If you own rental property in Minnesota, you’re probably wondering whether rental property insurance premiums can reduce your tax bill. The answer is yes-but only if you follow IRS rules carefully.

At Variant Insurance Group, we help landlords understand what’s deductible and what isn’t. This guide walks you through the tax rules, documentation requirements, and common mistakes that cost landlords money.

What Counts as Rental Property Insurance

Rental property insurance differs fundamentally from homeowners insurance, and Minnesota landlords often make expensive mistakes by treating them the same way. The IRS considers rental property insurance a deductible business expense only when it protects your financial interest in the rental activity itself. This means the policy must cover the building, not the tenant’s belongings, and you as the property owner must purchase and pay for it. If a tenant reimburses you for insurance costs, that reimbursement becomes taxable income, and you lose the deduction entirely. The coverage must relate directly to your rental operation-policies that cover general liability, property damage, fire, water damage, and weather events all qualify. Minnesota’s climate creates specific insurance needs that are fully deductible, including ice dam damage coverage and basement flooding protection (both common concerns for rental properties in our state).

Coverage Types That Reduce Your Tax Bill

Fire insurance, wind and hail coverage, and water damage protection form the foundation of most rental policies and are completely deductible. General liability coverage that protects you against tenant or visitor injuries also qualifies for deduction. Specialized coverages like loss of rents insurance (which covers your income if the property becomes temporarily uninhabitable) are equally deductible because they protect your rental income directly. Workers compensation insurance qualifies for deduction if you employ maintenance staff or contractors on your property. The key principle remains straightforward: if the policy protects your rental business interests rather than tenant possessions, the premium is deductible in the year you pay it, regardless of when the policy period ends. Many Minnesota landlords overlook how much they can deduct by not recognizing that umbrella liability policies extending to rental properties also qualify for deduction.

Understanding What Insurance Costs

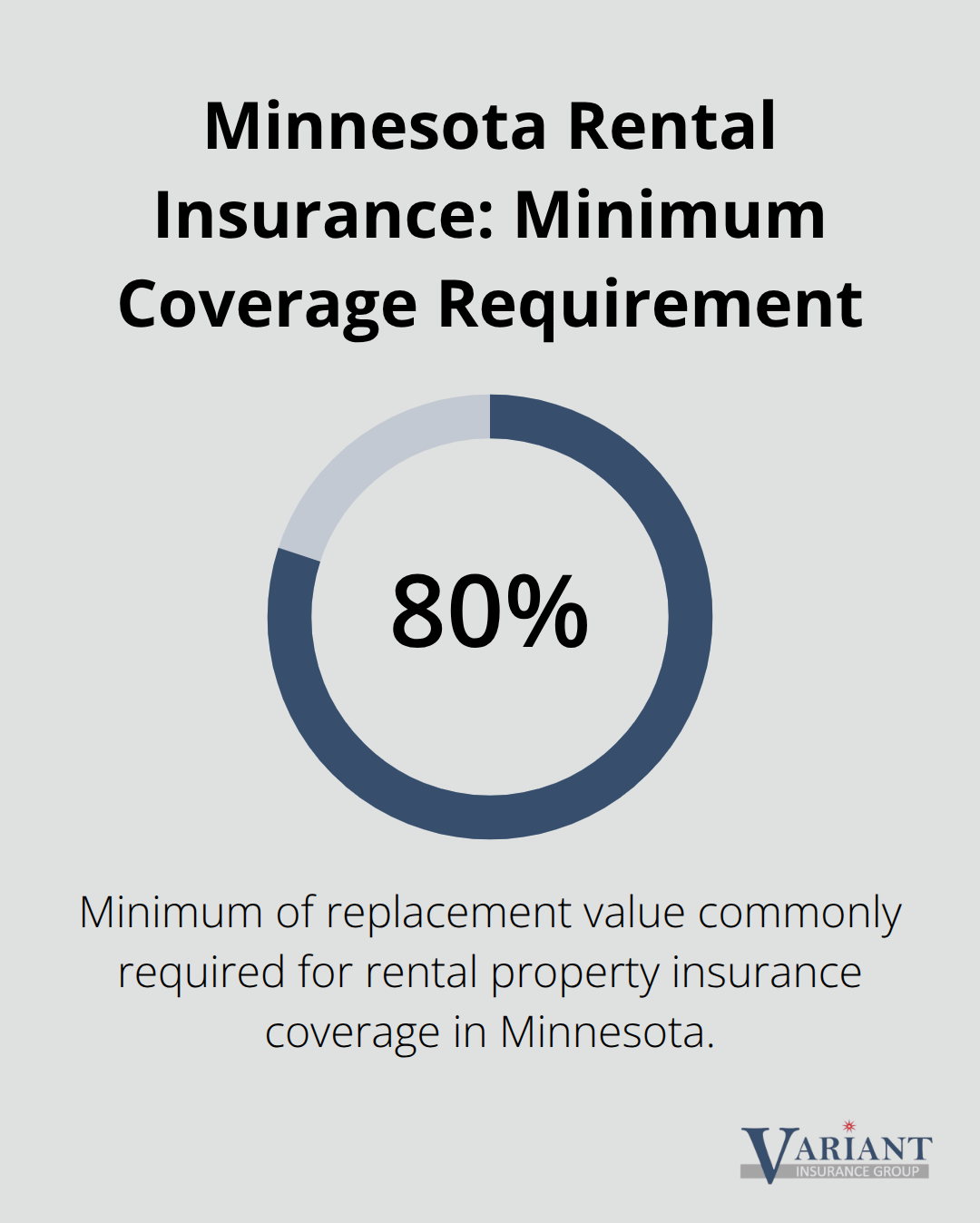

Rental property insurance premiums in Minnesota typically require minimum coverage of 80 percent of the replacement value of the house. Your specific premium depends on the property’s construction type, whether it’s single-family or multi-unit, loss history, and local risk factors like flood zones. Properties in flood-prone areas pay substantially more, sometimes 2 to 3 times the standard rate. Insurance companies also consider whether the property is owner-occupied or fully rented, with fully rented properties typically costing more to insure. When you calculate your actual tax deduction, you deduct the full premium amount in the year you pay it-not when coverage begins or ends-making December premium payments valuable for year-end tax planning.

How Payment Method Affects Your Deduction

The way you pay your insurance premium directly impacts your tax deduction eligibility. You must pay the premium yourself as the property owner; if tenants cover the cost and you reimburse them, the IRS treats that reimbursement as rental income rather than an insurance expense. This distinction costs landlords thousands in lost deductions annually. You deduct the full premium in the year you actually pay it, even if the policy covers multiple years ahead. This timing rule creates an opportunity: paying your annual premium in December rather than January can shift the deduction to the current tax year and reduce your current year’s tax liability. Keeping detailed records of payment dates, policy numbers, and which properties each premium covers protects your deduction if the IRS audits your return.

Now that you understand what qualifies as deductible rental property insurance and how much these policies typically cost, the next critical step involves navigating the specific IRS rules that govern these deductions and maintaining the documentation that proves your eligibility.

Tax Deductibility of Rental Property Insurance

IRS Rules on Deducting Insurance Expenses

The IRS classifies rental property insurance as an ordinary and necessary business expense, which means you can deduct the full premium amount against your rental income in the year you pay it. This rule applies whether your policy covers one property or ten properties across Minnesota. According to IRS Publication 527, which governs rental property taxation, insurance premiums rank alongside mortgage interest, property taxes, and repairs as core deductible expenses. The critical requirement is that you, the property owner, must purchase and pay for the insurance directly. If a tenant pays the premium and you reimburse them, that reimbursement becomes taxable rental income, and you forfeit the deduction entirely.

Minnesota property managers can deduct fire insurance, general liability coverage, workers compensation, ice dam damage protection, and basement flooding insurance without limitation. The timing of your payment matters significantly: if you pay a December premium that covers January through December of the following year, you still deduct the full amount in the year you paid it, not when coverage begins. This creates a legitimate tax planning opportunity that many landlords ignore. For properties with mortgages, your lender typically requires proof of active coverage, so maintaining continuous insurance and paying promptly serves both legal and financial purposes.

Documentation Required for Tax Deductions

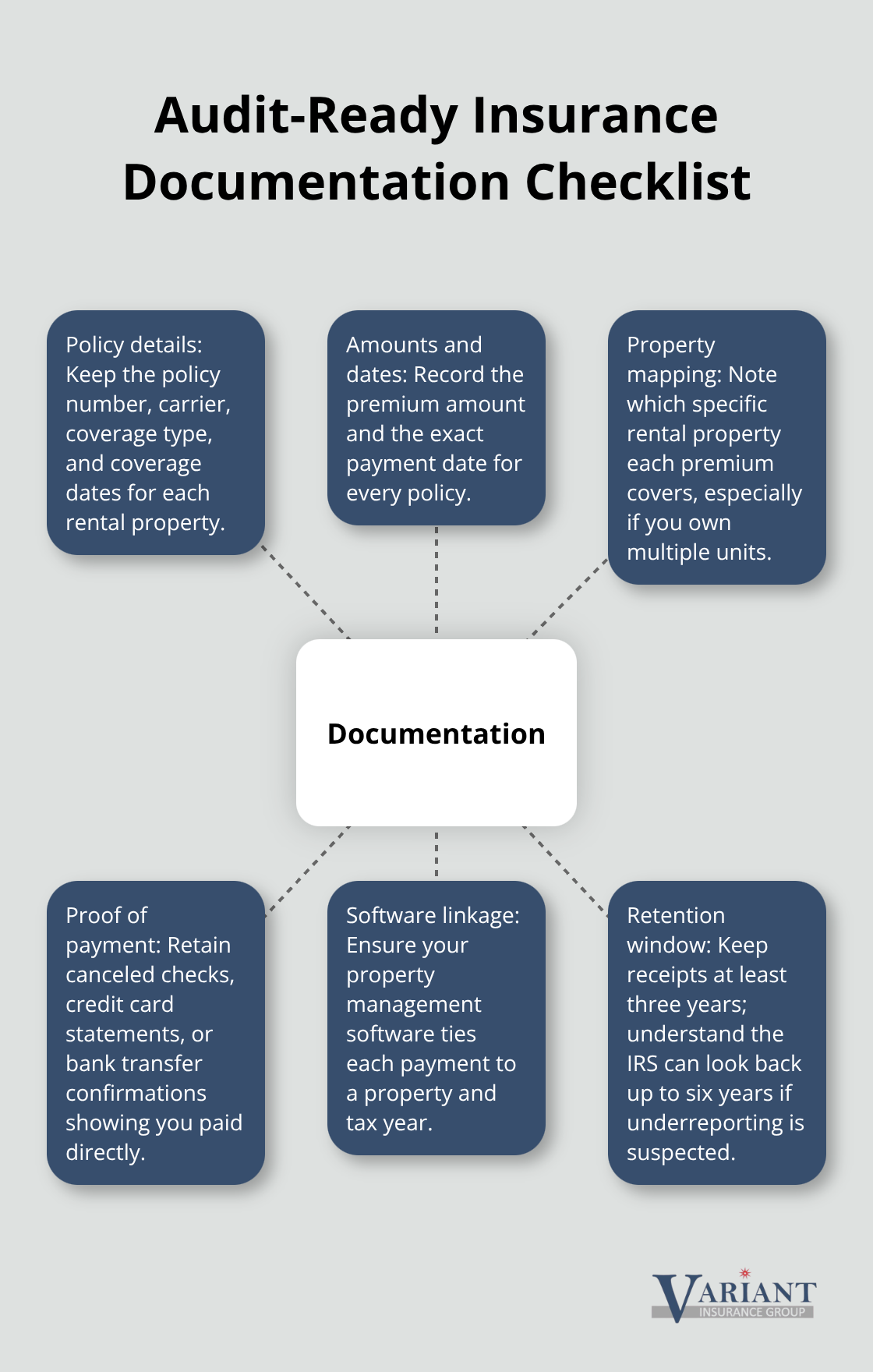

Documentation separates landlords who successfully claim deductions from those who lose them during audits. You need to maintain records showing the policy number, coverage dates, premium amount, payment date, and which property the policy covers if you own multiple rentals. The IRS expects canceled checks, credit card statements, or bank transfers showing you paid the premium directly.

If you use property management software to track expenses, ensure it clearly links each insurance payment to the specific property and tax year.

Minnesota’s Department of Revenue recommends keeping receipts for at least three years, though the IRS can go back six years if they suspect underreporting. A simple spreadsheet showing date, property address, policy number, coverage type, premium amount, and payment method gives you everything needed to defend your deductions confidently.

Common Mistakes Landlords Make When Claiming Deductions

Common mistakes cost landlords their deductions: mixing tenant-paid insurance with owner-paid insurance in your records, failing to distinguish between insurance premiums and security deposits in your accounting, and not allocating multi-property policies correctly. Some landlords deduct insurance expenses they didn’t actually pay or claim coverage that doesn’t relate to rental activity. Others fail to separate ice dam and basement flooding premiums from standard coverage, which is a particular mistake in Minnesota where these weather-related risks are substantial.

These errors often stem from poor record-keeping practices rather than intentional fraud. Landlords who maintain organized documentation from the start avoid these pitfalls entirely. The effort required to track insurance payments properly takes minimal time but provides maximum protection if the IRS questions your return.

Understanding how the IRS treats your insurance deductions and what documentation you need sets the foundation for maximizing your overall tax benefits. Beyond insurance, rental property owners can deduct numerous other expenses that directly reduce their taxable income and improve their bottom line.

Maximizing Your Tax Benefits as a Landlord

Other Deductible Expenses Beyond Insurance

Rental property insurance represents only one piece of your deductible expenses. The IRS allows you to deduct mortgage interest, property taxes, repairs, maintenance costs, property management fees, utilities paid by you, advertising for tenants, and travel expenses directly tied to property upkeep. According to IRS Publication 527, these expenses reduce your taxable rental income dollar-for-dollar, which means maximizing them matters significantly for your bottom line. Many Minnesota landlords focus heavily on insurance deductions while overlooking larger deductions hiding in plain sight.

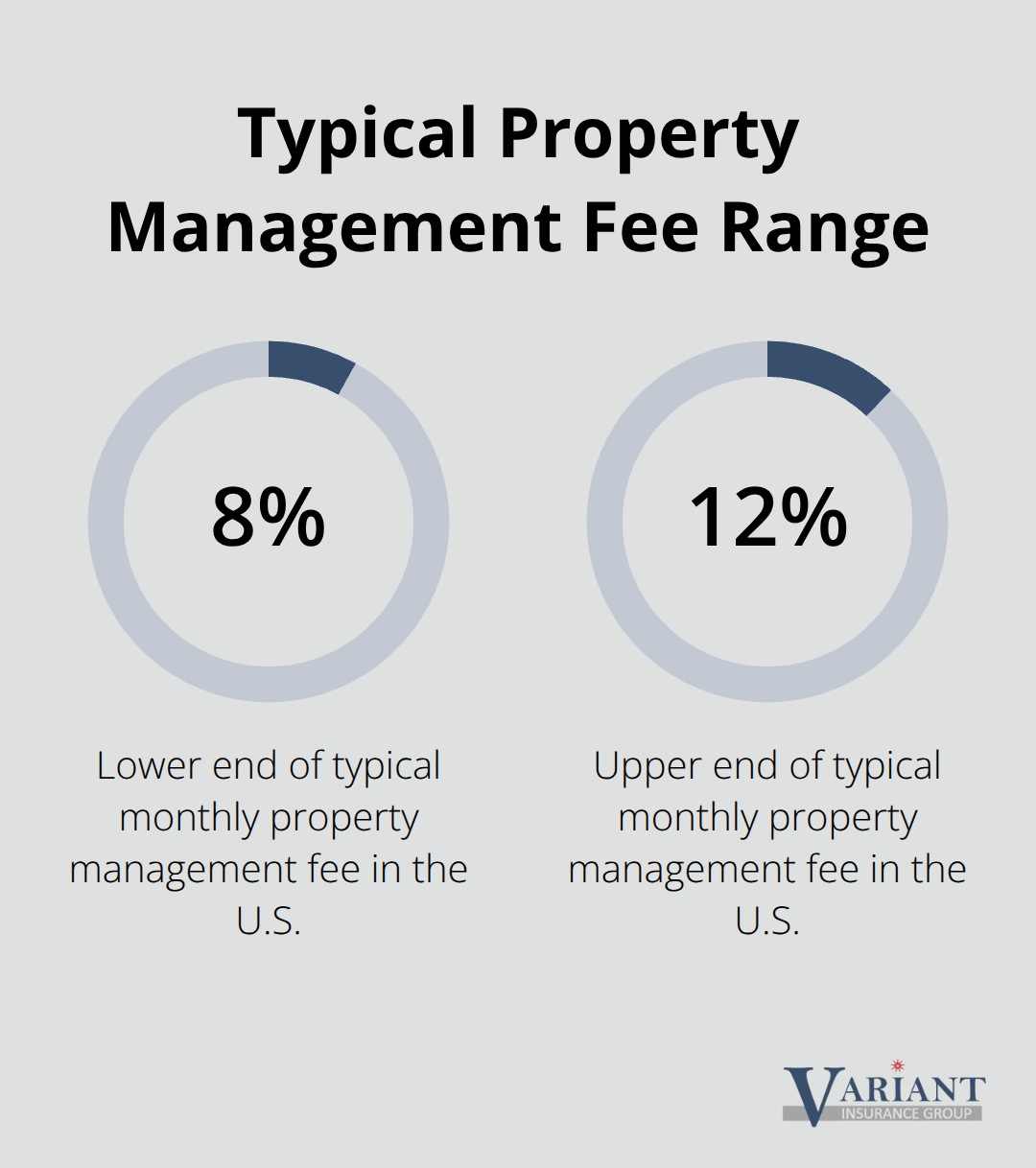

Property management fees alone typically range from 8 to 12 percent of monthly rental income, creating substantial deductions that landlords sometimes fail to claim because they don’t categorize them properly. Repairs qualify for full deduction in the year you make them, but improvements that add value require depreciation over time using Form 4562-a critical distinction that costs landlords money when confused.

If you travel to inspect properties, handle maintenance, or manage tenant issues, those mileage expenses qualify for deduction at the IRS rate, provided you document dates, destinations, and business purposes. Advertising costs for finding tenants, including online listing fees and newspaper ads, qualify entirely. The key principle separating what you can and cannot deduct is straightforward: if an expense is ordinary, necessary, and directly related to generating rental income, the IRS allows it.

Tracking and Organizing Rental Property Expenses

Organizing your expenses from the start eliminates scrambling at tax time and prevents missed deductions. Use property management software like Landlord Studio or Buildium to track expenses by property and category, automatically calculating totals for your tax return. Create separate bank accounts or credit cards for each property if you own multiple rentals, which simplifies categorization and provides clear documentation that auditors expect. Record the date, amount, vendor, property address, and expense category for every single transaction without exception.

This discipline takes minutes when done consistently but saves hours during tax preparation and protects you during audits. The IRS expects you to report all rental income separately for each property on Schedule E, and your expense documentation must match that same property-by-property breakdown. Minnesota’s Department of Revenue recommends maintaining records for at least three years, though the IRS can examine returns going back six years if they suspect underreporting.

Working with a Tax Professional for Optimal Results

A tax professional who specializes in rental properties is not optional for serious landlords. A good tax professional identifies deductions you miss, structures your depreciation strategy to minimize taxes legally, and ensures you comply with Minnesota and federal rules that change annually. The cost of professional tax preparation typically ranges from $500 to $2,000 depending on complexity, but landlords routinely recover that investment multiple times over through deductions the professional identifies.

Minnesota’s tax environment includes specific rules about passive activity losses that limit how much rental losses you can deduct in certain situations, making professional guidance essential for multi-property owners. A tax professional also handles Form 8582 and Form 6198 if your rental expenses exceed income, protecting you from penalties and audit risk. These forms require technical knowledge that most landlords lack, and mistakes on them trigger IRS scrutiny that costs far more than professional fees.

Final Thoughts

Rental property insurance tax deductibility hinges on three core requirements: the policy must protect your rental business interests, you must pay the premium directly, and you must maintain meticulous documentation. The IRS allows you to deduct the full premium amount in the year you pay it, reducing your taxable rental income dollar-for-dollar across fire insurance, liability coverage, ice dam protection, basement flooding insurance, and any other policy safeguarding your rental operation. This straightforward rule applies whether you own one property or ten properties across Minnesota.

The gap between landlords who maximize their tax benefits and those who leave money on the table almost always reflects record-keeping discipline. A simple spreadsheet or property management software system tracking payment dates, policy numbers, coverage types, and property addresses prevents costly mistakes and protects you during an IRS audit. Paired with other deductible expenses like mortgage interest, property taxes, repairs, and management fees, your insurance deductions work harder to reduce your overall tax liability.

We at Variant Insurance Group help Minnesota landlords understand their insurance needs and secure the right coverage for their rental business. Contact our team to review your current rental property insurance and explore how we can protect your investment while supporting your tax planning goals.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation