Most homeowners insurance policies explicitly exclude rental units and investment properties. If you own a rental home in Minnesota, your standard homeowners policy won’t protect your investment or your rental income.

At Variant Insurance Group, we see investors make this mistake repeatedly-and it costs them thousands when claims get denied. You need specialized coverage designed for investment properties, not a policy built for owner-occupied homes.

What Your Homeowners Policy Actually Excludes

Why Insurers Deny Claims on Rental Properties

Your homeowners insurance policy has a specific purpose: protecting a home where you live. The moment you convert that property into a rental, your coverage becomes invalid. Insurance companies view owner-occupied homes and investment properties as fundamentally different risks. A homeowner maintains their property carefully because they live in it. A tenant has no such incentive. This distinction matters enormously when claims arise.

Standard homeowners policies contain explicit exclusions for rental units, short-term rentals, and any property that generates income. If you file a claim on a rental property covered under a homeowners policy, the insurer will deny it. This isn’t a gray area or a matter of interpretation. The policy language is unambiguous, and insurers enforce these exclusions consistently. Your homeowners policy excludes these business-related claims entirely when rental income is involved.

Minnesota Weather and Rental Property Exposure

In Minnesota, where significant seasonal weather damage occurs regularly, this coverage gap becomes critical. A pipe freeze in January that damages your rental unit? Not covered under homeowners insurance. Tenant negligence that causes a kitchen fire? Denied. You’ll pay repair costs entirely from your own pocket. Winter storms, hail damage, and water intrusion-all common in Minnesota-leave you exposed without proper coverage.

The True Cost of Missing Coverage

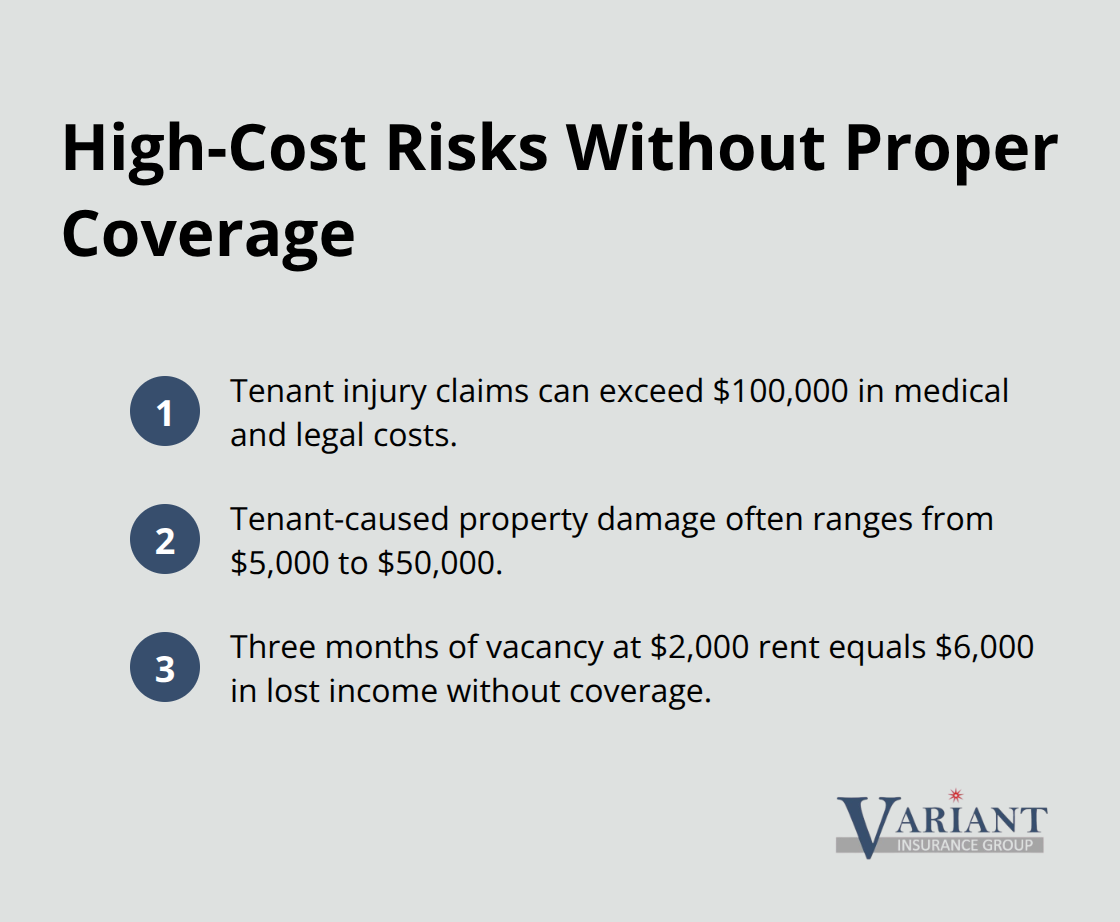

Landlords who rely on homeowners policies face staggering potential losses. A single tenant injury claim can exceed $100,000 in medical and legal costs. Property damage from tenant negligence typically ranges from $5,000 to $50,000 depending on severity.

In Minnesota, with median home prices around $308,000, the reconstruction cost alone justifies specialized coverage.

Loss of rental income during repairs adds another layer of exposure. If your property becomes uninhabitable for three months while repairs happen, and your monthly rent is $2,000, you lose $6,000 in income without loss of rent coverage. Standard homeowners policies provide zero protection here. Insurance companies will cite the policy exclusion and walk away. You become personally liable for every expense.

What Happens After the Denial

Many landlords discover this reality only after filing a claim, at which point it’s far too late. The denial letter arrives, and the financial damage is done. You’ve already paid contractors, covered living expenses for displaced tenants, and lost months of rental income. The insurer’s refusal to pay transforms a manageable loss into a catastrophic one. This is precisely why investment property owners need specialized landlord insurance-a policy designed to handle the unique risks that come with tenants and rental income. Understanding what landlord insurance actually covers helps you make informed decisions about protecting your investment.

What Landlord Insurance Actually Covers

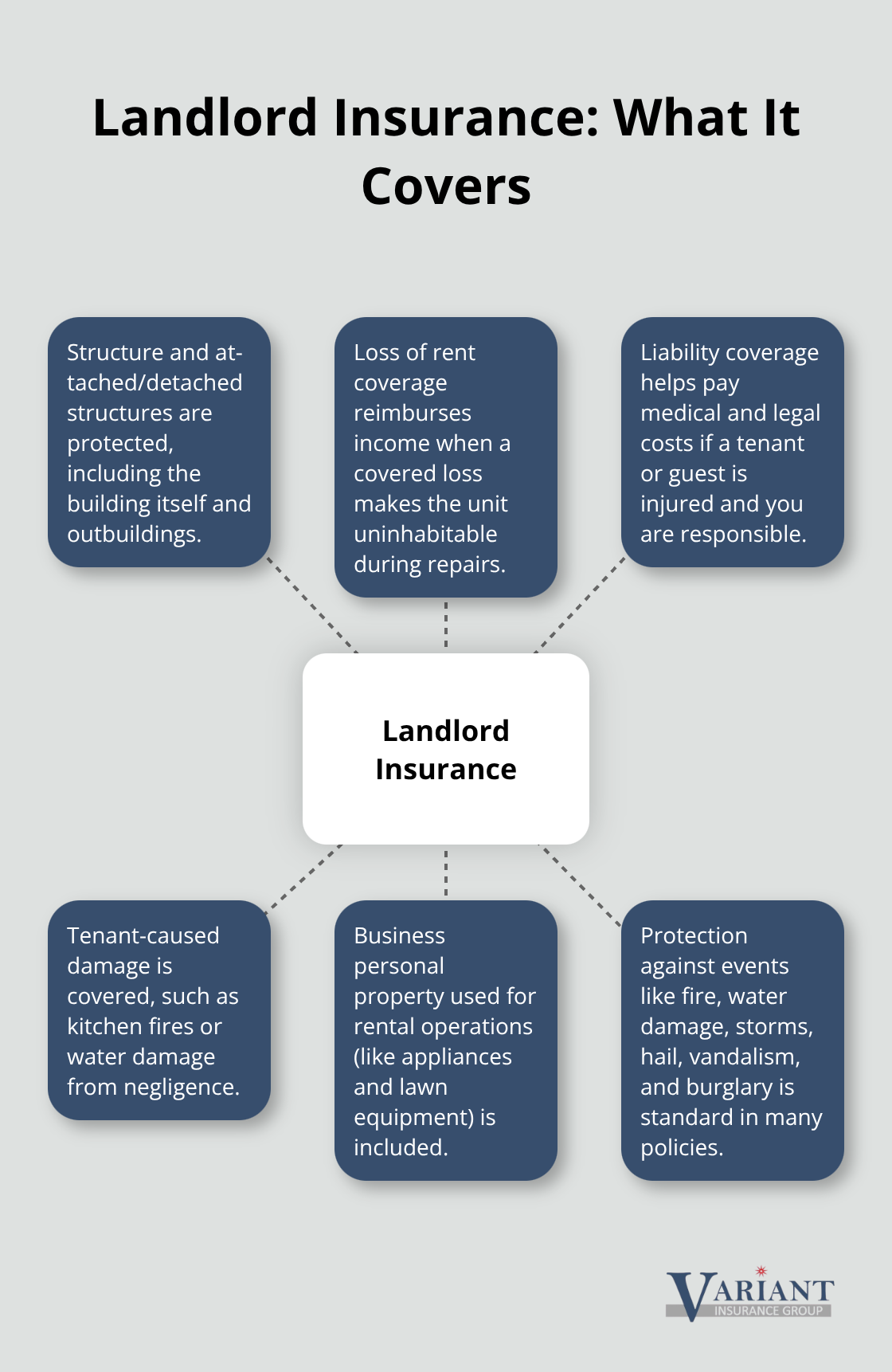

Landlord insurance addresses the specific risks of renting property to tenants in ways that homeowners coverage simply cannot. Unlike homeowners insurance, landlord policies protect the building structure, attached structures, detached structures, and business personal property used for rental operations-think appliances and lawn equipment. Fire, water damage, storm, hail, vandalism, and burglary all fall under core coverages in most policies. The critical distinction is that landlord insurance reimburses tenant-caused damages. A kitchen fire started by a renter, water damage from tenant negligence, or theft by a guest-these situations are covered under landlord insurance but explicitly denied under homeowners policies.

Your policy protects the physical asset itself, not the tenant’s personal belongings inside the unit, which is why renters insurance exists separately for tenant protection.

Income Protection When Disaster Strikes

Loss of rent coverage separates adequate landlord insurance from inadequate coverage. This protection reimburses your rental income if a covered event makes the property uninhabitable during repairs. In Minnesota, where a typical single-family rental generates $1,500 to $2,500 monthly, three months of vacancy costs between $4,500 and $7,500 in lost income. If a pipe freeze damages your property in January and repairs take eight weeks, loss of rent coverage pays your expected rental income while contractors work. Without this protection, you absorb the full income loss while also paying repair costs. The Connecticut duplex example near Yale University illustrates this reality: with $3,200 monthly rent and a replacement cost of $480,000, the annual landlord insurance premium was approximately $1,720, with loss of rent coverage contributing meaningfully to that cost. That investment protects six months of income worth $19,200. The math favors including loss of rent coverage rather than gambling that nothing will happen.

Liability That Protects Your Assets

Liability coverage in landlord insurance protects you from medical expenses and legal costs if a tenant or guest is injured on the property and you’re found responsible. A tenant slips on ice in your entryway and requires surgery costing $150,000. A guest at a tenant’s party falls down stairs and sues for $200,000 in damages. Standard homeowners policies provide minimal liability protection for rental activities, leaving you personally exposed. Landlord policies typically include higher liability limits specifically designed for rental properties, recognizing that tenant turnover and guest activity increase injury risk. Medical payments coverage under landlord policies covers immediate expenses regardless of fault, reducing litigation likelihood. In Minnesota, where weather hazards create slip-and-fall risks during winter months, adequate liability limits matter enormously. Most landlords should carry liability limits of at least $300,000 to $500,000, though higher limits cost relatively little more and provide substantially better protection.

Coverage Tailored to Your Property Type

Different rental properties require different coverage approaches. A single-family home rental faces different risks than a multi-unit building or a short-term vacation rental. Landlord policies adapt to these variations, offering coverage for single-family homes, multi-family buildings, accessory dwelling units, condo units, and even vacant or restoration properties. Short-term rentals like Airbnb and VRBO properties need specialized policies that account for higher guest turnover and increased liability exposure compared to traditional long-term leases. The property type directly influences your premium and the specific coverages you need. A vacation rental in the Boundary Waters region faces different weather risks than a rental in the Twin Cities metro area. Understanding your property’s characteristics helps you select appropriate coverage limits and endorsements that actually match your situation rather than overpaying for unnecessary protection.

What Landlord Insurance Does Not Cover

Landlord policies have clear exclusions that property owners must understand. Normal wear and tear from tenant occupancy is never covered-a worn carpet or faded paint requires your own funds. Intentional damage caused by you or damage resulting from your negligence falls outside coverage. Tenant personal belongings inside the rental unit are not covered (that’s what renters insurance addresses). Flood damage typically requires a separate flood insurance policy, as do earthquakes in certain regions. These exclusions exist because landlord insurance focuses on protecting the structure and your income, not every possible scenario. Knowing what falls outside your policy prevents costly surprises when you file a claim and discover a particular loss isn’t covered. This is precisely why comparing quotes from multiple carriers and working with an agent who understands investment properties helps you identify coverage gaps and fill them with appropriate endorsements or additional policies.

Selecting the Right Coverage for Your Rental Property

Document Your Property’s Exact Characteristics

Start with your property’s specific details, because generic policies waste money and create coverage gaps. Walk through your rental property and note the construction type, heating system, roof age, square footage, number of units, and any recent upgrades. A single-family home with a new roof in Edina faces completely different risks than a multi-unit building with an old furnace in Duluth. Insurance companies price policies based on these specific details, not on assumptions about average Minnesota rentals.

If your roof is five years old, you’ll pay less than someone with a fifteen-year-old roof. If you installed a monitored alarm system and water leak sensors, those safety features can reduce premiums by five to ten percent. Many landlords skip this step and end up with either overpriced policies that cover risks they don’t face or underpriced policies with dangerous coverage gaps. Spend an afternoon measuring square footage, photographing recent upgrades, and listing any structural improvements. This documentation becomes invaluable when you request quotes and invaluable again if you ever file a claim.

Obtain Multiple Quotes and Compare Carefully

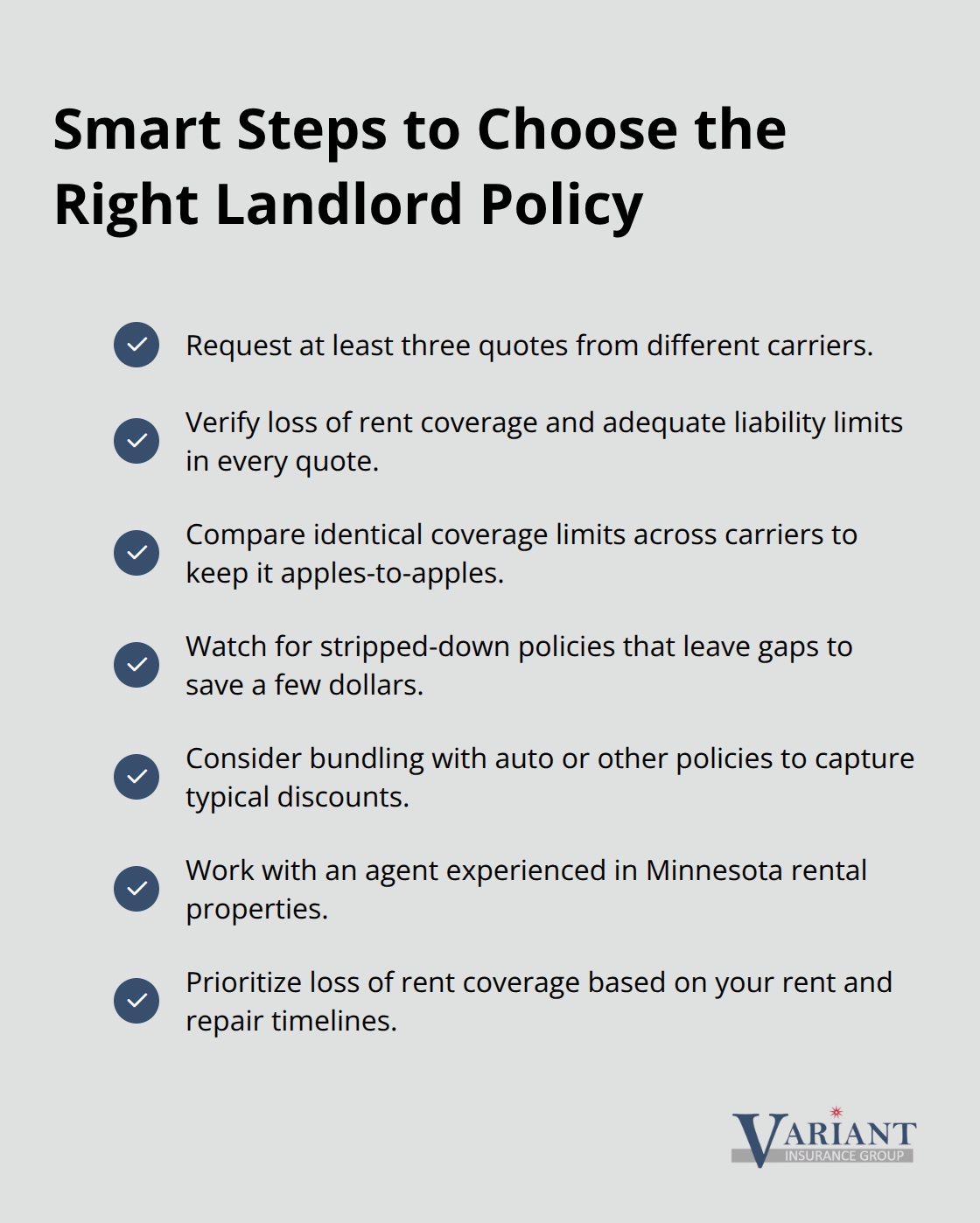

Request at least three quotes from different carriers before you make any decision. The variation in landlord insurance pricing is substantial. A three-bedroom, two-bath single-family rental in Minnesota might cost $800 annually from one carrier and $1,400 from another for identical coverage. Location matters enormously here. According to Steadily, sample Minnesota quotes in 2025 ranged from around $396 annually in Fulda to $787 in Duluth, reflecting local weather risks and claims history.

When you compare quotes, verify that each one includes loss of rent coverage and adequate liability limits, because some carriers offer stripped-down policies at low prices that leave you exposed. A $400 annual policy might exclude loss of rent coverage entirely, meaning you absorb income loss during repairs. A $900 policy with loss of rent included actually costs less in total risk exposure. Request quotes that include the same coverage limits across carriers so you’re comparing apples to apples.

Many agents will bundle your rental property policy with auto or other insurance, which typically generates discounts of ten to fifteen percent.

Work with an Agent Who Understands Rental Properties

Select an agent who owns rental properties themselves or has extensive landlord insurance experience, because this expertise directly impacts your coverage quality. An agent unfamiliar with rental properties might recommend standard homeowners coverage with a rental endorsement, which provides inadequate protection, or might miss critical coverage options for your specific situation. If you own a short-term rental like an Airbnb property, you need an agent who understands that traditional landlord policies often exclude frequent guest turnover. Vacation rentals require different coverage entirely.

Ask potential agents about their experience with investment properties in Minnesota, what coverage gaps they commonly see, and how they handle claims for rental properties. A knowledgeable agent will ask you detailed questions about your tenant screening process, lease terms, and maintenance standards, because these factors influence both pricing and appropriate coverage limits. They’ll also explain why loss of rent coverage matters for your specific property and recommend liability limits based on your property value and location. If you own multiple rental properties, an agent with experience managing portfolios can often negotiate better rates across your entire book of business.

Prioritize Loss of Rent Coverage

Loss of rent coverage separates adequate landlord insurance from inadequate protection. This coverage reimburses your rental income if a covered event makes the property uninhabitable during repairs. In Minnesota, where a typical single-family rental generates $1,500 to $2,500 monthly, three months of vacancy costs between $4,500 and $7,500 in lost income. If a pipe freeze damages your property in January and repairs take eight weeks, loss of rent coverage pays your expected rental income while contractors work. Without this protection, you absorb the full income loss while also paying repair costs.

The Connecticut duplex example near Yale University illustrates this reality: with $3,200 monthly rent and a replacement cost of $480,000, the annual landlord insurance premium was approximately $1,720, with loss of rent coverage contributing meaningfully to that cost. That investment protects six months of income worth $19,200. The math favors including loss of rent coverage rather than gambling that nothing will happen.

Final Thoughts

Standard homeowners insurance for investment property leaves you financially exposed when tenant-related incidents occur. Loss of rental income during repairs, liability claims from tenant injuries, and property damage from negligence all fall outside standard homeowners coverage. You need landlord insurance specifically designed to handle these risks, and the right policy depends on your specific property characteristics, location, and rental model.

Proper investment property insurance protects both your physical asset and your rental income stream. Loss of rent coverage prevents you from absorbing months of lost income while repairs happen, and liability protection shields you from medical and legal expenses when tenants or guests are injured on your property. Coverage for tenant-caused damage means you avoid personally funding repairs from kitchen fires or water damage caused by renter negligence.

At Variant Insurance Group, we help Minnesota property owners find the right insurance solutions for their rental investments. Contact us to discuss your homeowners insurance for investment property needs, and we’ll help you build a policy that protects your financial investment.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation