Minnesota businesses face complex risks that require comprehensive protection strategies. Business insurance and bonding work together to safeguard your operations from liability claims, property damage, and contractual obligations.

We at Variant Insurance Group understand that selecting the right coverage combination can feel overwhelming. The key lies in matching your specific industry risks with appropriate insurance policies and bond requirements.

Types of Business Insurance Coverage

General Liability Insurance Protection

General liability insurance serves as your first defense against third-party claims that could bankrupt your business overnight. This coverage protects against bodily injury lawsuits, property damage claims, and personal injury accusations that cost Minnesota businesses millions annually. The average claim reaches $47,316, but slip-and-fall incidents can easily exceed $50,000 in medical costs and legal fees according to the National Safety Council.

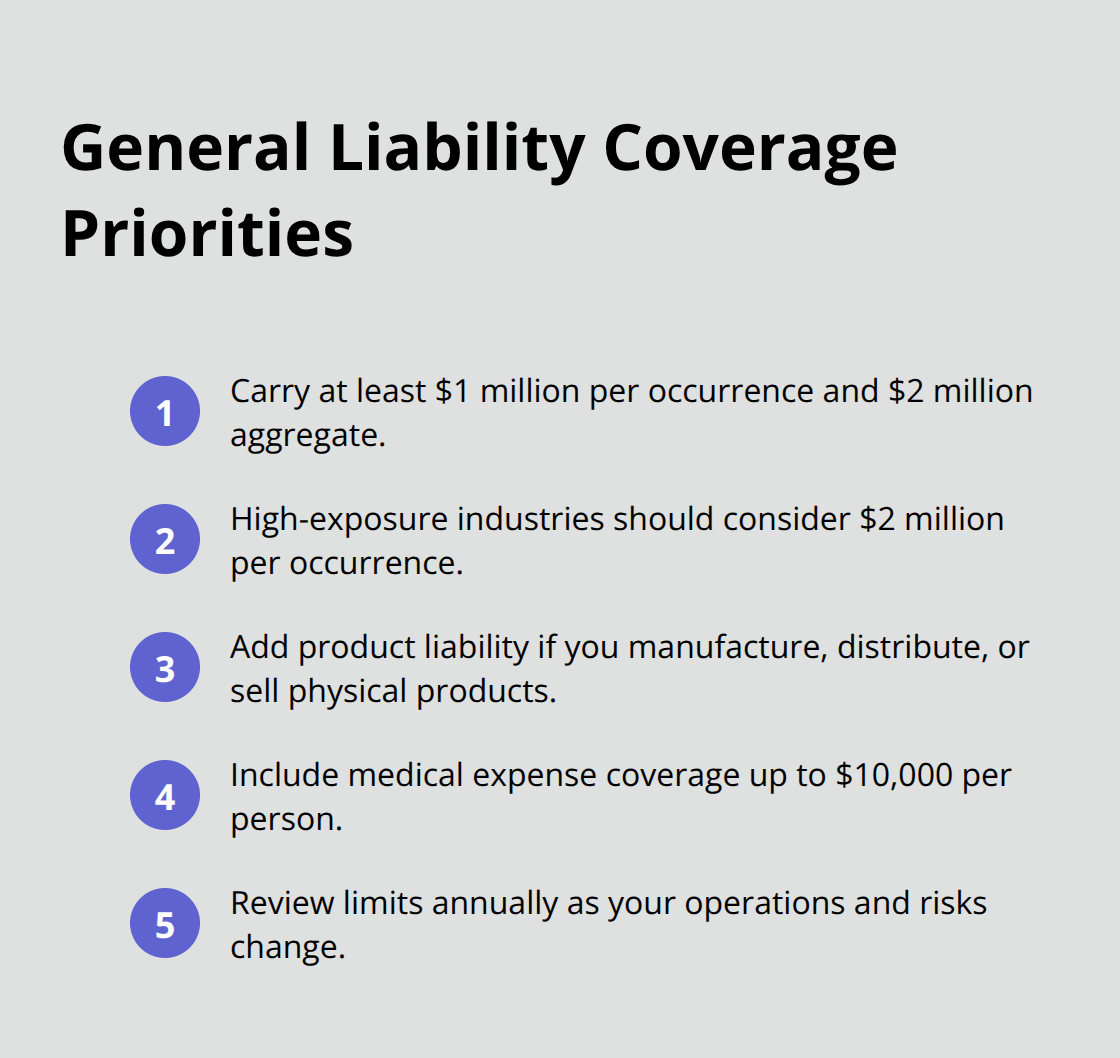

Smart business owners purchase at least $1 million per occurrence with $2 million aggregate limits. Restaurant owners, contractors, and retail businesses face higher exposure and should consider $2 million per occurrence. Product liability coverage becomes mandatory if you manufacture, distribute, or sell physical products. Medical expense coverage within your policy pays up to $10,000 per person for immediate medical costs, often preventing small incidents from becoming major lawsuits.

Property Insurance for Physical Assets

Commercial property insurance protects buildings, equipment, inventory, and business personal property against fire, theft, vandalism, and weather damage. Minnesota businesses face unique risks from severe winter storms, flooding, and hail damage that can destroy operations within hours. Replacement cost coverage costs 15-20% more than actual cash value but prevents devastating underinsurance gaps when equipment loses value over time.

Business interruption coverage pays ongoing expenses and lost income when property damage forces temporary closure. This coverage typically pays up to 12 months of lost revenue and continuing expenses (like payroll, rent, and loan payments). Equipment breakdown coverage protects against mechanical failures of HVAC systems, computers, and machinery that standard property insurance excludes.

Workers Compensation Requirements

Minnesota law requires workers compensation insurance for businesses with one or more employees, including part-time workers and family members. Penalties for non-compliance reach $1,000 per employee plus potential criminal charges and personal liability for all medical costs and lost wages. Construction, manufacturing, and healthcare businesses face the highest premiums due to injury frequency rates that exceed 4.0 cases per 100 workers annually.

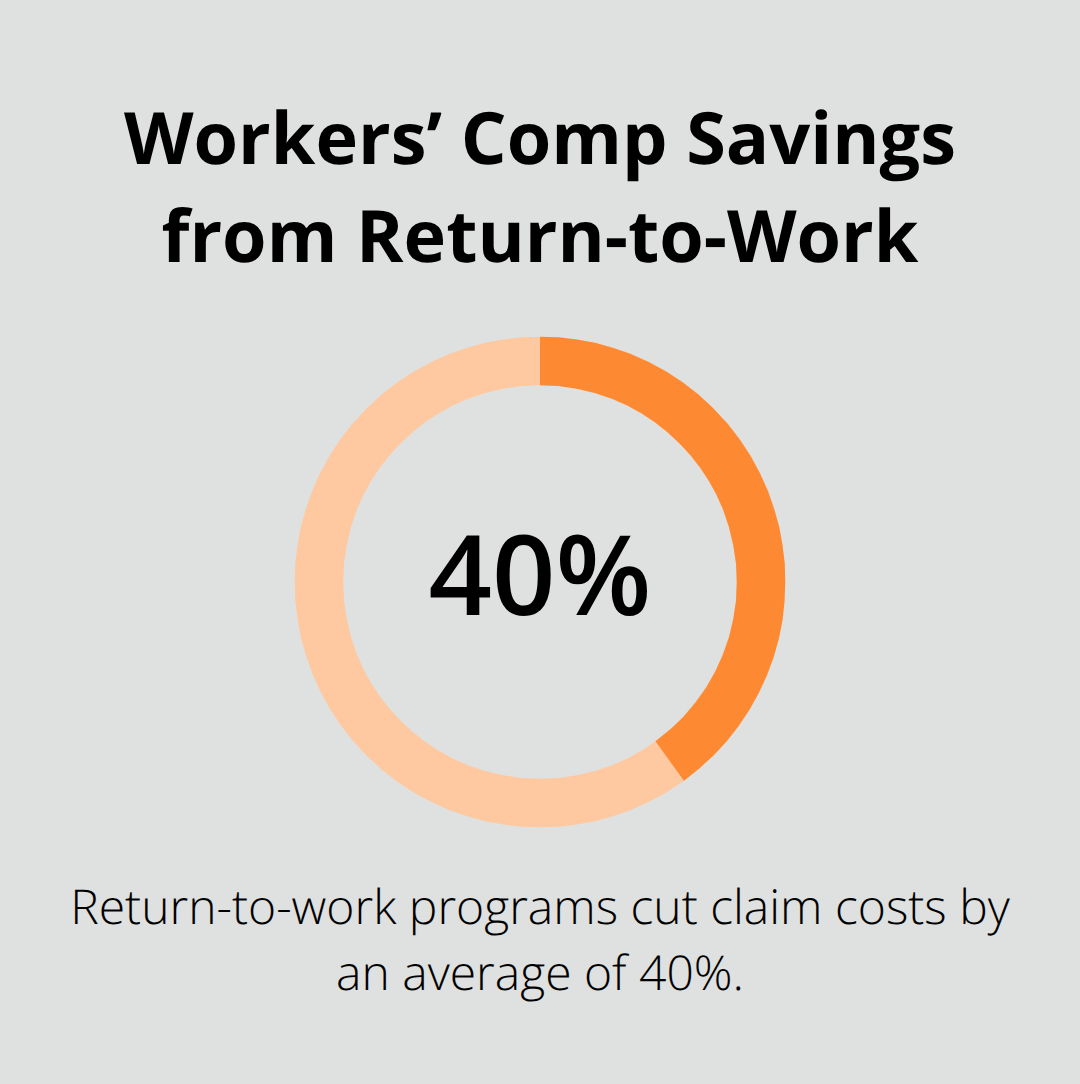

Experience modification rates directly impact your premiums based on your claims history compared to similar businesses. Companies with strong safety programs can achieve experience mods below 1.0, which reduces premiums by 20-30%. Return-to-work programs that bring injured employees back to modified duties cut claim costs by an average of 40% while they maintain workforce productivity.

These insurance foundations protect your daily operations, but contractual obligations and regulatory compliance require additional protection through specialized bonds.

Understanding Business Bonding Requirements

Contract Bonds for Construction Projects

Contract bonds create legally binding guarantees that protect clients, government entities, and business partners from financial losses when contractors fail to meet their obligations. Performance bonds guarantee project completion according to specifications while payment bonds protect subcontractors and suppliers from non-payment issues that plague the construction industry.

The SBA’s Surety Bond Guarantee Program guaranteed bonds totaling more than $9.2 billion in contract value in fiscal year 2024, supporting over 2,000 small businesses through guaranteed bid and final bonds. Minnesota contractors who work on federal projects can access SBA bond guarantees up to $14 million, with QuickApp processing that provides one-day approvals for contracts under $500,000.

License and Permit Bonds for Compliance

License and permit bonds fulfill state and local regulatory requirements across industries from auto dealers to mortgage brokers. These bonds protect the public from business misconduct and guarantee compliance with industry regulations that govern professional conduct.

Compliance bonds range from $10,000 to $100,000 depending on business type and regulatory exposure. Minnesota requires specific bonds for contractors, collection agencies, and financial service providers. Public safety bonds protect consumers from substandard work, while financial guarantee bonds secure proper handling of client funds.

Fidelity Bonds for Employee Protection

Fidelity bonds protect against employee theft and dishonesty, which becomes mandatory for businesses that handle client funds or sensitive financial information. The average employee theft claim reaches $175,000 according to the Association of Certified Fraud Examiners, making fidelity coverage a smart investment for businesses with cash handling, bookkeeping, or client account access.

These bonds cover losses from employee fraud, forgery, and theft of money or securities. Businesses in banking, accounting, and retail face higher exposure and should consider blanket fidelity bonds that cover all employees rather than individual position bonds.

The right combination of insurance and bonds requires careful evaluation of coverage options, pricing structures, and carrier reliability to protect your business effectively.

Choosing the Right Insurance and Bonding Partner

Your insurance and bonding partner choice determines whether you receive competitive pricing, comprehensive coverage, and reliable claims service when disasters strike. Independent agents outperform direct carriers by shopping multiple companies to find the best combination of coverage and pricing for your specific risks. Direct carriers limit you to their single product line, which rarely provides optimal protection across all business exposures.

Compare Coverage Options and Pricing Structures

Smart business owners request detailed proposals from at least three different agents to compare coverage limits, deductibles, and exclusions across multiple carriers. Premium differences of 30-40% between carriers are common for identical coverage, which makes thorough comparison shopping mandatory for cost-conscious businesses.

Independent agents provide access to multiple insurance companies compared to captive agents who sell only one carrier’s products. Request specific coverage examples for your industry’s most frequent claims to identify gaps in proposed policies. Workers compensation experience modification factors, general liability aggregate limits, and property replacement cost provisions vary significantly between carriers and directly impact your financial protection.

Evaluate Financial Strength and Claims Performance

Choose carriers with AM Best ratings of A- or higher to guarantee they can pay claims during catastrophic events that bankrupt weaker insurance companies. The 2008 financial crisis eliminated dozens of insurance carriers, which left policyholders without coverage or claims payments.

Review your agent’s claims settlement statistics and average processing times for your coverage types. Property damage claims should settle within 30 days while liability claims require 60-90 days for complex investigations. Agents who handle 500+ policies annually possess the experience and carrier relationships needed to expedite your claims and negotiate better settlement terms than smaller agencies.

Assess Service Quality and Response Times

Your agent’s response time during emergencies can mean the difference between minor inconvenience and major business disruption. Test potential agents by calling their office during business hours and after hours to measure their accessibility. Quality agents return calls within two hours during business days and provide 24/7 emergency contact information for urgent claims situations.

Ask for client references from businesses similar to yours in size and industry. Contact these references to learn about their claims experiences, premium increases over time, and overall satisfaction with service quality. Agents who maintain long-term client relationships (averaging 5+ years) demonstrate consistent service delivery that builds trust over time.

Final Thoughts

Business insurance and bonding decisions demand careful analysis of your specific risks, regulatory requirements, and financial exposure. Minnesota businesses that combine comprehensive insurance coverage with appropriate bonds protect themselves against liability claims, property damage, and contractual failures that destroy operations overnight. Proper coverage planning delivers measurable benefits beyond basic protection.

Businesses with adequate business insurance and bonding access better contracts, qualify for government projects, and maintain operations during unexpected events. The SBA’s record-breaking $9.2 billion in guaranteed bonds shows how proper bonds open doors to lucrative opportunities that drive business growth. Smart business owners recognize that protection investments pay dividends through expanded market access and operational stability.

Your next step involves partnering with an experienced independent agent who understands Minnesota’s unique business environment. Variant Insurance Group shops Minnesota’s top-rated insurance companies to find the right combination of coverage and pricing for your specific needs. We review your options, compare protection levels, and build relationships that provide ongoing support as your business evolves (including claims assistance when you need it most).