Running an Airbnb in Minnesota comes with real financial risks. Guest injuries, property damage, and theft can happen, and your standard homeowners policy likely won’t cover them.

At Variant Insurance Group, we know that Airbnb liability coverage in Minnesota is often misunderstood. This guide walks you through the actual risks you face and the coverage options that protect your investment.

What Liability Risks Do Airbnb Hosts Actually Face in Minnesota

Guest Injuries Create Direct Financial Exposure

Guest injuries on your property expose you to immediate liability. If a guest slips on your stairs, falls from a balcony, or gets injured in a hot tub, they can sue you directly for medical bills, lost wages, and pain and suffering. Minnesota courts award significant damages in premises liability cases. Your homeowners policy explicitly excludes business activities like short-term rentals, meaning you remain personally liable for these costs. A guest’s medical emergency can drain your finances before any insurance claim is even filed. The Minnesota Department of Commerce has documented cases where hosts faced six-figure liability judgments because they lacked proper coverage.

Property Damage Claims Exceed Standard Coverage Limits

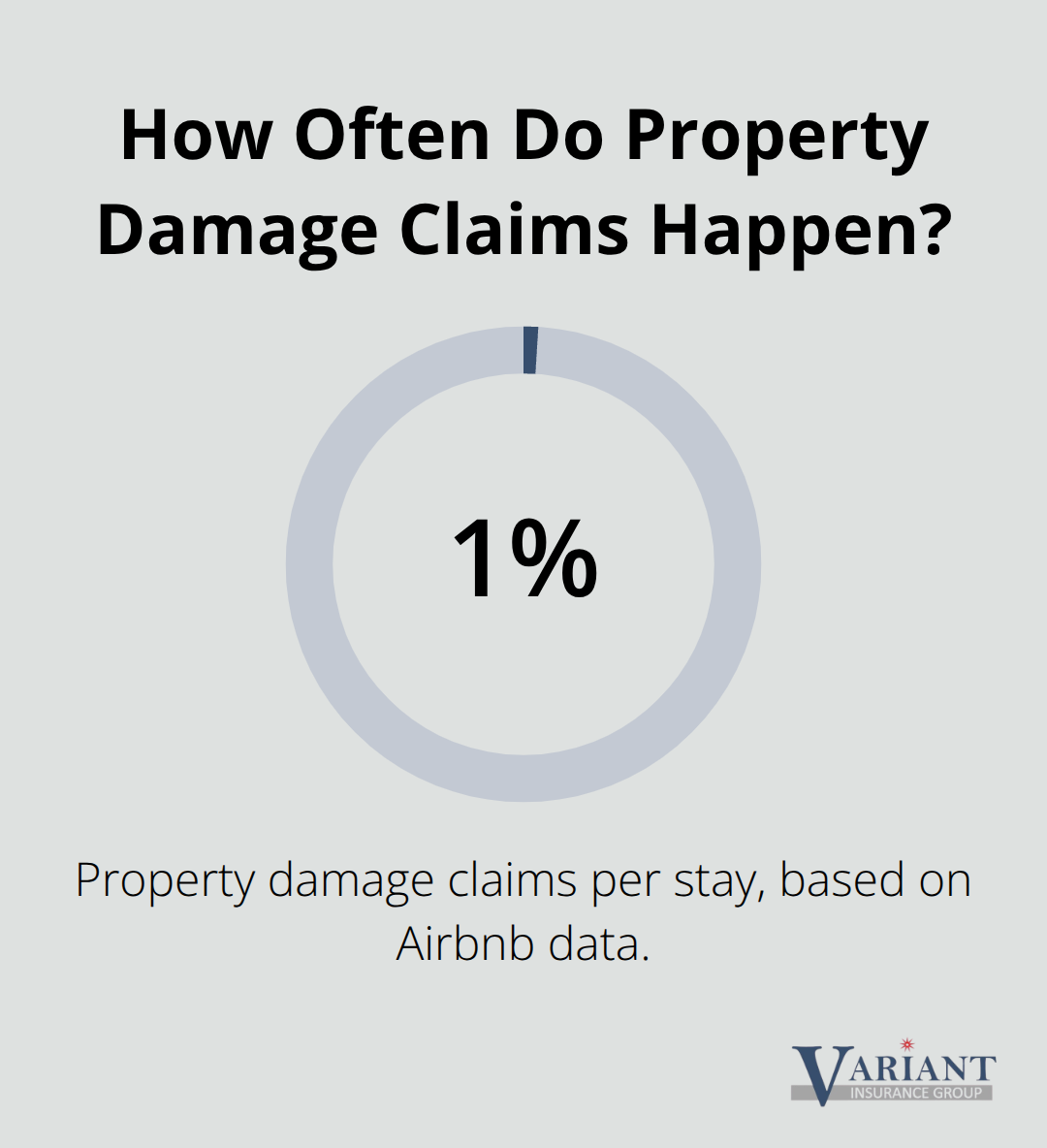

Guests cause real damage to short-term rental properties. Broken windows, damaged furniture, stained carpets, and holes in walls occur regularly in Minnesota Airbnb listings. According to Airbnb’s own data, approximately 1 in 100 stays result in some form of property damage claim. In Minnesota, repair costs for a damaged kitchen or bathroom easily reach $3,000 to $8,000.

Airbnb’s Host Protection Insurance covers up to $1,000,000 per occurrence, but this operates as a reimbursement program, not traditional insurance. You must file claims within 14 days of checkout with photos and repair estimates. If you miss the deadline or lack documentation, you receive nothing. Standard homeowners policies won’t cover any of this because the damage occurred during a rental activity.

Theft and Guest-Related Loss Require Specialized Protection

Guest theft happens more often than hosts expect. Guests steal electronics, jewelry, artwork, and even appliances from Minnesota properties. Airbnb’s Host Protection excludes theft without forced entry, which covers most guest theft scenarios since guests have legitimate access to your home. Your homeowners policy won’t cover theft related to short-term rental activity. If a guest steals your television or your guest’s friend steals a bicycle you provide, you absorb the loss. Specialized short-term rental policies (such as those offered through Proper Insurance, which VRBO endorses) specifically cover guest theft and property entrustment. These policies protect items guests steal, damage intentionally, or lose during their stay. Minnesota hosts with high-value furnishings or amenities like hot tubs and kayaks need this coverage because standard policies leave these gaps wide open.

Understanding these three liability categories-guest injuries, property damage, and theft-shows why your current homeowners policy falls short. The coverage options available to Minnesota Airbnb hosts address these gaps in different ways, each with distinct advantages and limitations.

Coverage Options That Protect Minnesota Airbnb Hosts

Airbnb’s Host Protection Insurance: A Reimbursement Program, Not True Insurance

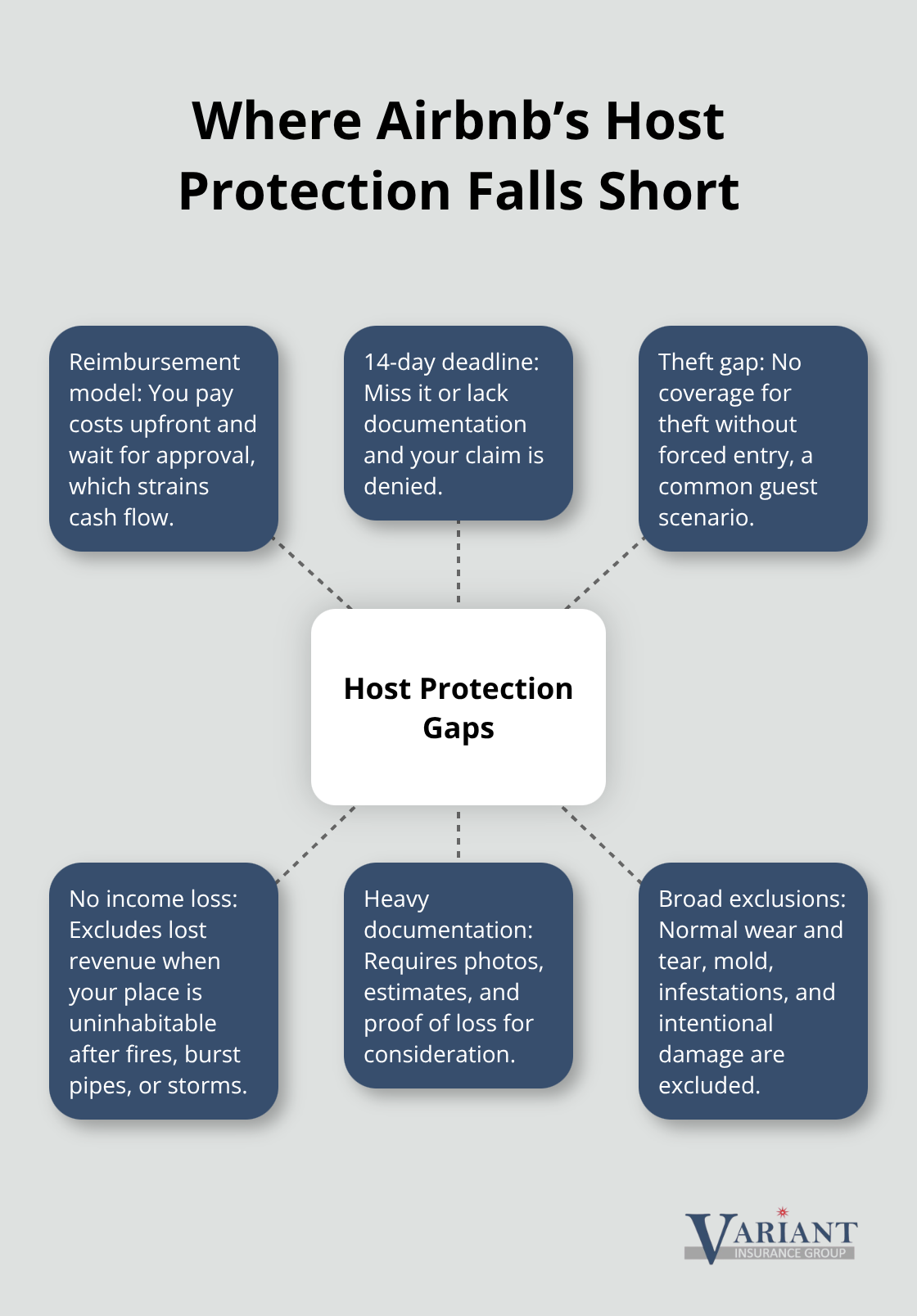

Airbnb’s Host Protection Insurance provides an important first layer of defense, but Minnesota hosts who understand how it actually works quickly realize it falls short. The program covers up to $1 million in host liability for bodily injury and property damage, plus up to $3 million for guest-caused property damage. However, this operates as a reimbursement program rather than traditional insurance. You must file claims within 14 days of checkout through Airbnb’s Resolution Center with photos, repair estimates, and proof of loss. Miss that deadline or lack documentation, and Airbnb denies your claim entirely. The coverage also excludes normal wear and tear, mold, infestations, intentional damage, and theft without forced entry.

For Minnesota hosts, this means a guest who steals your electronics or intentionally damages your kitchen cabinets leaves you unprotected. Airbnb’s protection also excludes lost income when your property becomes uninhabitable due to kitchen fires, burst pipes, or severe storms. The Minnesota Department of Commerce specifically warns hosts that this reimbursement model is not a substitute for proper insurance because you personally cover all costs upfront while waiting for claim approval.

Why Your Homeowners Policy Leaves You Exposed

Your standard homeowners policy actively works against you as an Airbnb host in Minnesota. Insurance carriers view short-term rental activity as a commercial business, and homeowners policies explicitly exclude business liability. A guest who sues you for injuries sustained on your property will find your homeowners insurer denies the claim, leaving you personally responsible for legal fees and damages. Minnesota courts have awarded judgments exceeding $100,000 in premises liability cases involving short-term rentals. Your current policy provides zero protection for the three liability categories that destroy unprotected Minnesota hosts: guest injuries, property damage, and theft.

Specialized Short-Term Rental Policies Address the Real Gaps

Specialized short-term rental insurance policies fill these gaps directly. These policies provide unmatched property, business liability and lost revenue coverage for short-term rental hosts, including owners and arbitrageurs. For Minnesota properties valued between $200,000 and $500,000, comprehensive short-term rental policies cost approximately $800 to $2,400 annually. Lake-area properties in Duluth see 40 to 60 percent higher premiums due to increased water damage and liability exposure. Downtown Minneapolis listings run 25 to 35 percent higher than suburban properties because of density and foot traffic. This pricing remains substantially lower than the financial exposure you face with inadequate coverage.

How to Evaluate Your Current Protection Level

The gap between what Airbnb covers and what you actually need depends on your specific property and guest volume. A host with a modest suburban home and occasional rentals faces different risks than someone operating a downtown Minneapolis property with high turnover. Your property type, location, and the amenities you offer (hot tubs, kayaks, expensive furnishings) all affect which coverage gaps matter most. The next section walks you through assessing your exact needs and comparing the coverage options that actually protect your investment.

How to Assess Your Coverage Needs and Compare Your Options

Evaluate Your Property Type and Guest Activity

Your property basics determine exactly what coverage level you need. A downtown Minneapolis one-bedroom apartment with high turnover faces completely different risks than a Duluth lake house rented occasionally. Hosts operating in dense urban areas pay 25 to 35 percent higher premiums than suburban properties because foot traffic and density increase injury liability exposure. Lake-area properties cost 40 to 60 percent more due to water-related injuries and damage claims.

Count your annual guest stays and identify your amenities. If you offer hot tubs, kayaks, or high-value furnishings, you need coverage that protects these items specifically. Airbnb’s Host Protection excludes theft without forced entry, meaning guest theft of your amenities leaves you unprotected. Specialized short-term rental policies include amenity liability explicitly, covering bikes, kayaks, pools, and hot tubs whether on-site or off-site.

Calculate Your Annual Coverage Costs

Properties valued between $200,000 and $500,000 with standard amenities typically cost $800 to $2,400 annually for comprehensive short-term rental coverage. This pricing varies based on location premium and your claims history. High-turnover properties in Minneapolis often fall at the higher end of this range. Once you know your property category and guest volume, you can compare what Airbnb’s reimbursement program actually covers versus what you genuinely need.

Compare Coverage Limits and Exclusions

Comparing actual coverage limits requires reading the exclusions, not just the headline numbers. Airbnb provides $1 million in host liability and $3 million in guest damage coverage, but the $3 million applies only to guest-caused incidents, not all property damage. The 14-day claims deadline eliminates coverage if you discover damage after checkout or lack documentation.

Specialized policies remove this deadline problem entirely. Proper Insurance offers business revenue protection with no time limit on actual loss sustained, meaning if a guest causes damage that forces you to cancel bookings for weeks, you recover that lost income. Your deductible choice directly impacts your annual premium and out-of-pocket costs per claim. A $1,000 deductible on a comprehensive short-term rental policy costs less annually than a $500 deductible, but you pay more when claims occur.

Minnesota hosts with properties valued over $300,000 should avoid high deductibles because guest damage claims frequently exceed $5,000. Check whether the policy covers loss of bookings due to non-guest events like kitchen fires or burst pipes. Airbnb explicitly excludes income loss from these scenarios. Proper Insurance includes business revenue protection that covers actual loss sustained with no time limits, addressing the exact gap Airbnb leaves open.

Review Theft Coverage and Guest-Related Protections

Review whether theft coverage requires forced entry. Airbnb excludes guest theft entirely unless a guest forced entry to steal something. Proper Insurance covers guest theft and property entrustment without forced entry requirements. For Minnesota hosts, this difference matters because guests have legitimate access to your home.

Confirm whether the policy covers squatters protection and legal support if a guest refuses to leave. Standard homeowners policies and Airbnb provide nothing here. Proper Insurance includes legal support and lost revenue protection specifically for this scenario, which protects hosts managing longer stays that turn problematic.

Final Thoughts

Running an Airbnb in Minnesota without proper liability coverage exposes you to financial devastation. Guest injuries, property damage, and theft can occur on any stay, and your homeowners policy will deny every claim because short-term rental activity falls outside standard coverage. Airbnb’s Host Protection Insurance provides a starting point, but its 14-day claims deadline, theft exclusions, and income loss gaps leave you personally responsible for thousands in damages and lost bookings.

The reality is straightforward: Airbnb liability coverage in Minnesota requires more than platform protection. Specialized short-term rental policies address the exact gaps that destroy unprotected hosts by covering guest theft without forced entry requirements, providing business revenue protection with no time limits, and including amenity liability for hot tubs, kayaks, and other high-value items. For Minnesota properties valued between $200,000 and $500,000, comprehensive coverage costs $800 to $2,400 annually-a fraction of what a single major claim costs.

Contact an independent insurance agency that understands Minnesota’s short-term rental landscape to review your current protection and secure the coverage that keeps your investment financially safe. We at Variant Insurance Group shop Minnesota’s top-rated insurance companies to find the policy that actually protects your Airbnb investment. Our team compares protection levels and pricing across multiple carriers based on your property type, guest volume, and specific amenities.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation