Small businesses in Minnesota face unique challenges when protecting their company vehicles. Commercial auto insurance for small business provides essential coverage that personal policies simply can’t match.

At Variant Insurance Group, we see firsthand how proper commercial coverage protects business assets and prevents costly gaps in protection. The right policy shields your company from liability claims while keeping operations running smoothly.

Understanding Commercial Auto Insurance Requirements

Minnesota law mandates specific commercial auto insurance requirements that differ significantly from personal coverage. Business vehicles must carry minimum liability limits of $30,000 for bodily injury per person, $60,000 for bodily injury per accident, and $10,000 for property damage according to state regulations. These minimums represent the bare legal requirement, but most businesses need substantially higher limits to protect against today’s lawsuit costs.

Personal vs Commercial Coverage Differences

Personal auto policies exclude business use coverage entirely. The moment an employee uses a personal vehicle for business deliveries, client visits, or supply runs, personal insurance becomes void for that trip. Commercial policies cover vehicles that the business owns, employee-owned vehicles used for work, and hired or borrowed vehicles during business operations. Commercial auto insurance policies have higher liability limits, for example $1 million, which reflects their broader coverage scope compared to personal policies.

When Commercial Coverage Becomes Mandatory

Any business that owns vehicles requires commercial auto insurance immediately upon purchase. However, the requirement extends beyond ownership. Businesses that use personal vehicles for work tasks, transport clients, make deliveries, or carry business equipment need coverage. Construction companies face particularly high risks according to Insurance Information Institute data, with delivery services close behind. Even home-based businesses that occasionally drive to meet clients or pick up supplies should consider hired and non-owned auto coverage to fill protection gaps.

State Penalties for Non-Compliance

Minnesota imposes fines of at least $200 for businesses that operate vehicles without proper commercial auto insurance. The state may also suspend business licenses and require community service. These penalties can disrupt operations and damage business reputation (particularly for companies that depend on vehicle access for daily operations).

The specific coverage types and limits you select will directly impact both your protection level and premium costs.

Types of Commercial Auto Insurance Coverage

Liability coverage forms the foundation of commercial auto insurance, but Minnesota’s minimum requirements leave dangerous gaps. The state mandates $30,000 bodily injury per person, $60,000 per accident, and $10,000 property damage, yet a single serious accident easily exceeds these limits. We recommend $1 million liability coverage as the practical minimum for most businesses. The National Association of Insurance Commissioners shares data on average auto insurance costs, with higher limits adding surprisingly little extra cost compared to the protection they provide.

Comprehensive and Collision Protection

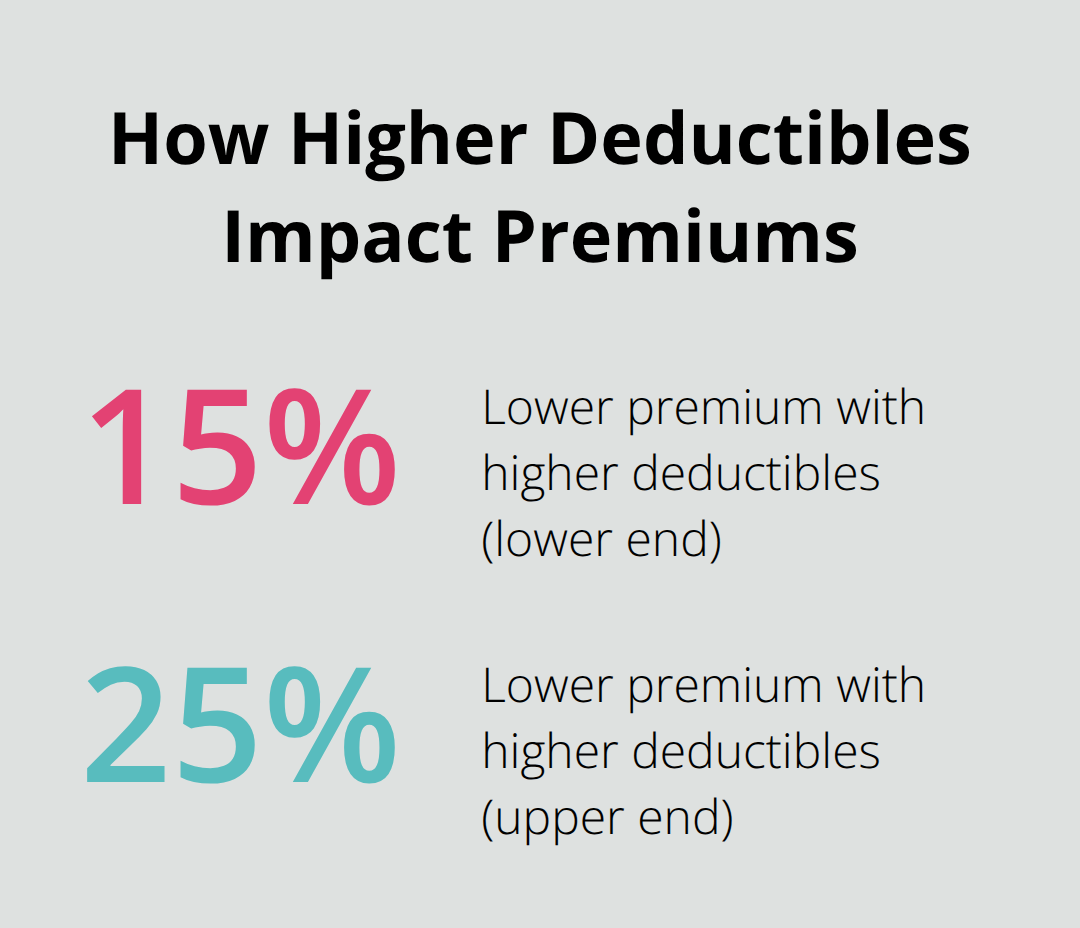

Collision and comprehensive coverage protect your actual vehicle investment, not just liability to others. Collision covers accident damage regardless of fault, while comprehensive handles theft, vandalism, and weather damage. Businesses that operate in Minnesota’s harsh winters need comprehensive coverage specifically for weather-related incidents. The Insurance Information Institute shows construction and delivery companies file the highest claims rates, which makes physical damage coverage non-negotiable for these sectors. Deductibles typically range from $500 to $2,500, with higher deductibles that reduce premiums by 15-25 percent.

Uninsured Motorist Protection

Uninsured motorist coverage becomes vital when 13 percent of Minnesota drivers lack proper insurance according to state data. This coverage protects your business when an at-fault driver cannot pay for damages they cause. The coverage applies to both bodily injury and property damage situations. Medical payments coverage handles immediate medical costs for employees and passengers, regardless of who causes the accident.

Additional Coverage Options

Hired and non-owned coverage protects when employees use personal vehicles for work tasks. Cargo coverage protects goods in transit (particularly important for delivery businesses). Rental reimbursement keeps operations active during vehicle repairs, typically costing $30-50 annually for $40 daily coverage. Fleet tracking systems can reduce premiums by demonstrating active risk management to insurers.

These coverage decisions directly impact your premium costs, which vary based on several business-specific factors that insurers evaluate carefully.

Factors Affecting Commercial Auto Insurance Costs

Commercial auto insurance premiums vary dramatically based on specific business factors that insurers evaluate. Construction companies pay the highest rates according to Insurance Information Institute data, with delivery services close behind. Restaurant delivery drivers face premiums 40-60 percent higher than office workers who occasionally drive to client meetings. Vehicle usage frequency matters more than mileage alone – a plumber who makes 15 service calls daily pays more than a consultant who drives 20,000 miles annually for occasional site visits. High-risk industries like towing, taxi services, and hazardous material transport see premiums increase by 150-300 percent over standard business use.

Driver Records Impact Premium Rates

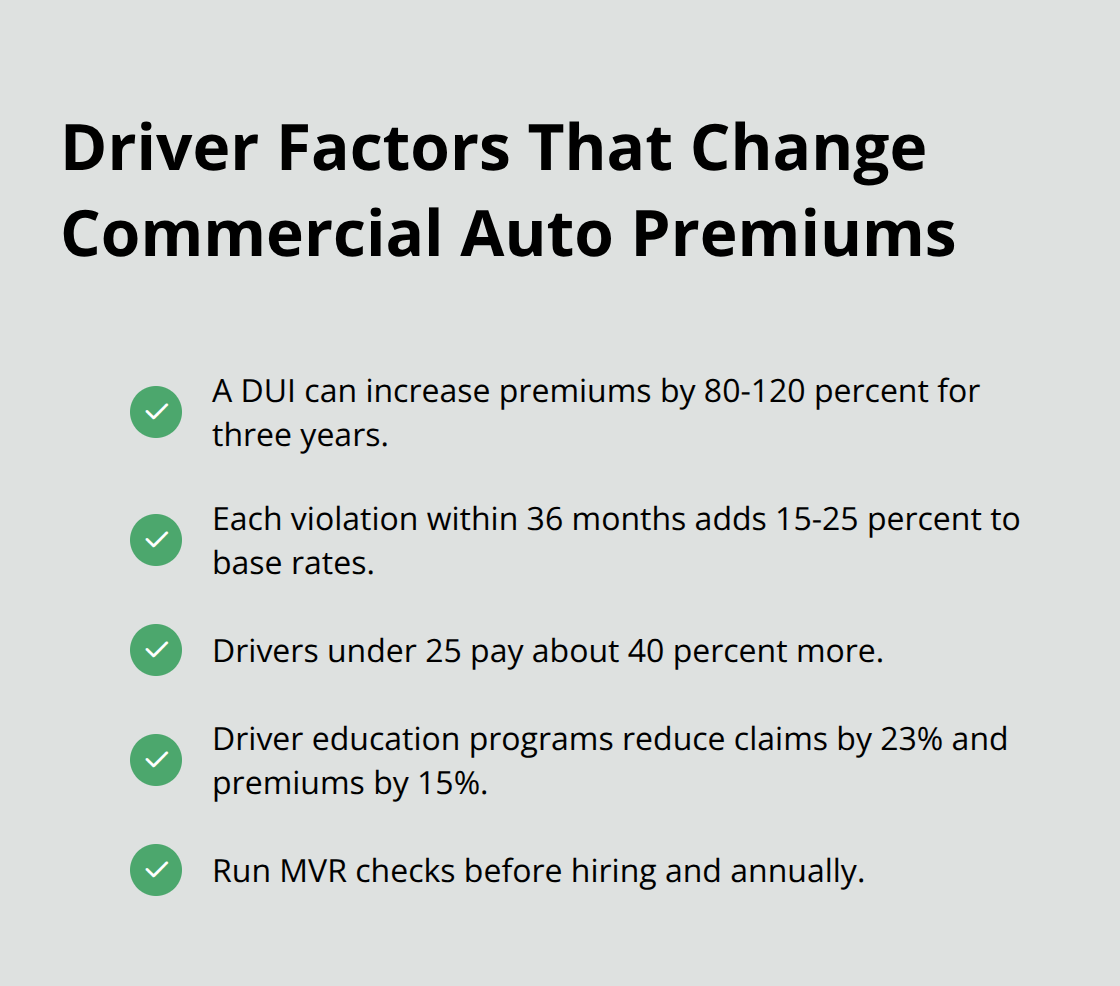

Employee records directly impact your rates, though companies with small premium volume may not be required to report statistics in great detail for general liability coverage. A single DUI conviction increases commercial premiums by 80-120 percent for three years. Each violation within 36 months adds 15-25 percent per incident to your base rate.

Companies with drivers under 25 pay 40 percent higher premiums due to accident statistics. The National Association of Insurance Commissioners shows businesses that implement driver education programs reduce claims by 23 percent and premiums by 15 percent. Motor Vehicle Record checks should happen before you hire and annually thereafter (one bad driver can double your entire fleet’s insurance costs).

Fleet Size Creates Premium Advantages

Businesses with multiple vehicles benefit from significant economies of scale. Single-vehicle operations pay premium rates, while fleets of 5-10 vehicles see 20-30 percent reductions per vehicle. Companies with 25 or more vehicles negotiate custom rates that can cut costs by 40 percent. However, vehicle types matter enormously – when you add one heavy truck to a fleet of sedans, you increase the entire policy cost. Newer vehicles under three years old qualify for safety discounts of 10-15 percent, while vehicles over ten years old face surcharges of 25 percent or higher due to increased breakdown and accident risks.

Vehicle Usage Patterns Determine Risk Levels

Insurers classify business use into distinct categories that affect rates significantly. Local delivery operations face higher premiums than service calls within a 50-mile radius. Companies that transport passengers (like ride services) pay rates 200-400 percent above standard commercial use. Seasonal businesses can adjust coverage during inactive periods to reduce costs by 30-50 percent. Vehicles that carry hazardous materials require specialized coverage that doubles or triples standard premiums due to environmental liability exposure.

Final Thoughts

Small businesses must secure commercial auto insurance for small business the moment they operate any vehicle for work purposes. Evaluate your actual coverage needs beyond Minnesota’s minimum requirements, then gather quotes from multiple carriers to compare both protection levels and costs. Document all business vehicle usage patterns, driver records, and operational risks to provide accurate information during the application process.

Experienced local insurance professionals make this complex process manageable. At Variant Insurance Group, we help Minnesota businesses find the right commercial auto coverage for their specific needs. Our team reviews your options and compares protection and prices to deliver value for your operations.

Commercial auto insurance protects your business investment from potentially devastating financial losses. A single serious accident without proper coverage can bankrupt a small business (while adequate protection keeps operations active). The cost of comprehensive commercial coverage represents a fraction of your potential liability exposure.