Minnesota homeowners pay an average of $1,847 annually for homeowners insurance, which sits 15% below the national average of $2,151. Understanding how much homeowners insurance costs in your specific area helps you budget effectively.

We at Variant Insurance Group know that rates vary significantly across the state based on your home’s location, value, and personal risk factors. Smart shopping and policy adjustments can reduce your premiums substantially.

What Do Minnesota Homeowners Actually Pay?

Minnesota homeowners spend an average of $1,847 per year on homeowners insurance, which breaks down to roughly $154 monthly. This places Minnesota homeowners in a favorable position compared to the national average of $2,151 annually. The National Association of Insurance Commissioners data shows Minnesota ranks among the more affordable states for homeowners insurance, with premiums that run approximately 14% below national rates.

Minnesota Beats Most Midwest Neighbors

Minnesota outperforms most surrounding Midwest states when it comes to homeowners insurance costs. Wisconsin homeowners pay an average of $1,950 annually, while Iowa residents face $2,100 per year. North Dakota homeowners see the highest rates in the region at $2,300 annually.

Only South Dakota offers lower premiums than Minnesota at $1,650 per year.

These regional differences stem from weather patterns, construction costs, and state insurance regulations that vary across the Midwest. Minnesota’s competitive insurance market and relatively stable weather (compared to tornado-prone areas) keep rates reasonable for homeowners throughout the state.

Payment Options Impact Your Budget

Most Minnesota insurers offer both monthly and annual payment plans, but annual payments typically save you 3-5% on total premiums. State Farm and other major carriers charge processing fees for monthly payments that can add $50-100 to your yearly costs. Annual payments eliminate these fees and often qualify you for additional discounts.

However, many homeowners prefer to spread the $1,847 average cost over 12 months at $154 monthly, which makes budget management easier despite the slight premium increase. The choice between monthly convenience and annual savings depends on your cash flow preferences and financial planning approach.

These statewide averages provide a baseline, but your actual premium depends on several specific factors that insurance companies evaluate when they calculate your individual rate.

What Drives Your Minnesota Insurance Rate

Your home’s replacement cost determines the foundation of your premium calculation. Minnesota insurance companies evaluate your home’s square footage, construction materials, and local rebuilding costs to set coverage limits. A 2,000-square-foot home in Minneapolis costs approximately $150 per square foot to rebuild, while rural areas see costs around $120 per square foot. Insurance companies adjust premiums based on these rebuilding expenses, which explains why identical homes in different counties carry different rates.

Weather Risks Shape Your Premium

Minnesota’s severe weather patterns directly impact your insurance costs. Rising insurance rates are due to extreme weather, increased reinsurance costs, and higher labor and supply costs for repairs. Homes in the Twin Cities metro area face higher premiums due to frequent hailstorms, while northern Minnesota properties see lower rates despite harsh winters.

Flood risk adds another layer of complexity since 40% of Minnesota flood claims over the past 30 years originated outside designated high-risk zones. Insurance companies now use advanced mapping technology to assess flood probability for individual properties, often resulting in premium adjustments that homeowners don’t expect.

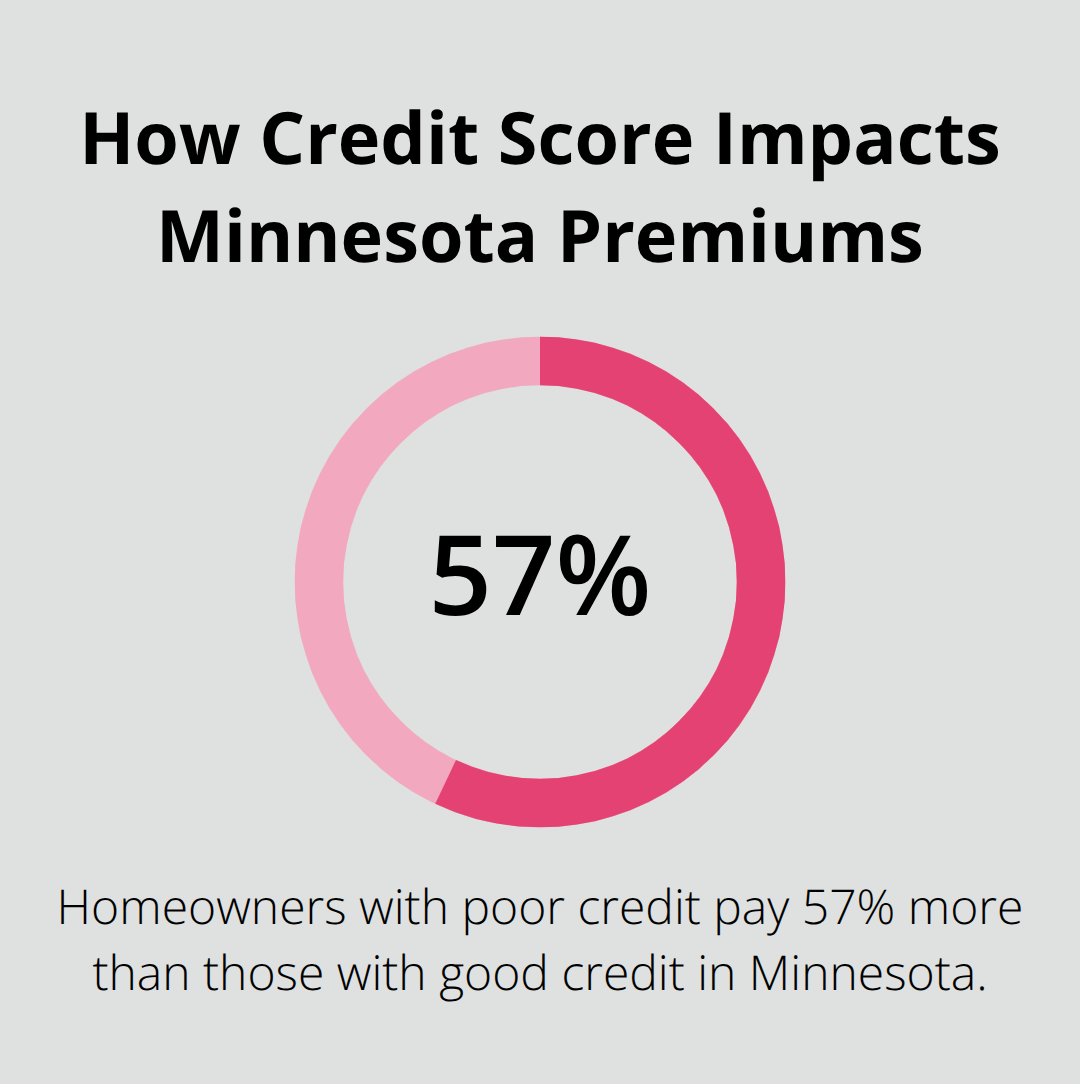

Your Credit Score Controls Your Rate

Minnesota insurers legally use credit scores to calculate premiums, and the impact is substantial. Homeowners with poor credit pay an average of $4,585 annually compared to $2,920 for those with good credit scores. This 57% difference means improving your credit score from fair to good can save you over $1,600 yearly.

Claims History Affects Future Rates

Filing two claims within three years typically increases your premium by 25-40%, while claim-free homeowners often receive discounts of 10-15% after five years without incidents. Insurance companies track your claims history carefully and adjust rates accordingly (even for claims that weren’t your fault).

Smart homeowners who understand these rate factors can take specific steps to reduce their premiums through strategic policy choices and available discounts.

How Can You Cut Your Minnesota Homeowners Insurance Costs

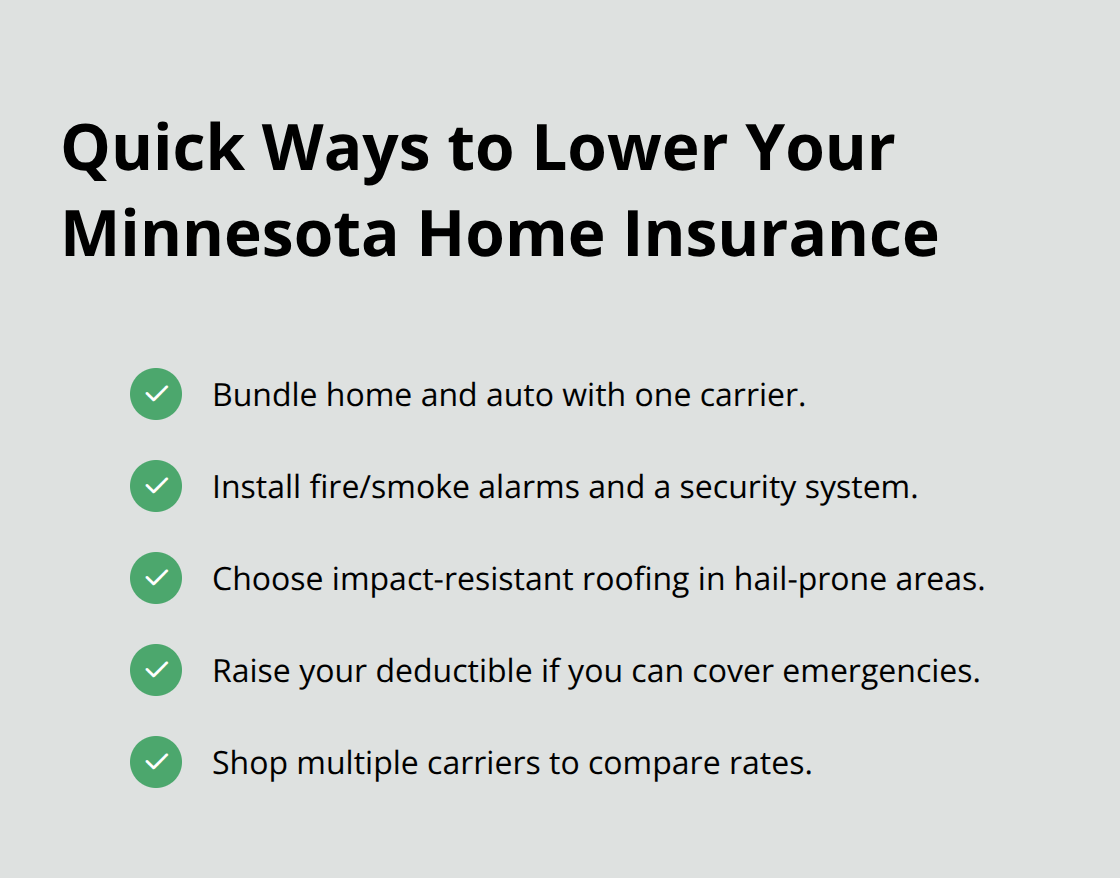

Bundle Policies for Maximum Savings

Bundling your home and auto insurance with the same carrier delivers the most reliable premium reduction available to Minnesota homeowners. State Farm offers bundling discounts that reduce combined premiums by 15-25%, while Allstate provides similar savings of 20-30% for multi-policy customers. Most carriers reward customers who consolidate multiple policies, with annual savings that typically range from $400-600 for Minnesota homeowners.

Install Safety Features That Pay for Themselves

Insurance companies reward Minnesota homeowners who invest in protective devices with substantial premium reductions. Fire and smoke alarms reduce rates by 5-10%, while comprehensive security systems can cut premiums by 15-20%. State Farm provides smart home devices like the Ting electrical monitoring system to prevent electrical fires, which qualifies for additional discounts.

Impact-resistant roofing materials designed for hail protection can reduce premiums by 10-15% in storm-prone areas like the Twin Cities metro. These materials protect your home from Minnesota’s frequent hailstorms while lowering your insurance costs over time.

Raise Your Deductible Strategically

Increasing your deductible from $500 to $1,000 typically reduces premiums by 12-15%, while jumping to $2,500 can save you 25-30% according to Minnesota Department of Commerce data. A homeowner paying the state average of $1,847 annually could save $462-554 yearly with a higher deductible.

However, maintain enough emergency savings to cover the higher out-of-pocket costs if you need to file a claim. This strategy works best for homeowners who rarely file claims and can handle larger upfront expenses.

Shop Multiple Carriers for Best Rates

Rates vary dramatically between companies for identical coverage in Minnesota. State Farm has higher average rates at $2,351 per year, while Chubb provides comprehensive coverage for high-value homes (though at higher rates). USAA delivers excellent rates for military families at 4.8 stars, but restricts eligibility to service members and veterans.

Cincinnati Insurance provides unique benefits like green upgrade endorsements for eco-friendly repairs, while Amica maintains strong customer service ratings with fewer complaints than industry averages.

Final Thoughts

Minnesota homeowners pay an average of $1,847 annually for homeowners insurance, which places the state 15% below national rates. Premium differences between carriers can exceed $500 annually for identical coverage. State Farm averages $2,351 yearly while other insurers offer significantly lower rates for the same protection.

Your specific rate depends on home value, location risks, credit score, and claims history. Strategic choices like policy bundling, safety feature installation, and higher deductibles can cut premiums by 20-30% or more. Smart homeowners who understand how much is homeowners insurance in their area make better decisions about coverage and costs.

We at Variant Insurance Group shop Minnesota’s top-rated insurance companies to find the perfect policy for our clients. As an independent agency, we compare protection and prices across multiple carriers to get you the best possible value. Contact us today to see how much you can save on your Minnesota homeowners insurance (and get the coverage you actually need).