Your commercial property needs protection that actually works when disaster strikes. At Variant Insurance Group, we help Minnesota business owners find the best commercial property insurance companies that match their specific risks and budgets.

Choosing the right coverage means understanding what protects your building, equipment, and inventory-and knowing which insurers deliver when you file a claim. This guide walks you through the selection process step by step.

What Protects Your Business and What It Costs

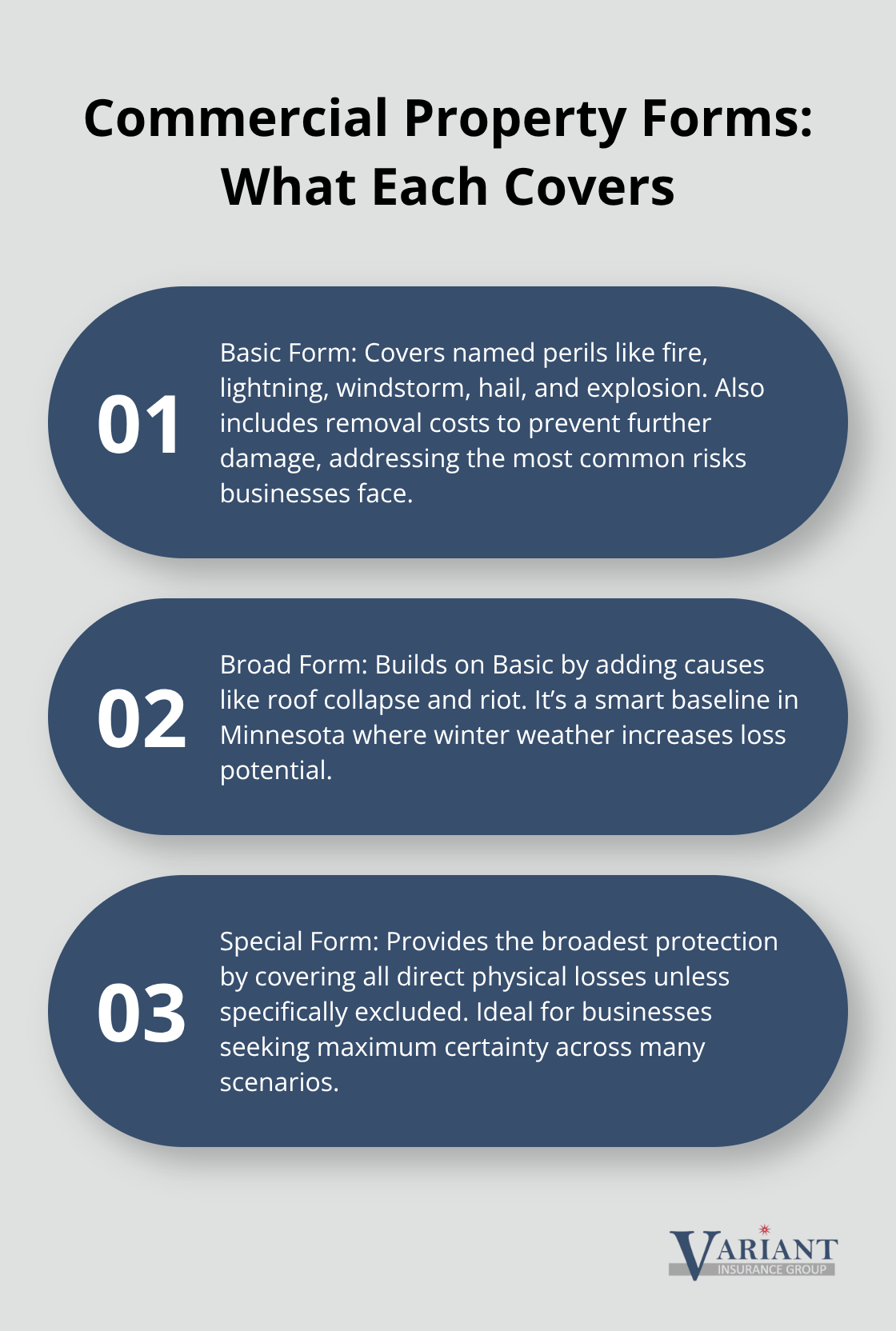

Commercial property insurance comes in three main forms, and your choice determines what actually gets covered when damage occurs. The Basic form covers fire, lightning, windstorm, hail, explosion, and removal costs to prevent further damage-these are the most common perils Minnesota businesses face. The Broad form adds roof collapse and riot to that foundation. The Special form provides the widest protection, covering all direct physical losses except those explicitly excluded. Most Minnesota business owners should select at least the Broad form because winter weather and storms strike frequently here.

When you select your form, you also choose between Actual Cash Value, which depreciates what you lost, and Replacement Cost, which pays to rebuild with similar-quality materials without that depreciation penalty. Replacement Cost costs more upfront but protects you from absorbing depreciation losses, which is why it’s the stronger choice for most businesses.

Building Coverage and Equipment Protection

Your building structure needs protection separate from your contents. Building coverage pays for repairs or replacement of the physical structure and fixtures like built-in shelving or HVAC systems. Equipment coverage handles damage to machinery, computers, production equipment, and other gear essential to running your operation. If you lease your space, don’t assume your landlord’s insurance covers your equipment or inventory-landlords typically insure only the structure. You need your own commercial property policy to protect what you own. For high-value items like specialized machinery or artwork, obtain a formal appraisal and request an agreed-upon amount endorsement so the insurer commits to that value without depreciation.

Premium Costs and Deductible Decisions

According to Insureon data, the average small-business property premium runs about 67 dollars per month, though this varies significantly based on property type, building age, location, and deductible. Your deductible directly impacts your premium: selecting a 2,500-dollar deductible instead of 500 dollars can lower your annual cost substantially, but only if you can actually cover that amount out of pocket after a loss. About 80 percent of small businesses now manage policies online, which means you should verify your carrier offers digital claims filing and status tracking.

Financial Strength and Equipment Breakdown Coverage

When disaster strikes, your insurer’s response speed matters more than the premium you paid. Request quotes from carriers with strong financial ratings-The Hartford, Chubb, and Liberty Mutual all carry A or higher ratings from AM Best, the agency that measures insurance company stability.

Roughly 35 percent of claims in Minnesota’s manufacturing sector involve equipment breakdown, so if you operate industrial equipment, confirm your policy includes equipment breakdown coverage or add it as an endorsement.

Business Interruption and Documentation

Business interruption coverage protects your lost income and ongoing expenses like payroll and utilities when a covered event forces a temporary shutdown. This coverage typically has a waiting period (often 24 or 48 hours) before benefits start, so factor that into your decision. Before purchasing any policy, have your property professionally valued and keep detailed receipts or photos of equipment and inventory stored in multiple locations. This documentation streamlines claims processing and prevents disputes over loss amounts. With your property protection strategy in place, the next step involves identifying which Minnesota insurers actually deliver the financial strength and local expertise your business needs.

Which Minnesota Insurers Deliver When You Need Them Most

The Hartford’s Manufacturing Focus and Financial Strength

The Hartford stands out as the strongest choice for Minnesota manufacturers and established businesses seeking comprehensive coverage with deep industry expertise. According to AM Best ratings, The Hartford carries an A+ financial strength ratings, meaning your claims will be paid when equipment fails or property damage strikes. The Hartford’s Business Owner’s Policy bundles property and liability coverage, and their risk management resources specifically address manufacturing challenges like equipment breakdown. Liberty Mutual and Chubb both maintain A-level ratings and offer similar bundled protection, but The Hartford’s manufacturing focus makes it the preferred option for industrial operations.

Smaller Businesses and Competitive Pricing Options

For smaller businesses and startups, Hiscox provides highly customizable policies with strong online management tools, though it lacks standalone commercial property insurance, so you’d need to pair it with a separate property policy from another carrier. Acuity Insurance carries an A+ rating and appeals to businesses seeking competitive pricing without sacrificing financial stability. Your actual cost depends on building condition, location, and whether you select a higher deductible to lower premiums.

Minnesota’s Broker Network and Local Expertise

Minnesota’s broker network through the Minnesota Chamber of Commerce connects you with vetted insurance agencies across the state, including national firms like Marsh & McLennan Agency and Gallagher alongside regional specialists. This network matters because local brokers understand Minnesota’s specific risks-severe winter weather exposure, agricultural volatility in certain regions, and manufacturing concentration in specific areas. Brokers access multiple carriers simultaneously, comparing coverage limits and deductibles to find genuine value rather than pushing you toward a single company’s products.

Building Your Quote Comparison Strategy

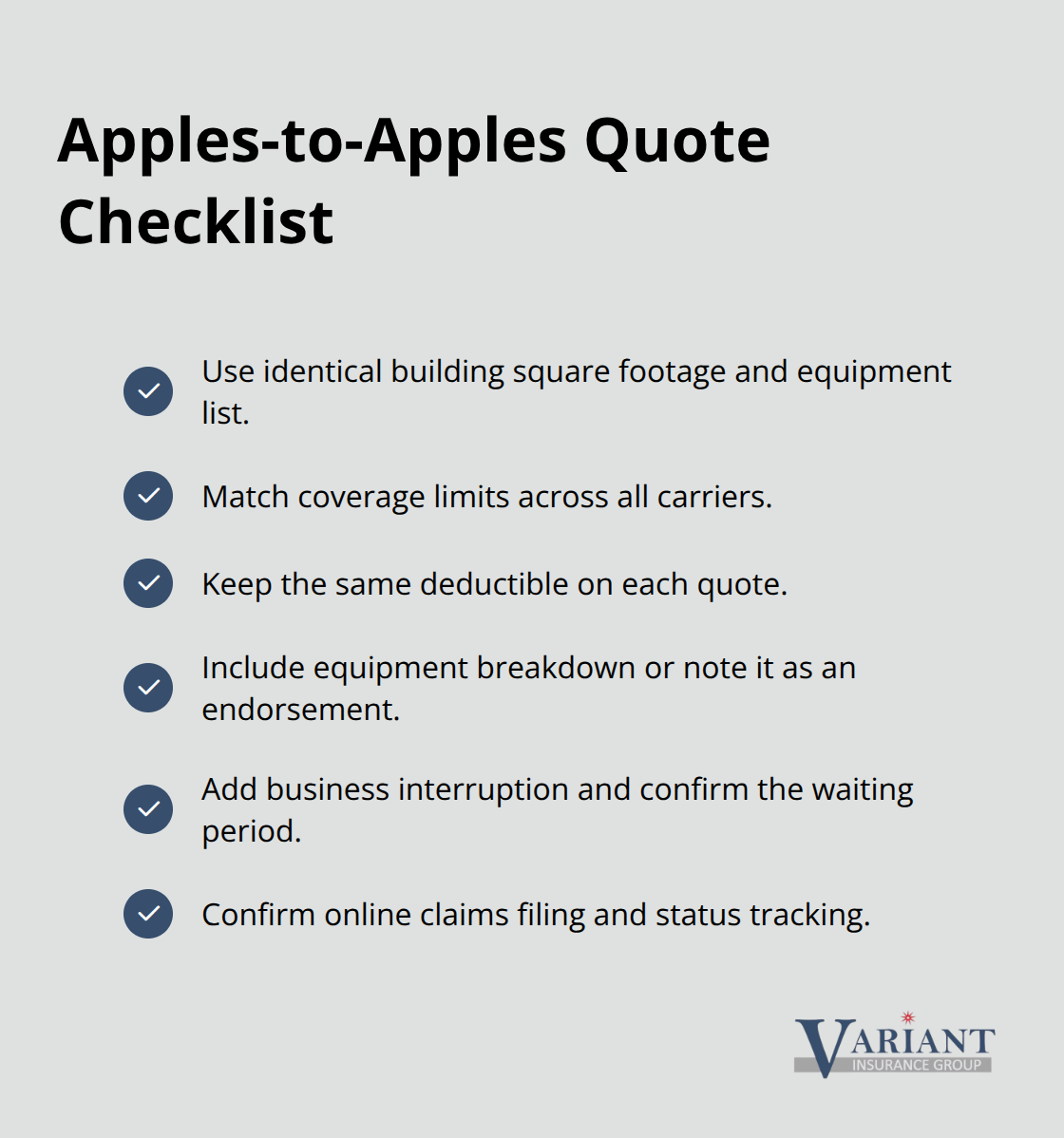

When evaluating any insurer, demand an apples-to-apples quote comparison showing identical coverage limits, deductibles, and endorsements across three carriers minimum. Equipment breakdown coverage should be included or available as an endorsement if you operate machinery. Business interruption coverage, which protects lost income during shutdowns, typically costs extra but proves essential if a single event could threaten payroll or lease obligations. Confirm your chosen carrier offers online claims filing and status tracking, since digital policy management has become standard.

Verifying Financial Strength and Policy Details

Request financial strength ratings directly from AM Best rather than relying on carrier marketing claims, and verify that your policy includes agreed-upon value endorsements for high-value equipment or inventory to prevent depreciation disputes during claims. Once you’ve narrowed your options based on financial strength and coverage flexibility, the next step involves assessing your own property and assets to determine exactly what protection you actually need.

Selecting Coverage That Matches Your Actual Business

Document Your Property and Assets

Start by recording exactly what you own and what replacement would cost. Walk through your building and photograph or video your equipment, inventory, furniture, computers, and any specialized machinery your operation depends on. This inventory establishes your baseline for determining coverage limits. Many Minnesota business owners underinsure because they estimate property values instead of measuring them. If you operate a manufacturing facility with equipment worth 500,000 dollars, you need building coverage reflecting that reality, not a guess. For specialty items like artwork, antiques, or high-value machinery, hire a professional appraiser and provide that report to your insurer. This step prevents the painful discovery during a claim that your coverage limit falls short of actual replacement costs.

Organize Your Financial Records

Keep receipts for major purchases and store copies in cloud storage separate from your physical location. If a fire destroys your office, you need proof of what you owned to support your claim amount. Digital backups in multiple locations protect your documentation from the same disaster that damages your property. This preparation streamlines claims processing and prevents disputes over loss amounts.

Request Quotes Using Identical Specifications

Request quotes from at least three carriers using the same building square footage, same equipment list, same coverage limits, and the same deductible across all quotes. Request quotes with a 2,500-dollar deductible, then ask what the premium drops if you increase it to 5,000 dollars. Some Minnesota businesses can absorb a higher deductible and save 15 to 20 percent annually.

Compare Coverage Details and Endorsements

Compare whether each quote includes equipment breakdown coverage or charges extra for it as an endorsement. Ask specifically whether business interruption coverage is bundled into a Business Owner’s Policy or sold separately, and what the waiting period is before benefits begin. Verify that any high-value items are covered under agreed-upon value endorsements rather than depreciated actual cash value, which protects you from losing money to depreciation calculations during claims settlement.

Final Thoughts

Selecting the best commercial property insurance companies for your Minnesota business requires three core actions: matching coverage types to your actual assets, comparing financial strength across carriers, and choosing an insurer that responds quickly when you file a claim. You now understand the difference between Basic, Broad, and Special forms, know why Replacement Cost protects you better than Actual Cash Value, and recognize that equipment breakdown coverage matters if you operate machinery. Financial ratings from AM Best tell you whether your insurer can actually pay claims, and local brokers give you access to multiple carriers simultaneously rather than locking you into one company’s limited options.

The real advantage of working with a local agency is having someone who understands Minnesota’s specific risks and can navigate policy details on your behalf. Winter weather, manufacturing concentration in certain regions, and seasonal business volatility all shape what coverage makes sense for your operation. A local agent compares quotes from multiple carriers, explains what each endorsement actually costs, and adjusts your coverage as your business changes.

Document your property and assets, request quotes from at least three carriers using identical specifications, and schedule a consultation with a local agent who can explain what each quote actually covers. Contact Variant Insurance Group to discuss your commercial property protection and get quotes that match your business’s real risks and budget.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation