One lawsuit or serious accident could wipe out years of financial progress. Standard homeowners and auto policies typically cap liability coverage at $300,000 to $500,000-far below what you might owe if someone is severely injured on your property or in an accident you cause.

Umbrella liability insurance in Minnesota fills this gap by providing an extra layer of protection for your personal assets. At Variant Insurance Group, we help Minnesota residents understand how this coverage works and why it matters for their financial security.

Understanding Umbrella Liability Insurance

Umbrella liability insurance is straightforward: it activates after your homeowners or auto policy limits are exhausted. According to the National Association of Insurance Commissioners, an umbrella policy covers bodily injury, property damage, and personal injury claims that exceed what your underlying policies will pay. In Minnesota, most umbrella policies start at $1 million in coverage, with higher limits available up to $5 million or more depending on your assets and risk profile. The coverage operates separately from your home and auto policies, meaning it activates only when those policies reach their limits. If someone sues you for $750,000 in damages and your homeowners policy covers $300,000, your umbrella policy covers the remaining $450,000 plus legal defense costs.

What Umbrella Coverage Actually Protects

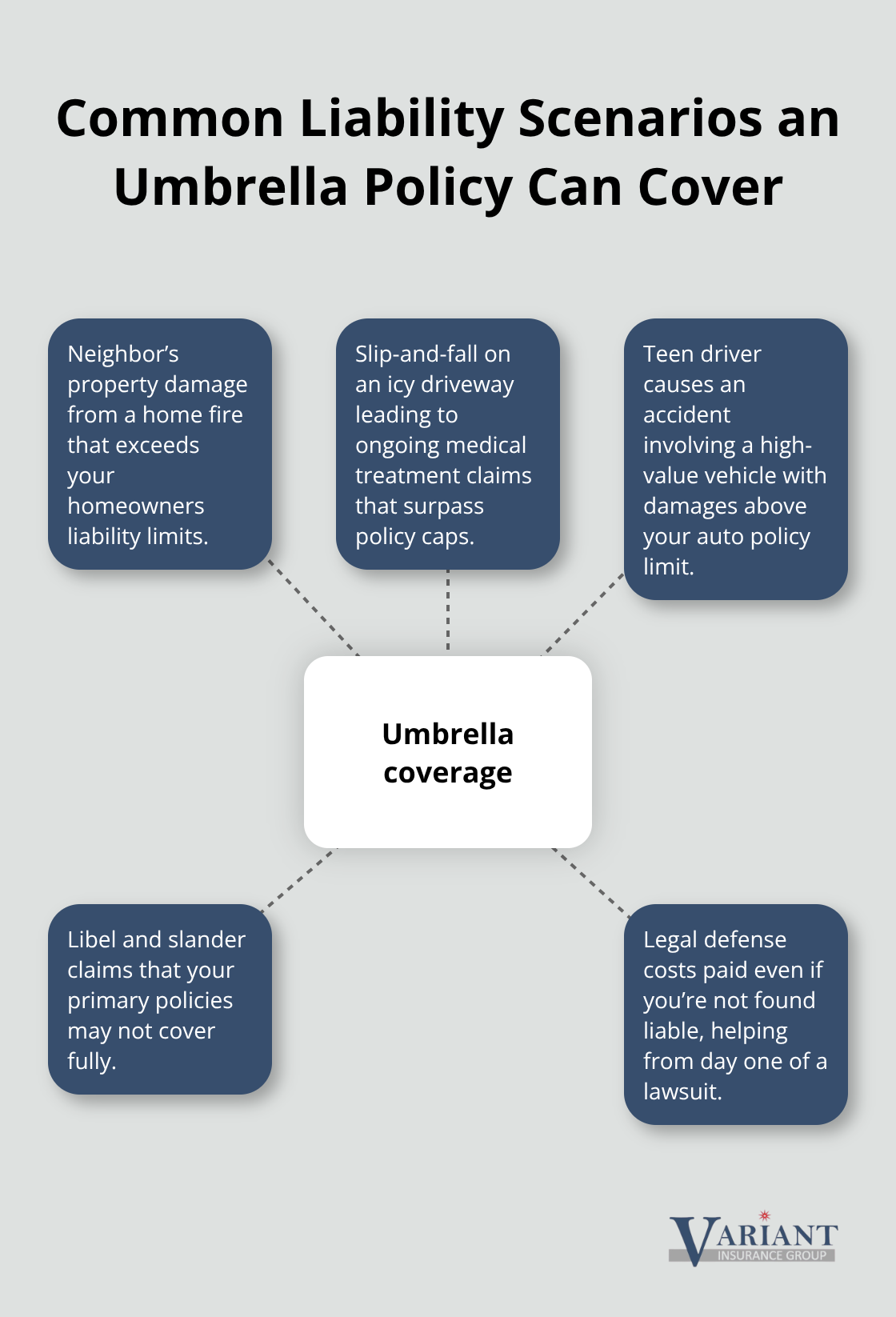

Umbrella policies cover liability and legal defense costs that your primary policies do not cover. This includes libel and slander, which can be costly for professionals or business owners with public visibility. The coverage extends worldwide in most cases, protecting you and family members living in your home regardless of where an incident occurs. However, umbrella policies do not cover intentional acts, professional errors, or damage to your own property. According to the NAIC, punitive damages from incidents like drunk driving are also excluded. The key advantage is that umbrella coverage pays legal defense fees even if you are not found liable, protecting your finances from the outset of a lawsuit rather than only after a judgment.

Why Standard Policies Fall Short in Minnesota

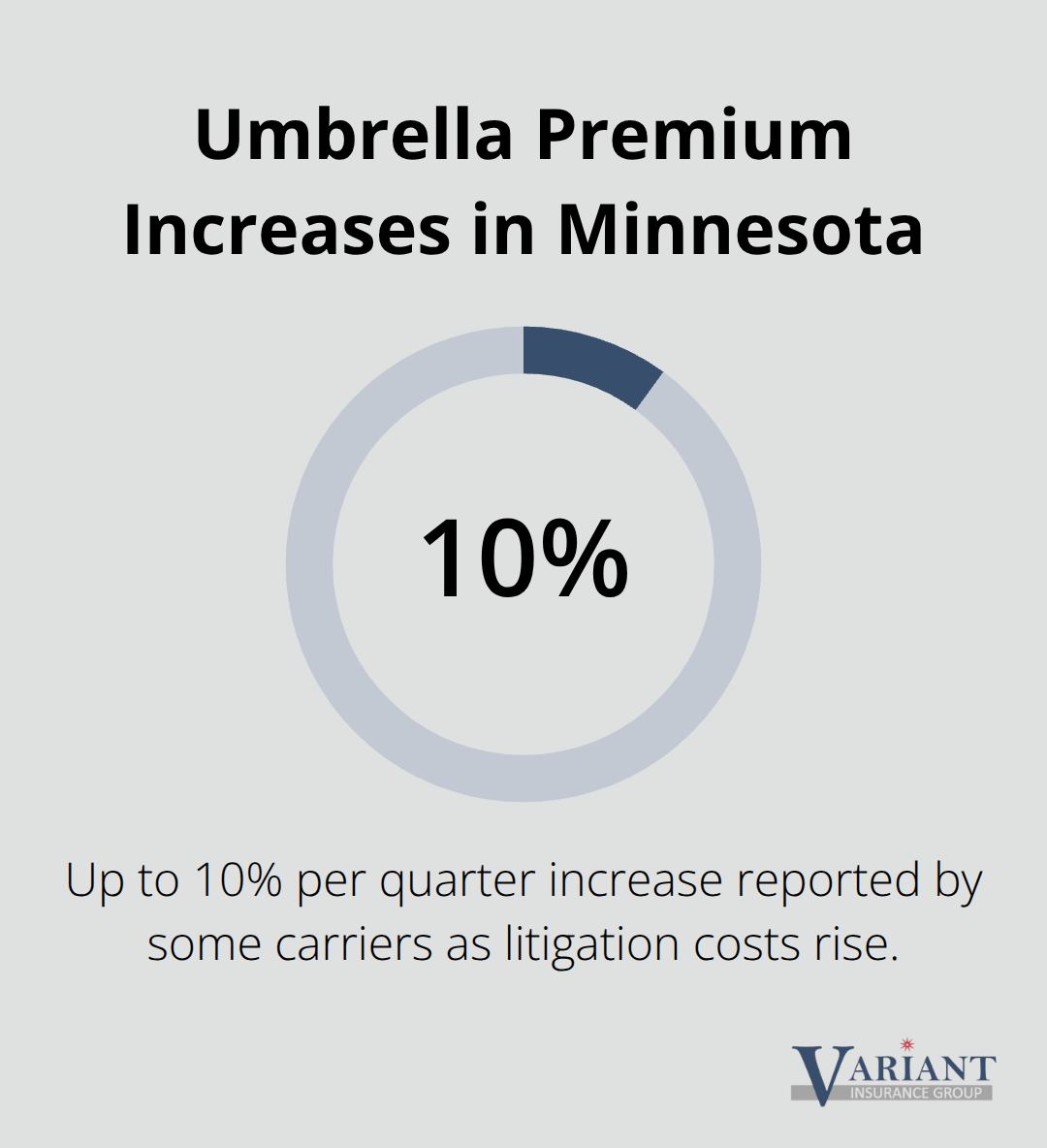

Standard homeowners policies in Minnesota typically provide $300,000 to $500,000 in liability coverage, while auto policies often cap at $250,000 to $300,000. A single serious incident can exceed these limits rapidly. For example, a dog bite results in $750,000 in medical costs and leaves you responsible for $450,000 out of pocket with standard coverage alone. Minnesota’s rising litigation costs have pushed premiums higher, with some carriers increasing umbrella rates by up to 10% per quarter. High-asset households, those with teen drivers, rental properties, or large gatherings face elevated liability exposure that standard policies simply cannot address.

To qualify for umbrella coverage in Minnesota, you typically need to maintain minimum auto liability of about $250,000 and homeowners liability of about $300,000 on your underlying policies first.

Coverage Gaps That Leave You Vulnerable

Your standard homeowners and auto policies exclude many liability scenarios that umbrella coverage handles. A fire in your home spreads to a neighbor’s garage, creating property damage claims that exceed your policy limits. A visitor slips on your icy driveway (common in Minnesota winters) and sues for ongoing medical treatment costs. Your teenage driver causes an accident involving a valuable vehicle, and the damages far surpass your auto policy cap.

These situations happen regularly in Minnesota, yet most residents operate without the extra protection umbrella policies provide. The gap between what your standard policies cover and what you actually owe in a serious incident can devastate your financial security.

Determining Your Coverage Needs

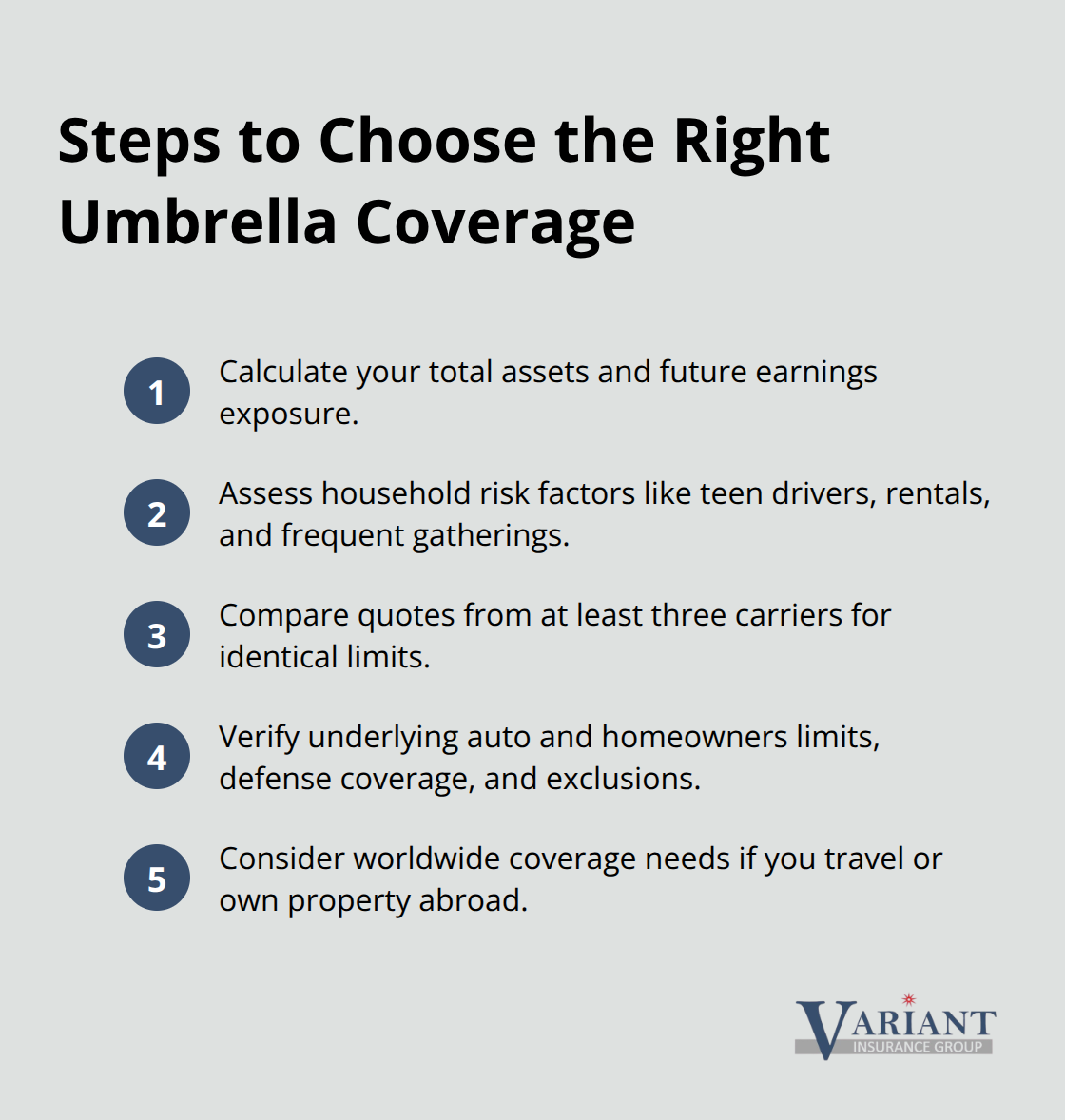

The right umbrella limit depends on your total assets, including savings, investments, properties, and future earnings. Most people should try $1 million in umbrella coverage as a starting point, though $3 million or more makes sense for high net worth individuals or those with multiple properties. If you own rental properties, host large gatherings, or have teen drivers, your liability exposure increases significantly. Your insurance agent can help you calculate an appropriate limit that matches your specific situation and risk profile. Once you understand your protection needs, you can compare quotes from multiple carriers to find the best value.

Why Minnesota Residents Face Real Liability Risks

Winter Conditions and Seasonal Exposure

Minnesota’s climate creates liability exposures that most residents underestimate. Winter driving conditions lead to more accidents, icy sidewalks increase slip-and-fall claims, and unsupervised pool injuries happen frequently during summer months. A Stillwater homeowner’s dog bite resulted in significant medical costs, leaving them short after their standard homeowners policy maxed out. That’s not a hypothetical scenario-it’s what happens when liability claims exceed standard coverage. Minnesota’s rising litigation costs have pushed umbrella premiums up, reflecting the state’s growing lawsuit expenses.

High-Risk Household Situations

Teen drivers, multiple vehicles, rental properties, and hosting gatherings all amplify your liability exposure beyond what homeowners and auto policies cover. A single serious incident can easily trigger six-figure or seven-figure damages claims, and your standard policies simply won’t bridge that gap. These situations happen regularly in Minnesota, yet most residents operate without the extra protection umbrella policies provide.

The True Cost of Being Underinsured

Without umbrella protection, you face selling assets, liquidating investments, or garnishing future wages to pay a judgment. Medical bills alone from a severe injury on your property can reach substantial amounts, and that’s before legal fees. Minnesota’s minimum underlying policy requirements leave massive exposure above those thresholds. A business facing a significant injury claim with only limited general liability coverage would owe the difference from their own pocket without umbrella protection.

Legal Defense Costs Start Immediately

Legal defense costs start immediately when you’re sued, even before any judgment, and standard policies often cap these expenses. Umbrella policies pay defense fees regardless of fault, protecting your finances from day one of litigation. Most Minnesota umbrella policies start at $1 million in coverage for roughly $200 to $400 annually-a modest cost compared to the financial devastation a single lawsuit can inflict. Understanding your specific liability exposure helps you determine whether your current coverage leaves you vulnerable, which brings us to the next critical step: assessing your personal assets and choosing the right umbrella limit for your situation.

Choosing the Right Coverage Limit for Your Assets

Calculate Your Total Asset Exposure

Your umbrella limit should match or exceed your total assets plus future earnings. Add up your home value, vehicles, savings, investments, rental properties, and any other significant assets, then project your income over the next decade or two. A judgment creditor can pursue your wages and assets to satisfy a court award, so this calculation matters for your financial security. If you own a $400,000 home, drive two vehicles worth $60,000 combined, and have $150,000 in savings and investments, you’re looking at roughly $610,000 in exposed assets before considering future earnings. Most Minnesota residents should try $1 million in umbrella coverage as a starting point, though high net worth individuals typically need $3 million or more. The National Association of Insurance Commissioners notes that umbrella policies cover bodily injury, property damage, and personal injury claims beyond your underlying limits, so your chosen amount should account for worst-case scenarios in your specific situation.

Assess Your Household Risk Factors

Teen drivers increase your exposure significantly because they’re statistically more likely to cause serious accidents. Rental properties add liability from tenant injuries or property damage claims. Hosting large gatherings creates slip-and-fall risks on your property. Minnesota’s rising litigation costs mean that what seemed like adequate coverage five years ago may fall short today, particularly as medical costs and damage awards continue climbing. Your specific household situation determines whether you need $1 million, $3 million, or even higher limits to protect your financial future.

Compare Quotes from Multiple Carriers

Umbrella premiums in Minnesota typically range from $200 to $400 annually for $1 million of coverage, with each additional $1 million adding roughly $50 to $75 per year. Rates vary based on your location within Minnesota, driving history, claims history, and profession. A contractor or medical professional may pay more due to higher liability exposure in their occupation. Request quotes from at least three different carriers because premium differences for identical coverage can exceed $100 annually, and some insurers offer discounts you won’t find on your own.

Verify Coverage Details and Exclusions

When comparing quotes, verify that each carrier’s requirements for underlying auto and homeowners liability match your current policies. You typically need about $250,000 in auto liability and $300,000 in homeowners liability to qualify for umbrella coverage. Ask specifically whether each quote includes legal defense costs paid regardless of fault, whether defamation coverage is included, and what exclusions apply to your situation. Some carriers provide broader worldwide coverage than others, and if you travel internationally or own property outside the United States, this matters significantly. Don’t simply chase the lowest premium, because umbrella policies aren’t commodities-the carrier’s claims-handling reputation and the breadth of coverage matter far more than saving $50 annually.

Final Thoughts

Umbrella liability insurance in Minnesota protects your personal assets from the financial devastation of a single lawsuit or serious accident. Standard homeowners and auto policies leave gaps that can cost you hundreds of thousands of dollars out of pocket, but umbrella coverage fills those gaps affordably. Most Minnesota residents should try $1 million in coverage for roughly $200 to $400 annually, with higher limits available if your assets or risk profile demands it.

Review your current homeowners and auto policy limits to confirm they meet the minimum requirements for umbrella coverage (typically $250,000 in auto liability and $300,000 in homeowners liability). Estimate your total assets including your home, vehicles, savings, investments, and future earnings to determine an appropriate umbrella limit. Request quotes from at least three different carriers because premiums vary significantly for identical coverage, and some insurers offer discounts you won’t discover on your own.

We at Variant Insurance Group specialize in shopping Minnesota’s top-rated insurance companies to find the right umbrella liability insurance Minnesota policy for your specific situation. Our team compares coverage options and pricing across multiple carriers so you get the best possible value without overpaying for protection you don’t need or leaving gaps in coverage you do. Contact us today to discuss your umbrella liability insurance needs and get a personalized quote that protects your financial future.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation