Your home insurance personal property coverage protects the belongings inside your house-from furniture and electronics to clothing and kitchen appliances. Most Minnesota homeowners don’t realize how much their possessions are actually worth until they need to file a claim.

At Variant Insurance Group, we help homeowners understand exactly what their policy covers and whether they have enough protection. This guide walks you through the types of coverage available, how to calculate the right amount, and what steps to take next.

What Personal Property Coverage Actually Protects

Personal property coverage is the part of your homeowners policy that pays to repair or replace your belongings if they’re damaged or stolen in a covered loss. This includes furniture, electronics, clothing, kitchen appliances, tools, and nearly everything else inside your home. The coverage applies whether damage happens from fire, theft, wind, hail, or other covered perils-depending on the type of policy you have.

However, personal property coverage has important limits and exclusions. Cars, motorized vehicles, pets, and equipment used for a home-based business are not covered. If you run a business from home, you need to disclose this to your insurer because standard personal property coverage won’t protect business equipment or inventory. Most Minnesota homeowners underestimate what their belongings are worth, which means they often carry too little coverage.

Research shows that the average homeowner has only about 40% of the coverage they actually need to fully replace their possessions after a total loss.

How Much Coverage You Actually Get

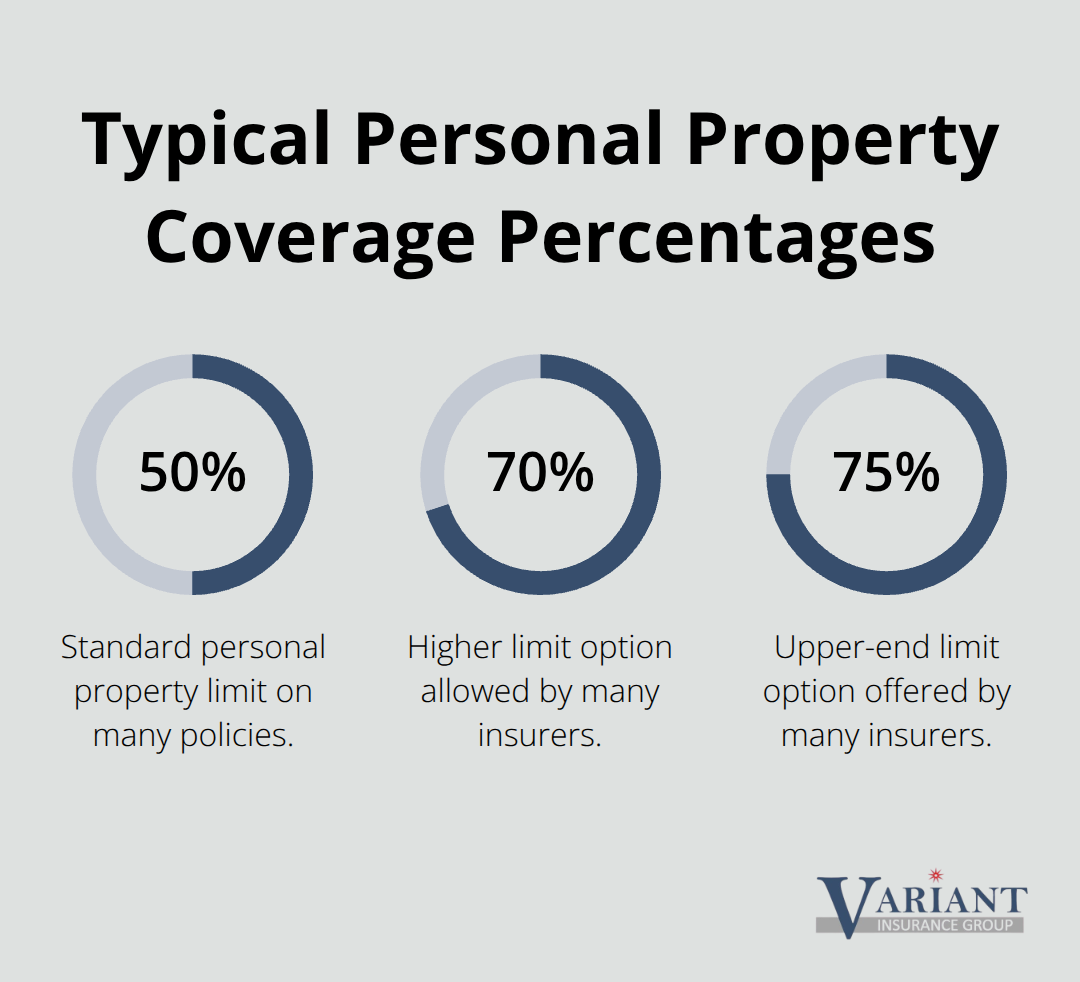

Personal property coverage is typically limited to 50% of your dwelling coverage amount. If your home’s replacement value is $300,000 and your dwelling coverage is set at $240,000, your personal property coverage would be $120,000. While you can request higher limits-many insurers allow you to increase personal property coverage to 70% or 75% of your dwelling amount-most policies cap coverage for specific items.

Jewelry is capped at $1,000 to $1,500 in most standard policies, which falls far short if you own engagement rings, watches, or other valuables. Money and securities are typically limited to $200 to $500. Firearms often have separate limits around $2,500. Your deductible applies to personal property claims just like it does to your home. If you have a $1,000 deductible and file a claim for $3,000 in damaged belongings, you receive $2,000.

The Deductible Trade-Off

Choosing a higher deductible lowers your premium but increases your out-of-pocket cost when you need to file a claim. The tradeoff matters most for people who have emergency savings and can afford to absorb larger losses.

Replacement Cost Versus Actual Cash Value

Minnesota law requires insurers to tell you whether your personal property coverage pays replacement cost or actual cash value. Replacement cost coverage pays what it costs to buy new items similar to what you lost, without subtracting for depreciation. Actual cash value subtracts depreciation, so a five-year-old television worth $800 new might only be worth $300 when it’s damaged.

The difference is substantial. A ten-year-old couch that cost $2,000 might have an actual cash value of just $400 because of age and wear. With actual cash value coverage, you receive $400. With replacement cost coverage, you receive enough to buy a comparable new couch. Replacement cost coverage costs more in premiums but protects you far better.

If your policy uses actual cash value for personal property, the declarations page must state this clearly. If you’re unsure which type you have, contact your agent immediately. For high-value items like jewelry, art, or collections, you may need a special endorsement or floater that insures those items separately at replacement cost, regardless of what your main policy provides. These endorsements protect your most valuable possessions and set the stage for understanding how much total coverage you actually need.

Which Coverage Type Protects You Better

Replacement Cost Versus Actual Cash Value

The type of personal property coverage you choose determines how much you actually receive when you file a claim. Replacement cost coverage pays what it costs to buy new items without deducting for depreciation, while actual cash value subtracts depreciation based on age and condition. The difference is dramatic. A ten-year-old laptop that cost $1,200 might have an actual cash value of $300 but a replacement cost value of $1,000 or more for a comparable new model. With actual cash value coverage, you walk away with $300. With replacement cost coverage, you get enough to actually replace the laptop.

Minnesota law requires your insurer to clearly state on your declarations page which type you have, so check your policy immediately. If you have actual cash value coverage and own items more than five years old, you’re significantly underinsured. Replacement cost coverage costs more in premiums-typically 10 to 15 percent higher-but the protection is substantially better. Most Minnesota homeowners should choose replacement cost coverage unless they’re on an extremely tight budget.

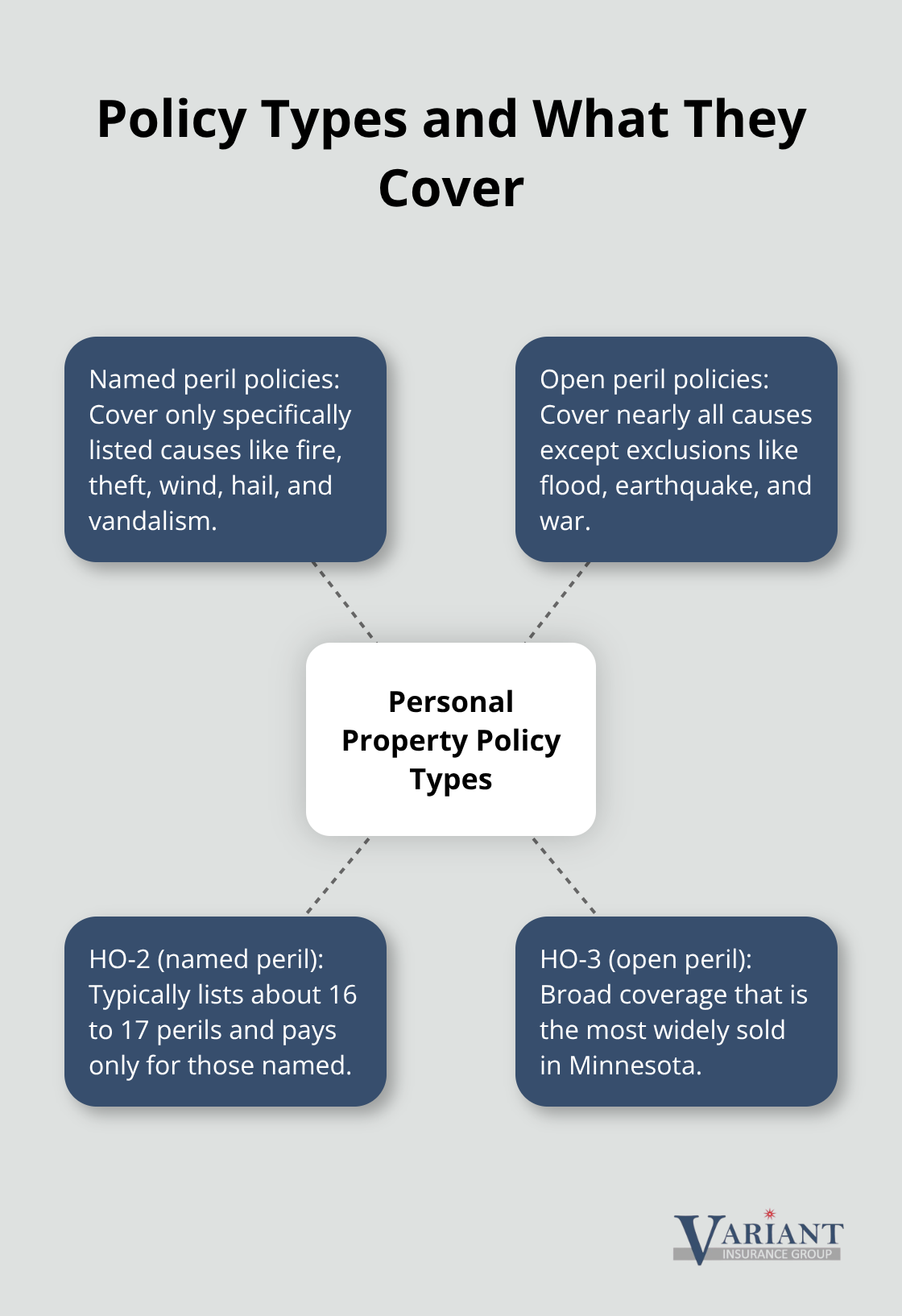

Named Peril Versus Open Peril Policies

Named peril policies and open peril policies work differently and affect what gets covered. Named peril policies cover only specific perils listed in the policy, such as fire, theft, wind, hail, and vandalism. An HO-2 named peril policy covers about 16 to 17 perils, but if damage comes from a peril not listed, you receive nothing. Open peril policies, typically HO-3 forms, cover nearly all perils except specific exclusions like flood, earthquake, and war.

Open peril coverage is far superior because it protects against unexpected losses not explicitly listed. For example, if a guest accidentally breaks a valuable piece of art while visiting, an open peril policy covers it while a named peril policy might not. HO-3 policies are the most widely sold homeowners policies in Minnesota because they offer this broader protection with simpler terms.

Special Endorsements and Floaters for High-Value Items

Special endorsements and floaters provide additional protection for high-value items that exceed standard policy limits. Jewelry floaters insure rings, watches, and other valuables at replacement cost without the typical $1,000 to $1,500 cap. Art and antiques floaters cover collections at appraised values. Electronics endorsements protect expensive computers and entertainment systems. These endorsements cost extra but are essential if you own items worth more than your policy’s sub-limits. Without them, you’re relying on depreciated actual cash value payments that won’t cover replacement. Once you understand which coverage types work best for your situation, the next step involves calculating exactly how much personal property coverage you actually need.

Calculating How Much Personal Property Coverage You Actually Need

Start by listing every item in your home room by room, including the attic, basement, and garage. Most Minnesota homeowners drastically underestimate their belongings’ value until they physically inventory them. Walk through your kitchen and add up appliances: a refrigerator costs $1,500 to $3,000, a dishwasher $700 to $1,200, and a range $800 to $2,500.

Your bedroom furniture, mattress, and clothing easily reach $5,000 to $8,000. Electronics in the living room-television, sound system, gaming console-quickly total $2,000 to $4,000. Include items you don’t think about daily: tools in the garage, sports equipment, hobby supplies, seasonal decorations, and kitchen gadgets. Most households find their total personal property value ranges from $80,000 to $150,000 when they actually count everything.

The Coverage Gap Most Homeowners Face

If your home’s replacement value is $300,000 and you have the standard 50% personal property limit, your coverage sits at $150,000-which sounds adequate until you realize you’re one fire away from losing thousands in uninsured items. Travelers insurance research shows that most standard policies cap jewelry at $1,000 to $1,500, yet the average homeowner with engagement rings and watches owns significantly more in valuables. Money and securities typically have $200 to $500 limits. Firearms often cap at $2,500. These sub-limits create dangerous gaps between what you own and what your policy covers.

Document Everything Before You Need It

Photograph or video record every room, including closets and drawers. Include receipts or appraisals with your inventory-this documentation makes claims processing faster and proves the value of items you’ve owned for years. Store your inventory digitally on a cloud service and keep a printed copy in a safe deposit box. Most people wait until after a loss to remember what they owned, which makes it impossible to prove value.

The Minnesota Department of Commerce provides a home inventory worksheet to help you organize belongings systematically. Once you have your total, compare it to your current personal property limit. If the gap is significant, increase your coverage to 70% or 75% of your dwelling amount rather than the standard 50%. This costs slightly more in premiums but prevents catastrophic underinsurance.

Protect High-Value Items With Scheduled Endorsements

For items exceeding your policy’s sub-limits-jewelry worth $5,000, art collections, expensive electronics-purchase scheduled personal property endorsements. These floaters insure specific items at their appraised replacement cost, bypassing the standard caps entirely. An engagement ring appraisal costs $100 to $300 and qualifies for a jewelry floater that covers its full value. Without this endorsement, you’re limited to that inadequate $1,000 cap regardless of actual worth.

Final Thoughts

Personal property coverage protects your belongings, but only if you understand what your policy covers and whether the limits match what you own. Most Minnesota homeowners carry far too little coverage because they’ve never inventoried their possessions or reviewed their policy limits. Start by walking through your home and documenting everything room by room, including closets, the garage, basement, and attic-this inventory reveals the true value of your belongings and shows whether your current home insurance personal property coverage is adequate.

Review your policy declarations page to confirm whether you have replacement cost or actual cash value coverage, since replacement cost protects you far better by paying what new items cost without depreciation deductions. Check the sub-limits for jewelry, money, securities, and firearms, and if you own valuables exceeding these caps, purchase scheduled endorsements or floaters to cover them at full replacement cost. Compare your total personal property value to your current coverage limit, and if the gap is significant, increase your limit to 70% or 75% of your dwelling coverage rather than accepting the standard 50%.

Variant Insurance Group helps Minnesota homeowners review their home insurance coverage and find the right protection for their specific situation. Contact us to review your current policy and make adjustments before you need to file a claim.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation