Minnesota homeowners face unique insurance challenges, from severe winter storms to summer hail damage. Finding the best homeowners insurance Minnesota offers requires understanding state regulations and local risk factors.

We at Variant Insurance Group know that choosing the right coverage protects your most valuable investment. This guide breaks down everything Minnesota residents need to make informed insurance decisions.

Understanding Minnesota Homeowners Insurance Requirements

State-Specific Coverage Mandates and Regulations

Minnesota homeowners face specific insurance requirements that differ significantly from other states. The Minnesota Department of Commerce regulates all insurance providers that operate in the state, but Minnesota does not legally mandate homeowners insurance coverage. However, mortgage lenders universally require coverage as a loan condition, which makes insurance practically mandatory for most homeowners.

The state requires insurers to offer dwelling coverage that matches your home’s replacement cost, not its market value. This regulation protects homeowners from underinsurance when they rebuild after a total loss. Minnesota also mandates that insurers offer liability coverage that starts at $100,000, though experts strongly recommend higher limits given today’s lawsuit climate.

Common Weather-Related Risks in Minnesota

Minnesota’s brutal weather patterns drive insurance costs well above national averages. The state experiences devastating hailstorms that cause roof damage, with some storms that produce golf ball-sized hail and destroy shingles in minutes. Winter brings ice dams that create water damage, frozen pipes that burst, and heavy snow loads that can collapse roofs.

Tornadoes strike Minnesota regularly, with the state that averages 45 tornadoes annually according to the National Weather Service. These weather risks push Minnesota’s average homeowners insurance premium to $2,920 annually, which represents 38% higher than the national average of $2,110.

Average Insurance Costs Across Different Regions

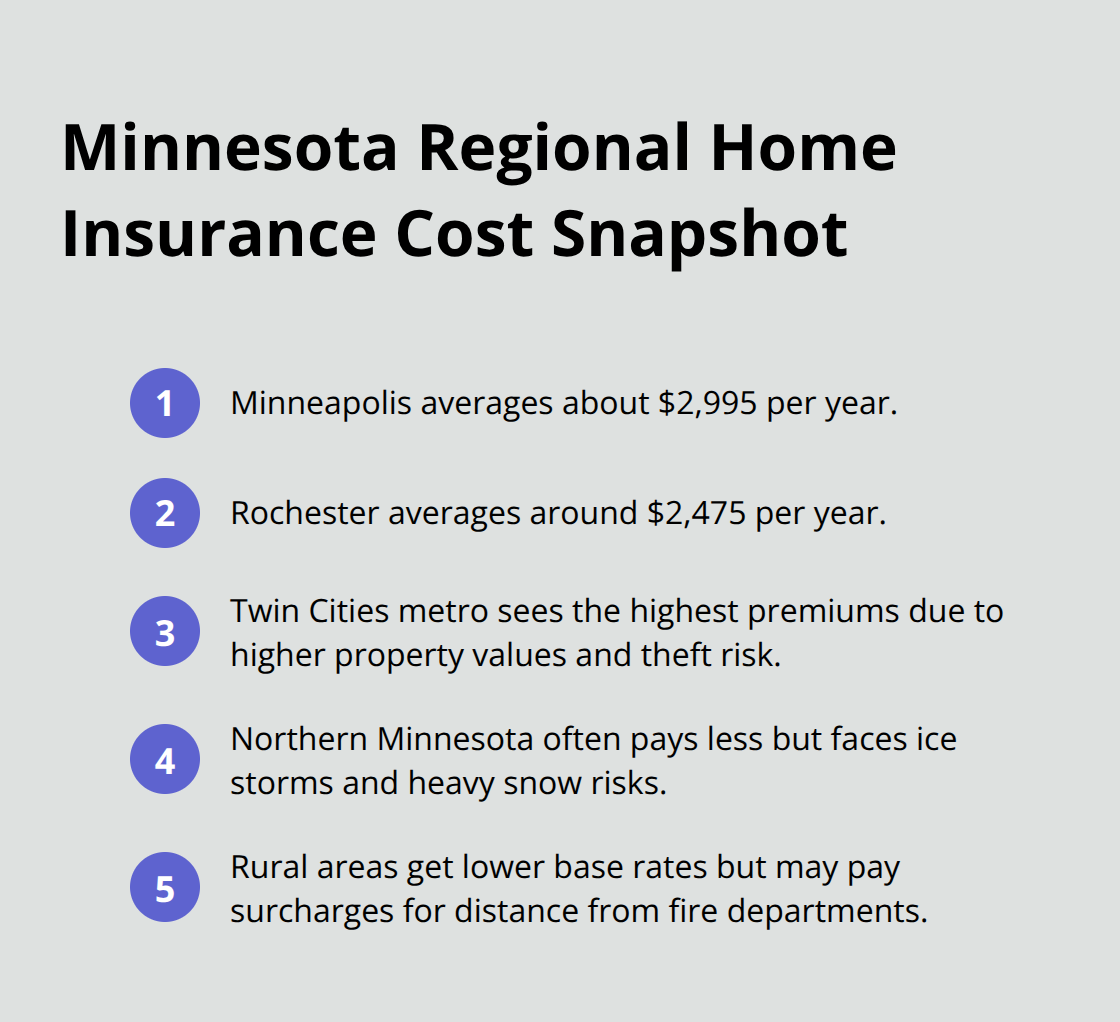

Insurance costs vary dramatically across Minnesota’s regions due to local risk factors. Minneapolis residents pay approximately $2,995 per year, while Rochester homeowners pay around $2,475. The higher costs in Minneapolis reflect increased theft risks and higher property values in urban areas.

Northern Minnesota homeowners typically pay less because of lower crime rates and reduced tornado activity, though they face higher risks from ice storms and heavy snow. The Twin Cities metro area commands the highest premiums due to higher property values, increased theft claims, and greater tornado exposure. Rural areas often see lower base rates but may face surcharges for distance from fire departments.

Minnesota homeowners pay an average of $1,847 annually for homeowners insurance, which sits 15% below the national average. Homeowners with poor credit pay significantly more than those with good credit scores. This credit-based approach affects Minnesota residents more severely than in states that restrict credit assessment for insurance rates.

These cost variations make it essential to understand what factors insurance companies evaluate when they determine your specific premium rates and coverage options.

Key Factors When Shopping for Homeowners Insurance

Coverage Types and Protection Levels

Minnesota homeowners must choose between actual cash value and replacement cost coverage, and this decision directly impacts your financial protection. Replacement cost coverage costs roughly 10% more than actual cash value but pays the full amount to rebuild your home with new materials. Actual cash value subtracts depreciation and leaves you thousands short when you rebuild after a total loss.

Dwelling coverage should equal your home’s reconstruction cost, not its market value. A standard policy with $100,000 in dwelling coverage costs around $1,169 per year in Minnesota, while homes needing $500,000 in coverage pay closer to $3,662 annually. Personal property coverage typically equals 50-70% of dwelling coverage, but Minnesota’s severe weather makes 70% the smarter choice. Liability coverage starts at $100,000, yet personal injury lawsuits regularly exceed $500,000 (making $500,000 the practical minimum).

Deductible Options and Premium Considerations

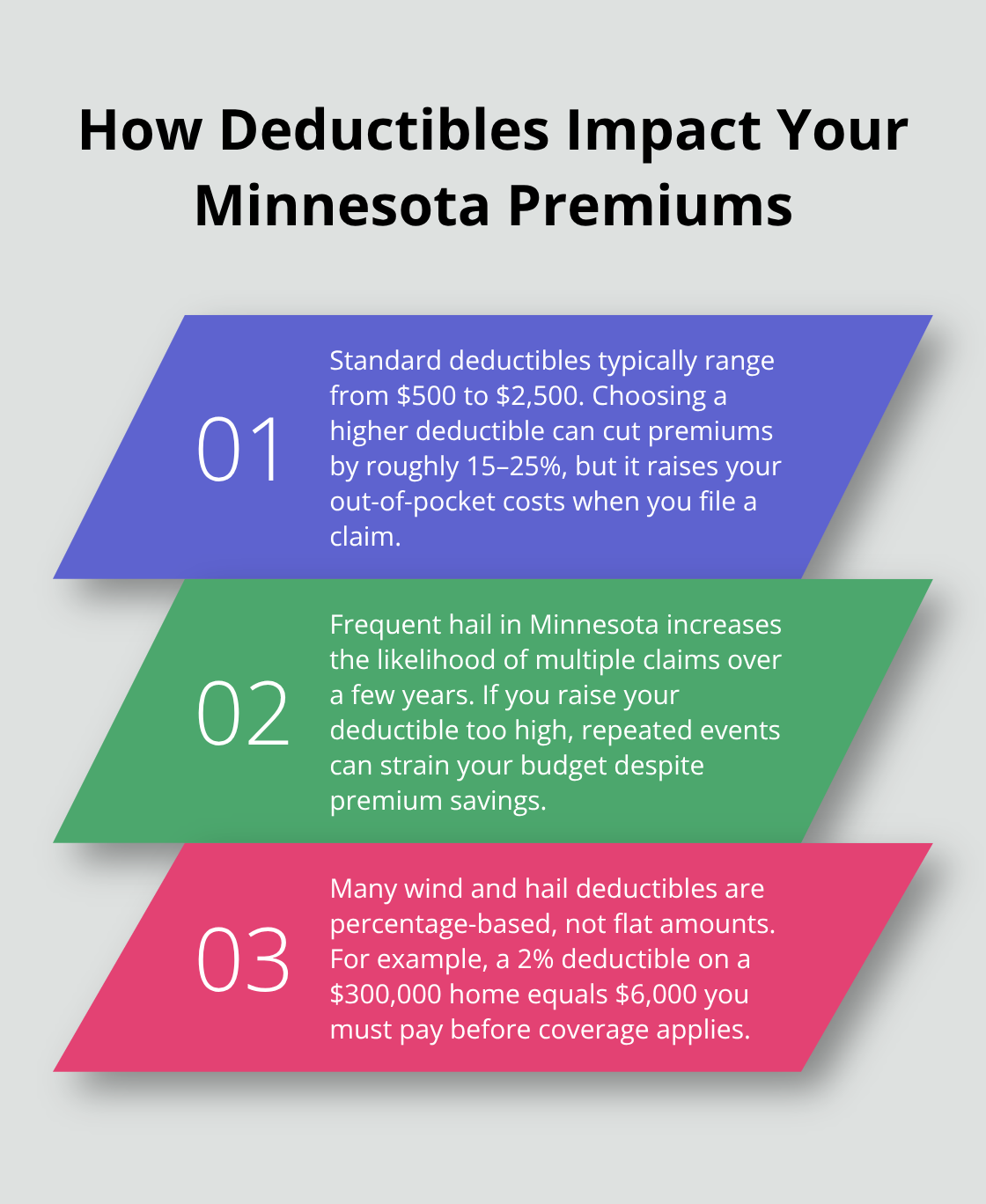

Minnesota homeowners face a critical deductible decision that affects both premiums and out-of-pocket costs during claims. Standard deductibles range from $500 to $2,500, with higher deductibles that reduce premiums by 15-25%. However, Minnesota’s frequent hail damage means you might file multiple claims within a few years.

Wind and hail deductibles often carry percentage-based amounts rather than flat dollar figures. A 2% wind deductible on a $300,000 home means you pay $6,000 before coverage kicks in. State Farm and Farmers typically offer 1% wind deductibles, while some carriers push 3-5% deductibles that create financial hardship during claims.

Insurance Company Financial Strength and Customer Service Ratings

Insurance company financial ratings determine whether your carrier can pay claims during catastrophic events. A.M. Best ratings of A- or higher indicate strong financial stability, while anything below B+ signals potential payment problems. Chubb and USAA received the highest ratings among Minnesota carriers, while some regional carriers struggle with lower ratings.

Customer service ratings from J.D. Power show dramatic differences in claims satisfaction. Amica consistently ranks highest for customer satisfaction with a 4.8 rating, while some major carriers score below 3.0. Claims processing speed varies from 7 days for simple claims to 60+ days for complex cases. Companies with dedicated Minnesota adjusters resolve claims 40% faster than those that use out-of-state teams.

These factors help narrow your choices, but insurance carriers can help you evaluate which specific companies perform best in Minnesota’s competitive insurance market.

Top Homeowners Insurance Companies in Minnesota

State Farm Leads Market Share Despite Mixed Performance

State Farm controls Minnesota’s largest homeowners insurance market share, though their performance reveals significant trade-offs. State Farm charges $2,925 annually for homeowners coverage and maintains a 4.7-star rating, which places them above the state average in cost but delivers solid reliability. Their extensive agent network spans Minnesota and provides local service access, yet their claims processing requires 21-30 days compared to faster competitors. Farmers Insurance provides more competitive rates at approximately $1,900 annually but receives customer satisfaction scores that fall below industry standards in J.D. Power studies.

Regional Carriers Deliver Superior Value

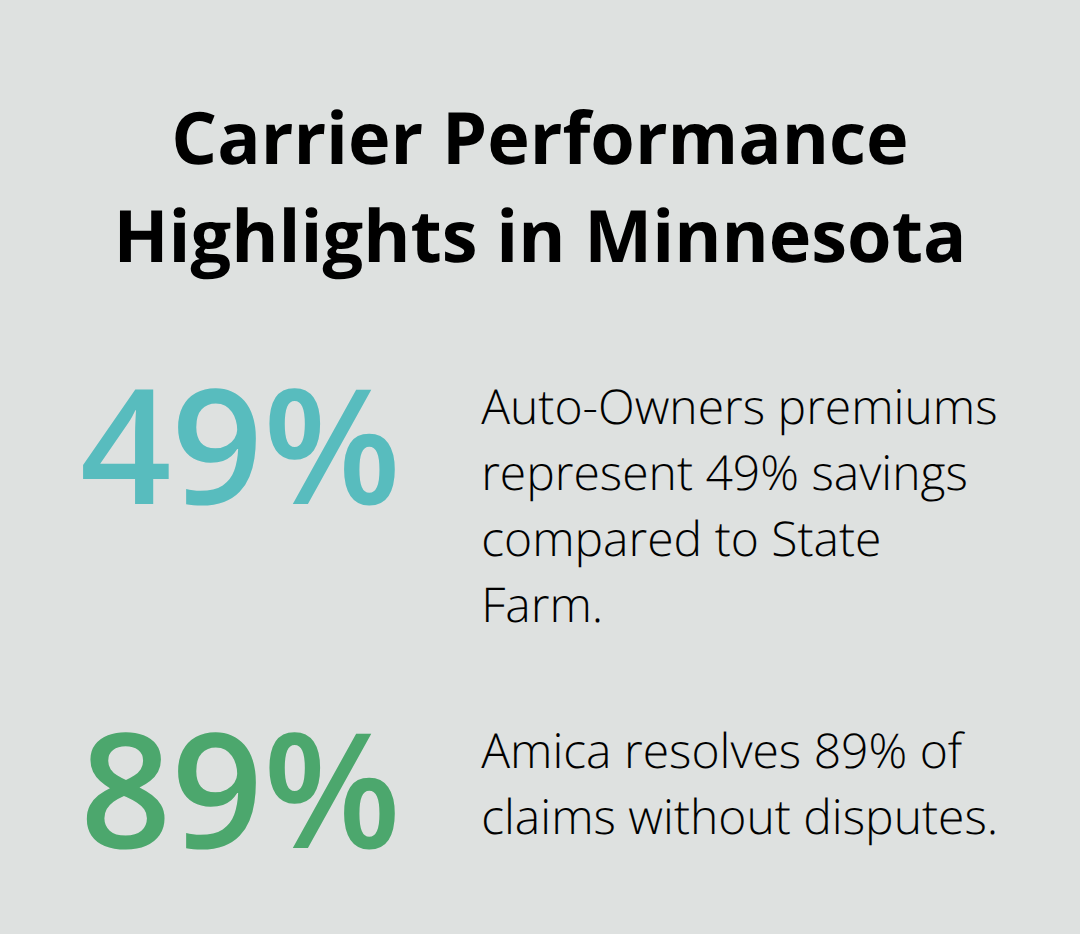

Auto-Owners Insurance consistently offers Minnesota’s lowest premiums at approximately $1,475 annually, which represents 49% savings compared to State Farm. This regional carrier focuses exclusively on Midwest markets and understands Minnesota’s specific weather risks better than national competitors. Amica ranks as Minnesota’s top performer with a 4.8 customer satisfaction score and maintains the lowest complaint index with the National Association of Insurance Commissioners. Their claims processing averages just 12 days, and they resolve 89% of claims without disputes.

Cincinnati Insurance offers unique eco-friendly repair options that use sustainably sourced materials, plus they provide faster claims resolution through dedicated Minnesota adjusters (typically within 14 days).

Customer Service Creates Clear Winners

Claims processing speed varies dramatically among Minnesota carriers, with the fastest companies that resolve standard claims in 7-10 days while slower carriers take 45-60 days. USAA leads in customer satisfaction for military families but restricts membership to active duty personnel and veterans. Chubb provides premium coverage with cash settlements for total losses, though their $2,300 average cost targets affluent homeowners specifically.

The performance gap between top-tier and average carriers becomes most apparent during severe weather events when multiple claims flood the system simultaneously (like after major hailstorms that affect thousands of homes). Minnesota homeowners face challenging market conditions, as insurers lost $190 for every $1.92 collected from homeowners in premiums according to the Insurance Federation of Minnesota.

Final Thoughts

Minnesota homeowners need strategic approaches to secure quality coverage in a challenging insurance market. Start with quotes from at least three carriers, and focus on companies like Auto-Owners and Amica that consistently deliver competitive rates and superior customer service. Compare replacement cost coverage options rather than actual cash value policies, and select deductibles that balance premium savings with your financial capacity during claims.

Independent agents provide significant advantages over direct-to-consumer purchases when you search for the best homeowners insurance Minnesota offers. These agents access multiple carriers simultaneously and understand Minnesota’s specific weather risks and regulatory requirements (plus they negotiate on your behalf during claims). They also provide ongoing policy reviews as your needs change over time.

We at Variant Insurance Group help Minnesota homeowners compare protection levels and pricing across multiple carriers. Our team works to find optimal value and coverage for each client’s unique situation. Schedule annual policy reviews, document your home’s contents with photos, and maintain detailed records of improvements that might qualify for discounts.