Minnesota rental property owners face unique risks that standard homeowners insurance won’t cover. Property damage, tenant injuries, and lost rental income can create significant financial exposure.

We at Variant Insurance Group see landlords struggle with coverage gaps that leave them vulnerable. Landlord insurance for rental property provides the specialized protection Minnesota property owners need to safeguard their investments.

What Landlord Insurance Covers

Property Damage Protection Extends Beyond Basic Homeowners Coverage

Landlord insurance protects your rental property’s physical structure from fire, storm damage, theft, and vandalism. The Insurance Information Institute reports that dwelling coverage typically ranges from $480,000 to over $1 million based on property value. Minnesota landlords face specific weather risks such as hail damage and ice dams that can cost $15,000 or more in repairs.

Your policy covers the building itself, attached structures like garages, and landlord-owned appliances or fixtures. Standard coverage excludes flood damage, which requires separate flood insurance through the National Flood Insurance Program.

Liability Coverage Shields You From Expensive Lawsuits

Liability protection covers legal fees and medical expenses when tenants or visitors suffer injuries on your property. Minnesota landlords should carry $500,000 to $1 million in liability coverage due to rising lawsuit settlements. The National Association of Insurance Commissioners found that slip-and-fall claims average $33,000 in medical costs alone.

This coverage also protects against property damage claims (such as a tenant’s car damaged by falling tree branches from your property). Legal defense costs alone can exceed $50,000 even when you win the case.

Loss of Rental Income Coverage Maintains Cash Flow During Repairs

Loss of rental income protection compensates for lost rent when your property becomes uninhabitable due to covered damage. Minnesota’s average rental income loss claims last 3-4 months during major repairs. If your $2,000 monthly rental unit suffers fire damage that requires six months of repairs, this coverage pays $12,000 in lost income.

The coverage typically includes additional expenses if you need temporary housing while repairs occur (making it invaluable for owner-occupied duplexes). This protection becomes even more important when you consider how landlord insurance differs from standard homeowners policies.

Key Differences Between Landlord and Homeowners Insurance

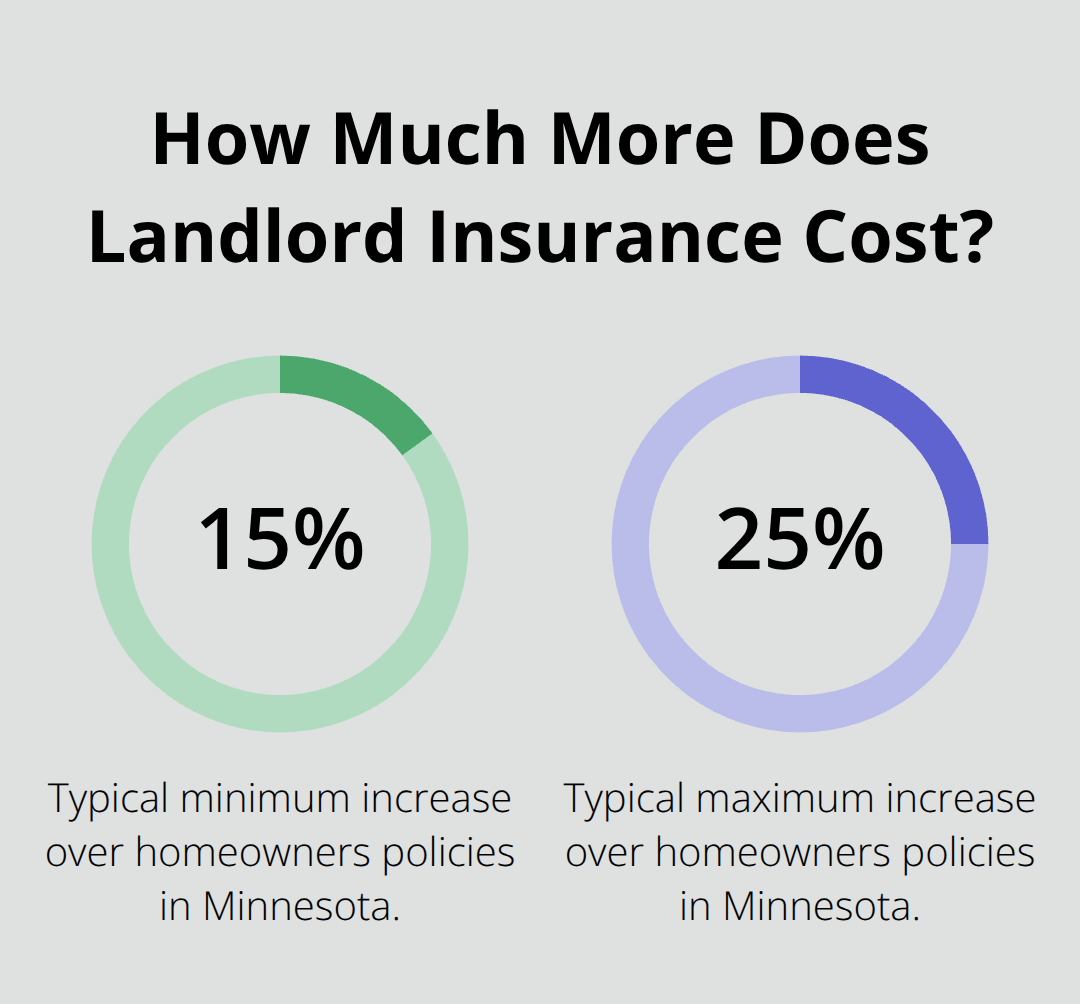

Standard homeowners insurance fails Minnesota rental property owners because it excludes rental-specific risks that generate the most expensive claims. The Insurance Information Institute reports landlord insurance costs 15% to 25% more than homeowners policies, but this premium increase reflects coverage gaps that could cost you tens of thousands without proper protection.

Rental Income Protection Changes Everything

Homeowners insurance never covers lost rental income, but landlord policies include this protection as standard coverage. Minnesota landlords lose an average of $8,000 during major repair periods when units become uninhabitable. A duplex that generates $3,000 monthly rental income faces $18,000 in lost revenue during a six-month storm damage repair.

Loss of rental income coverage pays these costs while homeowners insurance leaves you completely exposed. This coverage becomes essential for Minnesota property owners who depend on rental cash flow.

Higher Liability Limits Reflect Tenant Risk Reality

Landlord policies automatically include higher liability limits because tenant-occupied properties generate three times more injury claims than owner-occupied homes. Minnesota landlords need $1 million liability coverage minimum due to slip-and-fall settlements that average $47,000 statewide.

Multiple tenants, guests, and service providers increase your exposure exponentially compared to single-family homeowner scenarios. Standard homeowners policies cap liability at $300,000, which won’t cover legal defense costs that exceed $75,000 for serious injury claims. These higher limits protect you when rental property accidents result in expensive lawsuits.

Property Damage Coverage Addresses Rental-Specific Risks

Landlord insurance covers property damage scenarios that homeowners policies exclude or limit. Tenant-caused damage beyond normal wear and tear receives coverage under landlord policies (while homeowners insurance typically excludes tenant damage entirely). Minnesota rental properties face increased vandalism and theft risks that require specialized coverage terms.

The coverage also extends to landlord-owned appliances and fixtures that tenants use daily. When these items break down or suffer damage, landlord insurance replaces them while homeowners policies may not cover items used by non-family members. These differences become critical when you examine the specific factors that affect your insurance costs in Minnesota.

Factors That Affect Landlord Insurance Costs in Minnesota

Property Age and Construction Type Set Your Base Premium

Minnesota landlords with older properties face significantly higher insurance costs, with multifamily owners experiencing a 45% increase in premiums from 2023-2024 due to outdated electrical systems, plumbing, and old building materials. The National Association of Insurance Commissioners found that homes built in the 1960s generate twice as many claims as properties constructed after 2000.

Single-family rentals typically cost $800 to $1,200 annually while multi-unit properties range from $1,500 to $3,000 per unit based on age and construction materials. Frame construction costs less to insure than brick or stone structures, but Minnesota’s harsh winters make masonry construction more durable against freeze-thaw cycles that damage foundations and exterior walls.

Location and Crime Rates Drive Premium Calculations

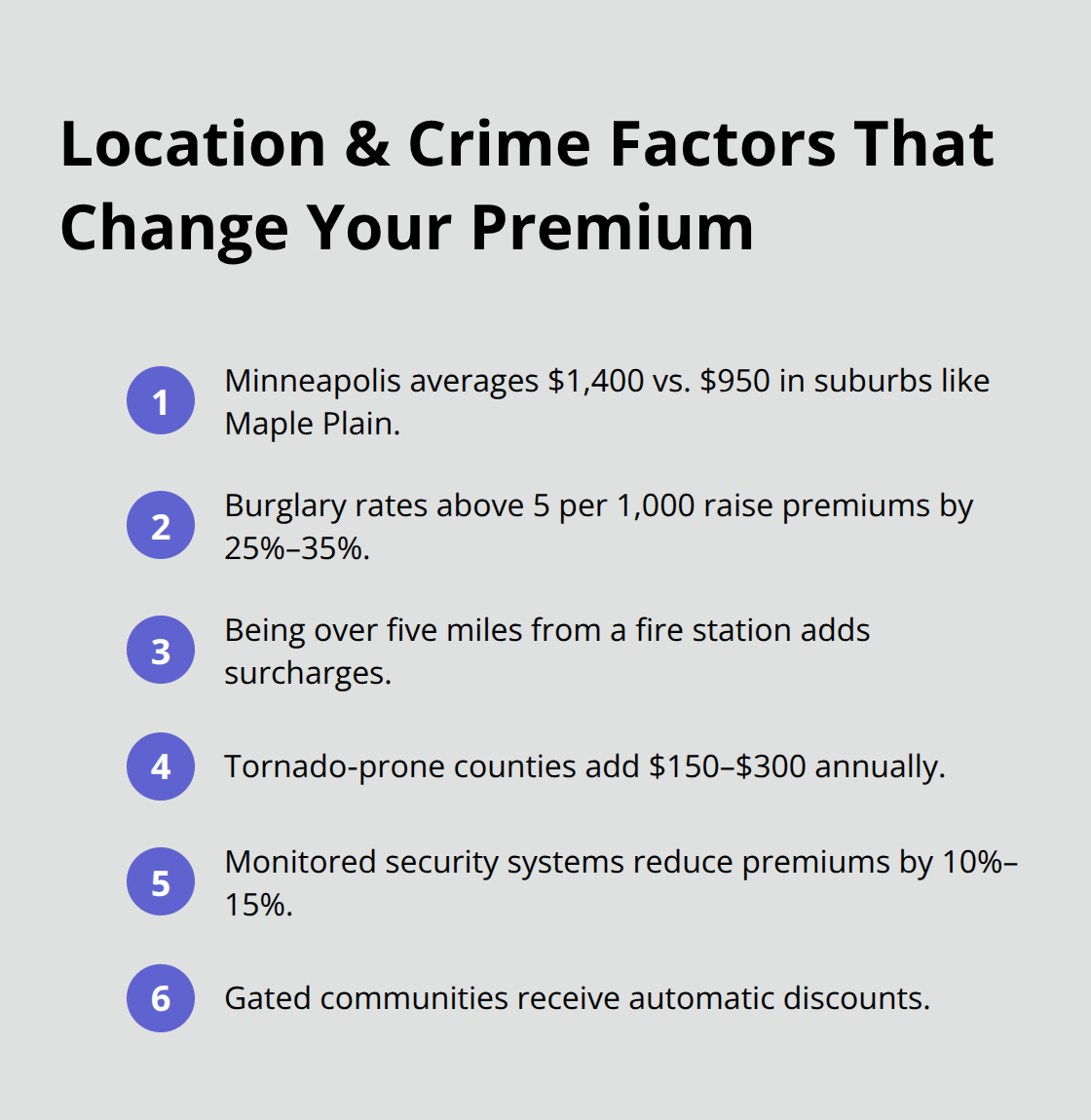

Minneapolis landlords pay average premiums of $1,400 annually compared to $950 in suburban areas like Maple Plain due to property crime rates that exceed state averages by 40%. The FBI’s Uniform Crime Reporting data shows that rental properties in neighborhoods with burglary rates above 5 per 1,000 residents face premium increases of 25% to 35%.

Properties located more than five miles from fire stations pay additional surcharges. Minnesota counties with higher tornado activity like Carver and Wright see weather-related premium adjustments that add $150 to $300 annually. Monitored security systems reduce premiums by 10% to 15% in high-crime areas, while properties in gated communities receive automatic discounts.

Tenant Stability and Unit Count Multiply Your Risk Profile

Landlords with stable, long-term tenants who stay three years or longer receive premium discounts of 10% to 20% because tenant turnover correlates directly with property damage claims. Properties with four or more units require commercial landlord policies that cost 40% more per unit than residential coverage due to increased liability exposure from multiple tenants and common areas.

The Insurance Information Institute reports that landlords who require tenant background checks and maintain occupancy rates above 95% qualify for preferred rates. Short-term rental properties face premium surcharges of 25% to 50% because frequent tenant turnover increases vandalism and theft claims by 60% compared to traditional leases (making stable tenants a valuable asset for premium control).

Final Thoughts

Landlord insurance for rental property offers Minnesota property owners protection that standard homeowners policies cannot provide. The specialized coverage addresses rental income losses, higher liability limits, and tenant-related property damage that make this insurance essential for anyone who rents property in Minnesota. These coverage differences protect your investment from financial risks that could otherwise devastate your rental business.

Independent agents provide access to multiple insurance companies and competitive rates across Minnesota’s insurance market. We at Variant Insurance Group compare policies from top-rated carriers to find coverage that matches your specific rental property needs. Our team evaluates the unique risks Minnesota landlords face and identifies policies that maximize protection while controlling costs.

Property owners need to assess their specific risks and coverage requirements before selecting a policy. An experienced independent agent who specializes in rental property insurance can review your options and secure appropriate protection. The right coverage protects your investment from unexpected losses that could otherwise create serious financial hardship (especially during Minnesota’s harsh weather seasons).