Your home contains thousands of dollars in belongings, yet most homeowners don’t fully understand what their insurance actually protects. At Variant Insurance Group, we’ve seen countless Minnesota families discover coverage gaps only after a loss occurs.

Homeowners insurance personal property protection is more complex than many realize. This guide walks you through what’s covered, where the gaps hide, and how to build a policy that truly matches what you own.

What Your Homeowners Policy Actually Covers

Homeowners insurance breaks into three main protection buckets, and most Minnesota homeowners misunderstand how they work together. Dwelling coverage protects the structure itself-your walls, roof, foundation, and permanently attached systems like electrical wiring and plumbing. Personal property coverage protects your belongings inside that structure, from furniture and clothing to electronics and kitchen appliances. Liability coverage protects you financially if someone is injured on your property and sues. These three pieces work independently, which means a covered loss under one category doesn’t count against another. For example, if a fire damages both your home’s structure and your furniture, the dwelling claim and personal property claim operate separately with their own limits and deductibles. This separation matters because it means you need to understand each component individually to know whether you’re actually protected.

Personal Property Coverage Is Usually Underestimated

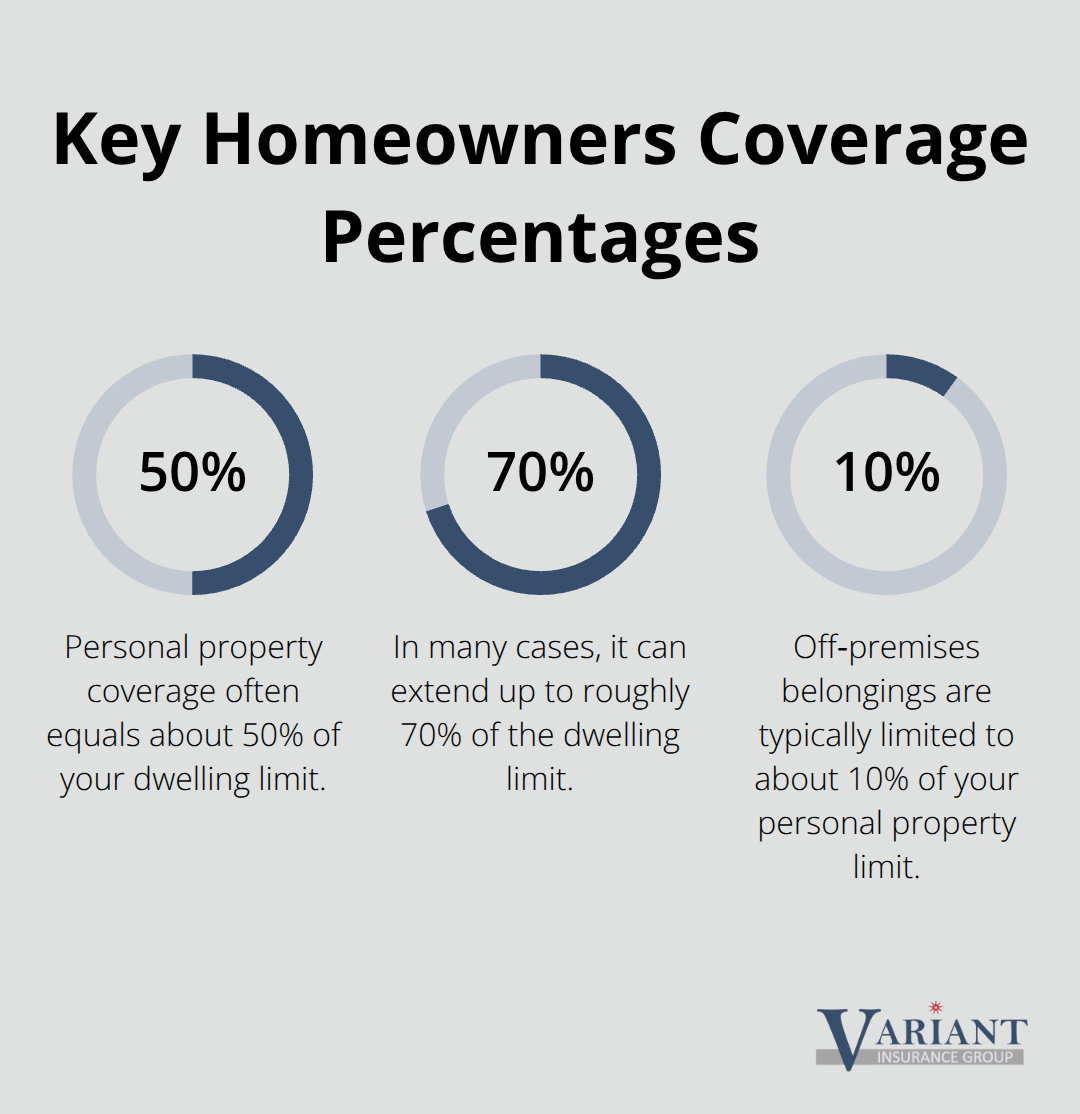

Most homeowners set personal property limits too low because they don’t realize how much their belongings are actually worth. Personal property coverage typically maxes out at about 50 to 70 percent of your dwelling coverage limit. If your home is insured for $400,000, your personal property coverage likely sits around $200,000 to $280,000. That sounds substantial until you start inventorying what you own. A basic bedroom set runs $5,000 to $8,000. A kitchen’s worth of appliances and cookware adds another $8,000 to $15,000. Electronics-televisions, computers, tablets, and audio equipment-easily reach $10,000 in a typical household. Add clothing, furniture, tools, and sporting equipment, and most Minnesota families discover they’re underinsured.

Sublimits Create Hidden Exposure

The real problem surfaces when you hit sublimits. Standard policies cap coverage on jewelry at roughly $1,500 to $2,500, electronics at similar amounts, and fine art or collectibles even lower. A single engagement ring or laptop can exceed these limits instantly, leaving you exposed. High-value items require scheduled personal property endorsements to raise those limits above what standard coverage allows.

Liability Covers What Happens When Someone Gets Hurt

Liability coverage on a homeowners policy typically starts at $100,000, though many policies offer $300,000 or higher. This covers medical bills and legal costs if someone is injured at your property and you’re found legally responsible. A neighbor slips on your icy driveway in January and breaks their leg-that’s a liability claim. Someone is bitten by your dog while visiting-liability applies. A child from down the street falls off your trampoline-liability protects you.

When Standard Liability Falls Short

The catch is that $100,000 or even $300,000 disappears fast in serious injury cases. A severe injury requiring surgery, ongoing physical therapy, and lost wages can easily exceed $500,000. This is why many insurance professionals recommend umbrella liability coverage, which adds another $1 million in protection for roughly $150 to $300 annually, depending on your location and risk profile. Minnesota homeowners with significant assets should seriously consider this layer because one serious accident can threaten your financial stability. Understanding these three coverage types sets the foundation for identifying where gaps actually exist in your protection.

Where Standard Coverage Really Falls Short

The gap between what homeowners think they’re covered for and what actually protects them creates serious financial exposure across Minnesota. Standard homeowners policies exclude water damage from external sources entirely, meaning if your basement floods during heavy spring rains or a pipe bursts inside your walls, you pay out of pocket. Flood damage requires separate flood insurance through the National Flood Insurance Program or private carriers, yet most Minnesota homeowners never purchase it. Earthquake coverage operates the same way-completely excluded from standard policies. Beyond these major exclusions, sublimits on specific categories create dangerous gaps that most people never discover until they file a claim.

Sublimits Leave High-Value Items Exposed

Jewelry sublimits typically cap at $1,500 to $2,500 despite many families owning engagement rings or heirloom pieces worth $5,000 to $10,000 or more. Electronics face similar caps around $2,500, which means a home office setup with multiple computers, monitors, and equipment instantly exceeds coverage. Fine art, antiques, firearms, and collectibles hit even lower sublimits, sometimes $500 to $1,000. A single piece of artwork or a modest firearms collection leaves you dramatically underinsured without scheduled endorsements.

Actual Cash Value Versus Replacement Cost

Actual cash value versus replacement cost creates another critical gap that catches Minnesota homeowners off guard. Standard policies often default to actual cash value, which means the insurer pays what an item is worth today after accounting for depreciation rather than what it costs to replace with something new. A five-year-old couch worth $800 today might cost $2,000 to replace with equivalent quality. A laptop purchased three years ago for $1,200 might be worth $400 in actual cash value but cost $1,200 to replace. This depreciation gap compounds across hundreds of items, and most claims fall significantly short of actual replacement costs.

Replacement cost endorsements cost more in premium but eliminate depreciation from the payout calculation. For Minnesota homeowners with substantial belongings, this endorsement typically pays for itself after a single claim.

Off-Premises Coverage Limits Create Exposure

Off-premises coverage creates another exposure point most people overlook. Standard policies limit coverage for belongings away from home to roughly 10 percent of your personal property limit. If your personal property limit is $200,000, items in your car, at a vacation property, or in temporary storage during a move only receive $20,000 in coverage. Valuable items taken on trips, stored in vacation homes, or in transit during relocations frequently exceed these limits, leaving significant exposure unprotected without additional endorsements.

Documentation Reveals True Replacement Costs

Most Minnesota homeowners dramatically underestimate what they own because they never create a detailed inventory. A room-by-room walkthrough with photographs and estimated values reveals the true replacement cost of your belongings. Average households discover they own $150,000 to $250,000 in personal property, far exceeding standard coverage limits. Serial numbers, purchase dates, and receipts for expensive items accelerate the claims process and prevent disputes over value.

Store this inventory digitally in cloud storage and keep physical copies in a safe deposit box so it survives any disaster affecting your home.

For high-value items exceeding sublimits, professional appraisals and individual scheduling on your policy provide broader coverage and often waive deductibles for those specific items. A scheduled property floater for jewelry, firearms, or collectibles ensures you receive full replacement value rather than fighting with the insurer over sublimit restrictions. This approach costs more but transforms your homeowners policy from a source of false security into genuine protection-and it’s exactly the kind of gap analysis that separates adequate coverage from real financial security.

Setting Coverage Limits That Match What You Actually Own

Most Minnesota homeowners start with whatever coverage their lender requires or their agent recommends without doing the math themselves. This approach leaves you either dramatically overinsured and overpaying, or dangerously underinsured and exposed. The reality is that coverage limits should reflect three concrete numbers: what your home structure costs to rebuild, what your belongings cost to replace, and how those costs will shift over time.

Starting with your home’s reconstruction cost matters because personal property limits tie directly to this figure. According to the National Association of Insurance Commissioners, personal property coverage typically maxes out at 50 percent of your dwelling limit. If your home reconstruction cost is $400,000 but you only insure it for $300,000 to save on premiums, your personal property limit drops proportionally, leaving your belongings exposed. A professional reconstruction estimate from a local contractor who understands Minnesota building codes and current material costs beats guessing based on your home’s purchase price. A 1970s home purchased for $180,000 might cost $450,000 to rebuild today due to labor and material inflation. This number becomes your baseline for calculating adequate personal property coverage.

Start with a Room-by-Room Inventory

The inventory process reveals why standard coverage limits fail most families. Walk through your home and photograph every room, then list major items with estimated replacement costs. A master bedroom typically contains a bed frame, mattress, dressers, nightstands, and clothing totaling $8,000 to $12,000 at current retail prices. A kitchen’s appliances, cookware, dishes, and food storage items add $10,000 to $18,000. A home office with computers, monitors, printers, and furniture easily reaches $6,000 to $10,000. Electronics scattered throughout the home (television, tablets, speakers, gaming systems) routinely total $8,000 to $15,000. Tools in the garage, sporting equipment, outdoor furniture, and miscellaneous belongings push most Minnesota households to $180,000 to $280,000 in personal property. The Insurance Information Institute recommends creating detailed inventories with purchase dates, serial numbers, and photographs stored in cloud storage. When you compare this actual number to your current policy limit, the gap becomes obvious. If your policy caps personal property at $150,000 but your inventory totals $220,000, you face a $70,000 shortfall that you’ll pay out of pocket after a major loss.

Account for Replacement Cost Inflation

Replacement costs climb faster than general inflation for home goods. According to recent data from the Bureau of Labor Statistics, furniture and household furnishings prices increased 18 percent between 2020 and 2023 alone. Electronics prices fluctuate but remain elevated compared to pre-pandemic levels. Labor costs for installation and repairs continue climbing across Minnesota. If you set your coverage limit today based on current prices, that limit becomes inadequate within three to five years without adjustment.

Many policies offer inflation guard endorsements that automatically increase your personal property limit by 3 to 5 percent annually, protecting you against this erosion without requiring annual policy reviews. This costs roughly $100 to $200 annually but prevents the scenario where a loss occurs in year four and your $200,000 limit only covers what $170,000 would have bought when you purchased the policy. Professional appraisals for high-value items should be updated every three to five years, especially for jewelry, art, and collectibles whose values shift independently of general inflation. Schedule these items individually on your policy rather than relying on sublimits, which ensures full replacement value regardless of inflation.

Final Thoughts

Your homeowners insurance personal property coverage only protects you if it actually matches what you own. The gap between standard policy limits and real replacement costs creates financial exposure that catches most Minnesota families off guard, and you won’t discover this gap until after a loss occurs. An honest conversation with someone who understands both your belongings and your local insurance market transforms this abstract risk into concrete action.

At Variant Insurance Group, we work with Minnesota homeowners to review existing coverage, identify gaps, and shop multiple carriers to find the right protection at the right price. As an independent agency, we compare options across top-rated insurers rather than pushing a single company’s limitations or pricing. This review process reveals where your current limits fall short, which endorsements and scheduled items would close those gaps, and how much additional protection costs.

Pull together your home’s reconstruction estimate and your personal property inventory this week, then contact an agent who will actually review these numbers against your current policy. Your belongings deserve protection that matches their real value, not protection that matches your lender’s minimum requirements.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation