Owning rental property in Maple Plain comes with real financial exposure. Weather damage, tenant injuries, and lost rent can quickly drain your profits if you’re not properly protected.

At Variant Insurance Group, we help landlords in Minnesota understand what coverage actually matters for their rental investments. The right Maple Plain landlord insurance policy shields your property and income from the risks that matter most.

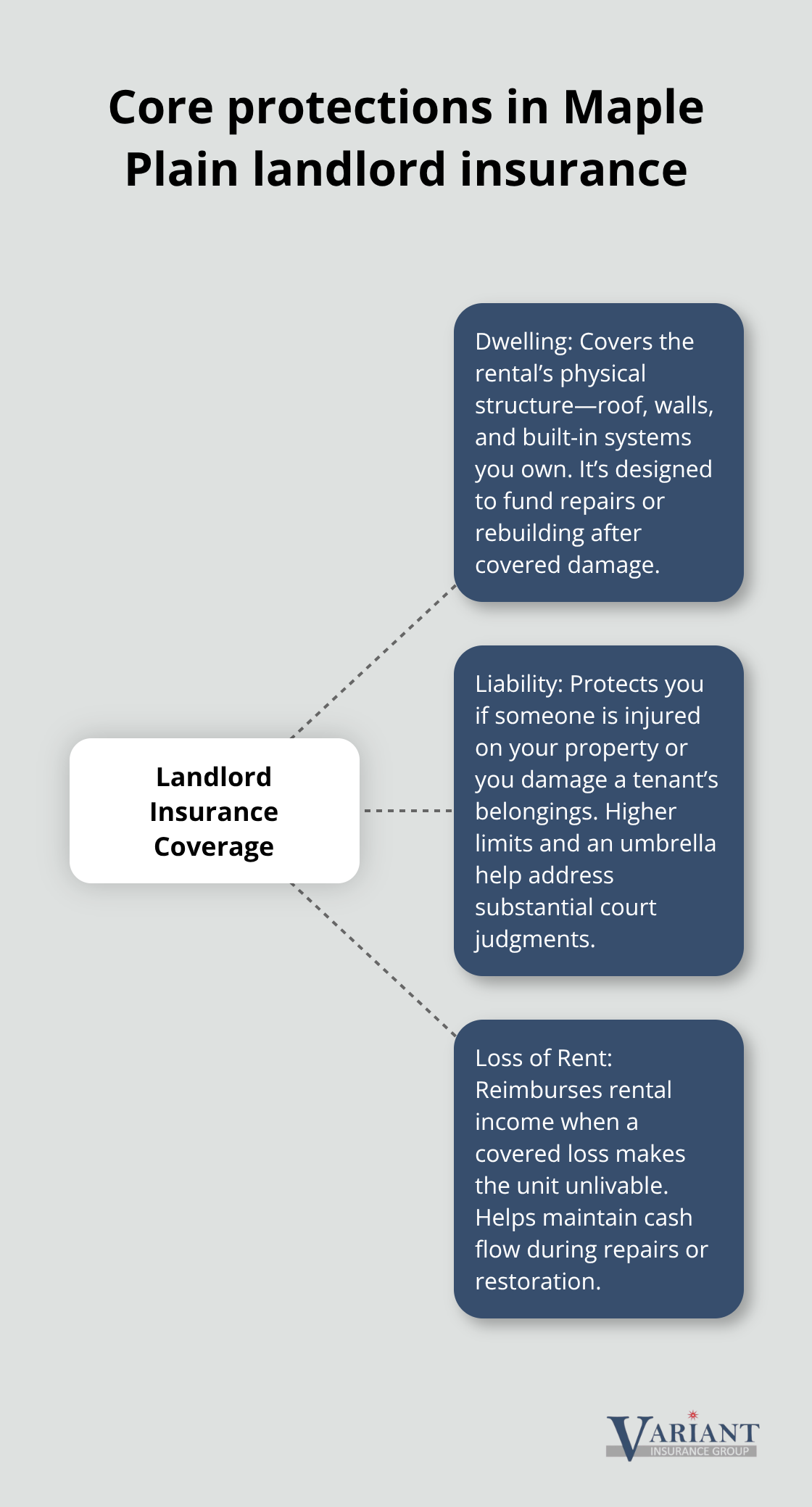

What Landlord Insurance Actually Covers

Landlord insurance in Minnesota protects three critical areas that standard homeowners policies ignore completely. The dwelling covers the physical structure of your rental property, including the roof, walls, and built-in appliances you own. Liability coverage shields you when someone is injured on your property or if you accidentally damage someone else’s belongings-Minnesota courts have awarded substantial premises liability judgments, which is why liability limits of at least $300,000 on a standard policy make sense, with umbrella coverage of $1 million or more if you own multiple properties. Loss of rent coverage reimburses your monthly rental income if the property becomes unusable after a covered loss.

If you collect $1,500 monthly rent and repairs take three months, this coverage pays $4,500 to maintain your cash flow while the property is restored.

Dwelling Coverage Reflects Actual Rebuild Costs

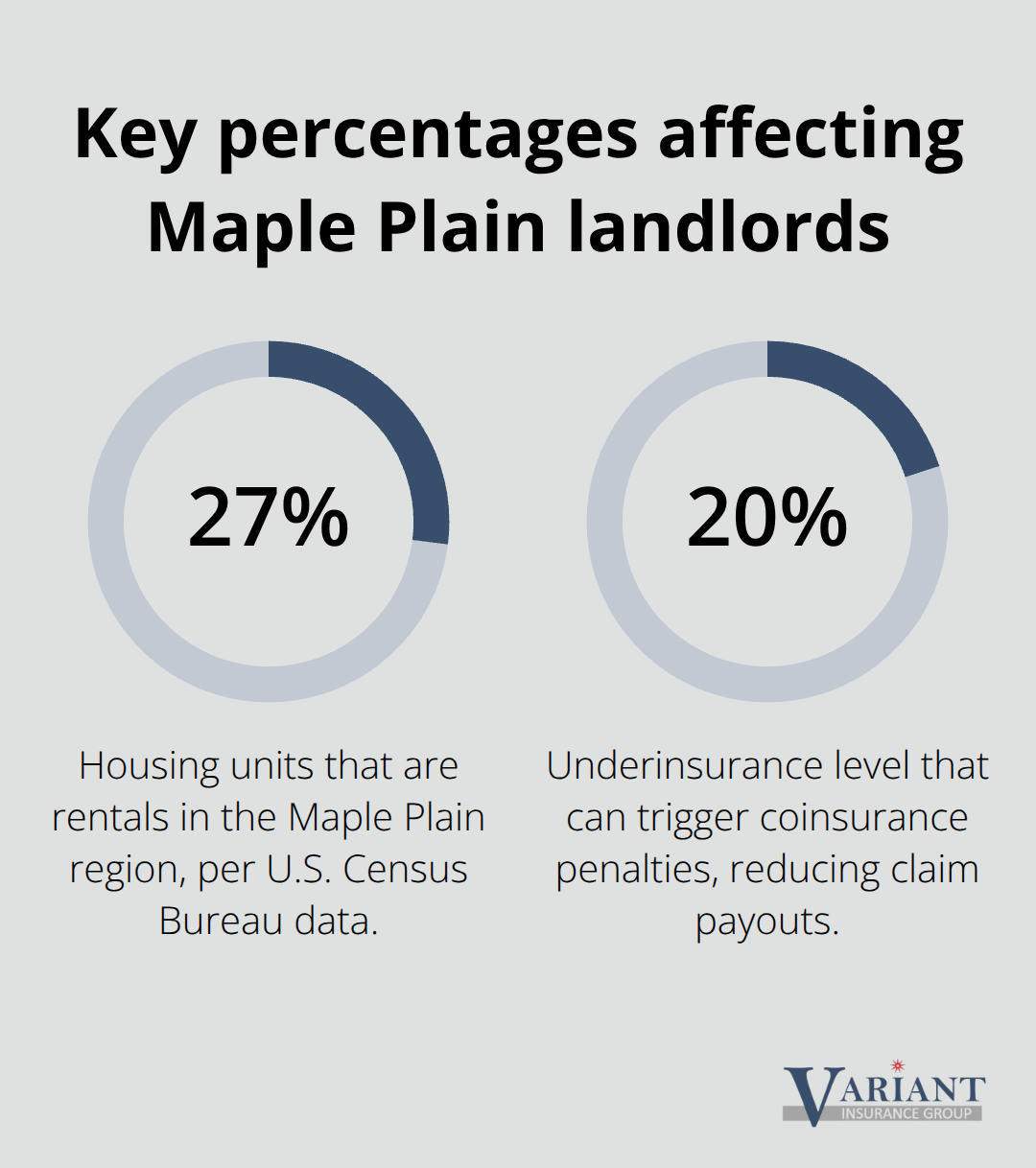

Most landlords make a critical mistake by basing dwelling limits on their purchase price rather than what it actually costs to rebuild. A typical 1,500-square-foot home in the Twin Cities requires around $250,000 to $350,000 to rebuild today, depending on materials and finishes. Underinsuring by just 20 percent triggers coinsurance penalties that reduce your claim payout significantly-you could lose thousands on a major loss. Older roofs present another issue: insurers often settle claims on actual cash value instead of replacement cost, meaning an aging roof may pay far less than a new one costs. Verify how your policy handles roof age and seek replacement cost coverage when available. Detached structures like garages or sheds require explicit coverage or endorsements, otherwise you face gaps when those buildings suffer damage.

Medical Payments and Non-Occupied Coverage

Medical payments coverage typically ranges from $1,000 to $5,000 per person and pays immediate medical bills for guests injured on your property without requiring a lawsuit-this can prevent litigation before it starts. Non-occupied dwelling coverage becomes essential if your property sits vacant for more than 30 days; standard policies exclude damage to unoccupied units, leaving you exposed during turnover periods or extended renovations.

Building Code and Rent Protection Options

Building code coverage reimburses costs to bring older Maple Plain properties up to current construction codes after a loss, which can be substantial on pre-1978 homes. Rent guarantee insurance protects against lost income during eviction, though it is expensive and typically pays only a portion after a deductible, so you should evaluate whether the cost justifies the protection for your situation. Requiring tenants to carry renters insurance naming you as an interested party shifts responsibility for their belongings and injuries to them, reducing your exposure while lowering your premium costs.

The specific coverage you select depends on your property’s age, occupancy status, and financial situation. Understanding these options positions you to make informed decisions about which protections matter most for your rental investment.

Why Maple Plain Landlords Need Local Coverage

Minnesota’s rental market creates specific exposures that generic insurance solutions simply don’t address. Maple Plain sits in a region where over 27 percent of housing units are rentals, according to U.S. Census Bureau data, meaning landlords here face competition and tenant turnover rates that directly impact your income stability.

The Minnesota Multi Housing Association recommends that landlords carry minimum liability insurance and property damage coverage as foundational protections, but many property owners treat this as a checkbox rather than understanding why these limits matter for their actual financial exposure. Winter weather in Minnesota causes ice dams, frozen pipes, and severe storm damage that destroys rental properties faster than in most states, and summer brings hail and wind that can disable a property for weeks or months. A three-month vacancy from storm damage on a $1,500 monthly rent property costs you $4,500 in lost income before you factor in repair delays or contractor availability during peak season. Standard homeowners policies exclude rental income entirely, which is why loss of rent coverage isn’t optional for Minnesota landlords-it’s the difference between staying profitable and facing a cash flow crisis when disaster strikes.

Minnesota Courts Award Substantial Liability Judgments

Liability exposure in Minnesota rental properties demands serious attention. Minnesota courts have awarded substantial premises liability judgments, meaning a single injury claim can create significant financial exposure, which is why standard landlord policies with only $100,000 in liability coverage leave you severely underprotected. If you own multiple rental properties, umbrella liability of $1 million or more across your portfolio becomes essential insurance, not luxury coverage. Legal requirements don’t mandate landlord insurance in Minnesota, but mortgage lenders almost always require it as a financing condition, and tenants injured on your property won’t care whether your policy is required-they’ll sue regardless. The Minnesota Attorney General’s Landlords and Tenants Handbook outlines landlord responsibilities around property maintenance and habitability, and failing to meet these standards while underinsured creates a path to financial disaster when an injury occurs.

Weather Patterns Shape Your Coverage Needs

Seasonal occupancy changes, renovation periods, and property transitions demand prompt notice to your insurer-failing to report that a unit will sit vacant for 45 days voids coverage for damage during that period. Weather patterns specific to Minnesota winters and summers influence which deductibles make financial sense and which endorsements actually protect your cash flow. Older Maple Plain properties built before 1978 require lead-based paint disclosures and present higher liability exposure, which affects your coverage structure and premium.

Local Expertise Prevents Coverage Gaps

A local insurance professional who understands Minnesota rental properties catches gaps that online quote systems miss entirely. Someone familiar with your community identifies risks that national insurers overlook and structures your policy to address them. Your insurer needs to understand local rental market conditions, Minnesota’s specific weather risks, and state tenant laws so you select coverage that prevents both gaps and unnecessary costs. This foundation positions you to make informed decisions about which protections matter most for your rental investment, and it prepares you to evaluate specific policy options that align with your property’s actual exposure.

How to Choose the Right Landlord Insurance Policy

Start with Your Property’s Actual Rebuild Cost

Start with your property’s actual rebuild cost, not what you paid for it. Contact local Maple Plain contractors and request a replacement cost estimate for your specific rental unit-this single number shapes every other decision you’ll make about dwelling limits. If you own a 1,500-square-foot home, expect rebuild costs between $250,000 and $350,000 in the Twin Cities area depending on materials and finishes. Many landlords discover their purchase price falls far short of true replacement cost, which means a policy built around purchase price leaves you exposed to coinsurance penalties that slash your claim payout. Once you know the real rebuild cost, set your dwelling limit to match it exactly.

Inventory Your Landlord-Owned Property

Next, audit what you actually own inside the rental unit. Landlord-owned appliances, furnishings, or equipment need specific coverage through landlord contents insurance-tenants’ belongings are never your responsibility, and standard landlord policies won’t cover them. Create a written inventory of these items with photos and purchase dates, which streamlines any future contents claim and prevents disputes about what you owned.

Calculate Your Income Protection Needs

Identify your income exposure by calculating monthly rent multiplied by your expected vacancy period during major repairs. If you collect $1,500 monthly and assume three months of downtime after a covered loss, loss of rent coverage should reimburse at least $4,500. This math prevents you from underinsuring income protection and keeps you cash-flow positive even after disaster strikes.

Assess Risk Factors and Deductible Options

Risk assessment shapes your deductible and liability choices in ways that generic online quotes cannot. Minnesota winter weather causes ice dams and frozen pipes that damage older properties more severely, so properties built before 1978 often need lower deductibles than newer construction to justify claim frequency. Conversely, if your Maple Plain rental sits in a low-crime area with minimal neighborhood risk, a higher deductible reduces premium costs without materially increasing your financial exposure.

Liability limits demand serious attention-Minnesota courts award substantial premises liability judgments, which means $100,000 in standard liability coverage leaves you severely underprotected if someone is injured on your property. Standard landlord policies typically offer $100,000 to $300,000 in liability, but if you own multiple rental properties, umbrella liability of $1 million or more across your entire portfolio becomes essential. Medical payments coverage of $1,000 to $5,000 per person pays immediate medical bills for guest injuries without litigation and often costs just a few dollars monthly, making it an inexpensive way to prevent lawsuits before they start.

Compare Quotes from Multiple Carriers

Once you’ve assessed dwelling, contents, income, and liability needs, contact an independent agency for personalized quotes from multiple carriers. An independent agency based in your region shops Minnesota’s top-rated insurers to show you real options side by side, with clear explanations of what each policy actually covers so you understand deductibles, riders, and coverage limits before you commit.

Final Thoughts

Protecting your Maple Plain rental property requires dwelling coverage that matches actual rebuild costs, liability limits that reflect Minnesota court judgments, and loss of rent protection that keeps you solvent when disaster strikes. You need to know your property’s true replacement cost, calculate your income exposure, and understand which optional coverages address your specific risks rather than padding your premium with unnecessary add-ons. The foundation of smart Maple Plain landlord insurance starts with these three decisions and moves forward from there.

Your next step is straightforward: gather your property details and contact an independent agency that shops multiple carriers for personalized quotes. An agent familiar with Minnesota rental properties identifies gaps that online systems miss and structures your policy around your actual exposure, not a template. Your coverage works best when it reflects your property’s age, location, occupancy status, and financial situation rather than following a one-size-fits-all approach.

We at Variant Insurance Group work for you, not a single insurance company, and we specialize in shopping Minnesota’s top-rated insurers to find coverage that fits your exact needs and budget. We review your options, compare protection and pricing, and explain what each policy actually covers so you understand your limits and deductibles before you commit. Contact Variant Insurance Group today for a personalized review of your rental property’s coverage needs.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation