Running multiple vehicles in Minnesota means juggling complex insurance decisions that directly impact your bottom line. Auto fleet insurance in Minnesota requires understanding what coverage you actually need, how to cut unnecessary costs, and when to adjust your policies as your business grows.

At Variant Insurance Group, we’ve helped countless fleet operators navigate these decisions with clarity. This guide walks you through the essentials so you can protect your vehicles and drivers without overpaying.

What Fleet Insurance Actually Covers in Minnesota

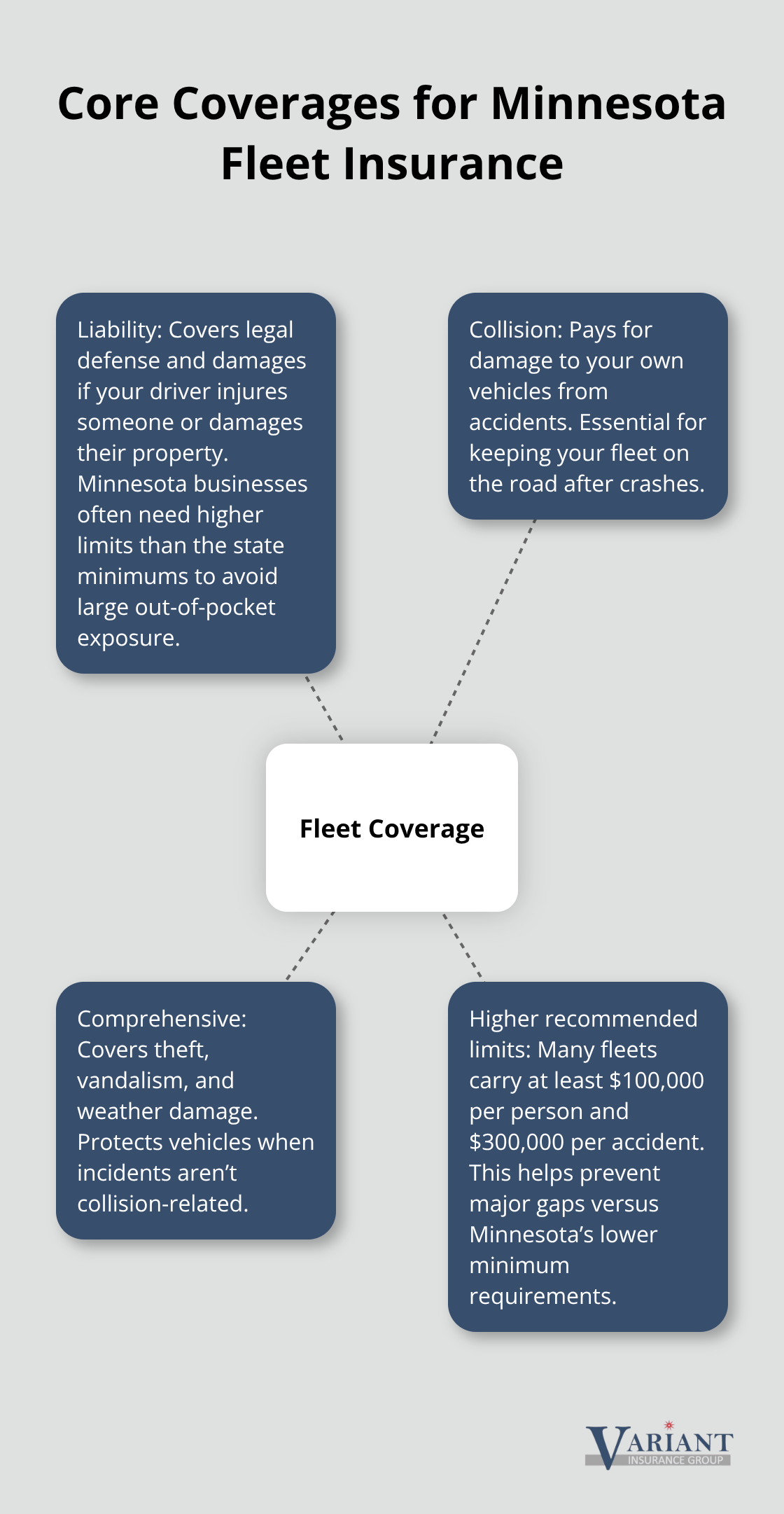

Fleet insurance in Minnesota consolidates multiple business vehicles under one policy, which differs fundamentally from stacking personal auto policies on top of each other. Commercial fleet policies cover liability (legal defense and damages if your driver injures someone or damages their property), collision (damage to your own vehicles from accidents), and comprehensive (theft, vandalism, weather damage). Minnesota’s minimum liability requirement stands at $30,000 per person and $60,000 per accident for bodily injury, plus $10,000 for property damage. However, these minimums expose most businesses to serious financial risk. A single serious injury claim can easily exceed $60,000, leaving your personal assets vulnerable.

Commercial fleets should carry at least $100,000 per person and $300,000 per accident in liability coverage-roughly double the state minimum. The difference matters: if an accident causes $150,000 in injuries and your policy maxes out at $60,000, you personally owe the remaining $90,000.

The Coverage Gap Personal Policies Create

Personal auto policies explicitly exclude business use, which means if your employee uses a personal vehicle for work deliveries and causes an accident, that person’s personal policy won’t cover it. This gap forces the claim onto your business, creating liability exposure you didn’t anticipate. A delivery business that occasionally rents a van for peak season, or a contractor whose crew uses personal vehicles for client visits, faces this exact problem. Fleet policies cover rented and non-owned vehicles your employees use for business-protection that personal policies do not provide. Minnesota regulators tightened requirements in 2026 for proof of insurance and driver safety records, with penalties including fines or license suspensions for noncompliance. A St. Paul delivery company had to overhaul its entire portfolio to meet new state rules after operating with insufficient coverage.

Additional Protections Fleet Policies Offer

Optional add-ons like uninsured motorist coverage and personal injury protection become critical when your drivers regularly encounter high-risk traffic. Minnesota operates under a no-fault system and requires a minimum Personal Injury Protection of $40,000, meaning your drivers’ medical bills get paid regardless of fault. Fleet policies also cover permanently attached equipment-a generator on a service truck, storage units on a utility vehicle-which personal policies exclude. Commercial fleet premiums in the Midwest rose approximately 8% from 2024 to 2026, making proactive risk management more important than ever.

Why This Matters for Your Bottom Line

A $50-per-month savings from using personal policies evaporates instantly after one uninsured claim. The cost difference between adequate fleet coverage and inadequate personal policies pales in comparison to the financial exposure you face. Understanding what your fleet actually needs sets the foundation for making smart coverage decisions. Next, we’ll examine the specific strategies that reduce your insurance costs without sacrificing the protection your business requires.

How to Cut Fleet Insurance Costs Without Cutting Corners

Driver Safety Programs Deliver Real Savings

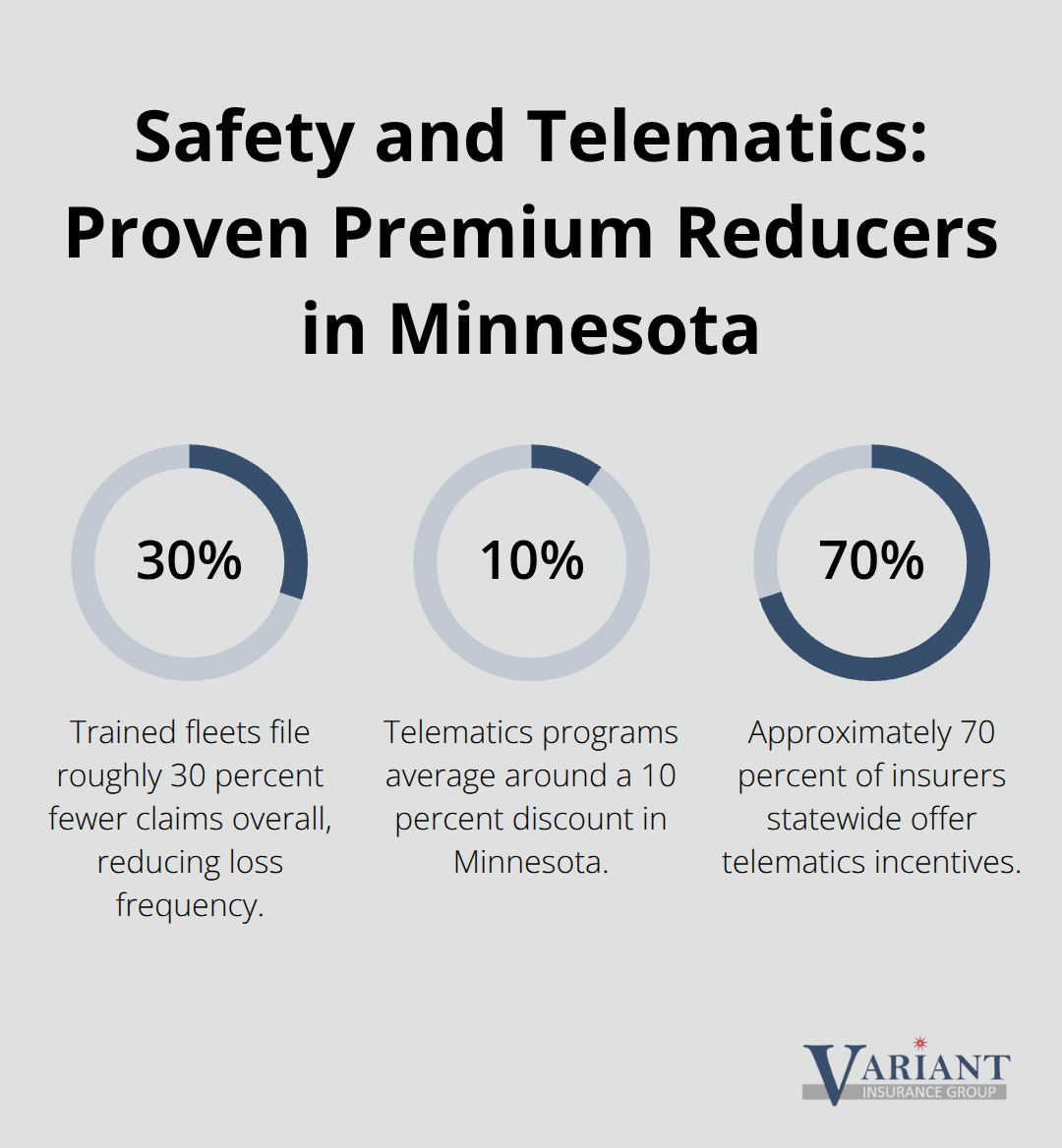

Driver safety programs produce measurable results that insurers reward with premium reductions. Comprehensive training cuts accident rates, and trained fleets file roughly 30 percent fewer claims overall. Minnesota fleets that implement defensive driving courses see tangible improvements in claim frequency, which directly lowers your renewal rates. Progressive, the No. 1 commercial auto insurer per NAIC 2024 data, offers telematics discounts averaging around 10 percent in Minnesota, with approximately 70 percent of insurers statewide now providing telematics incentives.

These programs track speed, braking, and acceleration patterns, giving you visibility into driver behavior while rewarding safer operators through lower premiums. The investment in monitoring equipment pays for itself quickly.

Maintenance Records Lower Your Risk Profile

Vehicle maintenance represents another direct path to cost reduction. Regular preventive maintenance lowers accident risk and claim frequency, and insurers recognize this through better pricing. A fleet that documents maintenance thoroughly can justify lower premiums because the insurer sees reduced risk of mechanical failure leading to accidents. Maintenance records also protect you during claim disputes by demonstrating that a vehicle was properly maintained when an incident occurred.

Bundling and Shopping Unlock Substantial Savings

Bundling multiple policies generates substantial savings. Combining fleet auto with property coverage typically yields discounts of 12 to 18 percent depending on your mix, and paying your premium in full can save an additional 13 percent or more. Annual shopping matters more than loyalty to a single carrier. Roughly 60 percent of Minnesota fleets that compare quotes yearly find better rates, and one Minnesota business saved $8,000 by switching to a provider with more favorable terms.

Deductible Strategy Shapes Your Bottom Line

Higher deductibles reduce premiums significantly, sometimes saving around $2,000 annually, though you must ensure your cash flow can handle the out-of-pocket costs if multiple claims occur. Evaluate your claims history and financial position before raising deductibles-a fleet with frequent minor incidents should maintain lower deductibles, while a fleet with clean records can safely absorb higher out-of-pocket costs. These cost-reduction strategies work best when combined with a thorough understanding of your coverage needs and regular policy reviews that align with your fleet’s growth and changing risk profile.

Working With Your Insurance Agency to Optimize Coverage

Schedule Regular Policy Reviews Throughout the Year

Annual policy reviews are non-negotiable if you want to stay protected and competitive on pricing. Most Minnesota fleet operators review coverage only when renewal notices arrive, which means they miss opportunities to adjust limits, add vehicles, or drop unnecessary add-ons before premiums spike. A quarterly audit of your fleet inventory-VINs, usage patterns, driver assignments-helps catch coverage gaps before accidents happen. This practice ensures your company vehicles are properly documented and protected.

If you added three new delivery vans in March but didn’t notify your insurer until June, those vehicles operated uninsured for three months. One accident during that gap leaves your business personally liable for the entire claim. Schedule reviews in January, April, July, and October to align with seasonal business changes. During these reviews, ask your agent whether your liability limits still match your exposure, whether your deductible strategy still makes sense given your claims history, and whether new coverage options emerged that could reduce your total cost.

Minnesota Department of Commerce resources and MnDOT updates occasionally introduce new regulatory requirements that affect coverage needs, so staying informed protects you from compliance penalties like fines or license suspensions that can reach $10,000 after state audits.

Document Every Accident and Claim With Precision

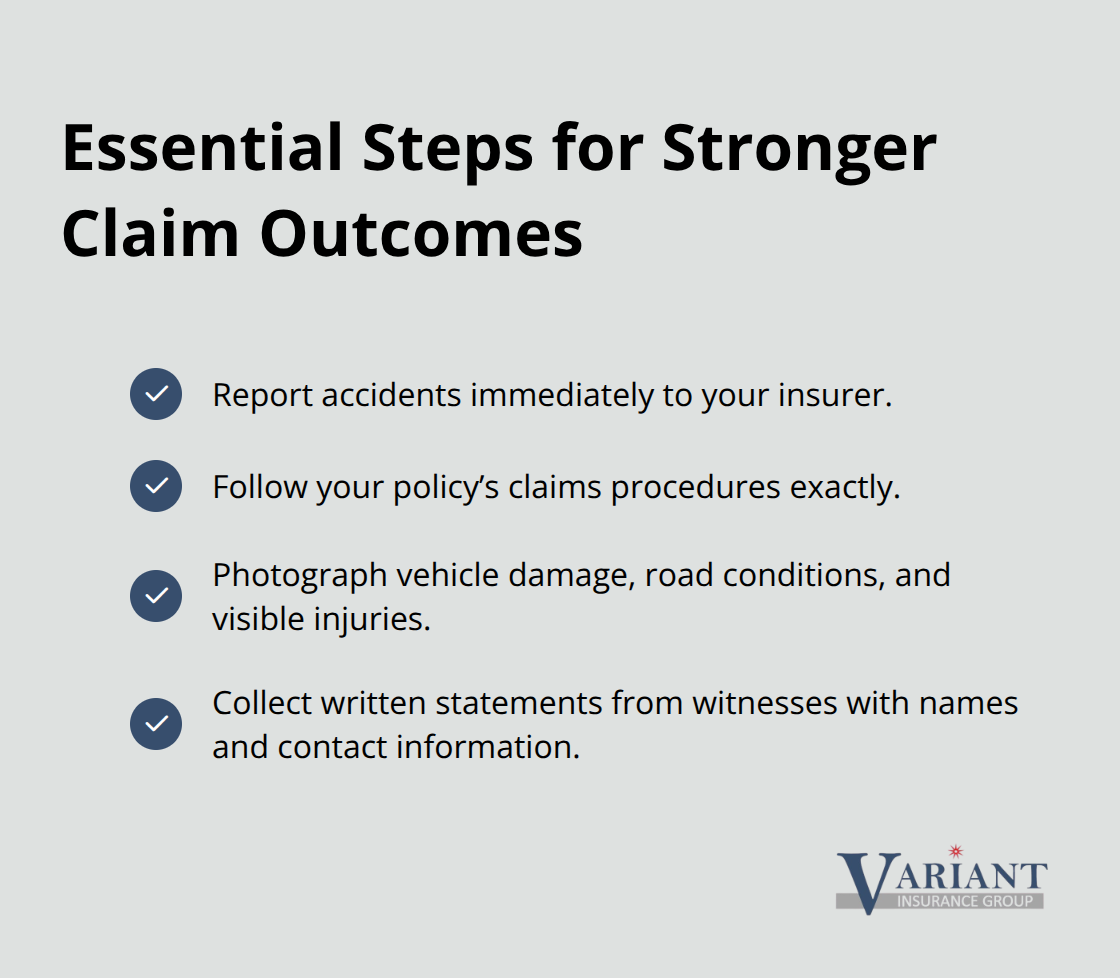

When claims occur, documentation determines whether you recover fully or absorb costs personally. Report accidents immediately to your insurer and follow your policy’s claims procedures exactly, even if they seem redundant. Photograph vehicle damage, road conditions, and visible injuries at the scene. Collect written statements from witnesses, including their names and contact information, rather than relying on memory later.

For commercial claims, document business context-was the driver on an authorized route, performing job duties, carrying cargo within policy limits. If your policy excludes hazardous materials but a driver was transporting restricted cargo, an undocumented detail transforms a covered claim into a denied one. Digital submission tools and 24/7 claims support available through most carriers enable roughly 40 percent faster recovery when you organize information beforehand.

Maintain Records That Prove Your Safety Standards

Keep maintenance records, driver training certificates, and vehicle inspection reports accessible so you can prove you maintained proper standards if a claim is disputed. An insurer investigating a collision wants to see that your fleet follows safety protocols, and documentation proves it. Local Minnesota insurers often handle claims faster than national carriers because they understand regional risks and maintain relationships with local repair shops, which accelerates vehicle recovery and minimizes downtime for your business.

Final Thoughts

Managing auto fleet insurance in Minnesota requires you to understand what coverage protects your business, actively reduce costs through proven strategies, and maintain a partnership with an insurance professional who knows your operation. Minnesota’s minimum liability limits leave most fleets dangerously exposed, and personal auto policies create coverage gaps that cost tens of thousands of dollars after a single accident. Adequate fleet coverage, combined with driver training programs and regular maintenance, reduces both your risk and your premiums.

Shopping annually, bundling policies, and optimizing deductibles save thousands without sacrificing protection. Quarterly inventory audits and meticulous claim documentation ensure you recover fully when incidents occur. Your insurance agency should function as a strategic partner, not just a vendor-they review your coverage annually, alert you to regulatory changes, and help you adjust limits as your fleet grows.

Contact Variant Insurance Group today to discuss your auto fleet insurance in Minnesota and discover how much you could save. Our team shops Minnesota’s top-rated carriers to find the coverage and pricing that match your exact fleet needs. We’re here to answer questions, handle claims, and ensure your fleet operates with confidence.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation