Many Minnesota homeowners and renters think property and casualty insurance are the same thing. They’re not. Understanding the difference between property and casualty insurance is essential for protecting yourself financially.

At Variant Insurance Group, we help people get the right coverage for their specific situations. This guide breaks down how these two types of insurance work and why most people need both.

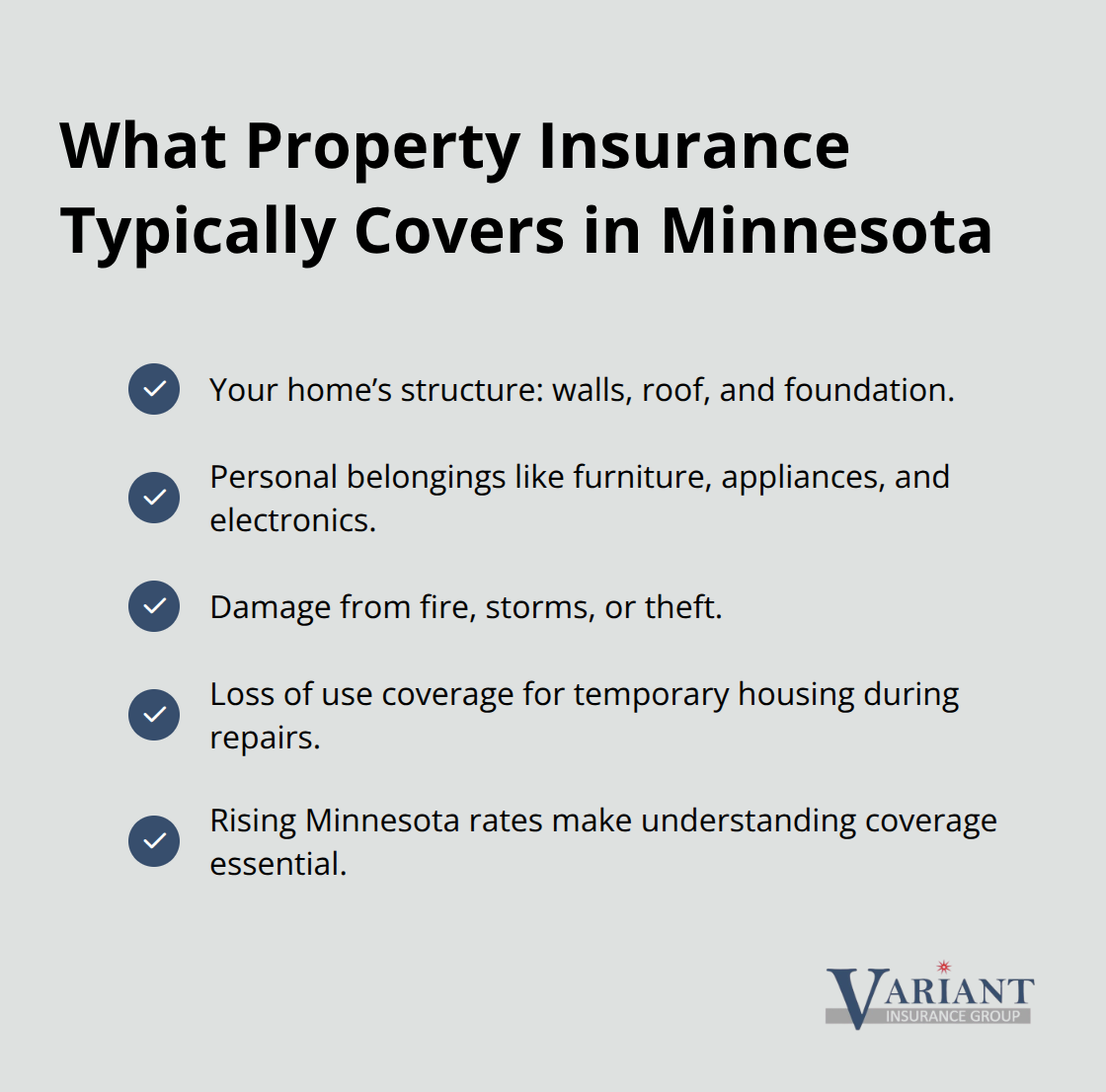

What Property Insurance Covers

Property insurance protects the physical structures and belongings you own. In Minnesota, this typically means coverage for your home’s walls, roof, and foundation, plus everything inside-furniture, appliances, electronics, and personal items. If a fire, storm, or theft damages your property, your policy pays for repairs or replacement. The Minnesota Department of Commerce notes that rising property insurance rates in Minnesota are a current trend, making it more important than ever to understand exactly what you’re paying for.

Loss of Use Protection

Your homeowners policy includes loss of use coverage, which reimburses temporary housing expenses if your home becomes uninhabitable after a covered event. This matters because staying in a hotel or rental while repairs happen can cost thousands of dollars quickly. Without this coverage, you absorb those costs out of pocket while waiting for your home to become livable again.

Common Coverage Gaps Most Homeowners Miss

Most Minnesota homeowners mistakenly believe their standard policy covers everything. It doesn’t. Flood damage, earthquake damage, and windstorm damage are typically excluded unless you add separate endorsements or riders. If you live near water or in a flood-prone area, flood insurance is a separate purchase-your homeowners policy won’t touch it. Similarly, sewer backup coverage, which protects against water damage from backed-up sewage lines, must be added as an endorsement.

The Coinsurance Clause and Underinsurance Penalties

The coinsurance provision in your policy is something many people overlook but shouldn’t. This clause requires you to insure your property for at least 80%, 90%, or 100% of its replacement value. If you underinsure and suffer a loss, the insurance company pays only a proportional amount.

The number 100% seems to be not appropriate for this chart. Please use a different chart type. For example, if your home is worth $400,000 but you insure it for only $320,000 when the policy requires 80% coverage ($320,000), you’re fine. But if you insure it for $300,000, you’ve violated the coinsurance clause, and a $50,000 claim might be reduced proportionally.

Protecting Yourself From Policy Blind Spots

Reviewing your policy with legal counsel helps you identify gaps like missing flood or earthquake protection before a disaster strikes. An attorney can also flag exclusions you might have missed and explain how specific endorsements affect your coverage. This step takes time upfront but prevents costly surprises when you file a claim. Understanding what your property insurance actually covers sets the stage for recognizing why casualty insurance fills a completely different role in your financial protection strategy.

What Casualty Insurance Actually Protects

Casualty insurance, also called liability insurance, protects you from financial responsibility when someone else is injured or their property is damaged because of you or your activities. This differs fundamentally from property insurance, which covers your own belongings. If a guest slips on your icy Minnesota driveway and breaks their arm, their medical bills and potential lawsuit fall under casualty coverage, not property coverage. Your homeowners policy includes liability protection, though many Minnesota homeowners carry insufficient limits given the cost of medical care today. A serious injury claim can easily exceed $500,000 when accounting for emergency surgery, ongoing physical therapy, lost wages, and pain-and-suffering damages. Understanding your casualty limits matters more than most people realize.

How Casualty Insurance Works Across Different Situations

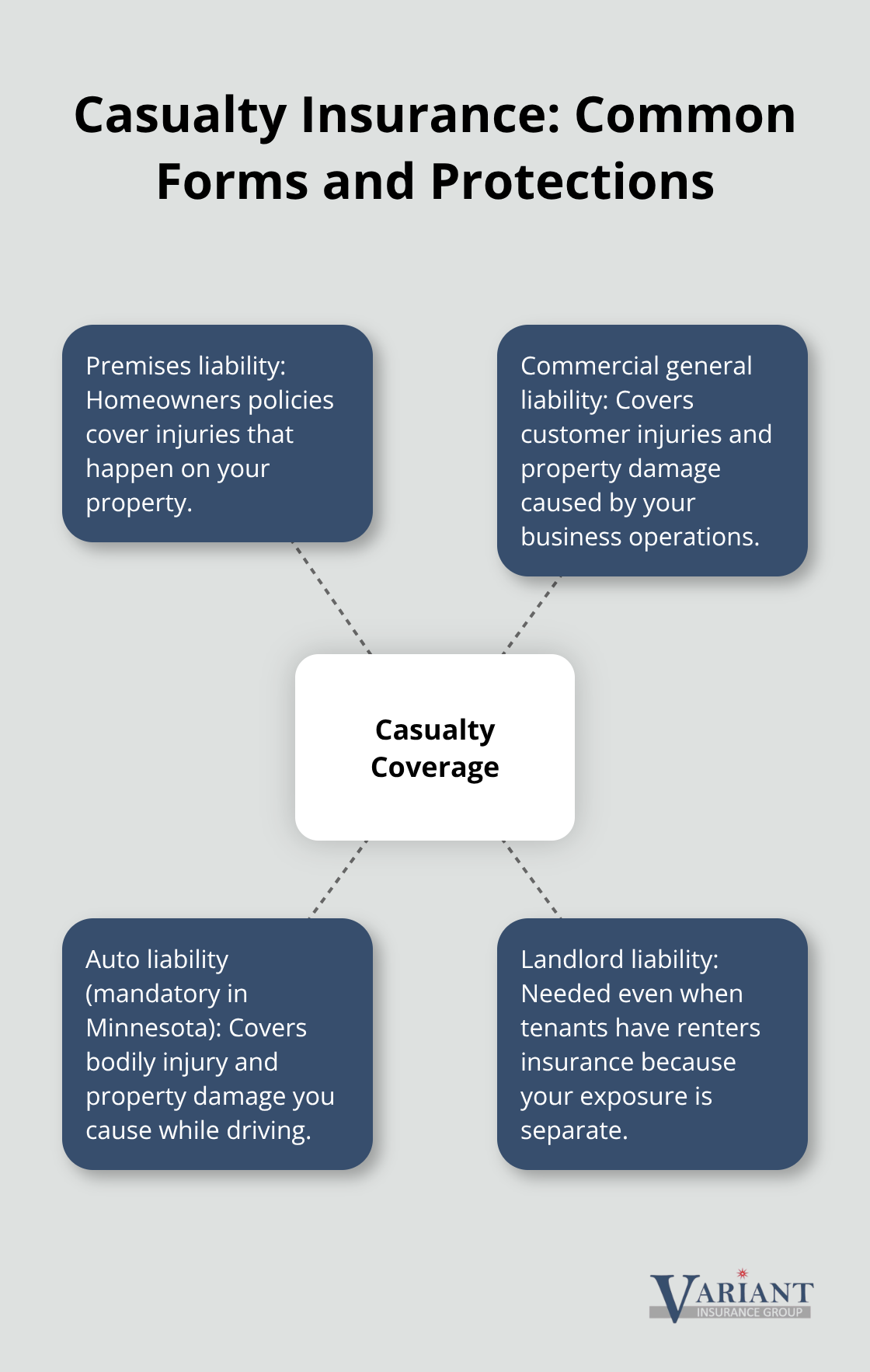

Casualty insurance takes multiple forms depending on what you’re protecting. Homeowners policies include premises liability, which covers injuries that happen on your property. Commercial general liability protects business owners from claims arising from their operations, covering everything from a customer injured in your store to property damage your business causes to someone else’s building.

Auto liability is mandatory in Minnesota and covers bodily injury and property damage you cause while driving. If you’re a landlord, you need casualty coverage even if tenants have their own renters insurance, because your liability exposure is separate from theirs.

Real Casualty Claims Show Why Coverage Matters

Real-world casualty claims happen constantly. A Minnesota homeowner faced a $400,000 lawsuit after a visitor fell from their deck during a summer gathering. Another paid $150,000 to settle a claim when their dog bit a neighbor’s child despite having no prior incidents. A small business owner faced a $200,000 lawsuit when a customer slipped on a wet floor inside the shop. These aren’t hypothetical scenarios-they’re situations your casualty insurance either covers or leaves you personally responsible for.

The difference between having adequate coverage and being underinsured can mean the difference between a claim being handled by your insurance company and losing your savings, home equity, or business assets to satisfy a judgment. This reality makes casualty coverage just as important as property protection, yet the two work in completely different ways. Understanding how they differ in what they cover, how claims get processed, and what factors affect your premiums helps you build a complete financial protection strategy.

How Property and Casualty Insurance Handle Damage Differently

When Claims Activate and How They Work

Property and casualty insurance operate on opposite ends of financial protection, which means they trigger claims in completely different situations and pay out accordingly. Property insurance activates when your physical assets suffer damage or loss-a house fire, stolen laptop, or storm damage to your roof. Casualty insurance activates when someone else is injured or their property is damaged because of you or your activities. This fundamental difference shapes everything about how claims get processed and what you’ll receive.

When you file a property claim, the insurance company sends an adjuster to assess the damage to your belongings or structure. They measure the cost to repair or replace what was damaged, then issue payment based on your policy limits and deductible. A $50,000 roof replacement claim gets paid out to cover that specific damage. With casualty claims, the process works backward. Someone files a claim against you, their attorney demands compensation, and your insurance company either negotiates a settlement or defends you in court.

How Payouts Differ Between the Two Types

The payout structure reveals why these two insurance types operate so differently. Property insurance pays for measurable, physical damage. The adjuster calculates repair or replacement costs, and your insurer writes a check for that amount (minus your deductible). Casualty claims don’t work that way. The payout isn’t tied to physical damage you can measure-it’s tied to medical bills, lost wages, legal fees, and damages a judge or jury assigns. A casualty claim for $200,000 might include $75,000 in medical expenses, $50,000 in lost income, and $75,000 in pain-and-suffering damages awarded by a court.

What Drives Property Insurance Premiums

Property insurance premiums depend heavily on the replacement value of your home or belongings, your location’s disaster risk, proximity to fire protection, building age, and claims history. A newer home in a low-flood-risk area with a fire station nearby costs significantly less to insure than an older home near water in a wildfire zone. Minnesota homeowners in flood-prone counties near the Mississippi River or St. Croix River pay substantially higher property premiums than those in elevated areas. Rising property insurance rates in Minnesota are a current trend, making premium comparison essential.

What Drives Casualty Insurance Premiums

Casualty insurance premiums reflect your liability exposure and risk profile. Your age, driving record, credit score, and prior liability claims affect auto liability rates. For homeowners liability, claims history and the nature of your property matter most-someone with a prior dog-bite claim pays more than someone with no incidents. Business liability rates depend on industry type, revenue, employee count, and safety practices. A restaurant faces higher casualty premiums than an accounting firm because restaurants carry greater slip-and-fall exposure.

Choosing the Right Coverage Limits for Each Type

Understanding these distinct cost drivers means you shouldn’t shop property and casualty coverage the same way. Lower property deductibles protect you against frequent smaller claims, while higher casualty limits protect you against catastrophic lawsuits. Most Minnesota homeowners carry $300,000 in liability coverage, which proves dangerously inadequate given modern medical costs and litigation expenses. Increasing to $500,000 or $1,000,000 in liability coverage costs only $50 to $150 more annually but prevents financial ruin from a serious claim.

Final Thoughts

Property and casualty insurance serve completely different purposes, yet most Minnesota homeowners need both to be truly protected. Property insurance covers the physical assets you own-your home, belongings, and structures. Casualty insurance covers your financial responsibility when someone else is injured or their property is damaged because of you. The difference between property and casualty insurance isn’t subtle; it’s fundamental to how each protects you.

A house fire illustrates why both types matter. Property insurance pays to rebuild your home and replace your belongings, while casualty insurance covers damages and legal claims if that fire spreads to your neighbor’s house because of your negligence. Without property coverage, you lose your home. Without casualty coverage, you lose your savings defending a lawsuit. Both gaps leave you financially exposed.

Determining your insurance needs starts with honestly assessing your assets and liability exposure. How much would it cost to rebuild your home at today’s prices? What’s your replacement value for belongings? Do you have significant liability exposure through property ownership, a business, or activities that could injure others? Minnesota homeowners often underestimate both their property replacement costs and their casualty exposure (a serious injury claim can easily exceed $500,000 when accounting for medical bills, lost wages, and court-awarded damages). Contact us at Variant Insurance Group to review your coverage and compare protection across Minnesota’s top-rated insurance companies.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation