Minnesota landlords face unique insurance challenges that standard homeowners policies simply can’t handle. Property damage, tenant lawsuits, and lost rental income create financial risks that require specialized protection.

We at Variant Insurance Group see landlords struggle with coverage gaps that cost thousands in unexpected expenses. Understanding landlord insurance Minnesota requirements protects your investment and rental business from devastating losses.

Understanding Landlord Insurance Requirements in Minnesota

Minnesota law doesn’t mandate landlord insurance, but mortgage lenders universally require it for financed rental properties. This creates a practical requirement for many Minnesota landlords who carry mortgages. The state’s Department of Commerce recommends landlord coverage for all rental properties, recognizing the financial risks involved. Research shows that more than a quarter of Minnesota families pay more than they can afford for housing costs.

Standard Homeowners Policies Exclude Rental Activities

Homeowners insurance explicitly excludes rental activities and leaves landlords exposed to massive liability gaps. When tenants cause property damage or visitors get injured, homeowners policies deny claims entirely. Premises liability cases can result in substantial financial awards, making proper coverage essential. Landlord policies specifically cover these rental-related risks that homeowners insurance won’t touch.

All Rental Property Types Need Specialized Coverage

Single-family homes, duplexes, apartment buildings, and condominiums all require landlord insurance when rented to tenants. Even basement apartments in owner-occupied homes need separate coverage since homeowners policies exclude rental income areas. Minnesota’s short-term rental market also demands landlord coverage, as platforms like Airbnb exclude many liability scenarios from their host protection programs.

Commercial Properties Face Additional Requirements

Commercial properties with mixed-use spaces need landlord coverage for residential units, regardless of the building’s primary purpose. These properties often face higher liability limits and additional coverage requirements that standard policies don’t address. Property owners must navigate both commercial and residential insurance regulations simultaneously.

The next step involves understanding exactly what types of coverage protect Minnesota landlords from the most common and expensive risks they face.

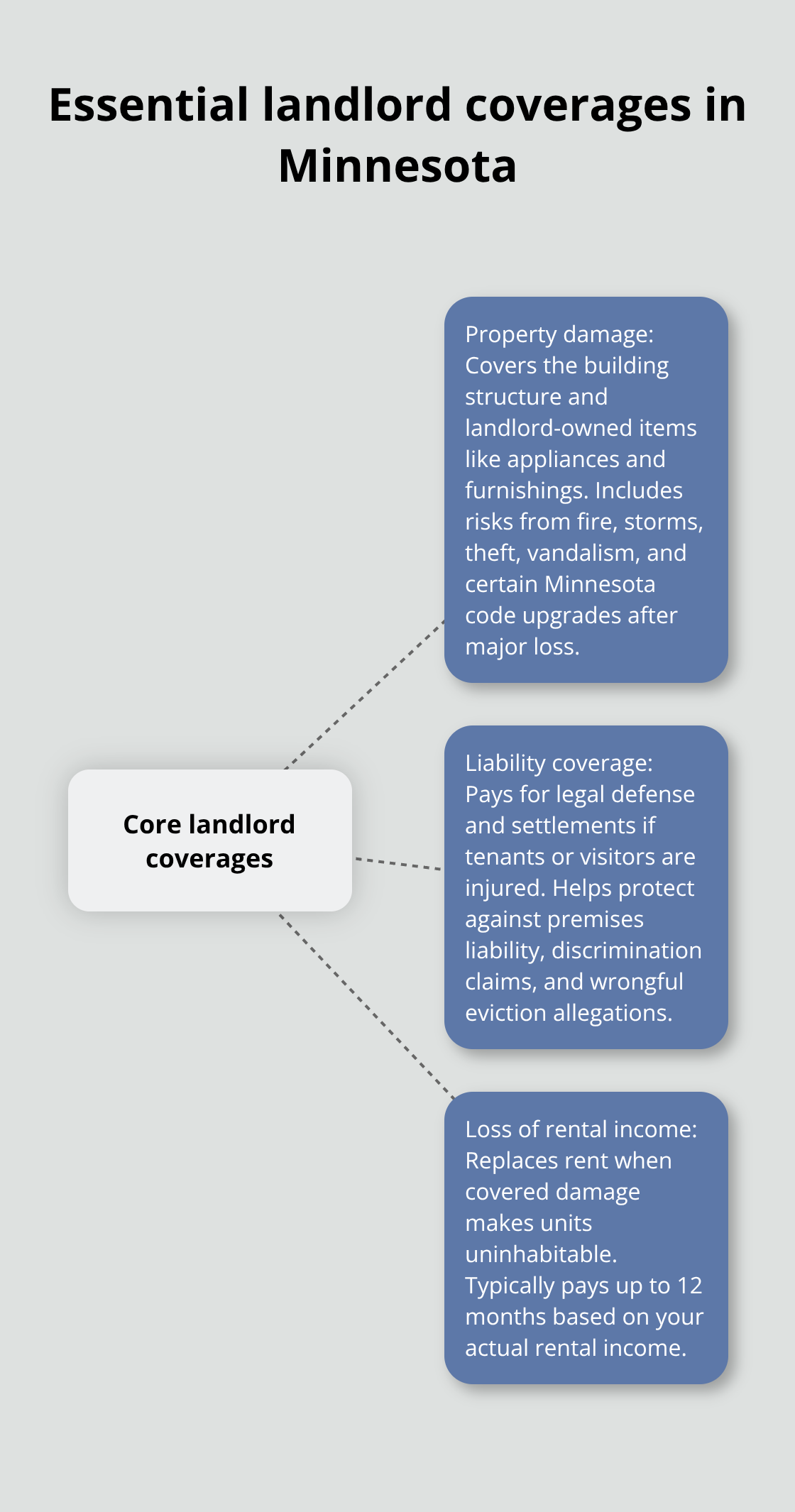

Essential Coverage Types for Minnesota Landlords

Minnesota landlords require three fundamental coverage types that standard homeowners policies completely ignore. Property damage protection covers your building structure and any landlord-owned items like appliances or furnishings when fire, storms, theft, or vandalism strikes. The Insurance Information Institute reports that property damage claims average $11,650 nationally, which makes this protection financially essential. This coverage extends beyond basic repairs to include code upgrade requirements that Minnesota often mandates after major damage occurs.

Property Damage and Dwelling Protection

Property damage coverage protects the physical structure of your rental property and any items you own as the landlord. This includes appliances, furnishings, and building components that tenants don’t own. Minnesota weather patterns create specific risks (including severe storms, hail, and winter damage) that can devastate unprotected properties. The coverage also handles vandalism and theft situations that frequently affect rental properties more than owner-occupied homes.

Liability Coverage for Tenant Injuries and Lawsuits

Liability coverage protects landlords when tenants or visitors suffer injuries on rental property premises. Minnesota premises liability awards for moderate injuries, fractures requiring surgery, and torn ligaments typically range from $75,000 – $500,000 for slip-and-fall incidents, broken stairs, or inadequate lighting situations. This coverage handles both legal defense costs and potential settlements or judgments against property owners. Smart Minnesota landlords carry minimum liability limits of $300,000 per occurrence, though $500,000 provides better protection against catastrophic claims. The coverage also protects against discrimination lawsuits and wrongful eviction claims that can devastate landlord finances.

Loss of Rental Income Protection

Loss of rental income coverage compensates landlords when covered damage makes units uninhabitable and tenants cannot pay rent. Minnesota’s average repair timeline for major property damage spans 3-6 months, which creates substantial income gaps for property owners. This coverage typically pays 12 months of lost rent, calculated from your actual rental income rather than market rates.

The protection activates immediately when covered perils force tenant displacement and prevents landlords from absorbing both repair costs and lost rental payments simultaneously.

These coverage types work together to protect your investment, but their costs vary significantly based on factors specific to your property and location in Minnesota.

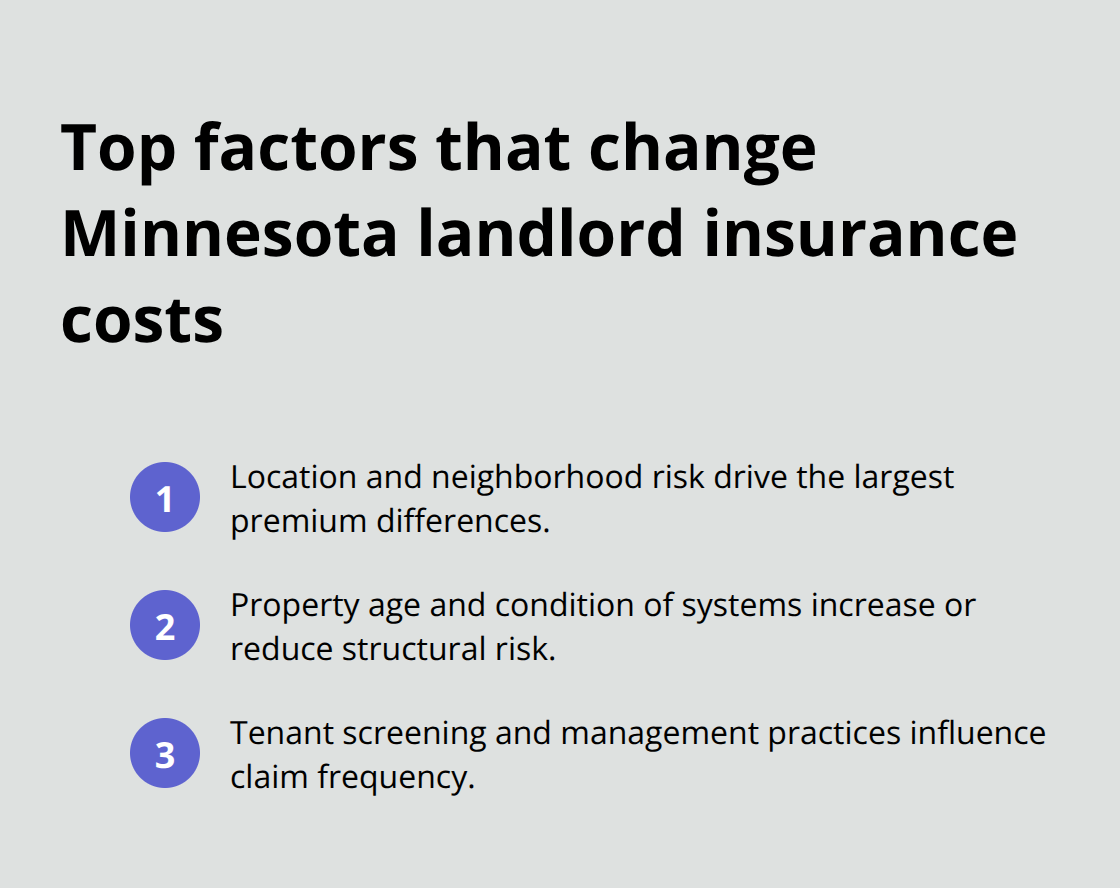

Factors That Affect Landlord Insurance Costs in Minnesota

Minnesota landlord insurance premiums range from $800 to $2,000 annually, but location drives the biggest cost differences. Properties in Minneapolis and St. Paul face premiums 40-60% higher than rural Minnesota locations due to elevated crime rates and litigation frequency. The FBI’s Uniform Crime Reporting data shows Minneapolis property crime rates at 4,847 incidents per 100,000 residents compared to statewide averages of 1,890 per 100,000, which directly impacts your insurance costs.

Crime Statistics Shape Premium Calculations

Insurance companies analyze neighborhood crime data down to the block level when they calculate your premiums. Properties within two blocks of high-crime areas face surcharges of 15-25% even if your specific block remains safe. Theft and vandalism claims in Minneapolis average $3,200 per incident according to Minnesota Department of Public Safety records, while Greater Minnesota claims average just $1,800. Security systems, motion-activated lights, and deadbolt locks can reduce premiums by 5-10% while they deter criminal activity that drives up neighborhood risk profiles.

Property Age Determines Structural Risk Premiums

Older properties face higher premiums due to outdated electrical, plumbing, or mechanical systems that create higher claim frequencies. Minnesota’s harsh winters particularly stress older properties with original windows, roofing, and insulation that haven’t received major updates. Electrical panel upgrades, new roofing installations, and HVAC system replacements can reduce premiums significantly while they prevent expensive damage claims. Properties with galvanized plumbing face additional surcharges since water damage claims from pipe failures cost insurers an average of $8,500 per incident.

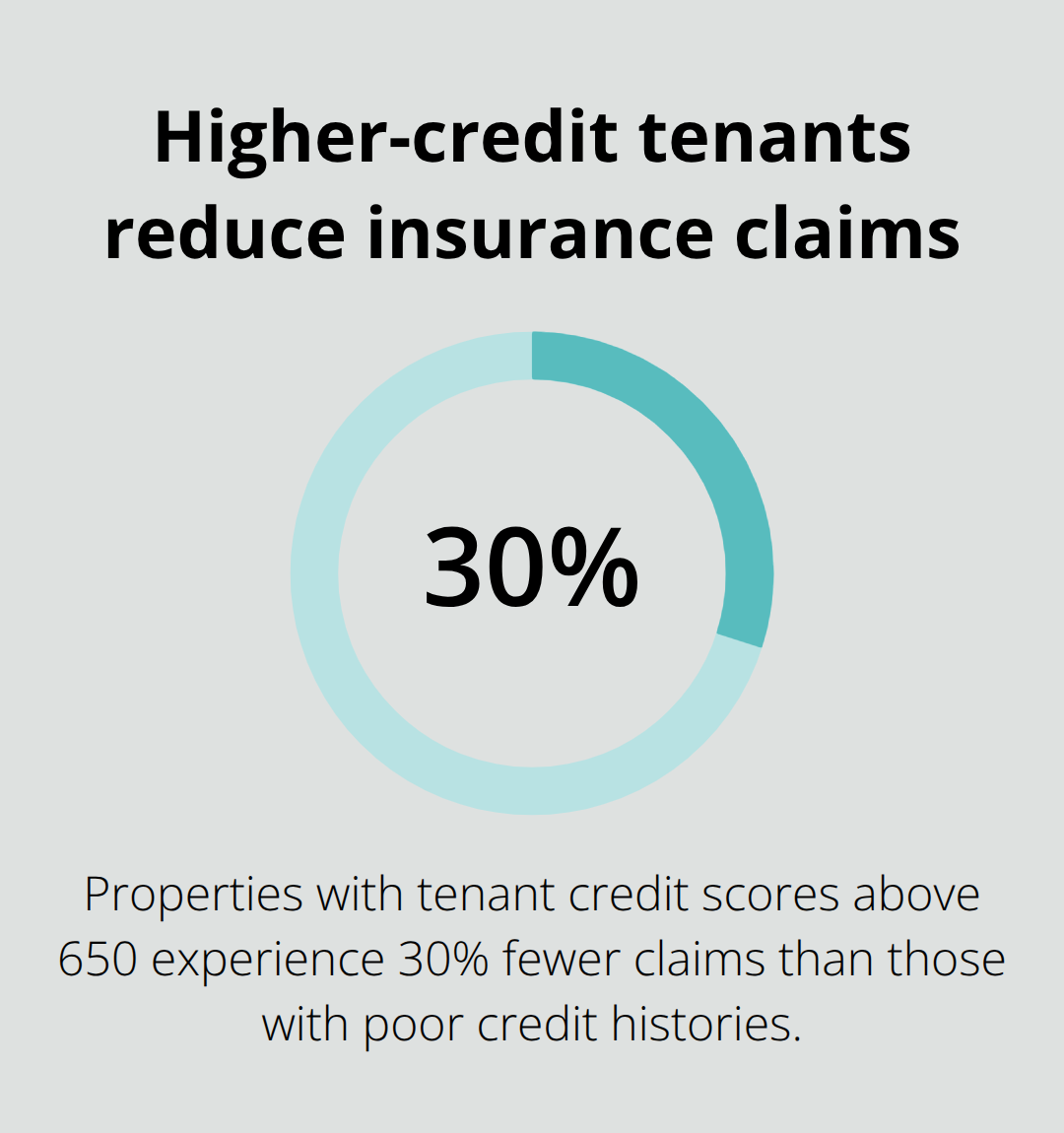

Tenant Quality Directly Impacts Your Rates

Insurance companies reward landlords who conduct thorough background checks, verify employment history, and require security deposits equivalent to two months rent. Properties with tenants who have credit scores above 650 experience 30% fewer claims than those that house tenants with poor credit histories. Professional property management companies often negotiate group discounts of 10-15% with insurers due to their systematic maintenance schedules and proven tenant screening processes (which reduce overall claim frequency across their portfolio).

Final Thoughts

Minnesota landlords who skip proper insurance coverage face financial disasters that destroy rental investments overnight. Property damage, liability lawsuits, and lost rental income create risks that standard homeowners policies won’t cover. Smart landlords protect themselves with comprehensive landlord insurance Minnesota policies that address these specific rental property exposures.

The right coverage starts with an understanding of your property’s unique risks and comparison of options from multiple insurance companies. Location, property age, and tenant quality all impact your premiums, but proper coverage prevents catastrophic losses that dwarf annual insurance costs. Professional agents help landlords navigate coverage options while they secure competitive rates (especially as rental businesses grow and change).

We at Variant Insurance Group help Minnesota landlords find policies that fit their specific needs and budget. Our team understands local market conditions and works with multiple carriers to provide options rather than push a single company’s products. Contact us to explore landlord insurance options that protect your rental property investment.