Minnesota contractors face significant financial risks every day on job sites. Property damage, worker injuries, and professional mistakes can cost thousands of dollars without proper protection.

We at Variant Insurance Group see contractors struggle with choosing the right coverage types and managing premium costs. This guide breaks down essential contractor insurance options, cost-saving strategies, and claim prevention methods specifically for Minnesota’s construction industry.

What Insurance Coverage Do Minnesota Contractors Actually Need?

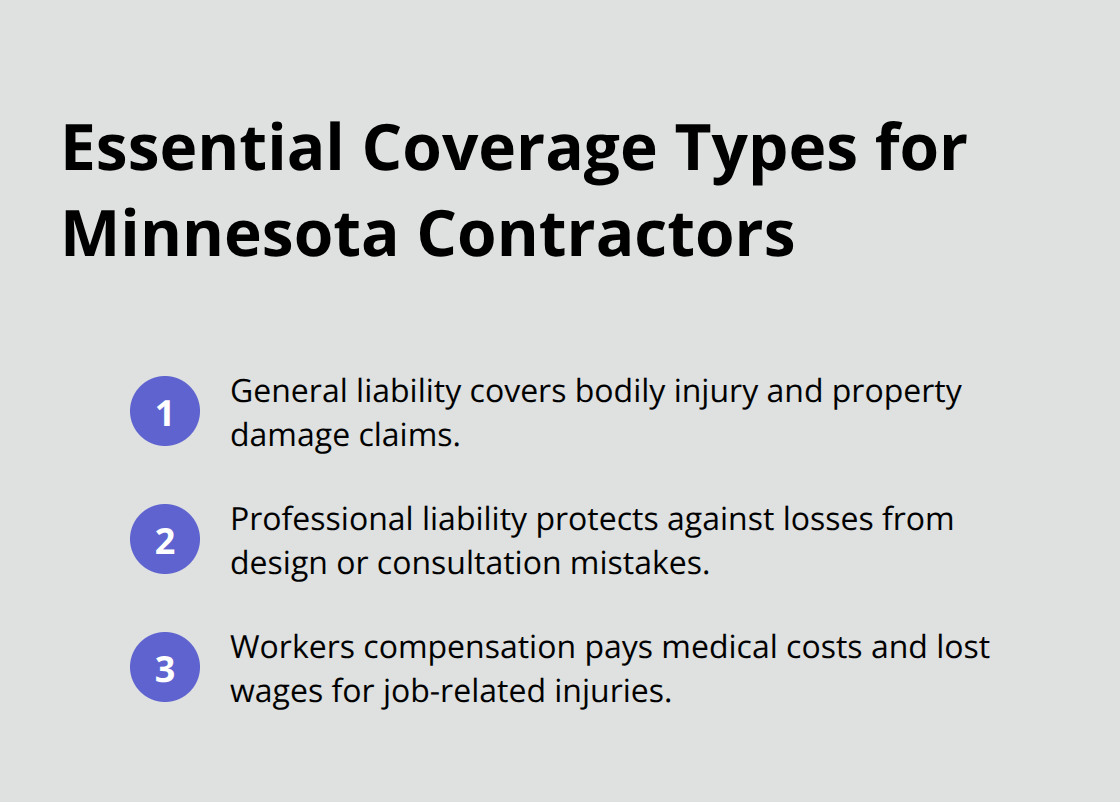

General Liability Insurance Protects Your Business Foundation

General liability insurance stands as the most important coverage for Minnesota contractors. This policy covers bodily injury and property damage claims during active work, with standard limits of $1,000,000 per occurrence and $2,000,000 aggregate that provide adequate protection for most contractors.

Minnesota contractors who work on larger projects often need $2-5 million umbrella policies to meet contract requirements. Property damage deductibles typically range from $1,000 to $2,500 for small to medium contractors. Products and completed operations coverage protects against claims after project completion, but many contractors miss this gap since basic general liability policies often exclude it.

Professional Liability Covers Costly Design and Consultation Mistakes

Professional liability insurance (also called errors and omissions coverage) protects contractors who provide consultation advice or design services from financial losses that professional mistakes cause. Contractors who give recommendations about materials, methods, or project specifications face liability risks when clients suffer losses from their advice.

This coverage becomes mandatory for contractors who perform any consultation work beyond basic construction services. The policy covers legal defense costs and settlements when clients claim that professional errors led to project delays or additional expenses.

Workers Compensation Requirements Protect Your Team

Minnesota law requires workers compensation insurance for contractors with employees. This coverage pays medical expenses and lost wages for job-related injuries. The employer is required to furnish medical treatment including psychological, chiropractic, and podiatric care as mandated by Minnesota statutes.

Roofing contractors and other high-risk trades benefit most from low experience modifiers through strong safety programs and minimal claims history. Contractors who hire subcontractors without workers compensation coverage become liable for any injuries that occur on their job sites.

These three core coverage types form the foundation, but specific project requirements and business operations often demand additional protection options that we’ll explore next.

How Much Does Contractor Insurance Really Cost

High-Risk Trades Pay Premium Prices

Roofing contractors and general contractors face the highest insurance premiums in Minnesota due to elevated accident rates and claim frequency. Roofing work generates significant workers compensation claims compared to standard construction trades, which pushes annual premiums from $8,000 to $15,000 for small crews. General contractors who subcontract 25-35% of their work pay higher rates because they lose direct control over job site safety practices.

Electricians and HVAC contractors typically secure coverage at 20-30% lower rates than roofers because electrical and mechanical work involves fewer fall hazards. Specialty contractors like floor installers or painters often qualify for the most competitive rates since their work presents minimal bodily injury risks to third parties.

Strategic Deductible Selection Cuts Annual Costs

Property damage deductibles between $1,000 and $2,500 represent the sweet spot for most Minnesota contractors. A contractor who chooses a $2,500 deductible over $1,000 reduces annual premiums by 15-20% while keeping out-of-pocket expenses manageable for typical claims. Contractors who select $5,000 deductibles save an additional 10% but risk significant cash flow problems during active claim periods.

Coverage limits of $1,000,000 per occurrence and $2,000,000 aggregate provide adequate protection for most residential and small commercial projects without inflated premiums. Contractors who work on projects that exceed $500,000 should consider umbrella policies that extend liability limits to $2-5 million at relatively modest additional costs.

Safety Programs Deliver Measurable Premium Reductions

Contractors with formal safety programs and documented safety meetings qualify for workers compensation discounts up to 30% through experience modifier improvements. The Minnesota Department of Labor and Industry tracks workplace injury rates, and contractors with three consecutive years of zero lost-time accidents often see their experience modifiers drop below 1.0 (which translates directly into lower premiums).

Claims-free contractors who implement drug tests, regular safety inspections, and mandatory hard hat requirements typically maintain the lowest insurance costs in their trade categories. Insurance companies reward proactive safety measures because they reduce claim frequency and severity across all coverage types. These cost factors matter, but contractors also need to understand what types of incidents actually trigger claims and how to prevent them.

What Claims Hit Contractors Most Often

Property Damage Creates the Highest Financial Losses

Property damage incidents create significant financial exposure for contractors, with the average settlement reaching $47,000 according to construction industry data. Contractors who work near existing structures face the highest risk when excavation equipment strikes underground utilities or when debris falls and damages vehicles and buildings. Water damage from plumbing mistakes generates claims that frequently exceed $25,000 because moisture spreads through multiple rooms before anyone detects the problem.

Minnesota Department of Labor and Industry reports show that contractors who implement daily site inspections reduce property damage claims by 40% compared to those who conduct weekly safety reviews. Contractors must secure all materials and tools at elevation to prevent falling object incidents that trigger expensive third-party claims.

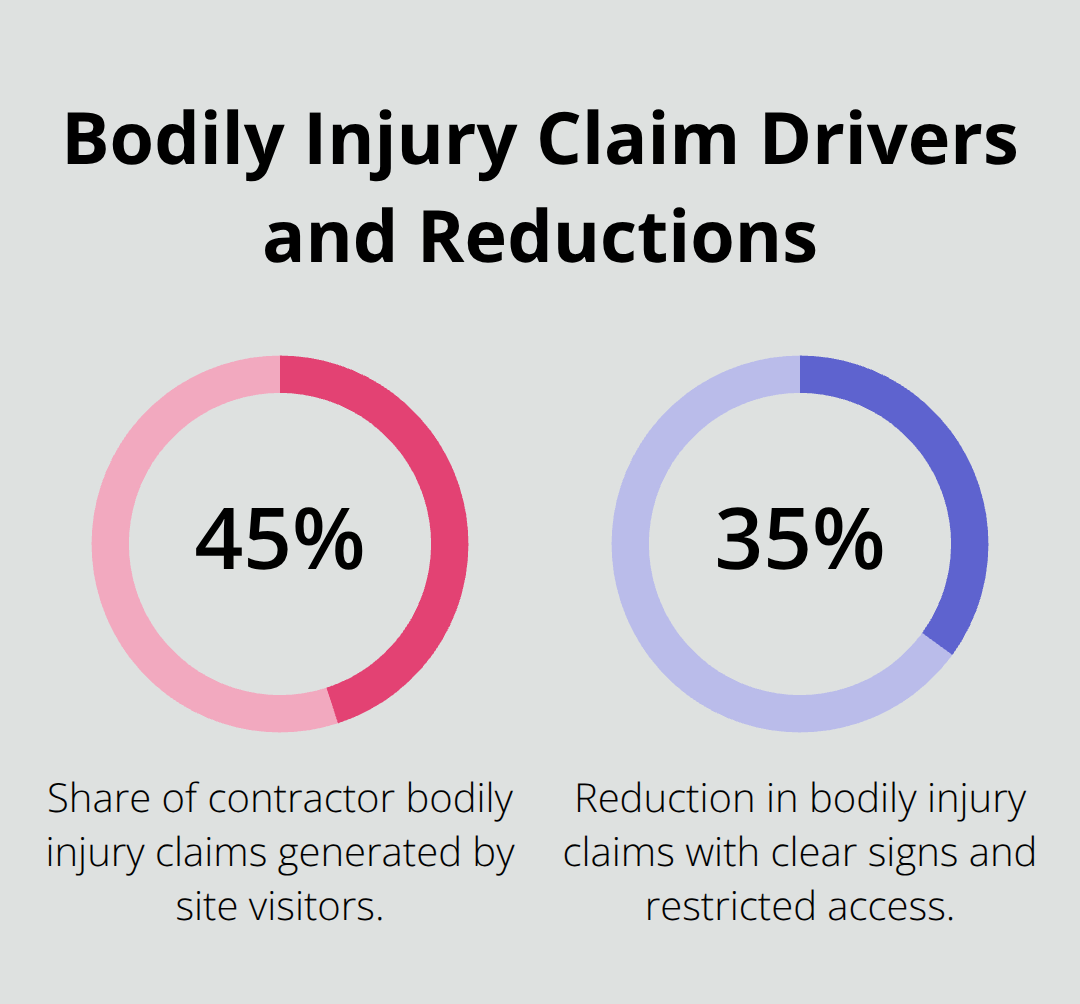

Bodily Injury Claims Target Site Safety Failures

Slip-and-fall accidents on job sites where contractors failed to maintain safe walkways create the most common bodily injury claims. Third-party injuries from tools or materials that fall from height create liability exposures that often trigger umbrella policy limits. Contractors who allow unauthorized personnel on active job sites face increased liability when visitors suffer injuries from construction hazards.

Site visitors (including homeowners and inspectors) generate 45% of contractor bodily injury claims because they lack familiarity with construction hazards. Contractors who post clear warning signs and restrict access to dangerous areas reduce bodily injury claims by 35% according to insurance industry data.

Professional Errors Generate the Most Expensive Settlements

Design mistakes and consultation errors generate the most expensive contractor claims, with professional liability settlements that average $85,000 per incident. Contractors who recommend specific materials or installation methods become liable when those recommendations fail to meet project specifications or building codes. Project delays that contractor mistakes cause trigger consequential damage claims that include lost rental income, additional costs, and business interruption expenses for commercial clients.

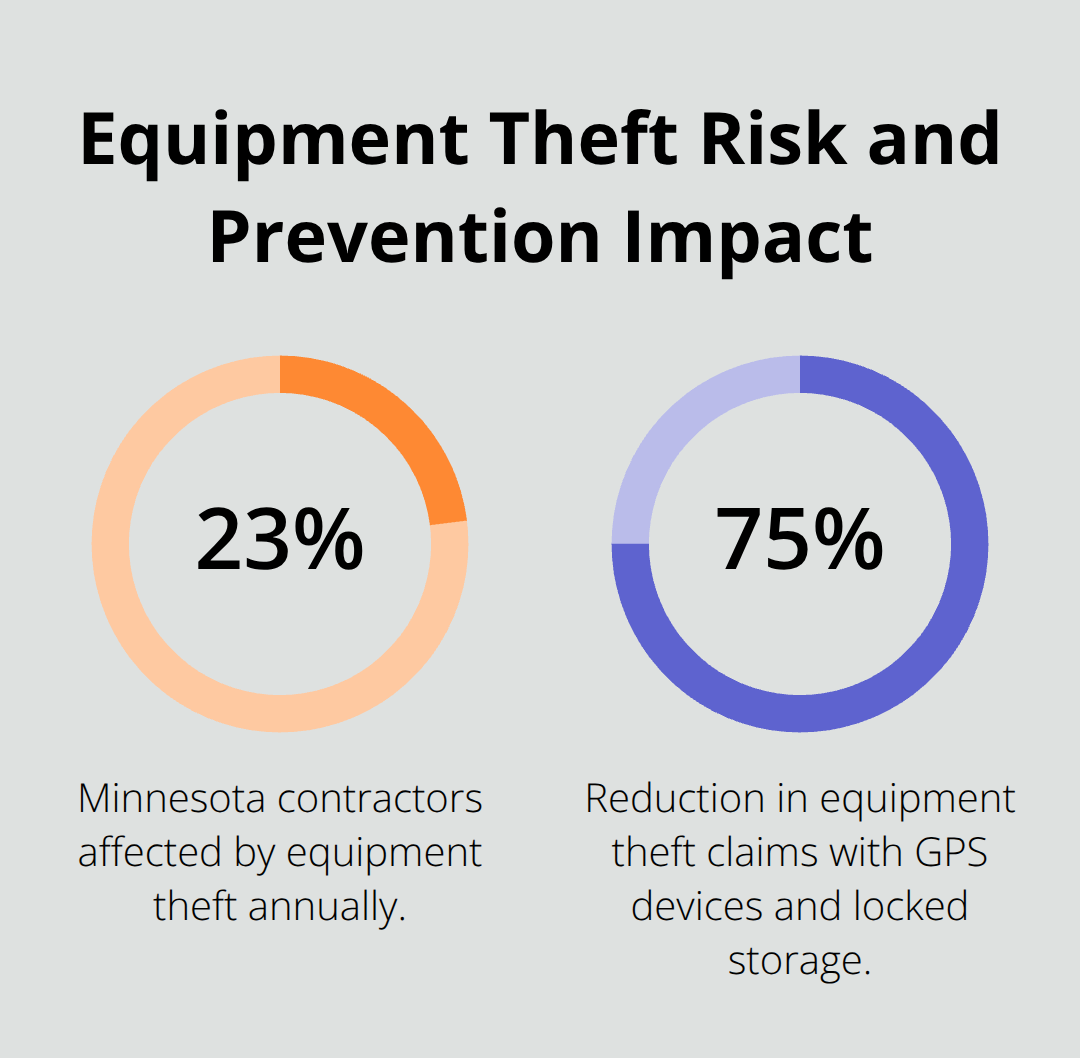

Equipment Theft Affects Nearly Quarter of Minnesota Contractors

Equipment theft affects 23% of Minnesota contractors annually, with stolen tools and machinery that average $15,000 per incident. Contractors who leave equipment overnight at job sites without proper security measures face the highest theft rates.

GPS devices and locked storage containers reduce equipment theft claims by 75% according to construction insurance data. Job site security cameras and motion-activated systems provide additional deterrent effects that insurance companies recognize through premium discounts.

Final Thoughts

Minnesota contractors need three essential coverage types to protect their businesses: general liability insurance with $1,000,000 per occurrence limits, professional liability coverage for consultation work, and workers compensation insurance as required by state law. These policies form the foundation that protects against property damage, bodily injury claims, and professional mistakes that cost contractors thousands of dollars annually. Smart contractors prioritize these core protections before they consider additional coverage options.

Local Minnesota insurance agents provide significant advantages over national carriers who lack understanding of state-specific requirements and regional construction risks. Local agents understand Minnesota’s contractor registration requirements, workers compensation regulations, and the unique challenges that harsh winters create for construction businesses. They also know which insurance companies offer the most competitive rates for specific trades in Minnesota markets.

We at Variant Insurance Group help Minnesota contractors find the right contractor insurance policy for their specific needs. Our team reviews your options and compares protection and prices to deliver competitive value. Proper coverage starts when you evaluate your current risks, determine required coverage limits, and request quotes from experienced construction insurance specialists who understand your trade’s unique exposures.