Hosting on Airbnb can generate solid income, but it comes with real liability risks that most hosts underestimate. Your guests could get injured on your property, damage your belongings, or cause harm to neighbors-and Airbnb’s built-in protection has significant gaps.

At Variant Insurance Group, we’ve seen too many Minnesota hosts discover these coverage holes only after a claim gets denied. Standard homeowners policies typically exclude short-term rental activity entirely, leaving you exposed to financial disaster.

This guide walks you through what Airbnb liability coverage actually includes, where it falls short, and how to protect your business properly.

What Airbnb’s Host Protection Actually Covers

The Coverage Limits and How They Work

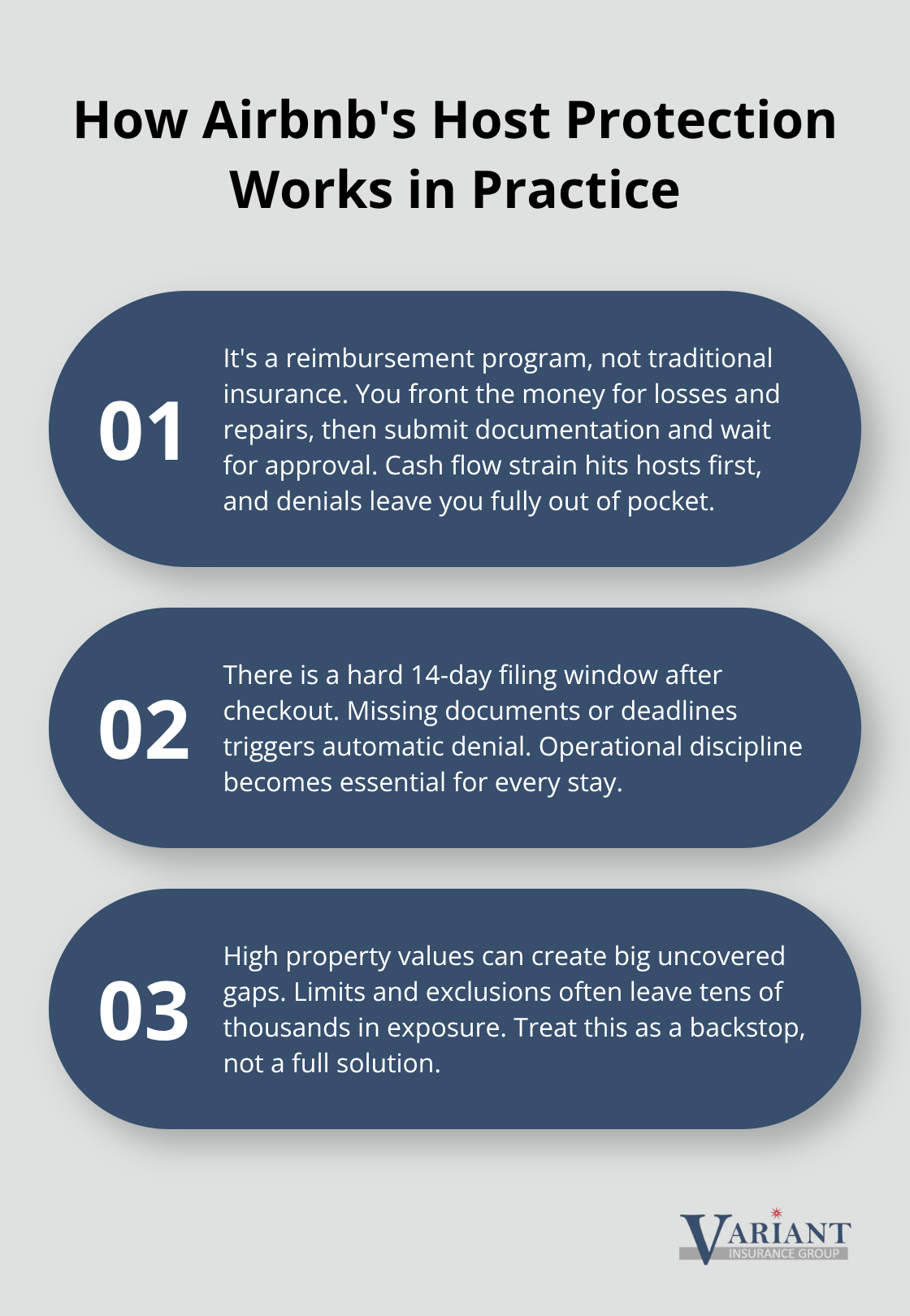

Airbnb’s Host Protection Insurance provides up to $1,000,000 for host liability and up to $3,000,000 for guest-caused property damage, which sounds comprehensive until you file a claim. The reality is far more restrictive. This coverage operates as a reimbursement program processed through Zurich, not traditional insurance, meaning you pay out of pocket first and hope Airbnb approves your claim later. You must file within 14 days of checkout with complete documentation, or the claim gets denied automatically. Minnesota hosts with properties valued between $200,000 and $500,000 often assume this coverage is sufficient, but it leaves critical gaps that can cost tens of thousands of dollars.

What Actually Gets Covered

Guest injuries on your property and property damage from guest negligence receive coverage under Airbnb’s program, along with some liability incidents. However, the exclusions create far more problems than the coverage solves for Minnesota operators. Airbnb explicitly excludes wear and tear, weather-related damage, mold, long-term liability, and intentional guest damage. If a guest steals your television or high-end kitchen equipment, you receive no reimbursement unless they broke down a door to get it.

The Real Financial Exposure

A burst pipe or kitchen fire that forces you to cancel bookings for three months leaves you with zero income protection from Airbnb. The Minnesota Department of Commerce reports that guest injuries can lead to six-figure damages in premises liability cases, yet Airbnb’s $1,000,000 limit may not adequately cover significant incidents at high-value properties. Kitchen and bathroom repairs in Minnesota short-term rentals commonly range from $3,000 to $8,000, and property damage claims occur regularly during short-term rental operations.

This frequency means you need protection that covers what happens regularly, not just catastrophic scenarios. Airbnb’s coverage functions as a starting point, but serious Minnesota hosts cannot rely on it as their foundation for protection. The gaps in this program create the need for additional specialized coverage that actually addresses the risks you face every day.

Why Your Homeowners Policy Won’t Cover Your Airbnb

Standard Policies Exclude Short-Term Rental Activity

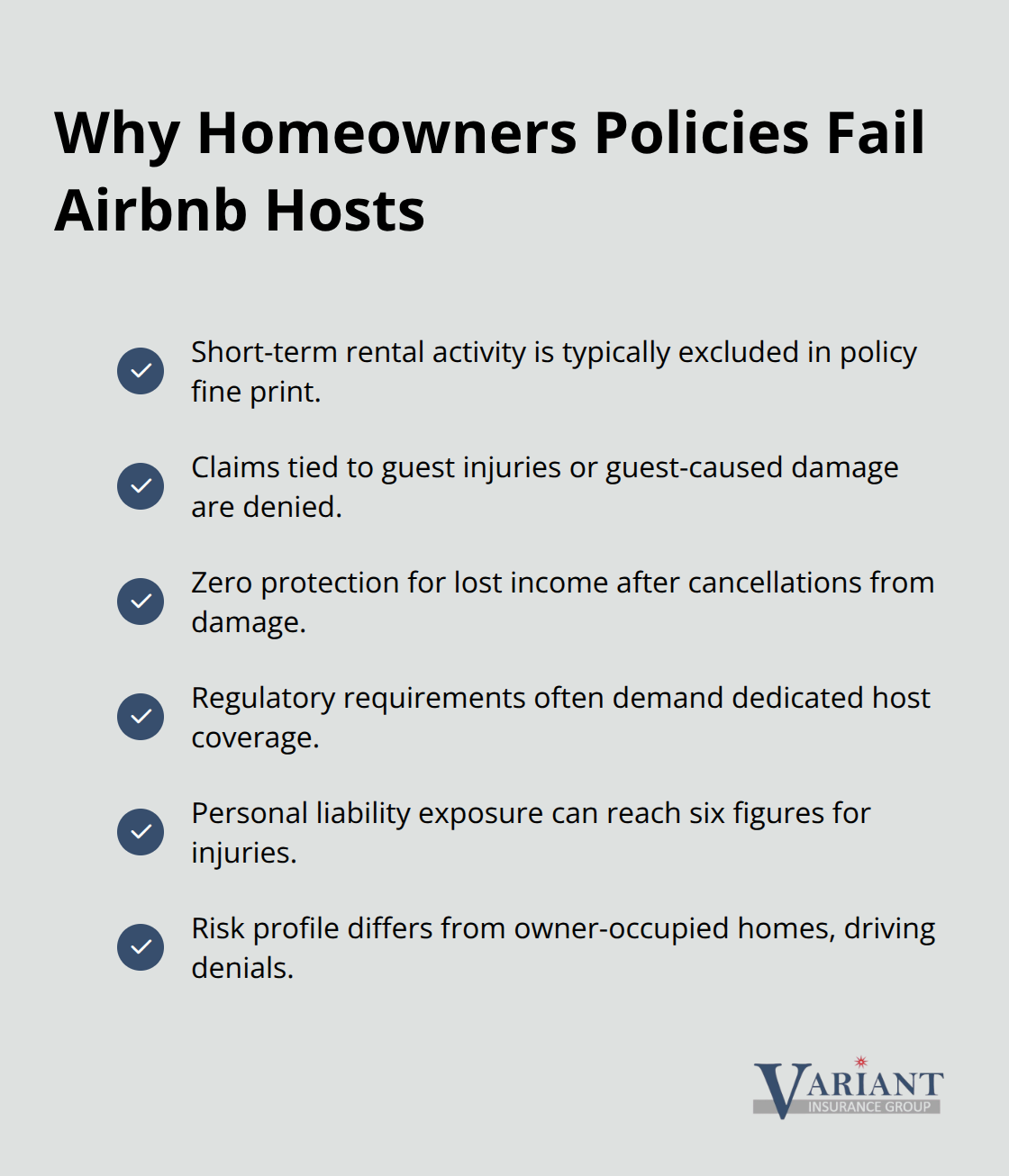

Your homeowners insurance policy was designed for owner-occupied homes, not income-generating rental operations. The moment you list your property on Airbnb, your standard policy becomes essentially worthless for the activities that generate your revenue. Most homeowners policies in Minnesota explicitly exclude short-term rental activity in their fine print, meaning your insurer will deny any claim related to guest injuries, property damage from guests, or liability incidents connected to your hosting business. This exclusion applies even if a guest breaks a leg on your stairs or causes a fire that damages your kitchen. Standard homeowners policies leave hosts personally liable for guest injuries, creating immediate financial exposure that can reach six figures in premises liability cases.

Insurance companies take this exclusion seriously because short-term rentals represent fundamentally different risk profiles than traditional home ownership. Your property experiences constant turnover, strangers access your belongings, and you have minimal control over guest behavior. An insurer that accepted this risk at standard homeowners rates would face catastrophic losses. When you file a claim after a guest incident, your insurance company reviews your policy, discovers the short-term rental exclusion, and denies coverage entirely. You learn about this protection gap only when you need it most.

Weather and Property Damage Leave You Unprotected

The financial consequences of operating without proper coverage extend far beyond property damage or guest injuries. If a burst pipe or kitchen fire makes your rental uninhabitable, Airbnb’s reimbursement program offers zero protection for lost income during the cancellation period. Your standard homeowners policy will not cover this loss either, since the damage occurred to a rental property.

Local Regulations Require Specific Coverage

Many Minnesota municipalities now require proof of specific host insurance coverage as a condition of operating legally, meaning Airbnb’s coverage alone fails to meet local regulatory requirements in your area. This regulatory gap creates additional liability exposure that most hosts overlook until a city inspector or licensing board raises the issue.

Specialized Coverage Fills the Gaps

Specialized short-term rental insurance addresses these gaps by covering guest-caused property damage, comprehensive liability for on-premises and off-premises guest activities, theft protection without forced-entry requirements, and loss of rental income with no arbitrary time limits on claims. The cost of comprehensive short-term rental coverage for Minnesota properties varies based on location and property features. Properties in lake areas see premiums higher due to water damage and liability exposure, while urban listings face higher premiums than suburban properties. This targeted coverage transforms your financial exposure from potentially catastrophic to manageable and predictable.

The gap between what your homeowners policy covers and what your Airbnb operation actually needs creates a dangerous blind spot. Understanding this gap is the first step toward protecting yourself, but knowing the gap exists and actually closing it are two different things. The next section explores the specialized insurance options available to Minnesota hosts and how to evaluate which coverage truly matches your property and business model.

Getting the Right Coverage for Your Rental Property

Why Specialized Insurance Matters for Minnesota Hosts

Specialized short-term rental insurance exists because standard policies and Airbnb’s reimbursement program cannot protect your income or your property adequately. Proper Insurance, which Vrbo exclusively endorses, represents the gold standard for Minnesota hosts because it addresses every gap that standard coverage leaves open. The policy includes commercial general liability starting at $1,000,000 per occurrence, building and contents coverage using replacement cost with no occupancy restrictions, business revenue protection that reimburses actual income loss from covered claims with no arbitrary time limits, property entrustment coverage protecting against guest theft without forced-entry requirements, and amenity liability extending to off-premises activities like kayaks and hot tubs. This comprehensive approach transforms your financial exposure from catastrophic to manageable.

Understanding Pricing and Location Factors

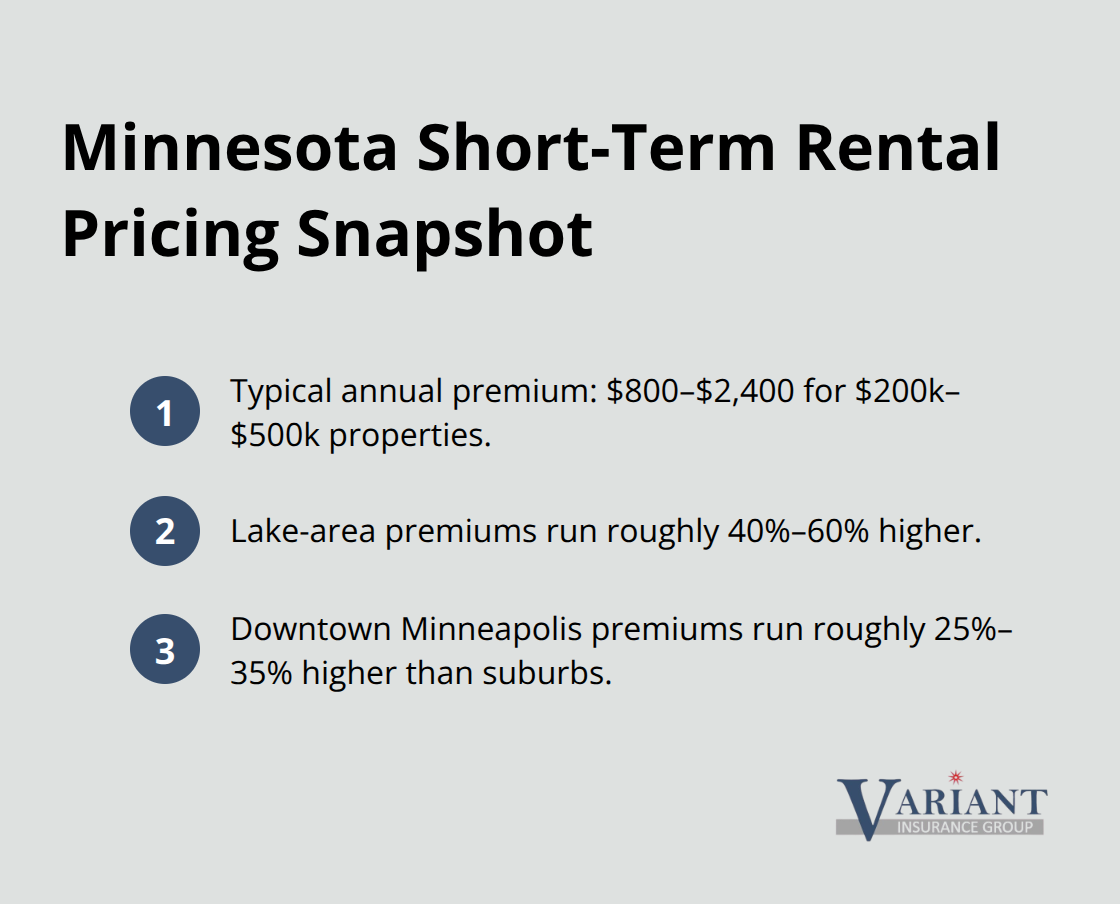

For Minnesota properties valued between $200,000 and $500,000, comprehensive short-term rental coverage typically costs $800 to $2,400 annually, though location significantly affects your premium. Lake-area properties in places like Duluth see premiums 40 to 60 percent higher due to water damage exposure, and downtown Minneapolis listings face premiums 25 to 35 percent higher than suburban properties due to density and foot traffic. Your specific location within Minnesota creates measurable differences in what you’ll pay for the same coverage level.

Comparing Policies Beyond the Premium Quote

Comparing policies requires moving beyond premium quotes to evaluate what actually gets covered when you file a claim. Airbnb’s 14-day reporting requirement means missed deadlines result in automatic denial, whereas Proper’s business revenue protection covers lost income with no time limit on actual loss sustained. If your property has high-value furnishings or unique amenities like pools or hot tubs, verify that the policy explicitly includes amenity liability rather than treating these features as exclusions. Deductible choices significantly impact your total cost and out-of-pocket exposure per claim, so calculate whether a $500 deductible or $1,000 deductible aligns with your financial situation.

Critical Questions to Ask Your Agent

Ask your agent whether the policy covers loss of bookings from non-guest events like kitchen fires or burst pipes, since Airbnb provides zero protection for these scenarios. Confirm that coverage remains active during vacancy periods if you operate seasonally, reducing cash-flow gaps during Minnesota winters. Document your property’s replacement cost for the building, furnishings, and appliances, then compare these figures against policy limits to confirm adequate coverage. Calculate your average monthly rental income during peak season and assess how much lost revenue would create financial hardship, then ensure your business revenue limits match this figure. Verify that the insurer covers your specific property type and whether occupancy restrictions align with your hosting schedule, since some policies contain hidden limitations that emerge only after you purchase coverage.

Final Thoughts

Protecting your Airbnb business in Minnesota requires moving beyond Airbnb’s built-in protection and your standard homeowners policy. Airbnb liability coverage provides a foundation, but the 14-day filing deadline, theft exclusions without forced entry, and zero income protection during property damage create gaps that will cost you thousands of dollars when claims arise. Your homeowners policy actively excludes short-term rental activity, leaving you personally liable for guest injuries that can reach six figures in premises liability cases.

The financial reality is straightforward: comprehensive short-term rental insurance costs $800 to $2,400 annually for Minnesota properties valued between $200,000 and $500,000, depending on your location and property features. This investment protects your income when burst pipes or kitchen fires force cancellations, covers guest theft without forced-entry requirements, and provides liability protection for amenities like hot tubs and kayaks. Lake-area properties and downtown urban listings face higher premiums due to water damage exposure and foot traffic density, but the coverage remains essential regardless of location.

Start by calculating your property’s replacement cost and your average monthly rental income during peak season-these figures determine the coverage limits you actually need rather than settling for whatever a generic quote suggests. Contact your current homeowners insurer and ask directly whether your policy covers short-term rental activity, then request written confirmation of their answer. We at Variant Insurance Group work with Minnesota hosts to compare Airbnb liability coverage against dedicated short-term rental policies from carriers like Proper Insurance, which Vrbo exclusively endorses, and we shop Minnesota’s top-rated insurance companies to find the coverage that matches your property type, hosting schedule, and financial situation.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation