Hosting on Airbnb comes with real financial risk. Property damage, theft, and liability claims can cost thousands of dollars, which is why understanding your Airbnb property protection plan matters.

At Variant Insurance Group, we’ve seen hosts make costly mistakes by relying solely on Airbnb’s built-in coverage. This guide walks you through what’s actually protected, where the gaps are, and how to build a complete insurance strategy.

What Airbnb’s Host Protection Actually Covers

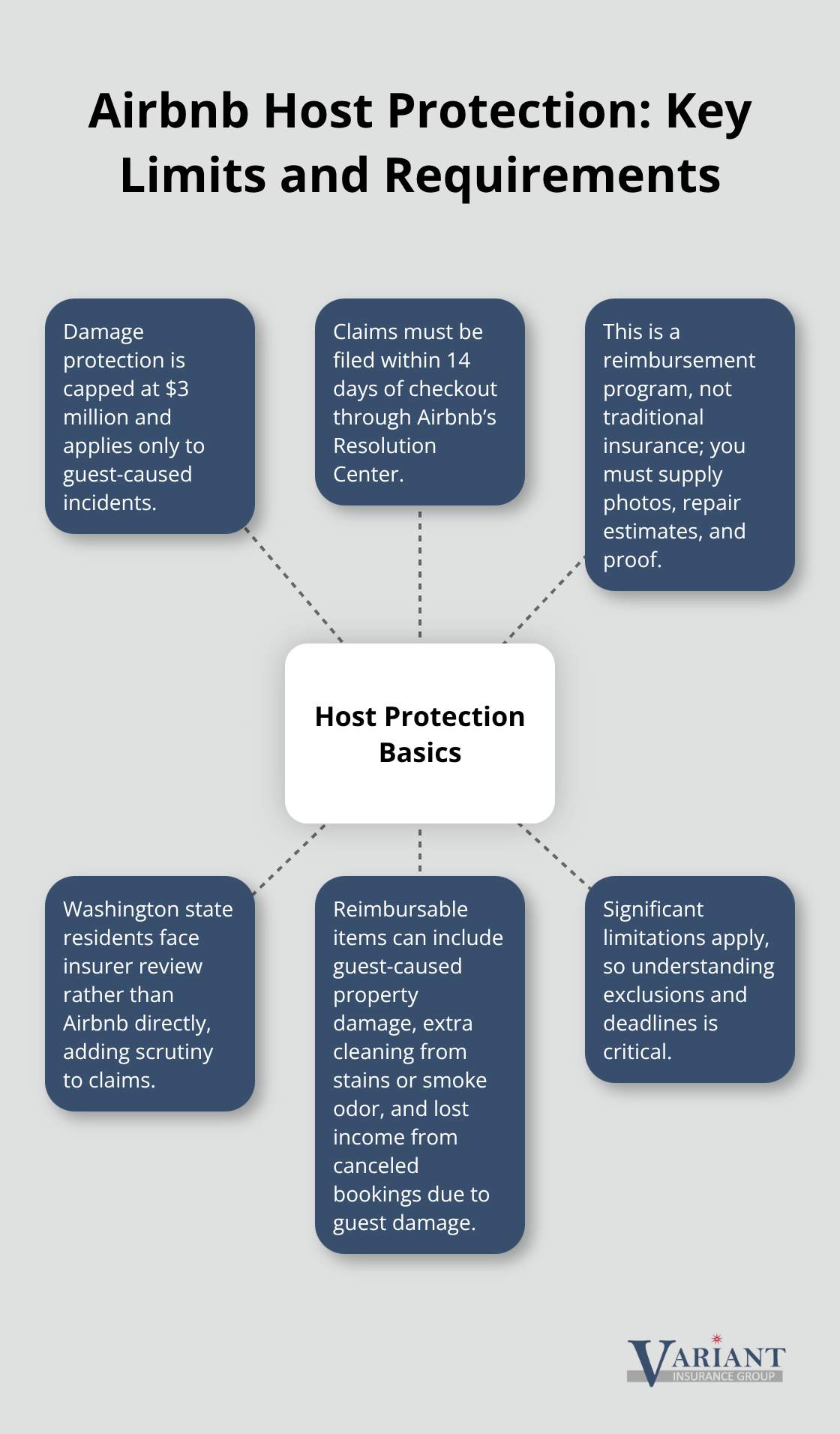

Airbnb’s Host Protection Insurance provides up to $3 million in damage coverage, $1 million in host liability, and $1 million in Experiences liability. The damage protection reimburses you when guests cause property damage, including harm to parked vehicles, extra cleaning costs from stains or smoke odor, and lost income from canceled bookings when guest damage forces closure. However, this protection has significant limitations you need to understand. The $3 million damage limit applies only to guest-caused incidents, and you must file claims within 14 days of checkout through Airbnb’s Resolution Center. In Minnesota, Washington state residents face additional scrutiny, as an insurer reviews their claims rather than Airbnb directly.

The liability coverage of $1 million sounds substantial until you face a serious slip-and-fall injury or a guest’s medical emergency that exceeds that threshold. Airbnb’s protection is not traditional insurance; it’s a reimbursement program that only pays after you document the issue with photos, obtain repair estimates, and submit proof within that tight 14-day window.

What Host Protection Excludes

Airbnb explicitly excludes normal wear and tear, loss of currency, acts of nature, mold, infestations, and cleaning tasks associated with standard checkout. This means if a guest leaves your property filthy, you cannot claim cleaning costs. Intentional damage, pet-related incidents, smoking damage, and theft without forced entry fall outside coverage. The most damaging exclusion for Minnesota hosts is the lack of income replacement for situations where your property becomes uninhabitable from events like a kitchen fire, burst pipe, or severe storm damage. You lose rental income during repairs, and Airbnb’s protection covers repair costs but not the thousands in canceled bookings. Medical payments coverage stops during rental periods, leaving guests with grounds to pursue you directly for injury costs. If a guest refuses to leave and you face eviction proceedings, Airbnb provides no legal support or lost revenue protection.

The Gap Between Platform Protection and Real Insurance

Relying solely on Airbnb’s Host Protection leaves you exposed to catastrophic financial loss. A dedicated short-term rental insurance policy fills these gaps by covering business income loss from covered damages, higher liability limits when needed, and guest theft with forced entry. Proper Insurance, endorsed by Vrbo, offers commercial general liability starting at $1 million with business revenue protection that pays actual loss sustained with no time limits. Their policies cover bed bug and flea infestations, squatters protection for guests refusing to leave, and amenity liability for bikes, kayaks, and hot tubs (coverage that standard homeowners policies typically exclude). For Minnesota hosts specifically, the combination of Airbnb’s $1 million liability plus a supplemental commercial policy with $2 million in additional protection creates genuine safety. Standard short-term rental policies cost between $800 and $2,400 annually for properties valued between $200,000 and $500,000, a reasonable investment against income loss that Airbnb won’t cover.

Your next step involves comparing what specialized short-term rental carriers offer against what you currently have in place.

Why Your Homeowners Policy Won’t Cover Your Airbnb

Standard Homeowners Policies Exclude Rental Activity

Your standard homeowners insurance excludes short-term rental activity entirely. Most carriers in Minnesota explicitly prohibit business use of residential properties, meaning that the moment you list on Airbnb, your policy becomes invalid for guest-related claims. If you file a claim for guest damage or liability without disclosing rental activity to your insurer, the Minnesota Department of Commerce can trigger immediate policy cancellation and claim denial. This exclusion applies regardless of how frequently you rent or how transparent you believe you’ve been with your carrier.

Coverage Limits Fall Short for Guest-Related Risks

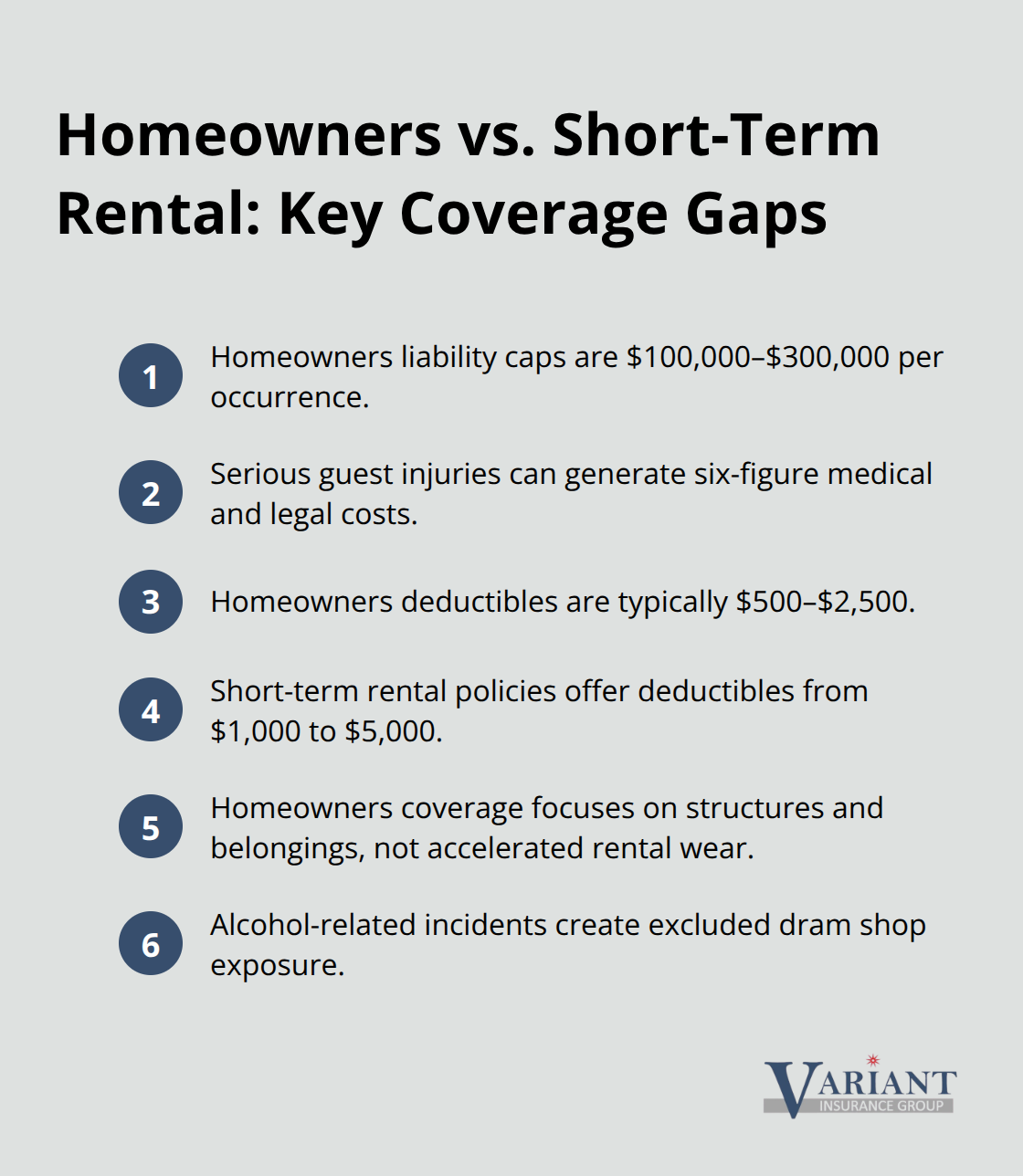

The coverage differences between homeowners and short-term rental policies run deeper than simple exclusions. Homeowners policies cap liability at $100,000 to $300,000 per occurrence, while a serious slip-and-fall injury or food poisoning incident from your kitchen can generate six-figure medical costs and legal fees. Your homeowners deductible typically ranges from $500 to $2,500, but short-term rental policies offer deductible options starting at $1,000 and scaling to $5,000 depending on your risk tolerance.

Property damage coverage under homeowners insurance focuses on permanent structures and personal belongings, not the accelerated wear patterns that short-term rentals create. Guest theft without forced entry isn’t covered by homeowners policies, yet electronics, artwork, and other valuables disappear during short-term stays regularly. Alcohol-related incidents create dram shop liability exposure that homeowners insurers explicitly exclude, leaving you personally liable when a guest drinks at your property and injures someone afterward.

The Real Cost Comparison Surprises Most Hosts

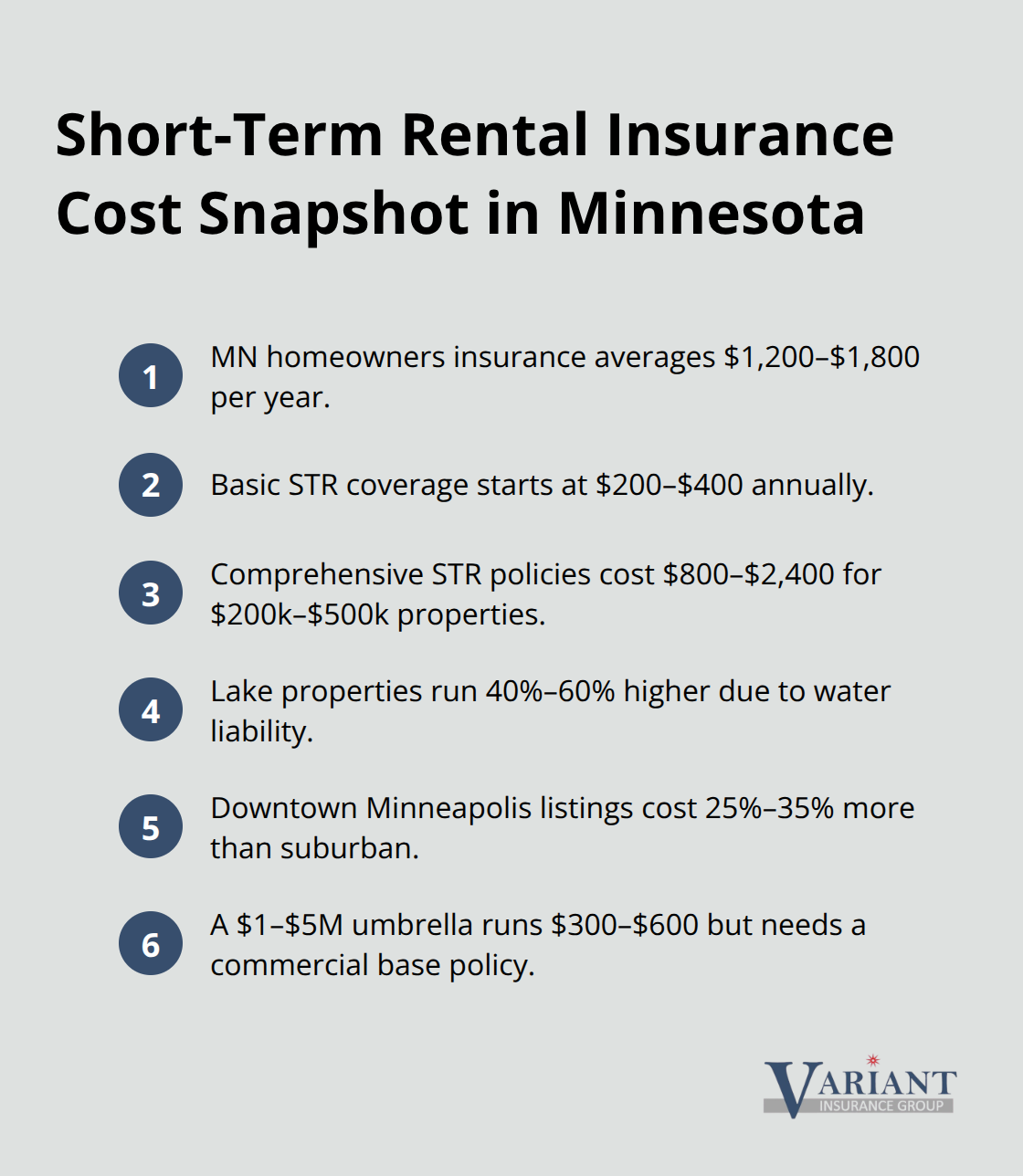

The cost gap between traditional homeowners insurance and specialized short-term rental policies is smaller than most Minnesota hosts expect. Standard homeowners insurance in Minnesota averages $1,200 to $1,800 annually, while basic short-term rental coverage from providers like Proper Insurance starts at $200 to $400 per year for limited protection. Comprehensive short-term rental policies with $1 to $2 million in liability coverage, business income protection, and guest damage coverage cost between $800 and $2,400 annually for properties valued at $200,000 to $500,000.

Lake properties in places like Duluth run 40 to 60 percent higher due to water liability exposure, and downtown Minneapolis properties cost 25 to 35 percent more than suburban listings. A commercial umbrella policy for $1 to $5 million in extra coverage runs $300 to $600 annually but requires attachment to a commercial base policy.

Income Loss Creates the Largest Financial Exposure

The real expense comes from not having income replacement coverage. A single week of canceled bookings during peak season costs $1,500 to $3,000 in lost revenue, and a property-damaging event like a burst pipe can force closure for weeks. Airbnb’s Host Protection covers repair costs but not income loss, meaning you absorb thousands in canceled reservations while paying for repairs. A dedicated short-term rental policy with business income protection pays actual loss sustained from covered claims, protecting your revenue stream when damage forces temporary closure. This income protection transforms your financial stability during property emergencies. Understanding these gaps positions you to make informed decisions about which coverage layers you actually need for your specific situation.

How to Protect Yourself Before Listing on Airbnb

Document Your Property Thoroughly

Start with documentation before your first guest arrives. Photograph every room, closet, appliance, and outdoor space in high resolution, noting the condition of walls, flooring, furniture, and fixtures. This creates a baseline that protects you during claims-when a guest damages a wall or stains a carpet, you have proof of its pre-rental condition. Take photos of serial numbers on electronics, artwork values, and any high-value items you keep accessible to guests. Store these images in cloud storage with timestamps, not just on your phone. When damage occurs, you’ll need repair estimates and photos to file claims within Airbnb’s 14-day window, so having pre-rental documentation accelerates the process and strengthens your position. Property damage claims often hinge on proving the damage didn’t exist before the guest arrived, which documentation establishes immediately.

Disclose your rental activity to Your Insurer

Contact your current homeowners insurer directly and disclose that you plan to list on Airbnb. Do not assume silence equals permission-your insurer requires explicit disclosure, and failure to report rental activity voids your policy entirely. Your carrier will either exclude short-term rental activity in writing or cancel your policy outright. Once you understand their position, you face a choice: purchase a home-sharing endorsement if your carrier offers one (typically $200 to $400 annually but with strict limits on rental days), or switch to a specialized short-term rental policy. Many Minnesota hosts discover their carriers don’t offer endorsements at all, forcing a policy change. This conversation happens before you list, not after a claim gets denied.

Choose the Right Coverage Level for Your Property

The supplemental coverage decision depends entirely on your property value, expected rental income, and risk tolerance. A $250,000 property generating $24,000 annually in rental income needs different protection than a $500,000 lake property with $60,000 in annual bookings. For properties under $250,000 with modest income, basic short-term rental coverage at $200 to $400 annually might suffice. For properties exceeding $400,000 or generating over $40,000 in annual revenue, comprehensive policies with $2 million liability limits, business income protection, and guest damage coverage at $1,500 to $3,000 annually become essential. Proper Insurance offers commercial general liability starting at $1 million and covers bed bug infestations and squatters protection-gaps that Airbnb explicitly excludes. Consider a commercial umbrella policy for $300 to $600 annually if your property sits in a high-liability category (lake access, hot tub, fire pit). The math is straightforward: a single serious injury claim or week-long closure from property damage exceeds years of premium payments.

Final Thoughts

Airbnb’s Host Protection Insurance provides a foundation of coverage that protects you from some guest-related damages and liability claims. The $3 million in damage protection, $1 million in host liability, and income reimbursement for canceled bookings sound comprehensive until you face the real gaps-normal wear and tear, mold, theft without forced entry, and most importantly, lost income from property damage that forces closure all fall outside Airbnb’s protection entirely. Your homeowners policy won’t help either, as it explicitly excludes short-term rental activity, and filing a claim without disclosing your Airbnb business to your insurer triggers policy cancellation and claim denial under Minnesota law.

The Airbnb property protection plan works best when you layer it with dedicated short-term rental insurance. A specialized policy fills the income loss gap that Airbnb leaves open, covers guest theft with forced entry, protects against bed bug infestations and squatters situations, and extends liability coverage for amenities like hot tubs and fire pits. For Minnesota hosts, the combination of Airbnb’s $1 million liability plus a commercial policy with $2 million in additional protection creates genuine financial security at a cost of $800 to $2,400 annually for properties valued between $200,000 and $500,000.

Contact your current homeowners insurer and disclose your rental activity, then compare specialized short-term rental policies from Minnesota carriers to understand what gaps exist in your current protection. At Variant Insurance Group, we compare Minnesota’s top-rated insurance companies to find the right coverage for your specific property and income situation-our team reviews your options and compares protection and pricing to ensure you get genuine value. Contact us at variantinsurance.com to discuss your Airbnb hosting situation and build a complete insurance strategy that protects your property, your income, and your liability exposure.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation