occurs. Many Minnesota homeowners skip this step and lose thousands when loss happens. If you own jewelry worth more than $2,500, collectibles with significant value, or fine art, scheduling becomes a financial necessity rather than an optional upgrade. Your agent can walk you through the scheduling process and explain which items in your home qualify for endorsements based on their replacement value and your policy specifics. The appraisal requirement protects both you and your insurer by establishing clear value before a loss occurs, which eliminates disputes during the claims process.

Business Equipment at Home

The exclusion for business property extends to any equipment or materials you use for income-generating activities. A home office setup for consulting work, craft supplies for a side business, or professional tools all fall outside coverage. This applies even if your business operates part-time or from a spare bedroom. Standard homeowners policies treat business property as a separate risk category that requires its own insurance solution. If you operate any business from your home, contact your agent about business property coverage or a home-based business endorsement to protect those assets separately from your personal property coverage.

Final Thoughts

Personal property insurance covers the belongings that make your house a home, but only if you understand what your policy actually protects. The gap between what Minnesota homeowners think they’re covered for and what their policies actually include costs families thousands of dollars every year. Standard homeowners policies protect furniture, electronics, clothing, and household goods from covered perils like fire and theft, yet they exclude vehicles, business equipment, and items with sublimits like jewelry.

Start by photographing items in each room and noting current replacement costs (add them up by category to see the real total). Most Minnesota homeowners discover they own far more than they realized when they actually complete this exercise. If your personal property limit falls short of that total, increasing it costs far less than absorbing a loss yourself, and if you own jewelry, collectibles, or fine art worth more than your policy’s sublimits, professional appraisals and scheduled endorsements protect those items fully.

The right policy matches your actual needs and budget. We at Variant Insurance Group work with Minnesota’s top-rated insurance companies to find the coverage and pricing that fit your home and your life. Contact us to review your personal property coverage and confirm you’re truly protected.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation