Renting out a property in Minnesota requires different insurance protection than living in your own home. Standard homeowners insurance won’t cover the unique risks landlords face, which is why homeowners insurance for rental property exists as a separate product.

At Variant Insurance Group, we help property owners understand these critical differences so they can protect their investment properly. The right coverage keeps you financially secure when unexpected events happen.

Why Rental Property Insurance Differs From Homeowners Coverage

Standard homeowners insurance is designed for owner-occupied homes and explicitly excludes rental income and tenant-related liability. If you rent out a property using a homeowners policy, you remain uninsured for the exact risks that matter most to a landlord. Most homeowners policies won’t cover loss of rental income if a covered event makes the property uninhabitable, won’t protect you against liability claims from tenants or their guests, and won’t cover landlord-owned appliances or equipment on site.

Insurance companies treat rental properties as higher-risk ventures because tenants create exposure that owner-occupants don’t. A tenant’s guest injured on the property, damage caused by a tenant’s negligence, or vacancy periods all represent financial threats that standard homeowners policies simply don’t address. In Minnesota, landlord insurance is highly recommended, which means protecting your rental investment requires specialized coverage even if the law doesn’t mandate it.

Landlord insurance-usually written as a DP-3 policy-covers the dwelling structure at replacement cost, other structures on the property, landlord liability with higher limits (typically $300,000 to $1 million), and loss of fair rental value if tenants can’t occupy the space due to a covered loss.

The Real Cost of Being Underinsured

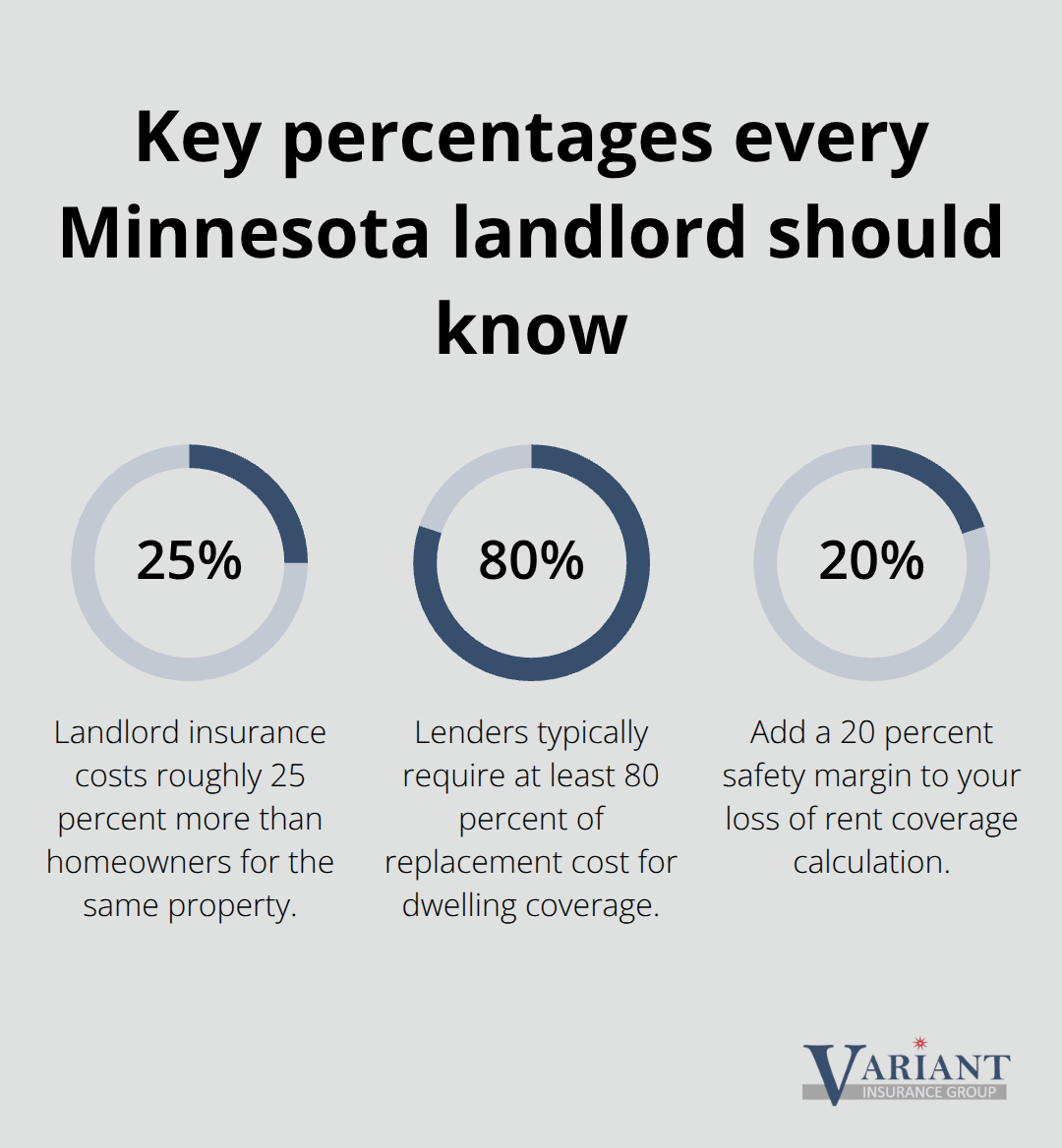

Landlord insurance costs roughly 25 percent more than homeowners insurance for the same property, with Minnesota averages around $1,083 annually, though premiums vary significantly based on location, property age, crime rates, and weather exposure. That extra cost reflects real protection: if a fire damages your rental and makes it uninhabitable for three months while repairs happen, loss of rent coverage reimburses the fair rental value during that period. Without it, you absorb the entire income loss yourself.

A property that generates $1,500 monthly in rent would cost you $4,500 in lost income over that recovery period. The difference between actual cash value and replacement cost also matters more with rental properties because landlord policies that pay replacement cost cover the full current cost to repair or rebuild, while actual cash value policies pay replacement cost minus depreciation. This gap can leave you thousands out of pocket on aging components like roofs or HVAC systems.

What Minnesota Landlords Must Know

Minnesota law doesn’t require landlord insurance, but mortgage lenders almost universally do as a financing condition. Your lease should also require tenants to carry renters insurance and name you as an interested party, protecting you if tenant negligence causes damage. Flood damage remains excluded from all standard landlord policies, so if your property sits in a flood zone or high-risk area, you need separate coverage through the National Flood Insurance Program or a private carrier.

Security features like burglar alarms, fire sprinklers, and gated access can lower premiums by 10 to 15 percent, making those upgrades financially sensible beyond just operational benefits. When you shop for landlord insurance in Minnesota, work with a local independent agent who can obtain quotes from multiple carriers rather than going directly to a single company. An agent understands Minnesota’s specific weather risks, local crime patterns, and lender requirements, positioning you to avoid coverage gaps that could derail your rental investment strategy.

The next chapter walks you through what rental property insurance actually covers and how each component protects your financial interests as a landlord.

What Your Rental Property Insurance Actually Covers

Your DP-3 landlord policy protects three distinct financial interests that homeowners insurance ignores. The dwelling coverage pays to repair or rebuild the structure itself at replacement cost, meaning you receive the full current expense to restore the building to its pre-loss condition rather than a depreciated amount. Other structures on the property, such as detached garages or sheds, receive separate coverage limits. Landlord personal property coverage protects appliances, tools, and equipment you own and keep on site for maintenance or tenant use-assets that standard homeowners policies exclude entirely. Most Minnesota policies set dwelling coverage limits between $200,000 and $500,000 depending on property size and rebuild costs in your area, though your mortgage lender typically dictates the minimum required amount.

Landlord Liability: Protection Against Tenant-Related Claims

Landlord liability coverage is where rental property insurance fundamentally differs from homeowners protection. Your policy typically provides $300,000 to $1 million in liability limits to cover injuries or property damage claims from tenants, their guests, or visitors on your property. A tenant’s guest slips on your icy sidewalk, a visitor’s child sustains an injury in a common area, or someone alleges negligence in property maintenance-these scenarios create lawsuit exposure that homeowners policies do not address. The higher liability limits in landlord policies reflect the reality that rental properties attract more foot traffic and generate more potential claims than owner-occupied homes. You should never accept the minimum liability limit your lender requires; instead, choose $500,000 or higher if your property produces substantial rental income or sits in a densely populated area. The premium difference between $300,000 and $1 million in liability coverage typically costs only $50 to $100 annually, making the upgrade financially sensible for most landlords.

Loss of Rent Coverage: Your Financial Safety Net

Loss of fair rental value coverage pays your monthly rent if a covered event makes the property uninhabitable during repairs. This coverage component has no homeowners insurance equivalent and offers no alternative if you remain underinsured. A pipe burst, electrical fire, or severe storm damage does not just cost repair money-it stops tenant occupancy and your rental income simultaneously. Loss of rent coverage typically reimburses the fair rental value for the shortest reasonable time to repair, usually 12 to 24 months maximum depending on your policy. A property producing $2,000 monthly rent that requires three months of repairs triggers $6,000 in reimbursement, protecting you from absorbing that income gap while contractors work. Minnesota landlords should carry loss of rent coverage equal to at least three months of rental income, and six months proves better if your property takes time to re-rent after repairs finish. This coverage does not reimburse you for tenant non-payment or market rent declines, only for income loss from covered perils that make the property temporarily uninhabitable.

Actual Cash Value Versus Replacement Cost

The difference between actual cash value and replacement cost coverage also matters more with rental properties because landlord policies that pay replacement cost cover the full current cost to repair or rebuild, while actual cash value policies pay replacement cost minus depreciation. This gap can leave you thousands out of pocket on aging components like roofs or HVAC systems. A 20-year-old roof that costs $8,000 to replace might receive only $3,000 under actual cash value coverage, forcing you to cover the remaining $5,000 yourself. When you shop policies, verify that loss of rent is included and ask specifically whether the limit covers your estimated annual rental income multiplied by your expected repair timeline for your property’s age and condition. You should also confirm whether your dwelling coverage uses replacement cost or actual cash value, as this choice directly impacts your out-of-pocket expenses after a loss.

The next chapter walks you through how to select the right rental property insurance by assessing your specific property needs and comparing quotes from multiple carriers in Minnesota.

How to Select the Right Rental Property Insurance

Calculate Your Property’s True Replacement Cost

Start with your property’s replacement cost, not its market value. Market value includes land, which insurance does not cover, while replacement cost reflects only the structure itself. A Minnesota property worth $350,000 might cost only $220,000 to rebuild if land comprises 40 percent of the purchase price. Contact local contractors or use the Marshall & Swift cost estimator to determine square footage rebuild costs in your area, typically ranging from $120 to $180 per square foot depending on construction quality and regional labor rates.

Your mortgage lender will demand dwelling coverage matching at least 80 percent of replacement cost, but you should insure for 100 percent to avoid out-of-pocket expenses after a total loss.

Determine Loss of Rent and Coverage Limits

Calculate your loss of rent coverage by multiplying monthly rental income by the number of months your property typically takes to repair after a covered loss. A property generating $1,800 monthly rent that historically requires four months for major repairs needs $7,200 in loss of rent coverage. Add 20 percent to this figure as a safety margin, bringing the recommendation to $8,640. Many Minnesota landlords underestimate repair timelines and carry insufficient loss of rent limits, leaving themselves exposed when contractors face material delays or weather interruptions. Document your property’s age, square footage, number of bedrooms and bathrooms, roof condition, HVAC system age, electrical and plumbing updates, and any prior claims history before obtaining quotes. Insurers use these factors heavily when pricing DP-3 policies, and accurate information prevents quote surprises later.

Obtain Quotes From Multiple Carriers

Obtain quotes from at least three different carriers rather than accepting the first offer. Travelers, Progressive, Safeco, and Foremost all write DP-3 policies in Minnesota, and premium differences of $300 to $500 annually between carriers are common for identical coverage. Work with a local independent agent who can access multiple companies simultaneously rather than calling each insurer separately, saving substantial time and effort. Specify that you want replacement cost dwelling coverage, not actual cash value, and confirm loss of rent limits match your calculated needs before comparing prices. Ask each insurer whether installing security features like burglar alarms or fire sprinklers qualifies for premium discounts, as these upgrades typically reduce annual premiums by 10 to 15 percent. A $150 annual discount on a security system that costs $400 to install pays for itself in under three years while protecting your property beyond just insurance benefits.

Review Written Quotes and Lender Requirements

Request written quotes showing dwelling coverage limits, loss of rent amounts, liability limits, deductibles, and any exclusions specific to Minnesota properties. Verbal quotes lack accountability and often change when you actually bind coverage. Compare the total annual cost of each quote multiplied by your expected holding period to understand the long-term investment. A policy costing $200 more annually than a competitor’s offer but providing superior loss of rent coverage and lower deductibles might save you thousands if a claim occurs. Your mortgage lender’s insurance requirements also influence your selection. Most Minnesota lenders require minimum dwelling coverage equal to the loan amount and demand that the lender be named as mortgagee on the policy. Verify whether your lender imposes specific liability minimums or requires particular coverage endorsements before finalizing quotes, as some lenders demand non-occupied dwelling coverage if the property sits vacant for more than 30 days. This requirement matters for landlords managing seasonal rentals or properties between tenants.

Balance Cost Against Coverage Quality

Never select a policy based solely on the lowest premium; instead, balance cost against coverage completeness and the insurer’s claims handling reputation in Minnesota. A policy $400 cheaper annually provides no value if the insurer denies a major claim due to coverage gaps or poor claims service delays your repairs for months.

Final Thoughts

Homeowners insurance for rental property and standard homeowners coverage serve fundamentally different purposes. Standard homeowners policies exclude rental income, tenant liability, and landlord-owned equipment, leaving you financially exposed on the exact risks that matter most. Landlord insurance fills these gaps with dwelling coverage at replacement cost, higher liability limits ranging from $300,000 to $1 million, and loss of rent protection that reimburses your income during repairs.

Proper coverage transforms a rental property from a financial gamble into a protected investment. Without loss of rent coverage, a three-month repair timeline costs you $4,500 to $6,000 in lost income on a typical Minnesota rental. Without adequate liability limits, a single injury claim from a tenant or guest can exceed your policy’s protection. Without replacement cost dwelling coverage, aging components like roofs or HVAC systems leave you absorbing depreciation costs after a loss.

Contact us at Variant Insurance Group to discuss your rental property’s insurance needs and receive personalized quotes that reflect your actual replacement costs and income protection requirements. Our team compares protection and prices across Minnesota’s top-rated carriers so you receive the best possible value without coverage gaps. We specialize in shopping landlord insurance policies that match your specific property and budget.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation