Running a construction business in Minnesota means managing more than just projects and crews. General contractor insurance Minnesota protects your business from the financial risks that come with every job site.

At Variant Insurance Group, we know that one accident or equipment loss can threaten your entire operation. The right coverage gives you peace of mind to focus on building.

What You Must Know About Minnesota’s Insurance Laws

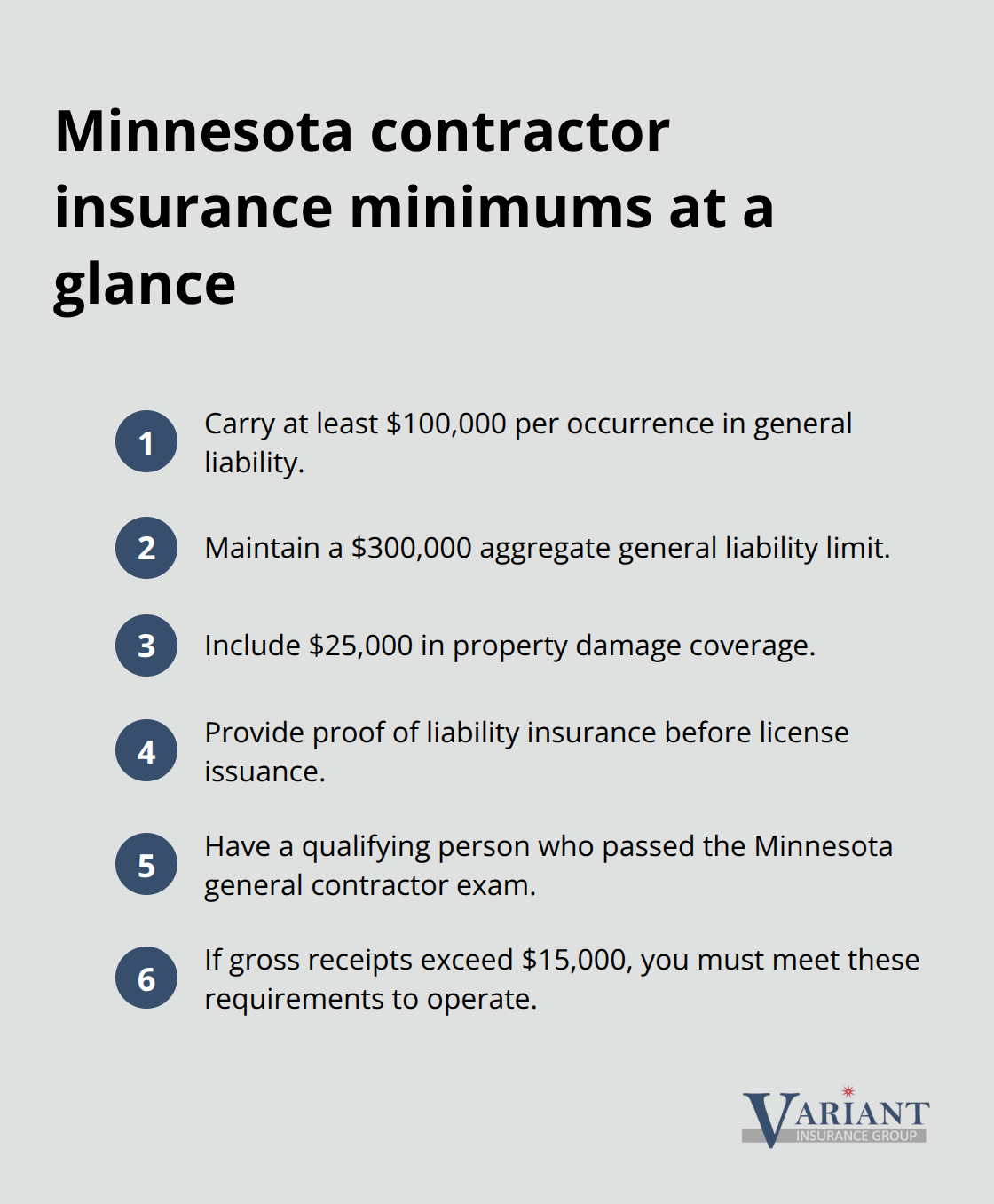

Minnesota’s residential contractor licensing system directly shapes your insurance obligations, and ignoring these rules costs money fast. To operate legally, you need a qualifying person on staff who has passed the Minnesota general contractor exam, and the Minnesota Department of Labor and Industry requires proof of liability insurance before they issue your license. Specifically, you must carry at least $100,000 per occurrence and $300,000 aggregate in general liability coverage, plus $25,000 in property damage protection. These aren’t suggestions-they’re mandatory minimums enforced through license audits and job-site inspections. If your business generates more than $15,000 in gross annual receipts, you cannot legally operate without meeting these requirements.

Minnesota Statute 325E.66 prohibits contractors from paying a homeowner’s insurance deductible or offering anything of value to induce a repair contract. This applies specifically to repairs funded through insurance claims, so your contracts must include written notification about the deductible prohibition in your initial estimate to homeowners. Violations trigger enforcement actions from the Department of Labor and Industry.

How Your Claims History Controls Workers’ Compensation Costs

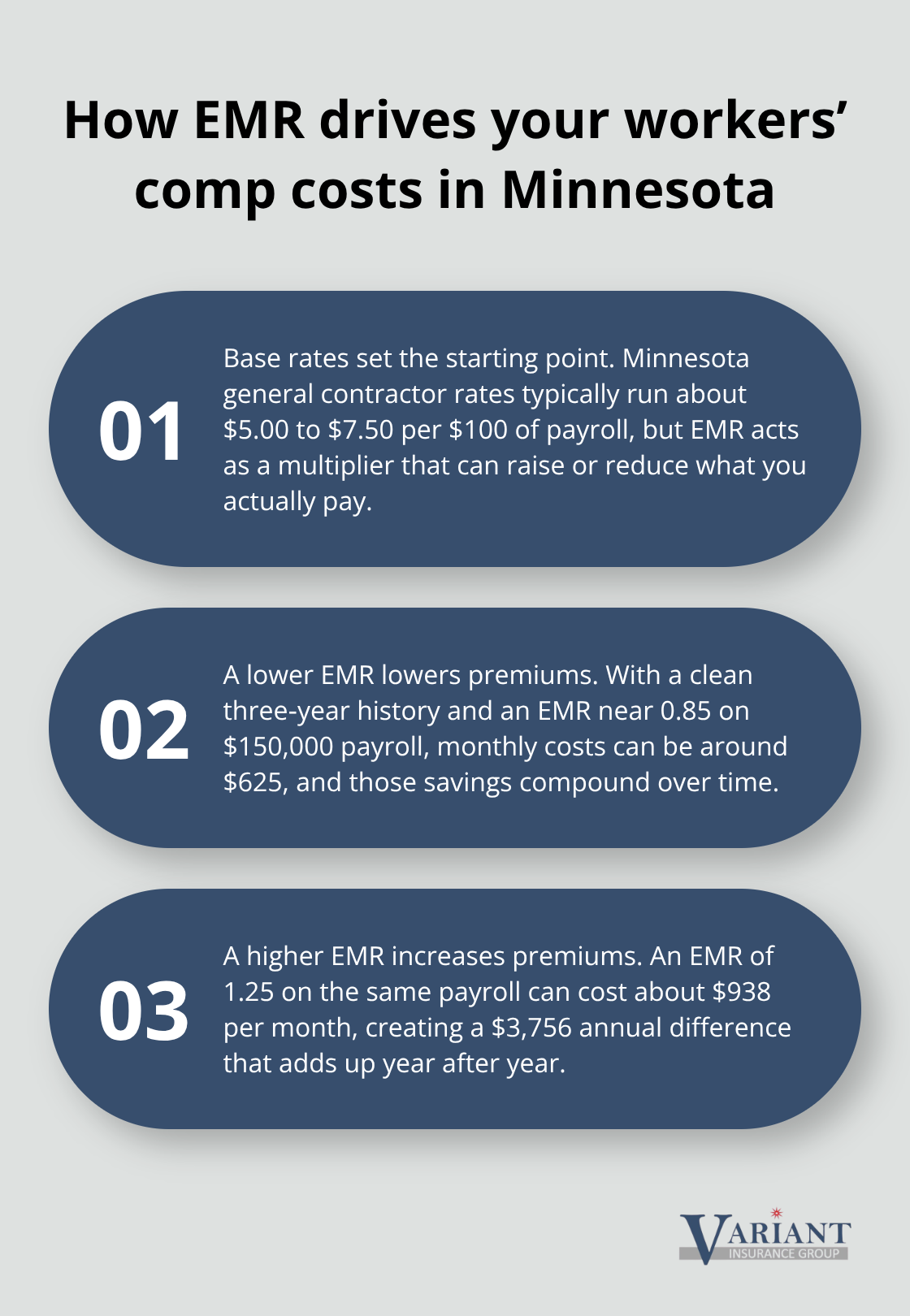

Your Experience Modification Rate, or EMR, is the single most powerful factor controlling what you pay for workers’ compensation insurance. Minnesota base rates for general contractors run about $5.00 to $7.50 per $100 of payroll, but a poor safety record can push your EMR above 1.0, multiplying those costs significantly. A contractor with a clean three-year history and an EMR near 0.85 might pay $625 monthly on a $150,000 annual payroll, while identical payroll with an EMR of 1.25 costs $938 monthly-that $3,756 annual difference compounds over years.

Workplace safety training and incident documentation act as essential business investments that lower your EMR over time. Subcontractor misclassification is actively enforced in Minnesota, and treating independent contractors as employees during a workers’ compensation audit can trigger substantial back-payment charges. Before you hire subcontractors, verify their certificates of insurance to protect yourself from assuming their uncovered payroll at audit time.

Climate-Driven Liability Exposures Across Minnesota

Minnesota’s climate creates distinct job-site risks that standard coverage gaps leave exposed. Winter slip-and-fall claims on icy surfaces, spring water intrusion damage from snow melt, and summer storm exposure all demand specific attention during contract bidding and coverage planning. Standard general liability policies exclude faulty workmanship-damage to work you performed or subcontractors performed-unless you request the CG 22 91 endorsement or similar modifications.

Environmental liability and pollution exposure receive zero coverage under typical contractor policies, yet Minnesota’s soil and water conditions make environmental risk real on many projects. Municipal work and government contracts often require you to name the government entity as an additional insured in writing before work starts, and verbal promises of coverage additions fail in court.

Matching Coverage Limits to Project Risk

High-risk projects exceeding $1 million in value should carry $2 million to $5 million per occurrence limits rather than the $1 million minimum, because Minnesota construction claims regularly exceed $500,000 and defense costs can deplete your limits fast. Your general liability policy pays defense costs outside the policy limits on an occurrence form, which underscores the value of an umbrella or excess liability policy that protects you as claims approach or exceed primary limits. The right coverage limits align with your actual project exposure rather than just the stated contract minimum, and contractual requirements often exceed the mandatory minimums set by the state.

The Coverage Your Minnesota Construction Business Actually Needs

General Liability: Your Foundation Against Job-Site Claims

General liability insurance forms the foundation of contractor protection in Minnesota, but the minimum $100,000 per occurrence and $300,000 aggregate required by the Department of Labor and Industry leaves most builders dangerously exposed. Minnesota construction claims regularly exceed $500,000, meaning a single accident can wipe out your entire policy limit before defense costs are paid. Try carrying at least $1 million per occurrence for residential work under $600,000 and $2 million to $5 million for projects exceeding $1 million in value. Your general liability policy pays defense costs outside the stated limits on an occurrence form, which sounds protective until you realize that a serious injury claim can consume your entire limit while your lawyer’s fees stack on top.

Subcontractor exposure represents your biggest coverage gap because standard policies exclude work performed by subcontractors unless you secure written additional insured endorsements and certificates of insurance before work starts. The CG 22 91 endorsement removes broad faulty workmanship exclusions for subcontracted work, but you must request it in writing during underwriting, not after a claim occurs. An umbrella or excess liability policy adds critical protection that keeps your defense coverage intact as claims approach or exceed your primary limits.

Environmental Liability and Climate-Specific Risks

Environmental liability and pollution exposure receive zero coverage under typical contractor policies, yet Minnesota’s soil and water conditions create real environmental risk on many projects. Winter slip-and-fall claims on icy surfaces, spring water intrusion damage from snow melt, and summer storm exposure all demand specific attention during contract bidding and coverage planning. Standard general liability policies exclude faulty workmanship-damage to work you performed or subcontractors performed-unless you request specific endorsements or modifications.

Workers’ Compensation and Your Experience Modification Rate

Workers’ compensation insurance in Minnesota directly ties to your Experience Modification Rate, which shows how many workers’ comp claims your construction company has compared to others doing similar work. A contractor with a clean three-year history and an EMR near 0.85 pays substantially less than identical payroll with an EMR of 1.25, creating meaningful annual savings that compound over years. Workplace safety training and documented incident procedures act as genuine business investments that lower your EMR over time, and Minnesota actively enforces subcontractor misclassification, meaning treating independent contractors as employees during audit can trigger substantial back-payment charges.

Equipment, Tools, and Vehicle Coverage

Equipment and tools coverage protects your on-site assets from theft and weather damage, with typical inland marine policies costing $300 to $1,200 annually depending on equipment value and location risk. Commercial auto insurance is essential for job-site travel and vehicle use, running $1,800 to $3,500 per vehicle annually in Minnesota, and personal auto policies explicitly exclude business use. Bundling general liability, workers’ compensation, commercial auto, and tools coverage with one carrier typically yields 10 to 20 percent multi-policy discounts, making consolidated coverage both more protective and more affordable than piecemeal policies.

Finding the Right Agent for Your Needs

Independent agents specializing in construction can often identify 15 to 25 percent in premium savings through specialty markets and proper endorsement structuring. An agent who understands Minnesota’s climate risks, licensing requirements, and project-specific exposures can match your coverage limits to actual job-site conditions rather than just checking boxes on a standard form. The difference between adequate coverage and dangerously thin protection often comes down to whether your agent asks the right questions about your subcontractor relationships, equipment values, and project locations before underwriting begins.

Picking an Agent Who Actually Knows Minnesota Construction

Shopping for contractor insurance in Minnesota means rejecting the one-size-fits-all approach that online quote tools and national carriers push. General contractors face climate-specific risks, subcontractor liability gaps, and regulatory requirements that generic policies simply do not address. An agent who has worked with Minnesota builders understands that winter slip-and-fall exposure differs fundamentally from summer storm risk, that municipal projects require written additional insured endorsements before work starts, and that your Experience Modification Rate compounds savings or costs over years.

What to Ask When You Contact an Agent

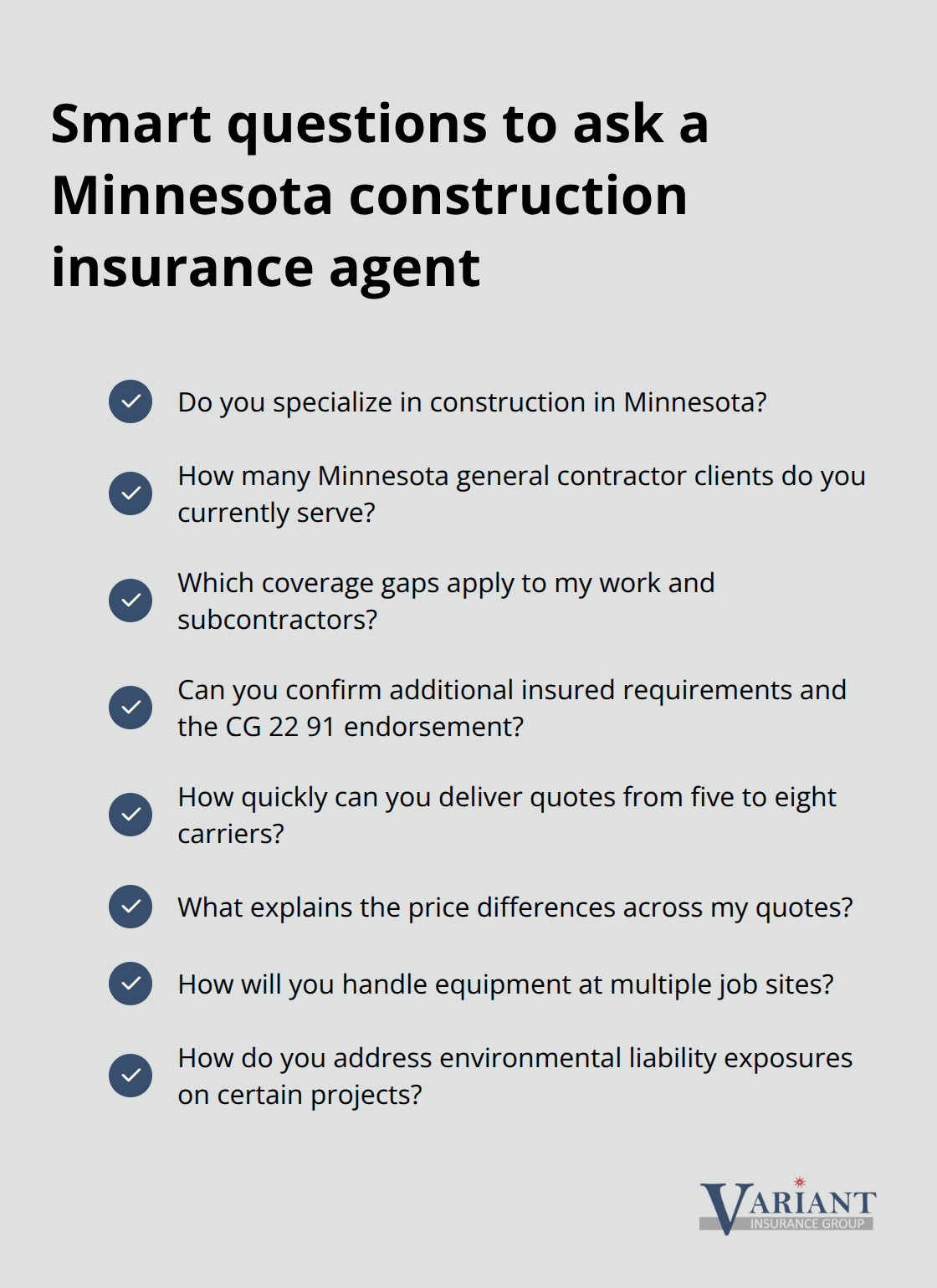

When you contact an agent, ask directly whether they specialize in construction and how many general contractor clients they currently represent in Minnesota. If they cannot name specific coverage gaps that apply to your work-subcontractor exposure, equipment value at multiple job sites, or environmental liability on certain project types-move to the next option. Most independent agents in Minnesota can obtain quotes from five to eight carriers within 48 hours, and you should expect to see meaningful price variation.

Solo operators and small crews often see quotes ranging from $500 to $2,300 annually for general liability depending on claims history and coverage limits, while larger operations with higher payroll face $2,500 to $5,000 or more.

The agent worth your time will explain exactly why quotes differ: one carrier might price workers’ compensation aggressively but charge premium rates for general liability, while another offers tools coverage bundled with GL at a discount. An agent who simply presents the lowest quote without explaining trade-offs between price, coverage limits, deductibles, and endorsements is prioritizing commission speed over your actual protection.

How Deductibles Control Your Monthly Cost

Deductibles directly control your monthly cost, and this is where contractors make expensive mistakes. Raising your deductible from $500 to $1,000 on general liability typically reduces premium by 10 to 15 percent, but only if you can actually cover that deductible from cash reserves when a claim occurs. Construction businesses with tight cash flow should stick with lower deductibles even if monthly payments climb slightly; a $500 deductible you can pay is infinitely better than a $2,500 deductible that forces you to liquidate equipment or delay payroll.

Your agent should also compare whether you need different deductibles for different coverage types-a higher deductible on equipment coverage paired with a lower deductible on general liability often balances cost and protection effectively. Try having your agent run quotes at three different deductible levels so you can see the actual dollar impact before you commit.

Shopping Multiple Agents, Not Just Multiple Carriers

Obtain quotes from at least two or three different agents, not just two or three carriers through a single agent. Different agents have access to different specialty markets and can leverage relationships to secure better pricing or coverage terms. An independent agency shops Minnesota’s top-rated insurance companies to find the right policy for your exact needs, but the principle applies universally: comparing across multiple sources prevents you from overpaying for thin coverage or underpaying for protection that fails when you need it.

Final Thoughts

General contractor insurance in Minnesota protects your business from the financial damage that one accident or equipment loss can inflict. You now understand the state’s mandatory minimums, how your Experience Modification Rate controls workers’ compensation costs, and why coverage limits matter far more than the lowest premium. The gap between adequate protection and dangerously thin coverage comes down to one decision: working with an agent who actually understands Minnesota construction or settling for generic quotes that miss critical exposures.

Contact an independent agency that specializes in construction and ask them to identify the specific coverage gaps in your current operation. If you work with subcontractors, ask whether your policies include written additional insured endorsements and the CG 22 91 endorsement for faulty workmanship. If you operate vehicles on job sites, verify that your commercial auto coverage meets Minnesota’s minimums and that your personal auto policy isn’t being stretched beyond its limits.

At Variant Insurance Group, we shop Minnesota’s top-rated insurance companies to find the right coverage for your exact needs. Our team reviews your options and compares protection and prices so you get genuine value rather than just the lowest quote. Contact Variant Insurance Group today to discuss your general contractor insurance Minnesota needs and discover the difference that specialized construction expertise makes when you need it most.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation