Most Minnesota homeowners don’t realize how much of their property and liability insurance coverage actually protects them-or what it doesn’t.

We at Variant Insurance Group see this gap firsthand. Many policies leave families exposed to unexpected costs when claims happen. This guide walks you through what property and liability coverage really means, where the holes typically are, and how to fix them.

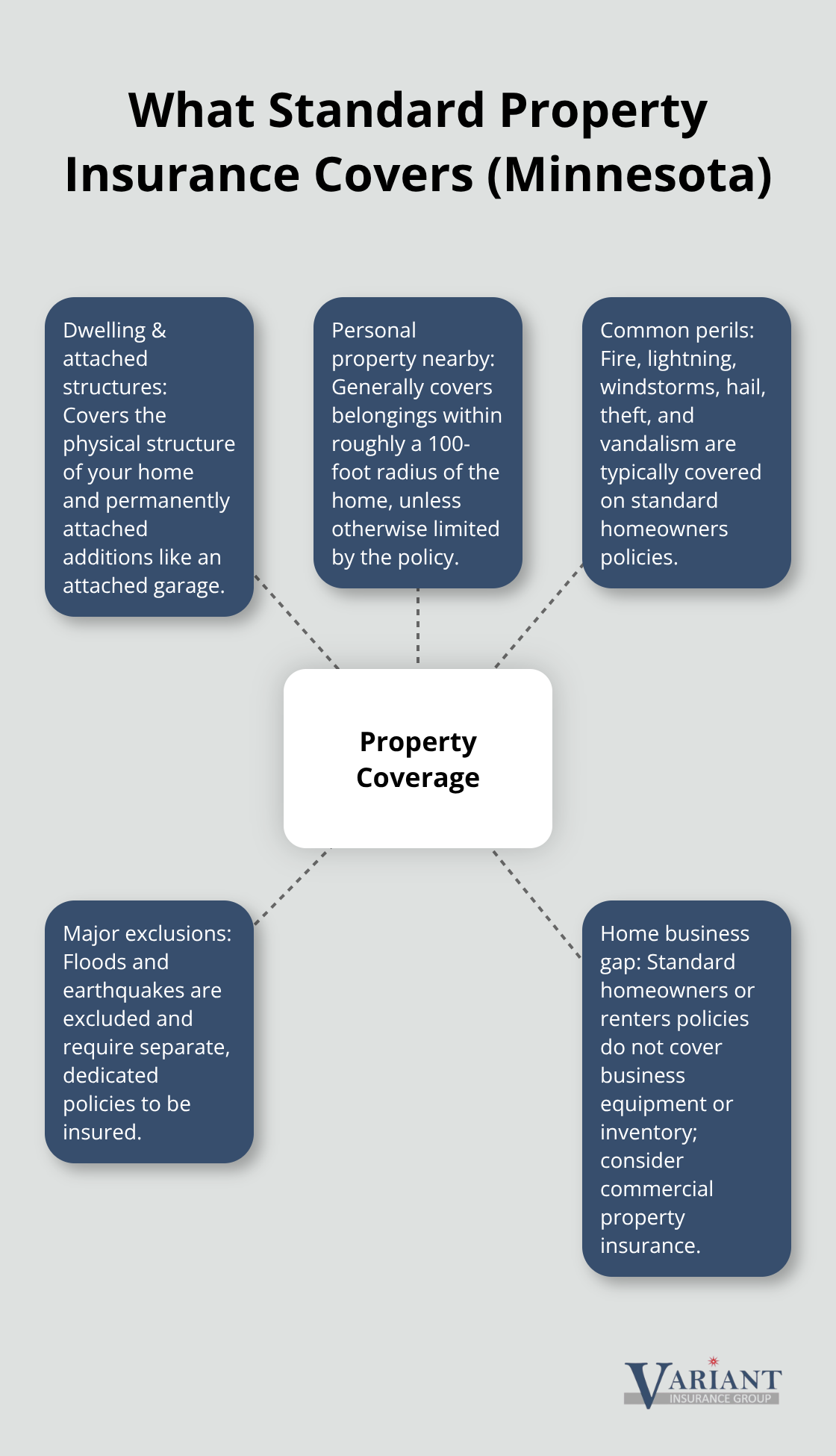

What Property Insurance Actually Covers

Property insurance protects the physical structure of your home and your personal belongings against direct physical loss. In Minnesota, this typically means coverage for damage from fire, lightning, windstorms, hail, theft, and vandalism under a standard homeowners policy. However, standard homeowners policy excludes floods and earthquakes, which require separate coverage. The coverage applies to your home’s structure, attached structures like garages, and personal property inside-generally items within roughly a 100-foot radius of your home. If you work from home, a critical mistake many Minnesota homeowners make is assuming their standard homeowners or renters policy covers business equipment and inventory. It doesn’t.

You’ll need commercial property insurance to protect business assets, which is a gap that catches people off guard during claims.

Open Peril Versus Named Peril Policies

When you shop for property coverage in Minnesota, you’ll encounter two types: open peril policies and named peril policies. Open peril coverage, sometimes called special risk coverage, protects against all direct physical losses unless explicitly excluded-this means if damage occurs and it’s not specifically excluded, you’re covered. Named peril policies cover only the specific risks listed in your policy, such as fire, lightning, theft, or windstorms. Open peril policies cost more upfront but provide significantly broader protection and fewer claim denials. Most Minnesota homeowners benefit from open peril coverage because weather-related damage is common here, and you avoid the frustration of discovering your specific damage type wasn’t listed on your policy. The trade-off is straightforward: you pay more in premiums but gain peace of mind that unexpected damage won’t leave you paying out-of-pocket.

How Claims Work in Minnesota

When you file a property claim in Minnesota, the insurance company sends an adjuster to inspect the damage and determine what your policy covers. The adjuster assesses whether the damage falls within your coverage, applies your deductible, and determines the payout amount based on your policy limits. This process typically takes two to four weeks, though complex claims can take longer. You should document everything before the adjuster arrives-take photos and videos of all damage, list damaged items with approximate values, and gather receipts if available. Your policy limits are the maximum your insurer will pay for a covered loss. If your home is underinsured and the damage exceeds your limit, you pay the difference yourself. This is why you need to review your coverage limits annually, especially as property values and replacement costs increase in Minnesota’s housing market.

Why Liability Coverage Matters Alongside Property Protection

Property insurance alone doesn’t protect you if someone else gets hurt on your property or if you accidentally damage someone else’s belongings. This is where liability coverage steps in-it covers injuries to others, damages to others’ property, and legal expenses for accident-related lawsuits. Your property policy and liability coverage work together to create a complete safety net. Without adequate liability limits, a single incident could expose your personal assets to significant financial risk. Understanding how these two coverages complement each other helps you identify the right protection level for your situation and avoid costly gaps when claims happen.

Understanding Liability Insurance Coverage

Liability insurance covers injuries to others, damage to others’ property, and legal expenses when you’re found responsible for an accident. This protection differs fundamentally from property insurance, which protects your own belongings and home structure. If someone slips on your icy Minnesota driveway and breaks their leg, liability coverage pays for their medical bills and any lawsuit they file against you. If your teenager accidentally damages a neighbor’s garage door with a baseball, liability coverage handles the repair costs. Without this protection, you’d pay these expenses directly from your personal bank account or assets.

Minnesota requires auto liability coverage by state law, but homeowners liability coverage isn’t legally mandated-your mortgage lender requires it instead. Many renters mistakenly skip liability coverage because they think they don’t own property worth protecting, but liability protects your personal assets, not the rental unit itself.

Choosing the Right Liability Limits for Your Situation

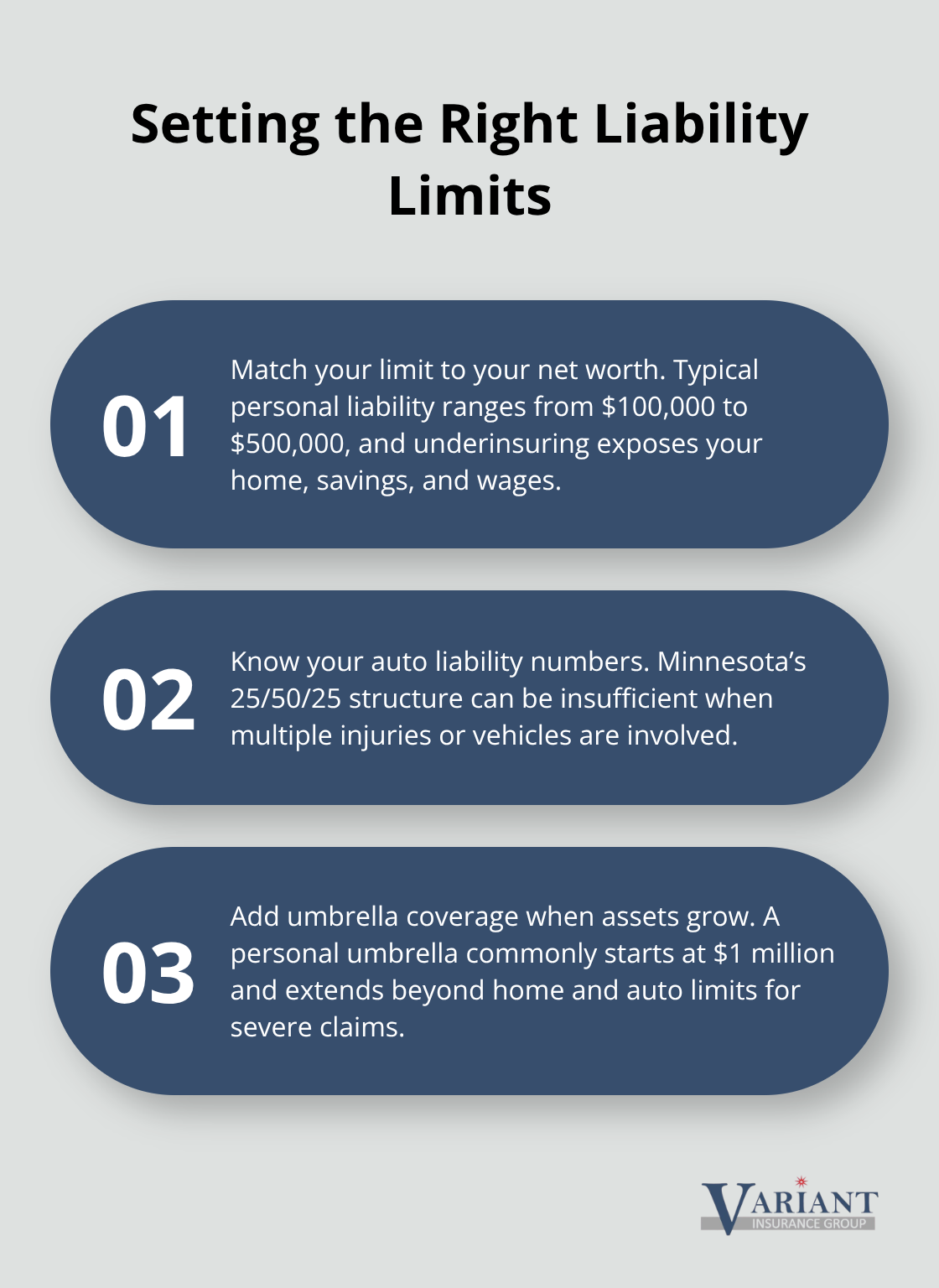

Liability limits represent the maximum amount your insurance company will pay for a single incident. For homeowners and renters in Minnesota, personal liability coverage typically ranges from $100,000 to $500,000 as a single limit. You should select a limit that matches or exceeds your total net worth to genuinely protect your assets. If your home is worth $400,000, your investments total $150,000, and your vehicles are worth $80,000, your net worth is approximately $630,000-meaning a $300,000 liability limit leaves you vulnerable.

A lawsuit judgment can exceed your policy limit, and the plaintiff can pursue your wages and assets to collect the difference. This is why underestimating your liability needs is a costly mistake. Auto liability in Minnesota uses three numbers displayed as 25/50/25, representing bodily injury per person, bodily injury per accident, and property damage per accident in thousands of dollars.

Most Minnesota drivers carry minimum limits of 25/50/25, but this is dangerously low if you cause a serious accident involving multiple vehicles or injuries. A single catastrophic crash with two injured occupants in another vehicle could easily exceed these minimums.

Consider umbrella insurance for additional protection beyond your standard policy limits. Personal umbrella coverage often starts at $1 million and protects you when costs surpass your auto or homeowners liability limits.

Real Incidents That Expose Liability Gaps

Everyday incidents turn expensive quickly when liability coverage falls short. A broken screw found in pizza at a restaurant causes internal injuries; a foreign object in food breaks someone’s tooth; a guest trips on your deck and requires surgery. Food safety liability has historically involved bacteria like Salmonella and Listeria in contaminated products from suppliers ranging from Cargill to Trader Joe’s, but residential liability claims center on slip-and-fall incidents, dog bites, and accidental property damage.

If your dog bites a neighbor requiring stitches and rabies treatment, liability coverage pays their medical costs and any settlement. If you accidentally damage someone else’s mailbox, fence, or vehicle in your driveway, liability covers repairs. These aren’t hypothetical scenarios-they happen regularly in Minnesota communities, and homeowners without adequate coverage face devastating financial consequences that property insurance never addresses.

How Liability Coverage Protects Your Assets

Liability coverage includes legal defense costs, which shields your finances during litigation. When someone files a lawsuit against you, your insurer pays for attorneys, court costs, and investigation expenses-costs that can reach tens of thousands of dollars even before a settlement or judgment. This defense component makes liability coverage far more valuable than many homeowners realize. Your policy limit applies to the total payout (defense costs plus damages), so a $300,000 limit covers both legal defense and any judgment amount combined. Understanding this distinction helps you recognize why adequate limits matter so much.

The gap between what you think you’re protected for and what you actually need often becomes apparent only after an incident occurs. This is precisely why reviewing your liability limits annually-especially as your net worth grows-prevents catastrophic financial exposure. Your current coverage may have made sense five years ago, but changes in your assets, property value, and life circumstances demand reassessment.

Where Your Coverage Actually Fails

Most Minnesota homeowners discover gaps in their policies only after filing a claim, which is far too late. Many policies look adequate on paper but leave families exposed to thousands in out-of-pocket costs. The problem isn’t always that coverage is too low-it’s that homeowners misunderstand what their policies actually protect and what they explicitly exclude.

Underinsurance Leaves You Vulnerable

Underinsurance happens when your coverage limits fall below the true replacement cost of your home and belongings or when your liability limits don’t match your net worth. Minnesota’s housing market has appreciated significantly, yet many homeowners haven’t increased their coverage limits in five or ten years. If your home was worth $350,000 when you bought it but is now worth $480,000, your coverage limits likely haven’t kept pace. A total loss would leave you paying the difference yourself.

Replacement cost coverage pays the cost to repair or replace your home or personal property based on its current value. Actual cash value policies depreciate your belongings, so a five-year-old roof or ten-year-old furniture receives pennies on the dollar. This depreciation can cut your claim payout in half compared to replacement cost coverage.

Standard Exclusions Create Dangerous Gaps

Exclusions create the most dangerous gaps because homeowners simply don’t read them. Standard homeowners policies exclude flood damage, earthquake damage, sump pump backups, and water damage from poor maintenance-yet these are common Minnesota claims. Damage from ice dams, which plague Minnesota winters, falls into a gray area depending on your policy wording. Business property inside your home isn’t covered under residential policies, and neither is property in detached structures unless you specifically add it.

Water damage represents one of the costliest exclusions. A burst pipe, roof leak, or foundation crack can cause tens of thousands in damage that your standard policy won’t cover if the damage stems from lack of maintenance or poor drainage. You need to understand exactly which water damage scenarios your policy covers and which ones it doesn’t.

Liability Exclusions Expose Your Assets

Liability exclusions are equally problematic: intentional acts aren’t covered, contractual liability isn’t covered, and damage you cause while performing business activities typically isn’t covered. If you run a consulting business from home and a client slips on your stairs during a meeting, your homeowners liability may deny the claim because you were conducting business. If you cause property damage to a rental property you own, your homeowners policy excludes it.

These gaps matter most when they intersect with your actual life. A side business, rental property, or professional services you provide from home all create liability exposures that standard homeowners coverage doesn’t address. You need to identify which of your activities fall outside your policy’s protection.

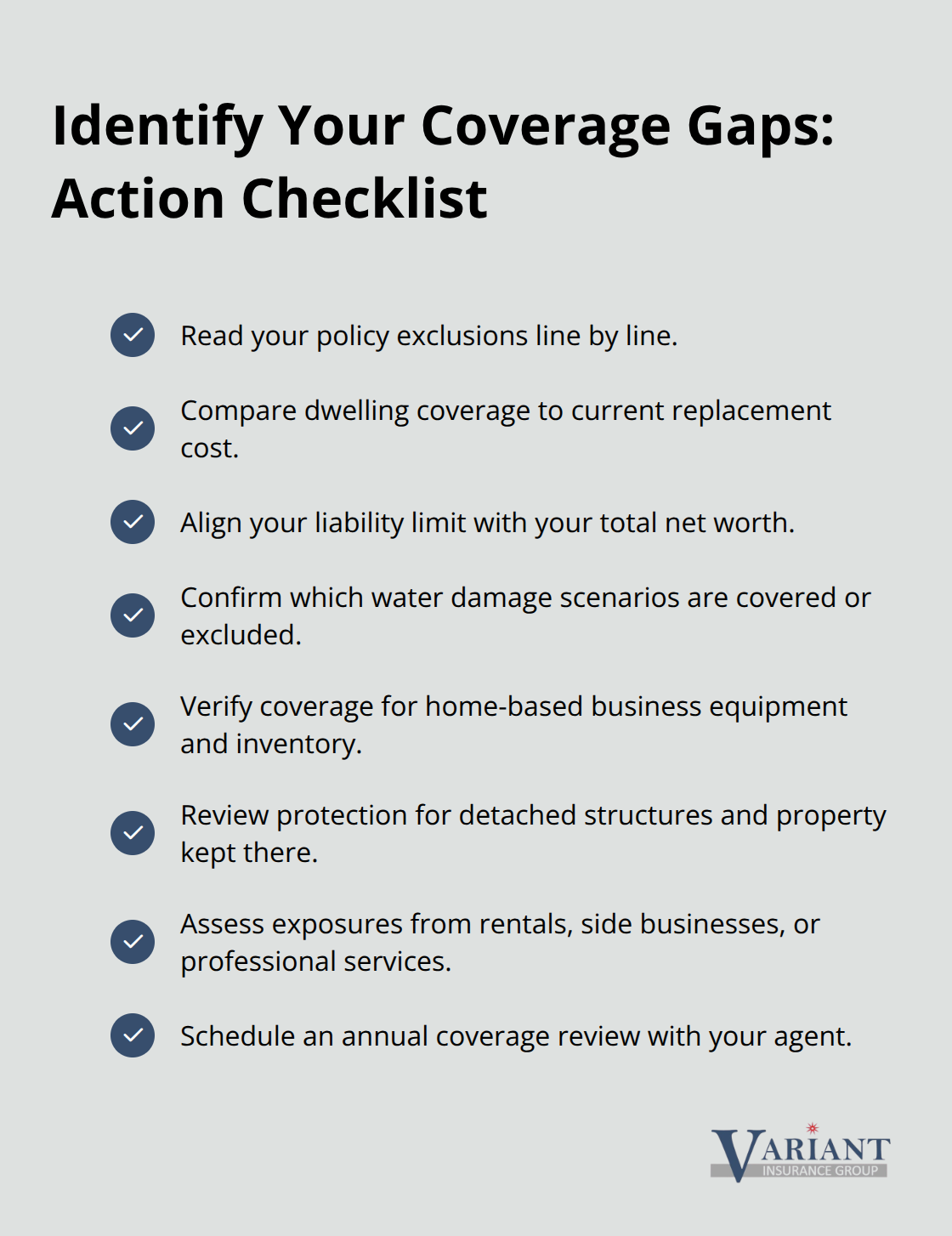

How to Identify Your Coverage Gaps

The solution requires actually reading your policy exclusions-not just skimming the declarations page-and having a conversation with your insurance representative about what situations worry you most. Compare your current limits against your home’s replacement cost, your net worth, and your specific exposures. This reveals exactly where you need additional protection or higher limits.

Ask your agent specific questions about scenarios that concern you. Does your policy cover water damage from a sump pump failure? What about damage from a burst pipe? If you work from home, does your coverage protect business equipment? If you own rental property, what liability gaps exist? These conversations uncover the real gaps that numbers on a declarations page never show.

Final Thoughts

Property and liability insurance coverage protects you from two distinct but equally important financial threats. Property insurance covers your home and belongings when damage occurs, while liability insurance protects your personal assets when someone else gets hurt or their property is damaged because of you. Together, they form the foundation of financial security most Minnesota homeowners need.

The gaps we’ve covered throughout this guide reveal a consistent pattern: homeowners either carry limits that don’t match their net worth, misunderstand what their policies exclude, or fail to address specific exposures like home-based businesses or rental properties. A single underinsured claim or liability lawsuit can wipe out years of financial progress. The solution requires honest assessment of what you actually own, what you could lose, and what your current policy truly covers.

Pull out your current homeowners and auto policies and review your coverage limits against your home’s replacement cost and your total net worth. Identify any exclusions that concern you based on your specific situation. Then contact Variant Insurance Group to discuss what you’ve found, and we’ll review your options, explain what gaps exist, and show you how to close them without overpaying.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation