Running a fleet in Minnesota means navigating state regulations, federal compliance rules, and coverage gaps that standard policies simply don’t address. A Minnesota commercial auto policy built for fleet operations protects your vehicles, drivers, and business from the real risks you face daily.

At Variant Insurance Group, we’ve seen too many fleet owners discover coverage holes only after a claim. This guide walks you through what you actually need.

What Minnesota Requires for Commercial Fleet Operations

State Minimum Coverage Limits Fall Short for Fleet Operations

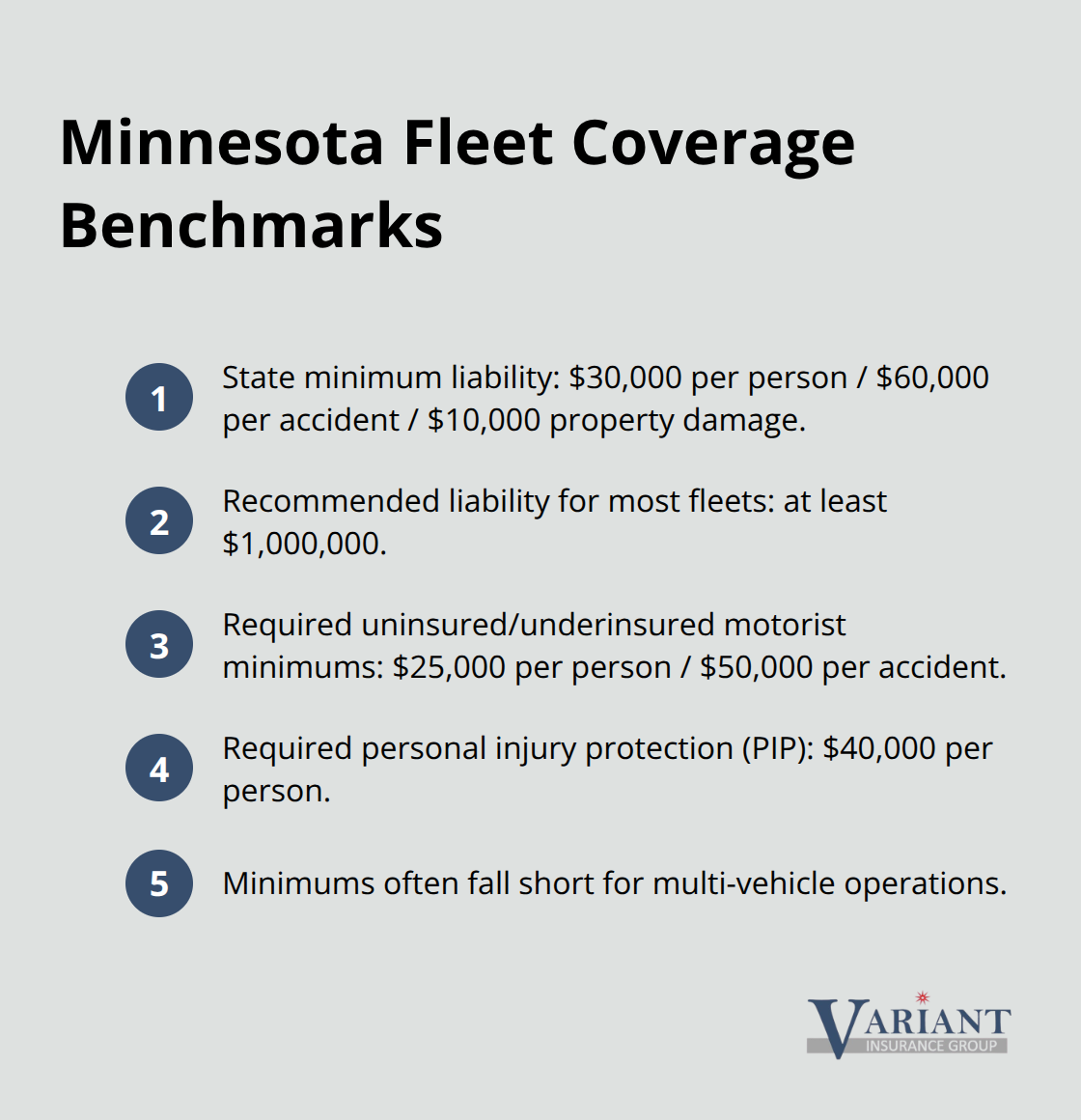

Minnesota law demands that any business using vehicles for work carry commercial auto insurance. Personal policies simply do not cover work-related use, and this distinction matters enormously. A delivery driver, service technician, or sales representative operating under your business name needs commercial coverage, even if they drive a single vehicle. The state’s minimum liability requirements are $30,000 per person for bodily injury, $60,000 per accident for bodily injury, and $10,000 for property damage. However, these minimums are dangerously low for fleet operations.

A single serious accident involving multiple vehicles or injuries can easily exceed these thresholds, leaving your business exposed to personal liability claims that pierce through your company’s assets. Most commercial operations should carry $1 million in liability limits or higher, particularly if your vehicles transport people, deliver goods, or operate in high-traffic areas. Minnesota also requires uninsured and underinsured motorist coverage at $25,000 per person and $50,000 per accident, plus mandatory personal injury protection at $40,000 to cover medical costs after a crash regardless of fault.

Federal Compliance Standards Add Stricter Requirements

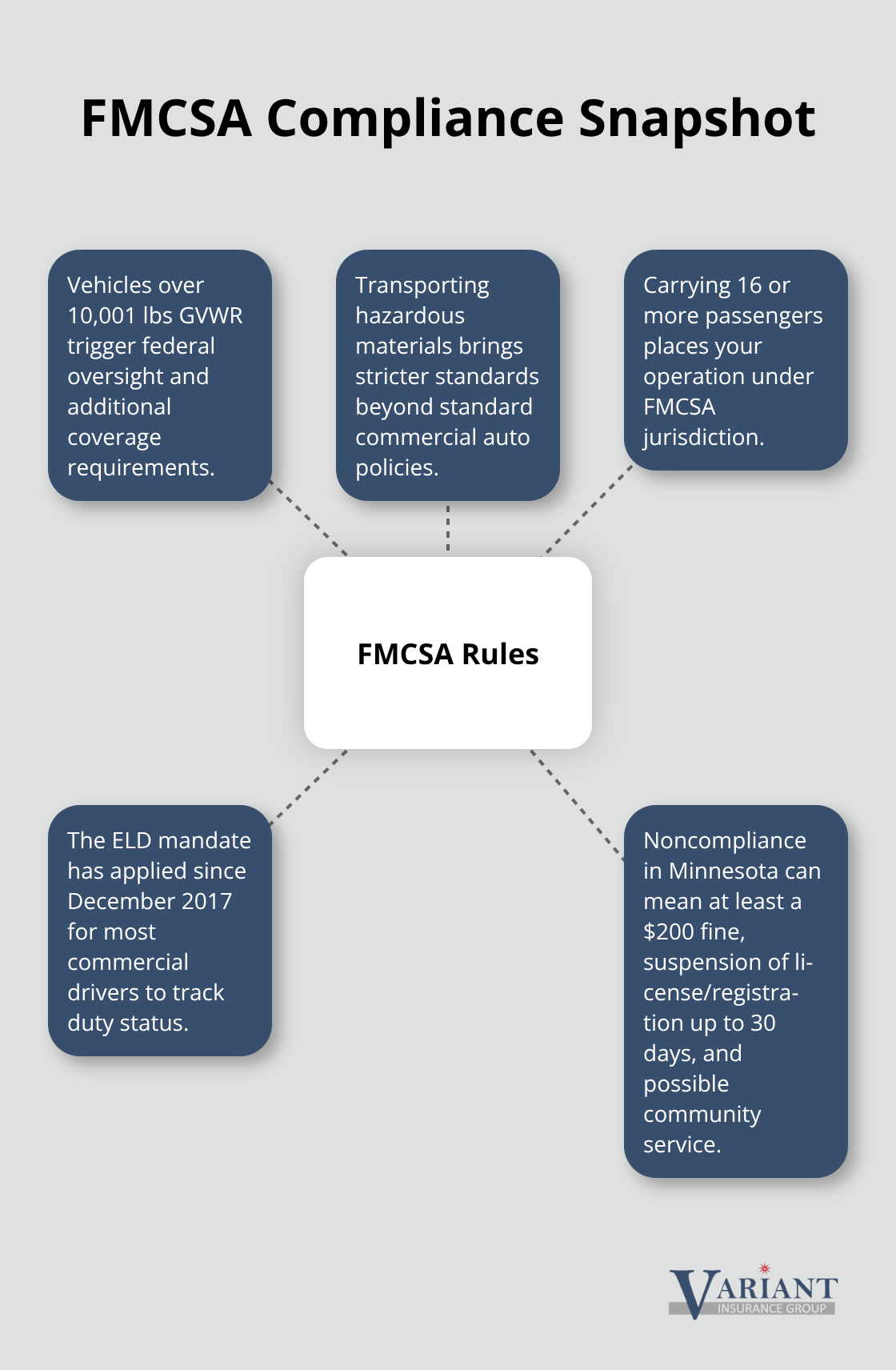

Federal compliance adds another layer of requirements that many fleet owners overlook. If your vehicles exceed 10,001 pounds gross vehicle weight rating, transport hazardous materials, or carry 16 or more passengers, your operation falls under Federal Motor Carrier Safety Administration jurisdiction and requires additional coverage. The FMCSA Electronic Logging Device mandate has been in effect since December 2017, meaning most commercial drivers must use electronic logs to track duty status.

Larger commercial vehicles like semi-trucks carry even stricter liability requirements determined by your USDOT number and docket with the FMCSA. These federal standards exist because commercial operations create significantly higher risk than personal driving. Failing to carry proper coverage results in at least a $200 fine in Minnesota, plus potential license and vehicle registration suspension for up to 30 days and possible community service.

Why Generic Policies Leave Fleets Unprotected

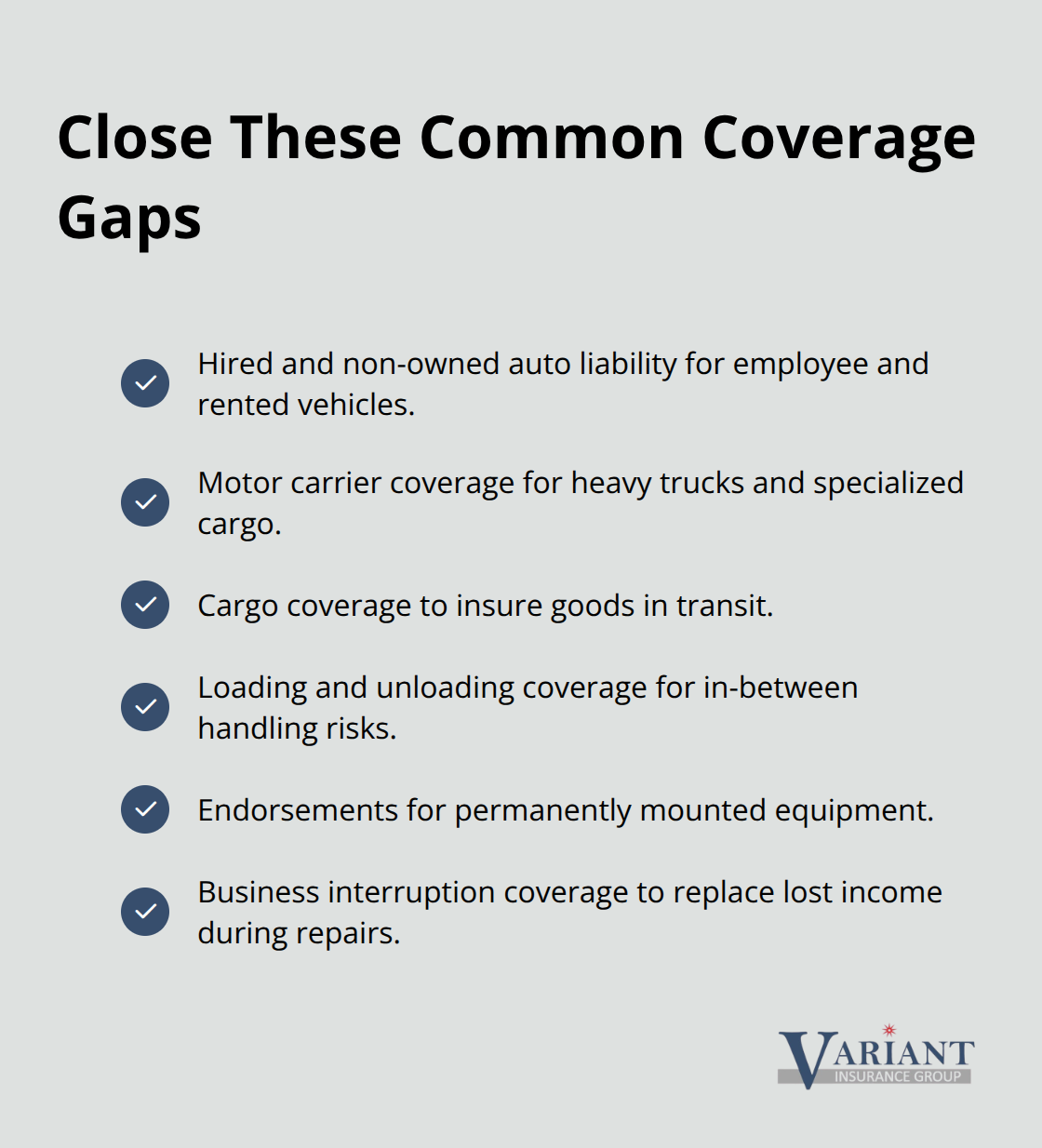

A generic commercial auto policy written for a single service vehicle will not adequately protect a multi-vehicle fleet with employees, varying vehicle types, or specialized cargo. You need hired and non-owned vehicle coverage if employees use personal cars for business tasks, motor carrier coverage if you operate heavy-duty trucks, and collision and comprehensive protection on all owned vehicles. The average Minnesota commercial auto insurance costs about $213 per month or $2,560 per year according to Insureon data, but this varies dramatically based on vehicle count, types, driver records, location, and claims history.

The specific coverage gaps in standard policies become apparent only when you examine what your fleet actually does. Understanding these gaps requires looking at the protection options that address them directly.

Coverage That Matches What Your Fleet Actually Does

Hired and Non-Owned Vehicle Coverage Protects Your Business

When employees drive personal vehicles for work or your operation includes hired equipment, standard fleet policies leave dangerous gaps. Hired and non-owned vehicle coverage helps protect businesses from property damage and bodily injury liability costs when you or your employees use personal cars, rental vehicles, or borrowed equipment for company tasks. This coverage applies liability protection to those vehicles even though your business does not own them-a critical distinction because personal auto policies explicitly exclude business use. If a delivery driver causes an accident while driving their own car to make a customer visit, your business faces direct liability exposure without this protection.

The cost of adding this protection typically ranges from $300 to $800 annually depending on your fleet size and driver count, making it one of the most affordable risk mitigation tools available. Without it, you rely on hoping the employee’s personal policy covers the incident, which it almost certainly does not.

Motor Carrier Coverage for Heavy-Duty Operations

Motor carrier coverage becomes essential if your operation runs heavy trucks, tanker vehicles, or hazardous materials transport. Federal regulations require specific liability limits based on your cargo type and vehicle weight, and standard commercial policies do not provide adequate protection for these specialized operations. A semi-truck operation needs $750,000 to $5 million in liability coverage depending on what the vehicle transports, compared to the $1 million baseline for standard fleet operations.

Minnesota businesses operating under FMCSA jurisdiction must verify their specific requirements through their USDOT number or by contacting the Federal Motor Carrier Safety Administration directly. The difference between underinsured and properly insured motor carrier operations often determines whether a single catastrophic accident bankrupts your business or remains a manageable claim.

Uninsured and Underinsured Motorist Protection Shields Your Fleet

Uninsured and underinsured motorist coverage protects your operation when another driver causes damage but lacks sufficient insurance to cover the costs. Minnesota requires a minimum of $25,000 per person and $50,000 per accident in uninsured motorist coverage, but this minimum protects only your vehicles and drivers. For fleet operations with multiple vehicles and employees, carrying higher uninsured motorist limits at $100,000 per person and $300,000 per accident shields your business from situations where another driver’s insurance falls short.

This coverage matters most in high-traffic corridors where uninsured drivers are statistically more common. Minnesota’s urban areas see higher claim frequency than rural regions, which means your location directly impacts how valuable this protection becomes. The next section addresses the coverage gaps that appear when you examine what happens after an accident occurs.

Common Coverage Gaps and How to Avoid Them

Liability Limits That Fall Short for Multi-Vehicle Operations

Most Minnesota fleet owners face genuine exposure when their liability limits fail to match realistic accident scenarios. Minnesota sees approximately 400,000 traffic accidents annually, and commercial vehicles account for a disproportionate share due to higher mileage and highway exposure. Medical costs for serious injuries routinely reach $500,000 to $2 million per person, and jury awards in Minnesota often exceed these amounts. A fleet with five vehicles carrying only $1 million in liability coverage faces substantial risk when a single accident injures multiple people or causes significant property damage. If your policy carries $1 million in total coverage and your fleet is involved in an accident injuring three people, each person’s recovery potential drops well below their actual damages.

The solution requires calculating realistic worst-case scenarios for your specific operation. A delivery fleet operating in the Minneapolis-St. Paul metro area faces higher accident frequency than rural operations, so your liability limits should reflect this elevated risk. Multi-vehicle operations should carry at least $2 million in liability coverage, particularly if your vehicles operate during peak traffic hours or in densely populated areas. Your location directly impacts how much coverage you actually need because urban corridors present higher accident frequency than rural regions.

Cargo and Equipment Protection Oversights

Cargo and equipment protection represents a critical gap that fleet operators frequently overlook until they experience a loss. Standard commercial auto policies cover only damage to the vehicle itself, not the cargo inside. A refrigerated truck carrying $15,000 in perishable goods that breaks down on a summer day exposes you to total cargo loss with no insurance recovery unless you carry specific cargo coverage. Loading and unloading coverage protects against damage to cargo during these vulnerable moments, which represent the highest-risk periods for loss.

Equipment mounted permanently on vehicles, such as generators, hydraulic lifts, or storage units, may not be covered under standard comprehensive and collision policies and requires additional endorsements to protect properly. A service fleet with permanently installed equipment on each vehicle could face $50,000 to $100,000 in uninsured losses following a single accident or theft. These gaps exist because standard policies treat vehicles as transportation only, not as mobile business assets carrying valuable cargo or specialized equipment.

Business Interruption Protection During Claims

Business interruption protection addresses a different but equally damaging gap: what happens to your revenue when vehicles are out of service. A serious accident that takes three vehicles out of your fleet for two weeks of repairs eliminates your income during that period with no insurance recovery. Some commercial auto policies include business interruption coverage that reimburses lost income during covered claims, though this protection is not standard and requires explicit addition to your policy.

A fleet generating $5,000 daily in revenue faces $70,000 in lost income during a two-week shutdown, making business interruption coverage worth the additional premium for most operations. This coverage type protects your business continuity when accidents or other covered events force temporary shutdowns. Reviewing your current policy with an independent agent who understands fleet operations reveals these gaps quickly and identifies which additional coverages make financial sense for your specific business model.

Final Thoughts

A Minnesota commercial auto policy built for fleet operations requires you to understand three critical layers: state minimums that fall dangerously short, federal compliance standards that add stricter requirements, and coverage gaps that generic policies cannot address. The state’s minimum liability limits of $30,000 per person and $60,000 per accident protect almost nothing in real accident scenarios, while federal requirements for vehicles over 10,001 pounds or carrying hazardous materials demand additional coverage that standard policies omit entirely. The gaps in cargo protection, business interruption coverage, and hired vehicle liability can cost your business tens of thousands of dollars after a single claim.

Most Minnesota fleet owners cannot navigate these requirements alone because your operation faces unique risks based on vehicle types, driver counts, cargo, location, and daily mileage that demand customized protection. An independent insurance agency that understands fleet operations can review your current coverage against your actual business activities and identify exactly where you face exposure. This matters because the difference between adequate and inadequate coverage often determines whether an accident becomes a manageable claim or a business-threatening event.

Contact Variant Insurance Group to schedule a policy review and we will compare your current coverage against what your fleet actually needs. Gather your current policy documents and a list of your vehicles, their uses, and your annual mileage before you reach out. We will show you options for closing gaps without overpaying for unnecessary protection.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation