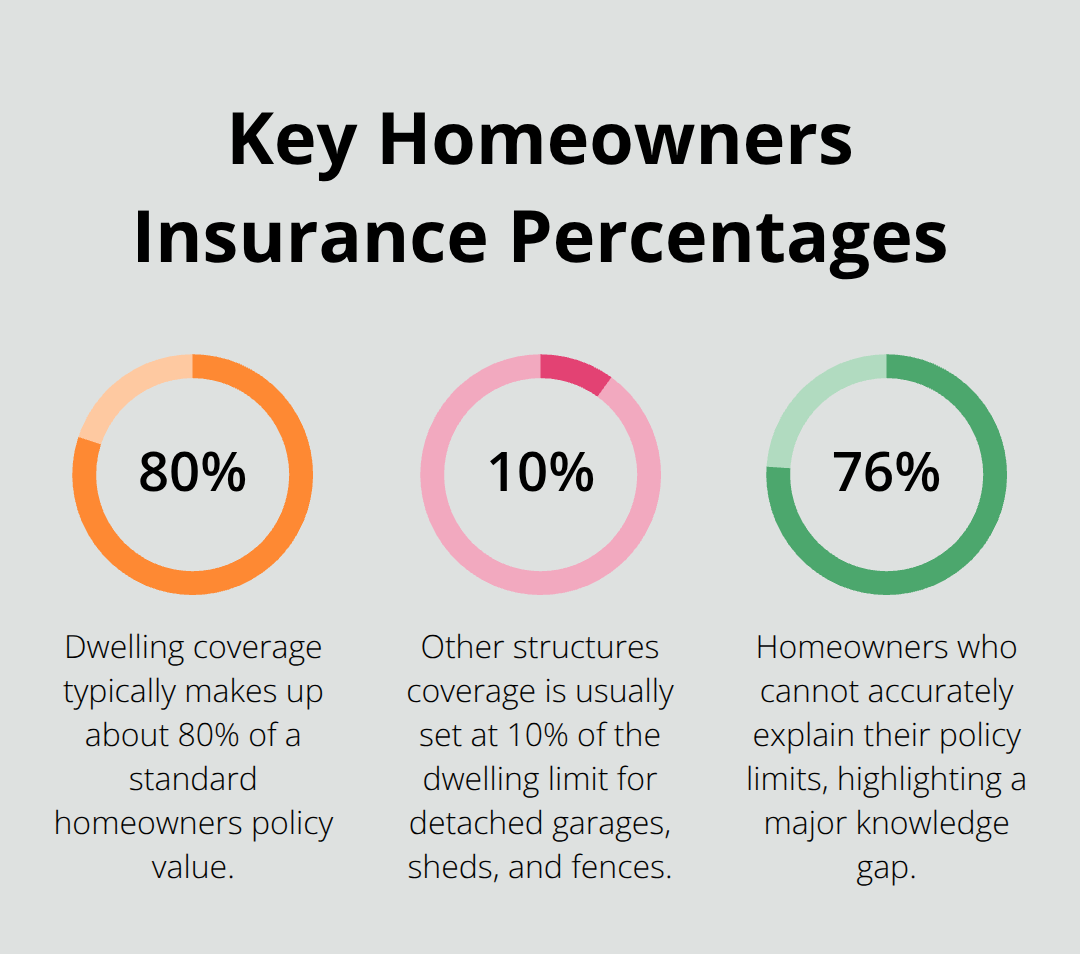

Homeowners insurance protects your biggest investment, but many Minnesota residents don’t fully understand what their policy actually covers. The average homeowner pays $1,383 annually for coverage, yet 76% can’t accurately explain their policy limits.

At Variant Insurance Group, we see confusion about coverage gaps cost families thousands in unexpected expenses. Understanding exactly what homeowners insurance covers helps you make informed decisions about protecting your property and finances.

What Protection Does Your Policy Actually Provide

Your Home Structure Gets Comprehensive Protection

Dwelling coverage forms the foundation of homeowners insurance and protects your house, attached garage, and built-in appliances against 16 named perils in most HO-3 policies. This coverage typically represents 80% of your total policy value and pays replacement cost for damages from fire, wind, hail, and vandalism. The Insurance Information Institute reports that wind and hail affect 1 in 35 homes annually, which makes this protection essential for Minnesota homeowners who face severe weather patterns.

Most insurers require coverage equal to at least 80% of your home’s replacement cost to avoid coinsurance penalties. A $300,000 home needs minimum dwelling coverage of $240,000, though full replacement cost coverage provides better protection. Other structures coverage automatically includes detached garages, sheds, and fences at 10% of your dwelling limit, but you can increase this percentage for additional premium.

Personal Property Receives Broad Coverage

Personal property protection covers furniture, electronics, clothing, and appliances at 50-70% of your dwelling coverage amount. This means a policy with $250,000 dwelling coverage includes $125,000-$175,000 for possessions. Standard policies cover personal property against the same 16 perils as your dwelling, which includes theft both at home and away from your property.

High-value items like jewelry, art, and electronics face sub-limits that range from $1,000-$5,000 per category. A stolen laptop worth $3,000 might only receive $1,500 under electronics limits. Scheduled personal property endorsements remove these restrictions and provide agreed-value coverage for specific items after professional appraisal.

Liability Protection Shields Your Assets

Personal liability coverage protects against lawsuits when someone gets injured on your property or you accidentally damage their property. Standard policies provide $100,000-$300,000 in liability protection, but legal experts recommend minimum $500,000 coverage since average bodily injury claims reach $30,000. Dog bite claims alone average $64,555 according to State Farm data, with nearly one-third of personal injury claims that involve pet incidents.

Medical payments coverage pays $1,000-$5,000 for guest injuries regardless of fault and handles minor accidents without liability claims. This coverage applies when your neighbor’s child breaks an arm after a fall from your tree or a delivery driver slips on icy steps. For additional protection beyond standard limits, consider personal umbrella insurance.

Additional Living Expenses Cover Temporary Displacement

Loss of use coverage pays for hotel bills, restaurant meals, and other extra expenses when covered damage makes your home uninhabitable. Most policies limit this coverage to 20% of your dwelling amount (or $50,000 on a $250,000 policy) and typically cap payments at 12-24 months. This protection activates when fire damage forces you into temporary housing or when burst pipes require extensive repairs that displace your family.

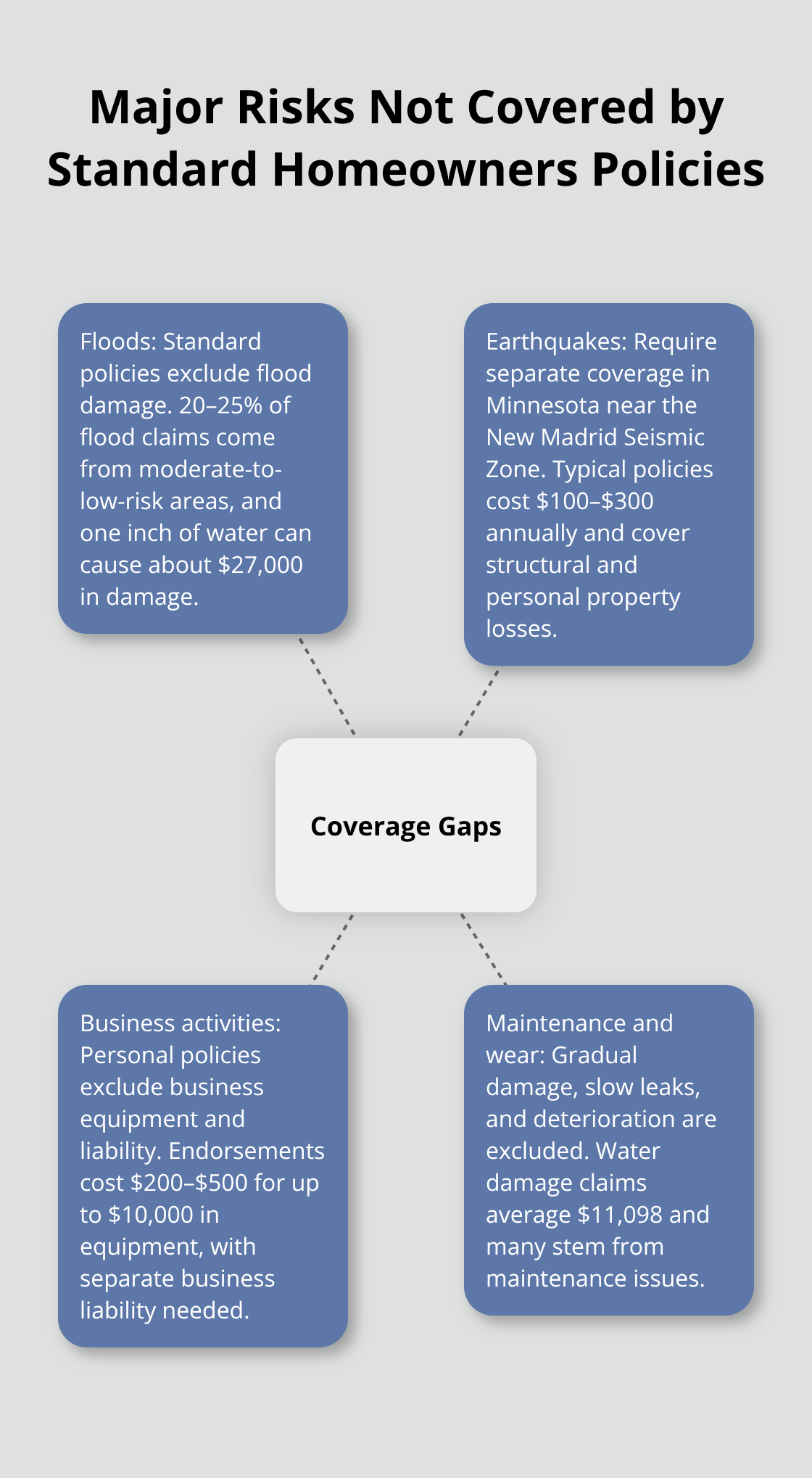

However, standard homeowners policies exclude many common risks that Minnesota residents face, which creates significant coverage gaps that require separate protection.

What Major Risks Aren’t Covered

Natural Disasters Require Separate Protection

Standard homeowners policies exclude flood damage entirely, even though Minnesota experiences significant water damage from spring snowmelt and severe storms. The National Flood Insurance Program reports that 20-25% of flood claims come from moderate-to-low-risk areas, which makes flood insurance essential for all Minnesota homeowners. FEMA data shows that just one inch of water causes average damages of $27,000, while flood insurance costs only $400-$700 annually for most properties.

Earthquake damage also requires separate coverage since Minnesota sits near the New Madrid Seismic Zone. Though earthquakes remain rare, the 1975 Morris earthquake caused $9 million in damages across western Minnesota. Earthquake insurance typically costs $100-$300 annually and covers both structural damage and personal property losses that standard policies exclude.

Business Activities Need Commercial Coverage

Home-based businesses face complete exclusion under personal homeowners policies. Standard policies provide zero coverage for business equipment, inventory, or liability claims related to commercial activities. A photographer’s $15,000 camera equipment damaged in a house fire receives no compensation under homeowners coverage. Business personal property endorsements cost $200-$500 annually and protect equipment up to $10,000, while separate business liability insurance handles customer injury claims.

Professional services like consultants or tutors create liability exposures that personal policies won’t cover. When a client trips during a home consultation, personal liability coverage applies only to social guests, not business visitors.

Maintenance Problems Cost Homeowners Thousands

Homeowners insurance never covers gradual damage from poor maintenance or normal wear. Burst pipes from freezing receive coverage, but slow leaks that cause mold growth over months get denied. The Insurance Information Institute reports that water damage claims average $11,098, yet most stem from maintenance issues that policies exclude. Roof leaks from missing shingles, foundation cracks from settling, and HVAC system failures all require homeowner payment regardless of repair costs (which often reach thousands of dollars).

These exclusions highlight why homeowners need to understand exactly how much coverage they actually need and how to calculate appropriate limits for their specific situation.

How Much Coverage Do You Actually Need

Calculate Your Home’s True Replacement Cost

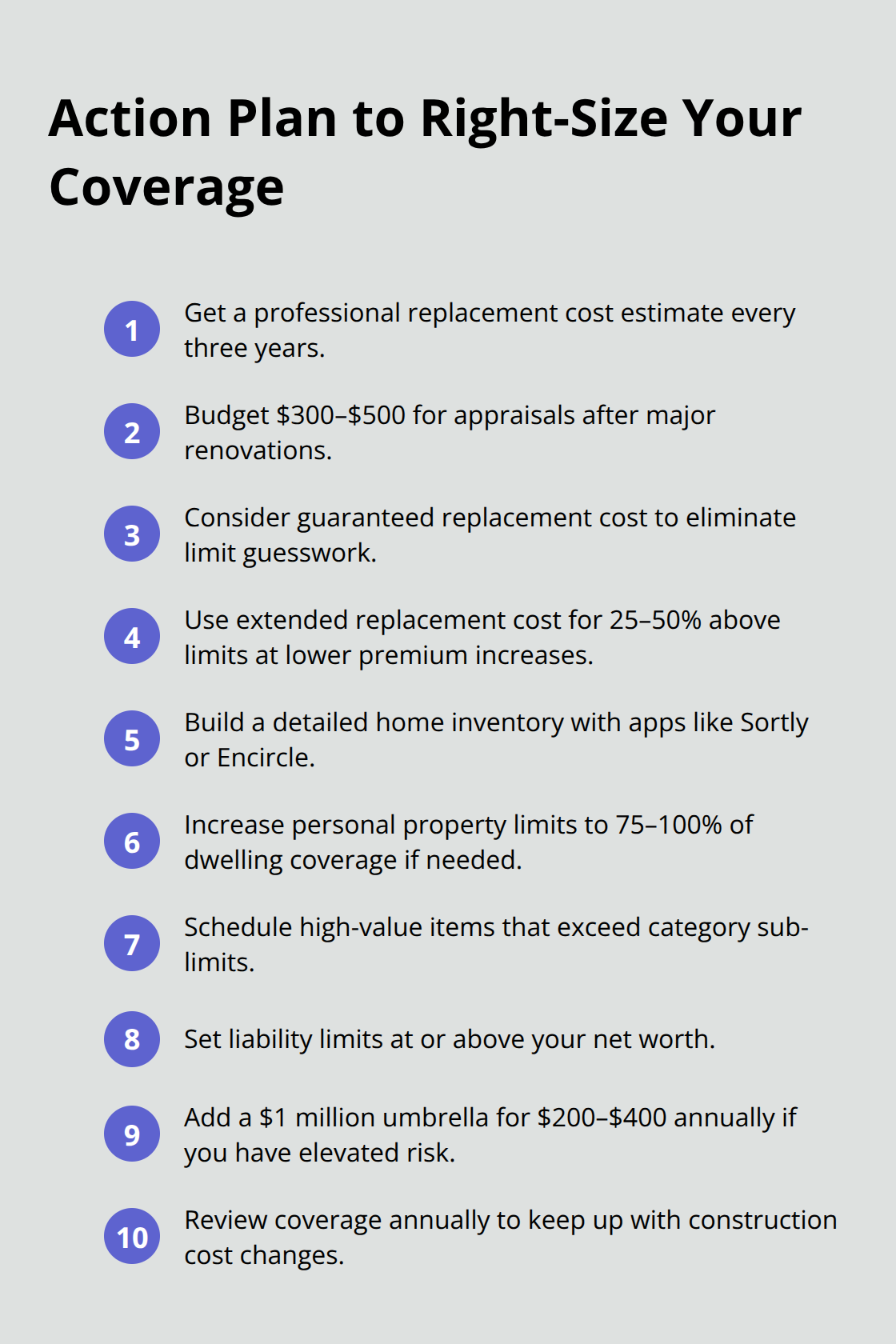

Most Minnesota homeowners underestimate replacement costs by 20-30%, which triggers coinsurance penalties when they file claims. Replacement cost differs significantly from market value since it reflects current construction expenses, not real estate prices. A $250,000 home might require $320,000 to rebuild with today’s material and labor costs. The National Association of Home Builders reports that construction costs accounted for 64.4% of the average price of a new home in 2024, which makes annual replacement cost evaluations essential.

Order a replacement cost estimate from a certified appraiser every three years or after major renovations. These appraisals cost $300-$500 but prevent massive out-of-pocket expenses when total loss claims occur. Guaranteed replacement cost coverage eliminates guesswork and pays full reconstruction costs regardless of policy limits, though premiums increase 15-25% for this protection. Extended replacement cost coverage provides 25-50% above policy limits for inflation protection at lower premium increases.

Set Personal Property Limits Based on Real Inventory

Standard 50-70% personal property coverage often falls short for Minnesota families with valuable possessions. Create a detailed home inventory with smartphone apps like Sortly or Encircle, which photograph and catalog belongings with current replacement values. Most homeowners discover they own $150,000-$200,000 in personal property when they conduct thorough inventories, yet many carry only $100,000 in coverage.

Increase personal property limits to 75-100% of dwelling coverage if your inventory exceeds standard percentages. This upgrade costs $50-$150 annually but prevents significant gaps when total loss claims happen. Schedule high-value items individually once they exceed policy sub-limits. Electronics, jewelry, and collectibles require separate coverage since standard policies cap these categories at $2,500-$5,000 regardless of actual value.

Liability Limits Must Reflect Your Net Worth

Personal liability coverage should equal or exceed your total net worth plus future earnings potential. Minnesota professionals with $500,000 net worth need minimum $500,000 liability coverage, though $1 million provides better protection against severe injury claims. Umbrella policies cost only $200-$400 annually for additional $1 million coverage and activate when underlying homeowners liability limits exhaust.

Consider your specific risk factors when you set liability limits. Pool owners, pet owners, and frequent entertainers face higher exposure and should carry $1-2 million in total liability protection. Teen drivers in the household create additional liability risks that standard coverage amounts won’t adequately address (especially in Minnesota’s harsh winter conditions). Liability coverage equal to twice your net worth provides comprehensive protection against devastating lawsuit judgments.

Final Thoughts

Homeowners insurance protects Minnesota families from devastating financial losses when you understand what homeowners insurance covers and what it excludes. Your policy provides comprehensive protection for dwelling structure, personal property, and liability claims, but floods, earthquakes, business activities, and maintenance issues require separate coverage or personal responsibility. Regular policy reviews prevent coverage gaps that cost homeowners thousands in unexpected expenses.

Construction costs increased 64.4% in 2024, which makes annual replacement cost evaluations essential for adequate protection. Most Minnesota residents underestimate their coverage needs by 20-30%, and this triggers coinsurance penalties when they file claims. Annual reviews help you adjust limits to match current replacement costs and avoid expensive surprises.

We at Variant Insurance Group help Minnesota homeowners find personalized coverage that fits their specific needs and budget. Our experienced professionals review your options and compare protection levels to help you receive appropriate value. We work with multiple carriers to find the right coverage and pricing as your life changes.