Owning rental properties in Minnesota comes with real financial exposure. Weather damage, tenant disputes, and liability claims can quickly drain your profits if you’re not properly protected.

Standard homeowners insurance won’t cover your rental business. You need Minnesota landlord coverage specifically designed for investment properties, and we at Variant Insurance Group help landlords like you build policies that actually match your risks.

What Your Minnesota Landlord Policy Actually Covers

Property Damage Protection for Your Building

Minnesota landlord insurance protects three critical areas of your rental business, and understanding exactly what each covers prevents costly gaps when damage or disputes happen. Property damage coverage pays for structural repairs to your building after fire, wind, hail, or winter storms-the most common claims in Minnesota. The national average property damage claim reflects significant exposure from harsh winters, heavy snow loads, and severe spring storms that Minnesota landlords face regularly. This coverage includes the dwelling structure, attached garages, sheds, fences, and any appliances or furnishings you provide as the landlord. It does not cover tenant belongings, which is why requiring renters insurance in your lease protects you from disputes over damaged personal property.

Liability Coverage Against Tenant and Visitor Claims

Liability coverage shields you when someone is injured on your property or files a lawsuit claiming discrimination or wrongful eviction. Typical minimums start around $300,000 per occurrence, though stronger protection runs $500,000 or higher depending on your property size and local risk. Theft and vandalism claims in Minneapolis average about $3,200 per incident compared with roughly $1,800 in Greater Minnesota, according to the Minnesota Department of Public Safety, so your location directly influences both your coverage needs and your premium. A local agent can help you determine whether your specific property and tenant profile warrant higher liability limits or additional protections like umbrella coverage.

Loss of Rent and Legal Defense Coverage

Loss of rent coverage reimburses you for lost rental income when a covered peril makes the unit uninhabitable, typically covering up to about 12 months of payments. Minnesota repair timelines commonly stretch 3 to 6 months after major damage, so this protection keeps your cash flow stable while contractors rebuild. Legal defense and medical payment coverage handles tenant injury claims and protects you against the cost of defending lawsuits, which can run into tens of thousands of dollars before settlement.

Your property’s specific characteristics-age, location, tenant profile, and local crime rates-all shape which coverage limits and add-ons actually make sense for your situation. That’s where working with a local agent becomes essential to match your policy to your actual exposure rather than settling for generic coverage that leaves gaps or overcharges for protection you don’t need.

Why Minnesota’s Rental Market Demands Specialized Coverage

How Minnesota’s Climate Creates Predictable Damage Patterns

Minnesota’s extreme seasonal swings produce weather-related damage that occurs predictably and frequently throughout the year. Winter temperatures drop below freezing roughly 170 days per year in the Twin Cities area, and annual snowfall ranges between 45 and 55 inches, making burst pipes from freezing and ice dams routine claims rather than rare events. Spring and summer bring severe thunderstorms with hail that damage roofs and siding, occasionally followed by tornadoes that cause catastrophic structural loss. Standard homeowners policies exclude rental activities entirely, which means any damage connected to your tenants falls outside coverage. You face personal liability for injuries on the property, discrimination claims, wrongful eviction lawsuits, and property damage caused by tenant negligence-all gaps that homeowners insurance leaves open.

Why Location Dramatically Affects Your Insurance Costs

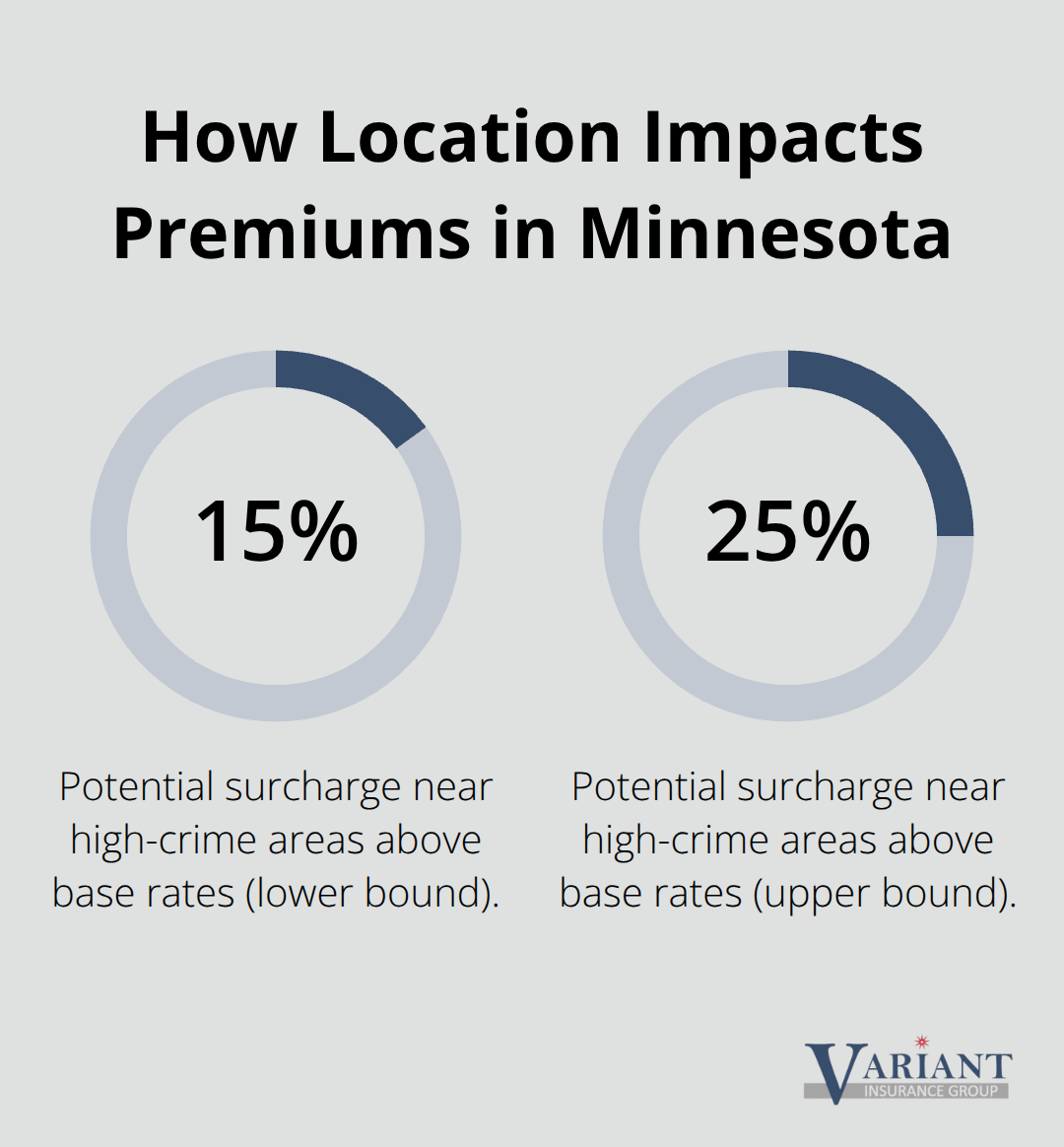

Theft and vandalism claims vary dramatically by location, with Minneapolis averaging $3,200 per incident according to the Minnesota Department of Public Safety while Greater Minnesota averages roughly $1,800, reflecting the crime rate differences that insurers price into premiums. Minneapolis crime rates reach 4,847 incidents per 100,000 residents compared to the statewide average of 1,890, and properties near high-crime areas can see surcharges of 15 to 25% above base rates. Your location matters enormously when calculating both your actual risk exposure and what you’ll pay for protection.

Minnesota’s Landlord-Tenant Laws Create Legal Exposure

Minnesota’s landlord-tenant laws are detailed and specific about your obligations regarding habitability, maintenance, privacy rights, and eviction procedures. According to Minnesota law, the landlord is responsible for keeping the unit in reasonable repair. Violations can result in significant legal defense costs that standard homeowners insurance won’t cover. Landlord-specific policies address these realities directly by covering weather damage to the building structure, liability protection against tenant and visitor injuries, loss of rental income during repairs, and legal defense costs.

What Specialized Landlord Coverage Actually Protects

Minnesota’s harsh climate and tenant-related liability exposure make specialized coverage non-negotiable rather than optional. A local agent familiar with Minnesota properties can assess whether your specific location, building age, and tenant profile warrant higher liability limits, flood insurance through the National Flood Insurance Program, or additional protections like umbrella coverage that extends beyond standard policy limits. Understanding these gaps in standard homeowners insurance sets the stage for selecting the right landlord policy-one that actually matches your property’s unique characteristics and local risks.

Selecting the Right Coverage for Your Minnesota Property

Calculate Replacement Cost and Compare Policy Forms

Start with your property’s actual replacement cost rather than relying on purchase price or assessed value, since Minnesota construction costs have risen steadily and underinsurance penalties apply if your dwelling limit falls below 80 percent of replacement value. Contact three to five local agents and request quotes that specify the form type-Basic Form costs least, Broad Form adds specific perils, and Special Form (DP-3) provides open-peril coverage and serves as the standard for Minnesota rentals. When you compare quotes, verify that each includes property damage, liability at minimum $300,000 per occurrence, and loss of rent covering at least 12 months of income.

Adjust Deductibles and Account for Location-Based Pricing

Ask each agent to explain deductible impact, since raising your deductible from $1,000 to $5,000 can significantly reduce annual premiums while increasing your out-of-pocket responsibility after a claim. Location drives pricing more than any other factor-properties in Minneapolis and St. Paul carry premiums roughly 40 to 60 percent higher than rural Minnesota due to crime rates and litigation risk, so obtain location-specific quotes rather than relying on statewide averages. Your property’s age matters substantially; older buildings with outdated electrical, plumbing, or mechanical systems carry higher premiums, but upgrading electrical panels, roofing, or HVAC systems can cut costs and lower underwriting risk.

Implement Security Measures and Screen Tenants Carefully

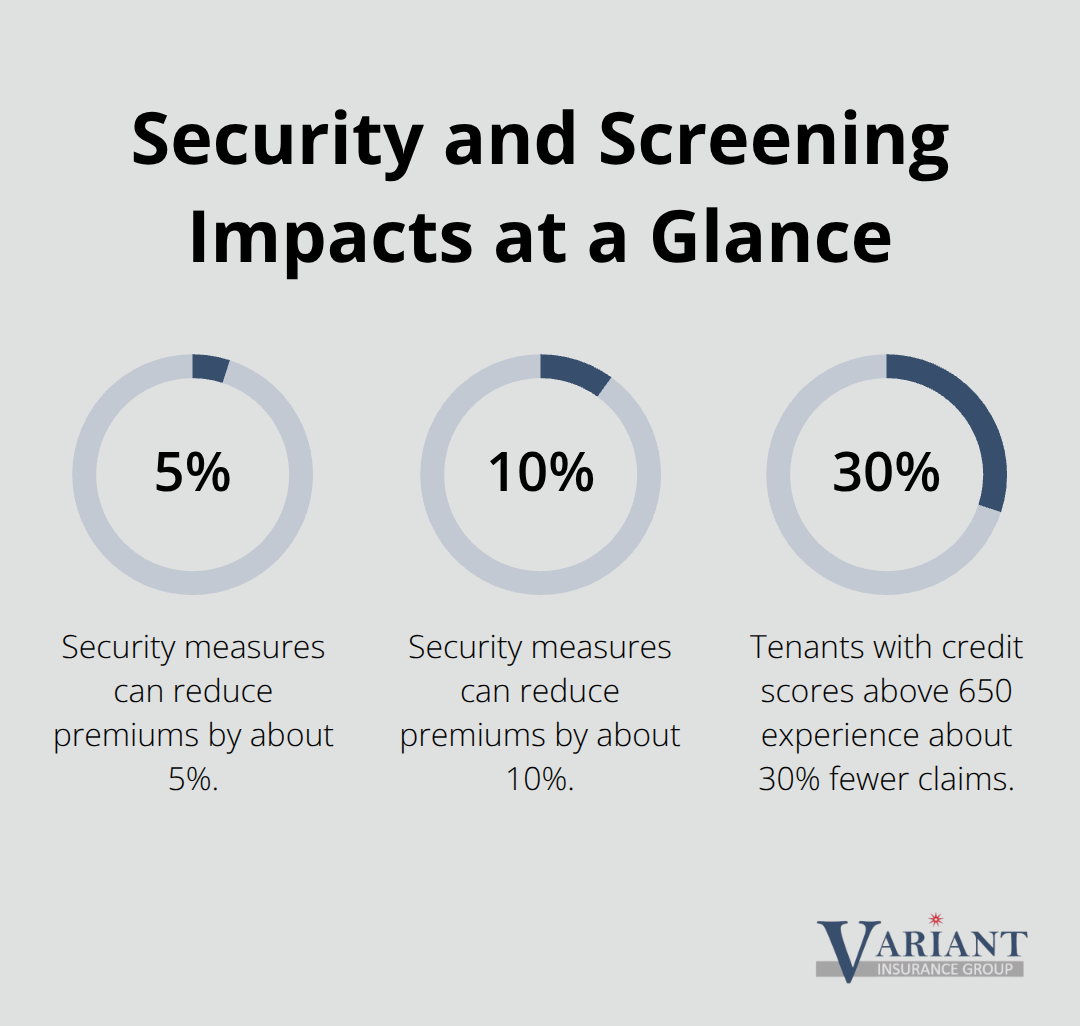

Install security measures like alarm systems, motion-activated lights, and deadbolt locks-these reduce premiums by about 5 to 10 percent and actively deter theft and vandalism. Tenant quality directly influences your rates and claims history. Screen tenants thoroughly through employment verification, background checks, and credit review-tenants with credit scores above 650 experience about 30 percent fewer claims according to underwriting data.

Professional property management firms can yield portfolio discounts of 10 to 15 percent if you manage multiple units.

Verify Carrier Strength and Confirm Coverage Timing

When you find a policy that fits your needs, verify the carrier’s financial strength by checking for an AM Best rating of A- VIII or higher, especially important for DSCR loans where lenders require specific carrier standards. Request that coverage take effect at least 24 hours before closing, provide ACORD certificates to your lender, and obtain final policy documents within 60 days. If your property sits in a flood zone near the Mississippi River, Red River Valley, or Minnesota’s lakes, flood insurance through the National Flood Insurance Program is separate from your landlord policy and essential-check FEMA’s Flood Map Service to confirm your exposure.

Work with a Local Agent for Customized Protection

A local agent who understands Minnesota’s specific weather patterns, tenant laws, and regional risk variations can identify whether your particular property warrants higher liability limits, umbrella coverage, or specialized protections that generic online quotes miss entirely.

Final Thoughts

Minnesota landlord coverage protects your rental income and shields you from the specific risks that Minnesota properties face. Burst pipes from freezing temperatures, hail damage to roofing, tenant injury claims, and liability disputes happen regularly to Minnesota landlords, and standard homeowners insurance leaves you exposed to all of them. The coverage you select directly determines whether a major claim strengthens your financial position or devastates it.

Start by calculating your property’s actual replacement cost and requesting quotes from multiple carriers that specify the policy form, deductible options, and location-based pricing. Compare what each quote includes for property damage, liability limits, and loss of rent protection. Ask about security discounts for alarm systems and motion-activated lights, and confirm that your carrier holds an AM Best rating of A- VIII or higher.

We at Variant Insurance Group specialize in shopping Minnesota’s top-rated insurance companies to find the exact policy that fits your rental business. Our team understands Minnesota’s weather patterns, tenant laws, and regional risk variations, and we compare protection and pricing across multiple carriers so you get the Minnesota landlord coverage you actually need at a fair price. Contact us to discuss your rental property’s specific exposure and secure the tailored protection that keeps your investment safe.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation